REC result…

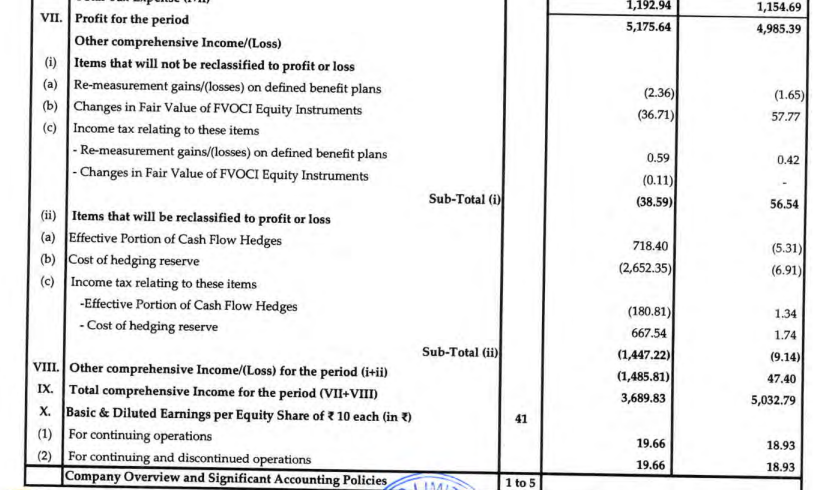

Can anyone explain what are the items mentioned at VII (ii) a,b and c…How come H1 fy 22 EPS is 18.93 when profit was 5032 crore and this H1 EPS 19.66 for a profit of 3689 crore (whereas bonus shaeres also have been issued this quarter)??

2 Likes

I am tracking a few commodities companies and EBITDA per ton keeps getting mentioned in the con calls. Can anyone pls help me understand the term and way to calculate it?

1 Like

How does one determine whether the management of the company is reliable to invest in the stock ?

I believe one could be matching their expectations (regarding profit , revenue etc.) with reality of what happened.

What are some other factors to take account of ?

1 Like

This is a qualitative aspect, so I am not sure if there are ways to reach a precise conclusion, although with regards to the business what they are saying can be quantifiable, like growth, margins etc.

One can look at interviews, conference calls and watch, listen to the management talk. One can understand and get the tone of management from them talking instead of reading about what they said, not that it is reliable, but it gives an idea.

Few questions like unlisted companies doing the same business as the listed business, appointing family members in key positions without them having sufficient qualification or experience, what they do in a particular situation - delayed orders (Mayur), no clarity regarding succession, CEO etc (Cupid), increasing remuneration despite having other options (Avanti), unrelated purchases (Venky’s), frequent auditor changes, RPT, interested about their stock price (Parag I think), poor/nil communication etc.

Few trustworthy points are dividend payout, buybacks, no key persons resigning, good capital allocation, transparency in communication, regular conference calls etc. One can even go by valuations - market trusts the management (Dmart).

These all are subjective and debatable, but gives a vague idea at the least.

The proof out of the pudding is obviously in the eating, and as investors belong to different groups, some stay for long term despite the business not performing for extended periods of time due to their trust, some may think of opportunity cost, some don’t find other opportunities so stay, it depends.

Just my thoughts.

6 Likes

Hi,

Does anybody know how to download private company financials from the MCA website? I have registered (As a registered user) but whenever I click on View Public Documents and try to add selected documents to Cart for purchase, the website asks me to login again at this screen - Ministry Of Corporate Affairs - MCA Services

I already have a registered account but it looks like that a/c can’t be used to download public documents? On the above login page I can’t even see an option to register (And my existing login/password does not work).

I have been using Tofler for accessing private documents, but they really charge a lot more than MCA I think (MCA charges Rs 100/company vs Tofler Rs 300).

Any help will be much appreciated ![]()

1 Like

You can try this. Charges might be slightly less or similar.

It’s a business opportunity for such intermediaries to provide documents from MCA and charge slightly higher. So don’t think it would be any less.

The below one is quite expensive but is a good option: -

https://www.zaubacorp.com/

1 Like

I don’t follow much, but from what little I know, when TV channels report such QoQ news, I guess this is to bring some cheer or excitement, particularly for the trader community and not to investors, or to entice new people to participate in the market.

Although a few stocks can rise and fall, whose story is done and dusted in a year, in 4 quarters, there exists a lot of stocks whose businesses are years old, sometimes decades old, where investors have been present for much longer periods than a typical short term trader, or even a positional trader. So for these long term investors folk, a few quarters is nothing, as they follow the story, and are not easily excited or deterred by quarters’ performance.

On the other hand, if I am new and I happen to see a TV channel or some other publication, where some excellent numbers of stocks are provided, I might get interested, and I might participate in them without knowing anything. Attracted to numbers, so to speak.

Of course, there exists some stocks, I cannot recollect them by name, that a lot of hype or optimism is built so quickly that, for a few quarters the stocks rise with no limit, and also fall rapidly. These stocks are not necessarily pump and dump stocks, but genuine businesses with unexpected huge tailwinds, which are temporary or not yet matured in nature, but prices go upwards very fast. Also, if the story is indeed true, there is a chance that if one waits, one could miss a good opportunity.

Even what I have said is generalized, and each stock should be looked in confluence of many factors, and looked at independently too.

Just some thoughts and some inferences.

4 Likes

Definitely.

For example, clothing, fashion etc companies do well in Q2 & Q3 as these are festive seasons; specially after November, sells pick up due to marriages season.

If you take a look at Redington, their Q3 numbers have been better than other quarters, as people also buy electronics during Diwali and all.

Though I do not follow, it could be interesting to compare numbers of beverages companies during different seasons. (I feel there should be more sells in summer).

2 Likes

Another example of the same.

1 Like

hope this help!

3 Likes

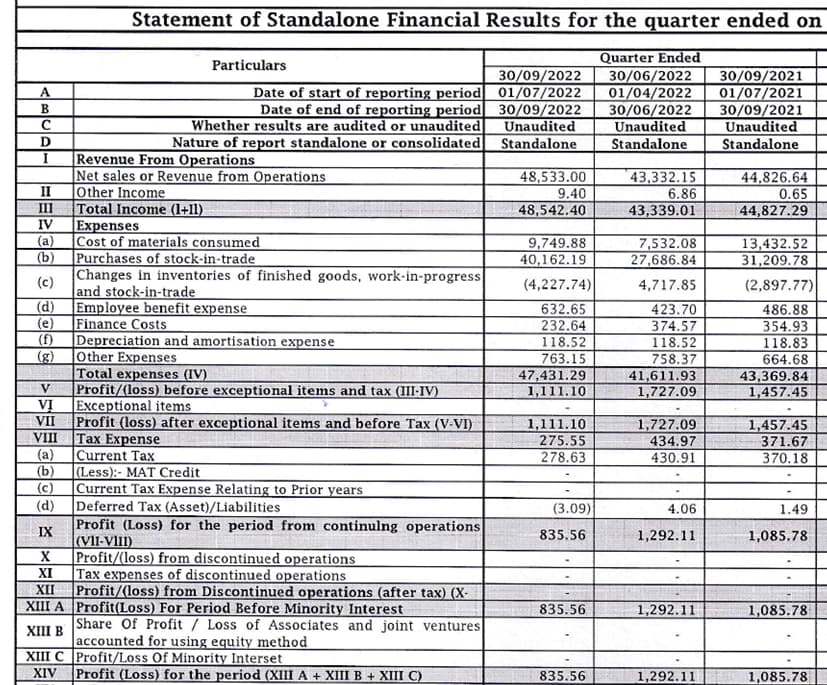

Query regarding Purchase of stock-in-trade

I am not an accounting expert so get confused at times because of accounting treatments. Please find below a snapshot of a jeweler retail company for Q2 FY23.

The sales have increased slightly YoY, but profit has decreased from Rs 10.8 crs to Rs 8.3 crs YoY for Q2 FY 23.

On looking at expenses, there is considerable increase in Purchases of stock-in-trade (Rs 401 crs vs Rs 312 crs YoY).

Queries:

-

Is this purchase of stock-in-trade basically unsold inventory of finished products of last quarter and carried forward to this quarter?

-

Is purchase of stock-in-trade not same as inventory?

-

If there is considerable increase in purchase of stock-in-trade then does it mean that the management expects higher sales and hence have increased the stocks?

-

Since stock is increased this time then does it mean that there will be comparatively less expenses in next quarter and hence more / increase in profits?

-

How is purchase of stock-in-trade different from finished goods?

-

Any reason why management opted to buy such high purchase of stock in trade? If they had less purchase of stock in trade then there would have been more profits.

1 Like

Here is my understanding, which shall answer all the above questions:

- Purchases of stock-in-trade: Includes cost spent to procure ready goods that are traded by the company.

- Inventory: Includes all the elements of in-house manufactured goods - Raw Materials, WIP, channel stock (stock-in-trade), and Finished goods.

P.S: No accounting expert. Just another DIY investor.

4 Likes

Haven’t previously participated in any merger. There are two mergers upcoming on my portfolio: HDFC-HDFC Bank and LTI-Mindtree.

Lets talk about HDFC-HDFC Bank. Here holders of 25 shares of HDFC will be allotted 42 shares of HDFC Bank. This means that 3 shares of HDFC Bank is equivalent to 1.786 shares of HDFC. So, if someone has 2 shares of HDFC, he will get 3 shares of HDFC Bank, and will get cash worth 0.214 part share of HDFC in his registered bank…

Is the above understanding correct?

1 Like

In the case of bonus shares for VBL, value of the fractional share has been credited to the bank.

Fractional entitlement(s) arising out of the allotment of above-mentioned Bonus Equity shares were consolidated and allotted to “Varun Beverages Limited - Bonus Issue Fractional Shares Trust” (“Trust”) created for the purpose of selling and distributing the net sale proceeds (after adjusting the cost, expense and applicable TDS for Non-Resident Members) of consolidated fractional Bonus Equity Shares among the eligible Members in proportion to their respective fractional entitlement.

Consequent to the sale of above-mentioned consolidated fractional Bonus Equity Shares by Trust, your entitled net sale proceeds have been transferred through online mode of payment in your bank account.

1 Like

Thanks Chaitanya. Same happened in my case with Bonus shares. So, I guess same will happen in merger case also.

Actually @keeyes was telling similar thing in Mindtree thread yesterday.

Probably yes, as fractional shares irrespective of the nature of their creation, be it merger or bonus, cannot be credited to demat accounts, hence value of the fractional share will be calculated and credited.

1 Like

@Surender bhai thank you for your kind reply.

So is “purchase of stock in trade” a P&L item or Balance Sheet?

Meaning, if it is P&L item then all stocks of Rs 401 crs would be utilized (sold) during the quarter. And if it’s a Balance Sheet item then stocks worth Rs 401 would be outstanding and available to be sold at the end of quarter.

So is stock of Rs 401 crs already sold? or is it lying in stores waiting to be sold?

@Patel_Bhai

PnL item. Expenses booked in the reported Qtr.

Hi- Any idea how to get a list of companies (using the exchange’s/screener’s website) that are listed for 12+ Years in the Indian equity market?

I am sure the consistent compounders of the order which you have mentioned grow. Past history tells that. However, when the PSU shares double and Bajaj Finance malingers, you are annoyed. I don’t regret selling either HDFC Bank or Bajaj Finance. I would rather take a risk and buy companies which have not yet caught the market fancy.

2 Likes