another source is https://www.researchbytes.com/SectorEventList.aspx

1 Like

Hi VKP,

Previous years are also available, please go to https://www.stockadda.com/concalls and type the company name, all available data from the repository would be shown.

You too can share concalls/reports/presentations etc on the site.

rgds

1 Like

Hello sir… I want to know how to check promoter share plugging… and wah5 is the impact of it.

In many websites ROCE and ROE is available but couldnt find ROIC. Can anyone suggest website that has ROIC ? Thanks in advance

ROIC is not a very popular ratio, so you won’t find it readily in most websites. Screener.in has it thought as “return on invested capital”. Screener also gives you the feature to add your own custom ratios.

1 Like

Thanks so much @basumallick dada

Hi fellow investors, first-time poster here.

I would like to know how do you determine whether a business is working capital intensive or not?

Also how would you determine how much money gets stuck in working capital requirements?

Thanks.

1 Like

You can basically look at the inverse of working capital turnover ratio. Or just calculate the working capital / net sales to understand how much working capital is needed to generate the sales.

3 Likes

Generally, a WCap/Sales of 10% or below indicates a business that has Working Capital under control. Of course, a negative Working Capital is the best thing to have.

But then like most Ratios, it’s relative to the industry. For many B2B firms, Working Capital is a necessity. So “high” or “low” here would depend on the industry average itself.

1 Like

The company I am studying Jamna Auto which has over 70% market share in the leaf spring market. It is one of the world’s largest manufacturers and no Co. in India comes close to its scale. Its WCap/Sales has been in the low single digits(I take WCap as Receivable+inventory-payable) with cash conversion cycle being negative in 8 of the last 10 years.

With peers of no real significance, I want to evaluate whether current working capital is efficiently managed and if there is scope for further improvement

Also, what are the effects of improving cash conversion cycle on the income statement?

An improvement in Working Capital cycle puts more money in the hands of the company. So that leads to higher turnovers and thus Sales. Otherwise, a long history of low / negative Working Capital indicates Pricing Power with Suppliers/Distributors and/or Customers. That’s indicative of a good moat.

2 Likes

But the Co.'s gross margins have not improved, and over the past 5 years it has incurred CAPEX of 400cr but gross block has not changed. Am I right in thinking that the Co. is in a fixed capital intensive business that needs such CAPEX just to maintain its position?

Given these facts how to analyze why the Co. has such a dominant market share?

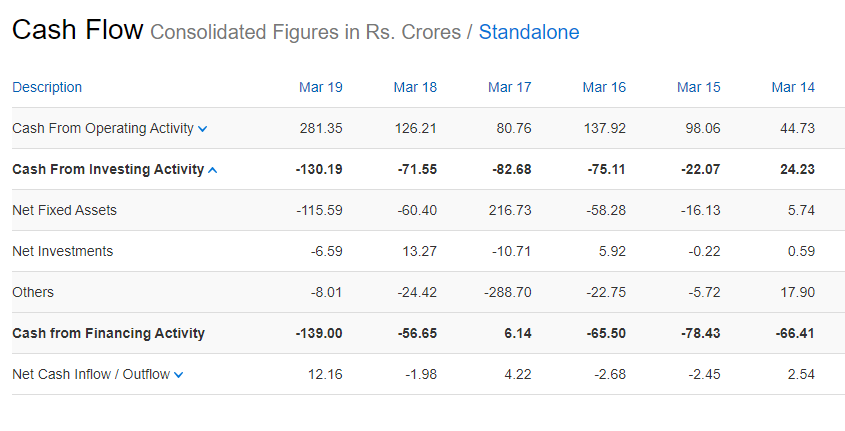

In RateStar, I can see that over the last 5 years, their Cash outflows due to purchasing Fixed Assets has been close to -27 Crs and the change in Gross Block has been about 24 Crs. There are usually small mismatches like this in websites like Screener / RateStar. The Annual Reports for the past 5 years should give you the complete picture.

Also, Working Capital, Margins and ‘Capex’ (Related to Capital Turnover) are different parts of the business. Market Share is in the past. The future depends upon how the business will evolve in the future (And consequently, the figures mentioned above). This understanding only comes after a thorough analysis of the company.

Do visit VP’s Jamna Industries thread to get a better understanding:

These figures are as per AR. Does this mean the assets that this Co. holds needs constant replacement/upgradation?

If Promoter holding is Zero…who owns and runs the company?

Ex…Redington (India)

It means that the company does not have a designated promoter and is run by a professional board.

2 Likes

You don’t need a promoter to run a company. The management & board runs the company. It’s actually better for minority shareholders like us if there is no promoter.

1 Like

Actually, in most cases, you are better off having a promoter. Lot of studies have been done globally on this and data suggests promoter-operators are the best for long term value creation. Primarily because they have skin in the game. A professional board by nature tends to have a short term mindset. Of course there are notable exceptions to this. In India, L&T and ITC are major board driven companies but both had the good fortune of having very strong leadership for a very long period in Naik and Deveshwar.

6 Likes

The problem we have faced with promoters is that they act in their own self interest rather than that of the minority shareholders. They mostly screw the minority shareholder. We have seen this time & again.

Proper long term growth based incentives would make the CEO & the board have skin in the game.

How would they go about and cause problems for the Minority shareholder? Can you elucidate a bit more on that? Personally, I think that having a promoter is good for a small to mid-cap company because those kinds of companies just can’t afford to have a professional board at this point in time. Please feel free to correct me if I may be wrong in some cases.