It has been a regular sight when employees discuss about early Retirement and financial independence. My office is no exception. While we were discussing this Yesterday, we were trying to identify opportunities which would ensure risk free monthly income.

Are there any FDs or bonds or funds with monthly return/dividend on investment? How much is the return and how safe are these investments?

Can rent on properties be safer vehicle investment here?

I thought of seeking fellow VPers input on such avenues considering depth amd breadth of their knowledge. Do advise.

At least I am in the same camp, who believes in early retirement and financial independence. My heart and mind always said there is no point working until the age of 58-60, when the life expectancy is so unpredictable. Then, when are we going to spend time on ourselves or spend at least last few years with family or friends ?

With above thought in mind, I decided to plan my investments accordingly. But I was clueless where to invest for good returns. Then I did some research on various options, particularly FDs and Bonds. Today I am 49 and until last year my most of the investments were in properties and equity. While I continue to hold the properties, I shifted a significant portion of equity profits and liquid money to fixed income options. For me the investment journey of fixed income started at the end of 2022.

In my research, I realized there is no such thing called “risk free”. Its just that some carry high risk and some low. While bank FDs promised 6-8% pre tax returns, a good A/AA rated bonds were giving anywhere between 8-11% pre tax. Of course there are lower rated bonds which offer higher returns, but I was not interested.

As I mentioned there is no such thing called risk free, one may go for traditional govt schemes if you need absolute low risk for your investment, but then returns are not that great. At the end I was okay with some small risk but with a guarantee, so rather going for traditional govt schemes, I opted long tenure FDs (5 years) and Bonds (10 years) which are backed by the state government guarantee. Never put all eggs in one basket applies here as well. So I ensured maximum exposure to each state government is not more than 10lakhs.

So far so good. FDs are giving me 8% and will continue for next 5 years. Bonds are giving me 9-10% and will continue for next 10 years. I am always in search of new bond offerings that are guaranteed by the state government.

Today I am happy that my fixed monthly returns are higher than my monthly expenditure (I am not worried even if I resign from the job ).

The ideal solution for this problem is Annuities, where you make payments for a specified term and get fixed term payouts for life. There are various kinds of annuities and they combine elements of insurance as well (life and death benefits)

A good source to read up is here

Be careful about tax implications, the accumulation phase have wide ranging GST components.

The other option is a Systematic Withdrawal Plan with a Mutual Fund where you ride the risk but withdraw with a fixed frequency. Most MFs offer this option. Good news is that withdrawal is treated as Cap Gains so tax impact could be minimised. You do run the risks of investing.

Using FDs with quarterly interest etc is risky if you expect a fixed income and tax inefficient (with TDS deductions). Further it may not be beating inflation post tax . So income / purchasing power can vary and the retiree takes the investment risk on herself.

One tax efficient Systematic Withdrawal Plan (SWP) strategy is to PLAN:

Invest a decent amount say 20L + in HDFC Corporate Bond Fund - Direct Plan - Growth or a similar option, available in the market,

Do nothing with the above investment & wait for 3 Years, in between use Fixed deposit route, where TDS gets applicable.

After 3Y, start SWP as per your requirement, say total expenditure is 30K per month, start two SWP, 15K in first week of month & 15K in the last week of the month.

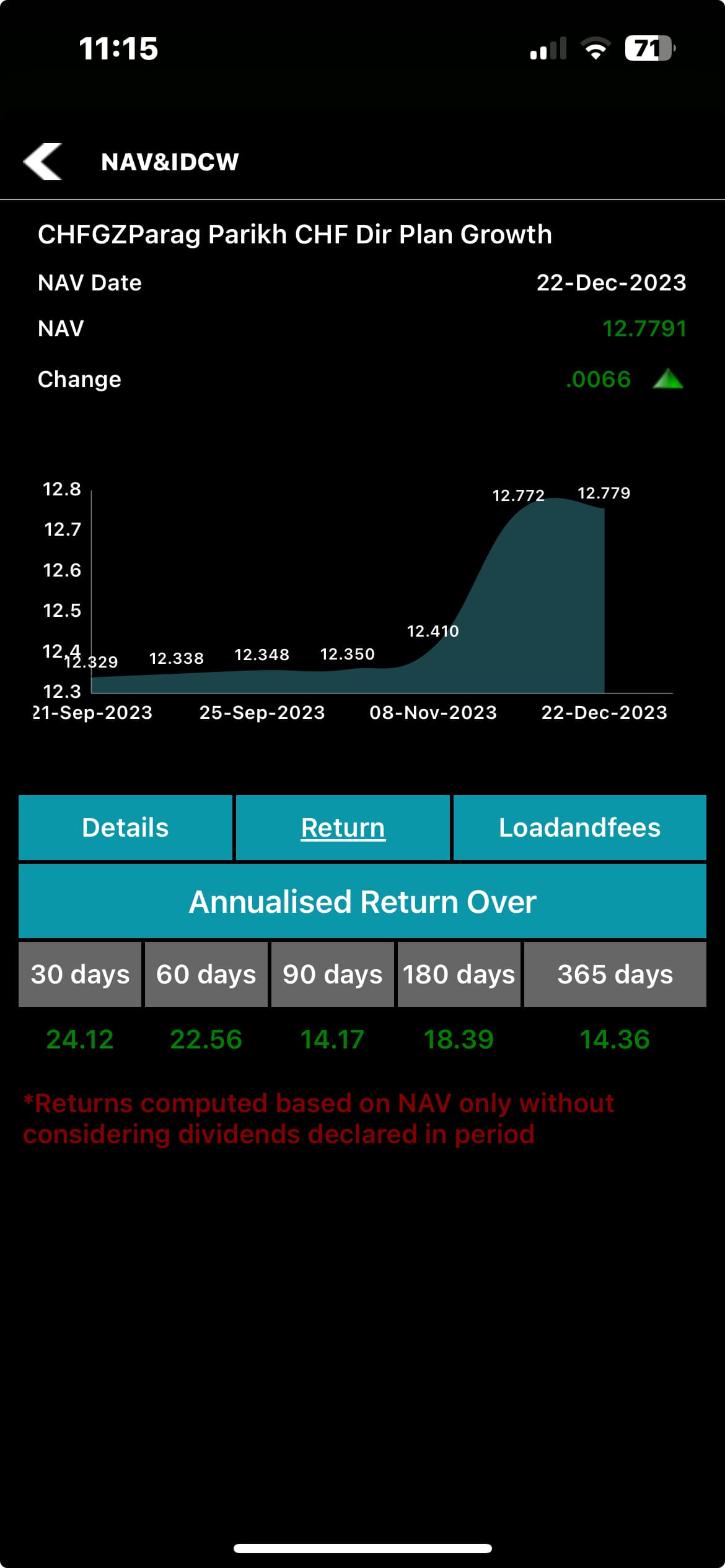

IMO investment in PPFAS Conservative Hybrid Fund (CHF) is a good option. It was launched in May 2021 and since then it has given a return of about 10%. They are investing about 75% in Govt Bonds, 10 to 25% in equity with high dividend yield and about 0 to 10% in REITs and INVITs. There are Chances of delivering 2 to 3% higher than FDs . After 3 to 4 years one can go for a SWP . Sharing the annual performance of the fund.