the valuation was post split…but he has also mentioned that…even at that valuation…paytm is not a buy and always hold stock….

and certainly not the one which should have a large allocation in ur portfolio…

he believes…paytm is the kinds…which could be 5-8% of ur portfolio at price 2200

Pharm Easy IPO : Sources says PharmEasy is all set to file DRHP for an IPO next week; API Holdings which operates PharmEasy to be listed

Issue size likely to be between Rs 6,000-6,500 cr; valuation expectation of the issue over $7 bn currently

Thank you for this … I am really grateful to you …

Extremely insightful thread on Policy Bazaar IPO.

The level of accounting dressing is superb just to be ready for an IPO. People should note the way the quoting of reports is done as shown by twitter writer. There’s absolutely very little one can do about this apart doing your own research.

Very detailed and useful analysis. VP is an honest platform, and I have benefited a lot because of the content here. I am so grateful to everyone on this forum.

It would be interesting to see which mutual funds buy into this IPO.

Interesting write up and that SEBI seems to be aware of the IPO window dressing roadmap to pump and dump.

Another insightful thread on PayTM’s mega IPO.

Sigachi Industries manufactures, exports, and supplies Microcrystalline Cellulose (or MCC). Microcrystalline has refined wood pulp and chemically inert substances. The company’s output is widely used as an excipient for finished dosages in the pharmaceutical industry.

In India, the microcrystalline cellulose market size is projected to reach $115 million by next year with a 4-year CAGR of 6.3%. Increasing pharmaceutical production, higher demand for processed food and cosmetics, and personal care products are the main driving forces behind the MCC market’s growth. The wider application of MCC in multiple industries is a key factor propelling the global MCC market’s growth. Microcrystalline cellulose is used as an anti-caking agent in beverages, gelling agent, suspending agent, and stabilizer. It is also used as a cold and hot stabilizer, in frozen food, ice cream, and canned meat to extend the product’s shelf life.

It’s a good company, no issue on corporate governance as such, reasonable valuations and best thing is no OFS at all , so money will b entirely going to company and they are planning capex with it.

Future outlook of sectors looks good…

Applied IPO , will buy on Listing if not alloted .

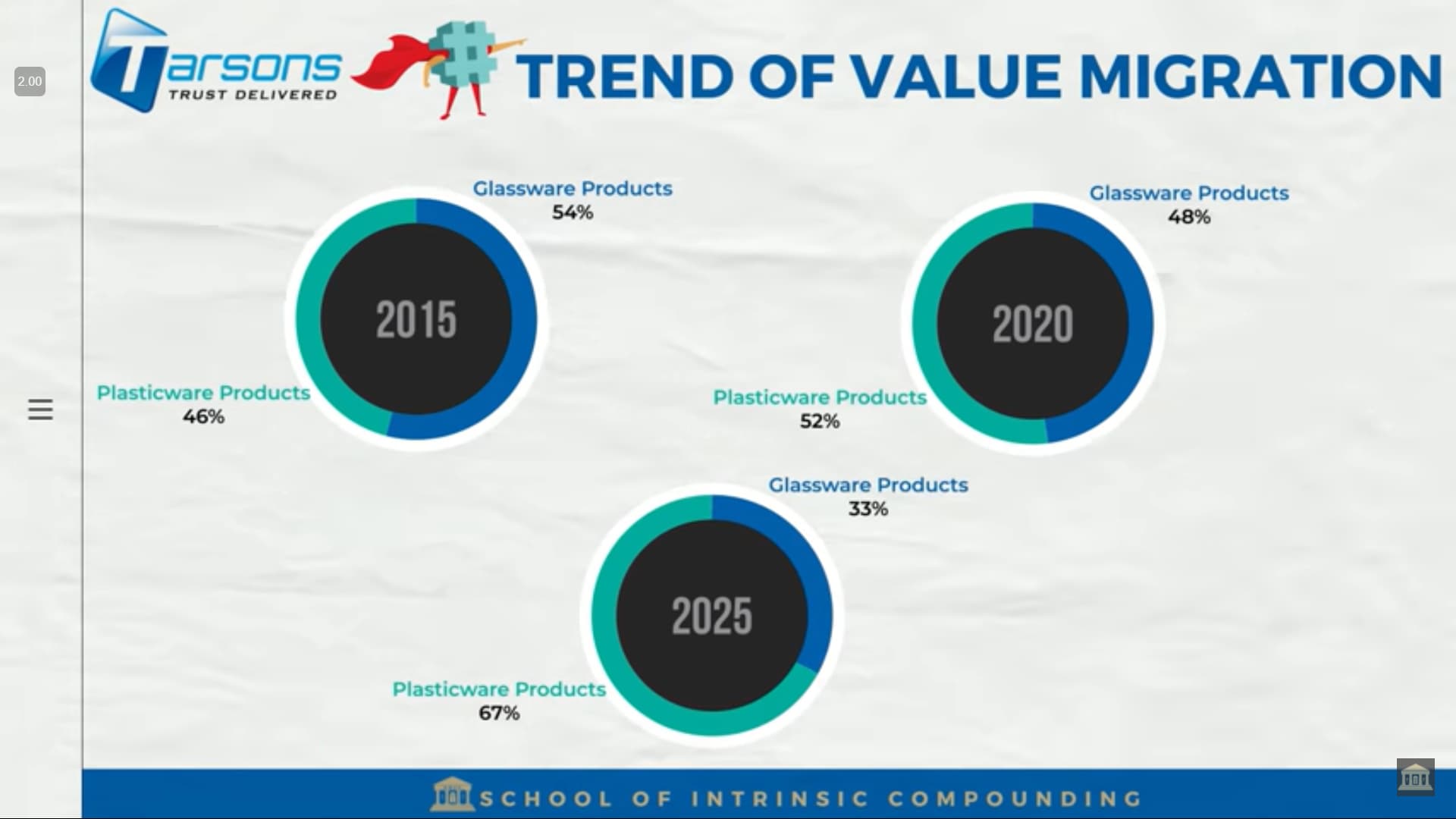

Very insightful analysis by SOIC on Tarsons Products.

From a valuation POV, it is fairly priced at a PE of 40x and the company will be approximately valued at 3500 Cr Mcap.

The lab equipment industry is currently experiencing value migration from glass equipment to plastic equipment as plastic is easier to use and recycle.

Source: SOIC

The Indian plastic equipment industry is expected to grow at 16% CAGR (10.5% CAGR globally) and Tarsons Products can be a direct beneficiary due to the tailwinds in this sector. It can be an interesting bet for the next few years.

Key Risks:-

- Geographical concentration risk (All the plants are in West Bengal. Any adverse event or a natural calamity can impact their operations)

- 75% of raw material is imported and fluctuating prices can dent their margins.

- PE firm holds 49% stake pre-IPO and post IPO holding is around 25%.

- No history of relevant experience of Promoter Group.

Disc:- Not SEBI registered. Still doing research.

25% crash on the listing seems to be a good entry point into paytm, this brings the market cap to $15 billion , when global wallets and payment enablers like square and paypal at 20x market cap and huge runway for growth with new products, new markets and young promoter, is it not a multi bagger in the next decade ?

For Square the last two years the EPS has been positive. Its trading at P/s of 5…

- Square revenue for the quarter ending September 30, 2021 was $3.845B, a 26.73% increase year-over-year.

- Square revenue for the twelve months ending September 30, 2021 was $16.742B, a 118.79% increase year-over-year.

- Square annual revenue for 2020 was $9.498B, a 101.5% increase from 2019.

- Square annual revenue for 2019 was $4.714B, a 42.91% increase from 2018.

- Square annual revenue for 2018 was $3.298B, a 48.95% increase from 2017.

P/s of Paypal is around 10 now. Paypal’s EPS has been positive for last so many years.

- PayPal Holdings revenue for the quarter ending September 30, 2021 was $6.182B, a 13.24% increase year-over-year.

- PayPal Holdings revenue for the twelve months ending September 30, 2021 was $24.569B, a 21.04% increase year-over-year.

- PayPal Holdings annual revenue for 2020 was $21.454B, a 20.72% increase from 2019.

- PayPal Holdings annual revenue for 2019 was $17.772B, a 15.02% increase from 2018.

- PayPal Holdings annual revenue for 2018 was $15.451B, a 18% increase from 2017.

Its not a fair comparison for Paypal & Square with Paytm. Also there is no UPI in USA unlike India. UPI has consumed wallets business. Paytm is not a leader in any of the business they have been into.

Just now heard PayTM CEO defending his valuations post listing/price discovery by market. Prashant Nayar from CNBC was asking all pertinent questions but PayTM CEO was very condescending in his responses and was very defensive. It was comical and tragical at the same time to watch the drama being played out on CNBC. I hope it will send signals to all the startups about what not to do  … It could be a turning point in the history of IPO market in India and it was long overdue considering the grotesque valuations all “new age” businesses.

… It could be a turning point in the history of IPO market in India and it was long overdue considering the grotesque valuations all “new age” businesses.