As for Mirza international in 2022, total debt is 77 crore. But in pnl statement, i observe that their interest expense is 26 crore. It is a massive interest cost of almost 35%. is it a true picture ? or i am wrong. please explain @harshitgoel @ayushmit

I am not sure if I am right, but I think Mirza Intl. reported “total principal payments” as “interest expenses”.

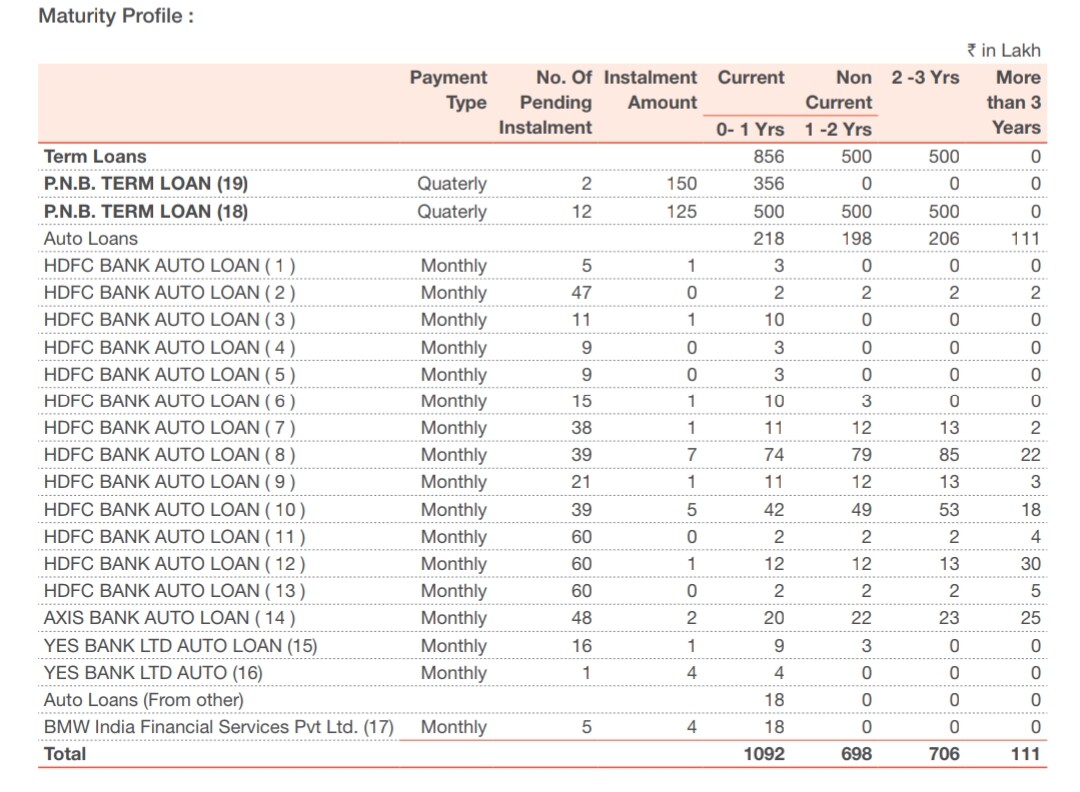

Have a look at the above maturity profile for all debt repayments. When you total all up, it comes out to be Rs. 2,607 lakhs.

The finance cost is Rs. 2,698 lakhs and interest income from cash is Rs. 96 lakhs (taken from cash flow statement), which means the interest expenses comes out to be Rs. 2,602 lakhs. (Pretty close to 2,607 lakhs though).

I don’t know. I might be wrong! This is just an analogy.

3 Likes

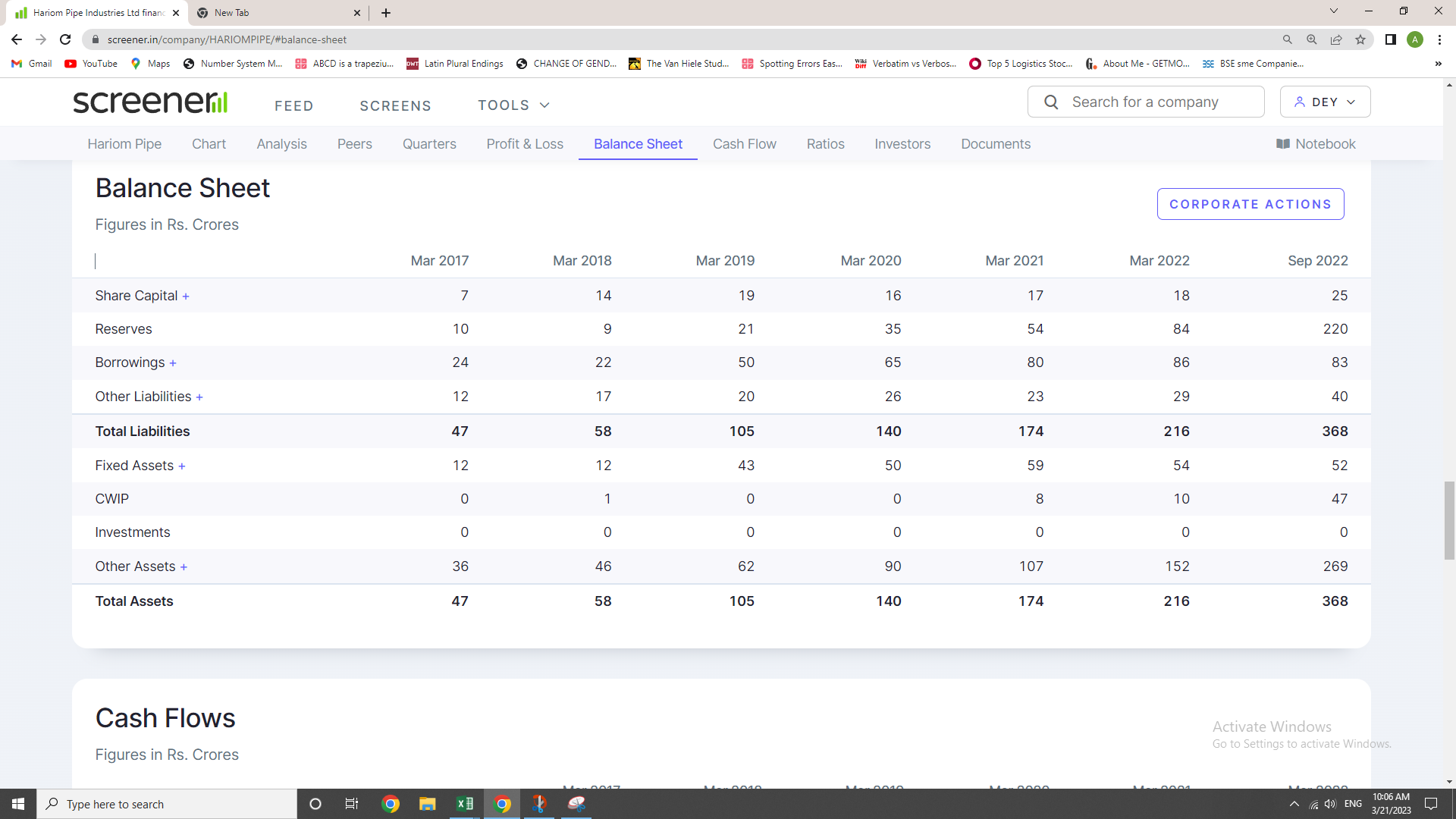

how does company’s reserve increases? lets see the screen shot. in hariom pipe reserve was 84 in 2022. in september it is increased to 220 . what is added to reserve? what is the calculation?

This company IPO’d in April 2022. The increase in reserves is due to the share premium earned via the issuance of new shares to the public markets.

Every share has a face value and a market value. When new shares are issued at market value, the face value component goes and sits in the share capital part of the balance sheet and the excess of market value over face value sits in the share premium account which is part of what you see as Reserves.

E.g. FV = 10, Market value = 100, assume 100 new shares issued at market price. Therefore 1000 (10100) will be added to the Share Capital part of B/S and 9000 (90100) will be added to reserves.

Google to understand more about Share Capital and reserves and read balance sheets in detail. Each element of share capital and reserves are broken down there.

2 Likes

is dividend a sign of good corporate governance? i observe that most of the outstanding companies has been giving dividend to the shareholders for a long time. It is true that there are few companies which have given good performance despite having not distrubuted a dividend in past. But the number is few. can i keep it a criteria for screening purpose?

This is a vast topic, not as simple as it sounds, and there are completely different schools of thought and very different points of view here, each having merit.

Certain businesses need capital for business growth or even for their operations, they don’t pay dividends, example Dmart. Some businesses need less capital, so while they keep some aside, they distribute a good portion of their profits to investors, cash rich companies from FMCG and IT. Some businesses may not grow beyond a point for any reason for a particular period, so they may announce a dividend instead of keeping cash, and some businesses while done with their capex for a period of time, may start giving dividends for the first time or may increase the payout. And PSUs give good dividend, one cited reason is government itself owns major stake in the company.

Investors who have bought such high dividend stocks a couple of decades ago, with stock splits and bonuses, even if the price has not moved, they have made good profits with dividends.

Dividend investing can still be a concept to look at, but not from a growth and share price appreciation perspective, but as it is, and acknowledging the fact that it could turn out to be an opportunity cost.

I have some positions in dividend companies, not yet came to the decision of increasing their positions.

On a side note, a psychological one, while the price appreciation is real mathematically, it is still notional, as the shares are not sold, but a credited dividend is absolute, so I guess it makes all happy, just like as it does me.

1 Like

- one small cap company (200 cr mcap) is growing at 20 % cagr in profit and trading at pe of 20

- another company having market cap of more than 15000 cr is growing at 20% cagr in profit and trading at pe of 20

which company should i invest in, assuming other fundmental conditions remains same for both? please guide

These type of questions are good in presentations, not here, even if the 2 companies are in the same business, because I don’t think such numbers without the mentioning of names of the companies don’t provide the full picture. So if indeed there exist such companies which are you are looking at, give the names and knowledgeable members may have some insights which can provide a new perspective and change your thesis.

On another note, full numbers do provide a fundamental sense of understanding, Screener’s page tells us a lot of things.

i want to understand the basic idea regarding this . some times i face such kinds of dialemma while choosing a company.

PE is subjective, and is not exact. Different sectors have different PEs, and some companies are valued more than others in the same sector. So in a way, your question is related to valuation, which is subjective. One can be proved wrong either way, high PE may continue for some more time after our purchase, or may revert to mean quickly, or low PE may remain low for some more time.

So it is better to look at all the metrics available to value, rather than single metric.

Adding to what other bros mentioned, I would start with what is the business of the company and what is driving the growth. What is oTotal

Addressable market to understand how far the company can grow?

Valuation is the last step in my humble opinion and has to be seen in relation to the sector (other companies in the same business).

Hope it helps

1 Like

Please refer the below post, it may help you to understand and decide:

2 Likes

PEG ratio, kind of answers this question.

Let’s suppose the historical profit growth is also expected in the future (assuming no dilution) too i.e. 20%. PE ratio is 20. PEG ratio comes out to be 1 for both companies

Given that, one is a 200cr company and other is 15,000 cr. Taking all else constant, I would choose 15,000 cr company (using a proxy that bigger mcap firms are safer bets).

Note: This is for academic purposes. Don’t invest based on a single metric.

2 Likes

I want to calculate my returns in excel using XIRR format.

Currently, I am just listing down cashflows and dates and using the xirr formula… so this way I have my returns since inception.

Now, I want to calculate returns for periods like 3m, 6m, 1y, 2y etc…to be able to compare to benchmark indices…

What is the data set that should be included in this calculation ?

- stock A in purchased in June 2022 and sold in Mar 2023. In which all data sets will the cashflows from this stock included ?

- Stock B is purchase in in Jan 2022 and sold in Mar 2023. In which all data sets will the cashflows from this stock included ?

So for eg - for 1y return period, only stocks that are BOUGHT and SOLD within 1Y period should be included or only the ones that are SOLD within that 1Y period.

Sorry, if this question looks quite naive…

TIA

All stocks and all transactions should be included to calculate the portfolio return. You will need the portfolio value for the two dates for which you want to calculate the returns, say for 31st March of last year and 31st March of current year (if you want to calculate this year’s return). Then you have to enter the starting date portfolio value as an outflow and ending date portfolio value as an inflow and all the buy / sell transactions in between. Add all the dividends received as well. That will give you your portfolio performance for the year.

1 Like

I am reading P&L of Barbeque-Nation Hospitality Ltd

| 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|

| FINANCE COSTS | 536 | 564 | 756 | 848.68 | 653.03 |

| Interest expense on: | |||||

| Borrowings | 98 | 173 | 161 | 222.51 | 44.98 |

| Provision for asset retirement obligations | 4 | 4 | 3 | 4.37 | 5.26 |

| Interest on lease liabilities | 394 | 481 | 341 | 499.23 | 508.03 |

| Gross obligation | 23 | 44 | 44.25 | ||

| Others | 1 | 0 | 20 | 20.00 | 0.01 |

| Receivable discounting charges | 54 | 157 | 10 | 25.55 | 54.26 |

| Other bank charges | 13 | 17 | 11 | 32.77 | 40.49 |

Bit confused with Fiancé cost mentioned in the P&L has above component.

I have few query

- Interest on lease liabilities is mentioned in this and another expanse has Rent paid — When company already pay rent what is this expanse under finance cost?

- Receivable discounting charges – what expanse is this? this number is very close to the asset company hold in balance sheer that particular year.

Warrants

How can one learn more about expiry and exercise price of a warrant? I couldn’t find any info from NSE/BSE websites.

For example, Share India Warrant with the scrip name SHAREINWARR. I couldn’t find the expiry date. Exercise price is also not easy to find. We can only guess from company filings.

Thanks for any help.

Good day

Can some please guide how rights entitlement works. I have received some shares of Som Distilleries in my demat and wish to know what happens if i apply and if I don’t.

Thanks and regards

I am studying a company and wanted to run a few things with others and see what your thoughts are:

- How do you rate managements that pay themselves or their relatives rent money? I understand renting for leases isnt a big deal. And paid to management itself is also fine as long as that helps the business.

But how about rents paid to farm houses owned by family members for hosting an AGM?

- This is a tricky one in my opinion

How do you rate managements who own 75% of stocks and gives dividends every Q while business needs cash and business needs are catered through debts?

With the company in question I am observing 8-9cr of dividend payout and 12cr debt for Capex.

Would love to hear what others think of such managements

1 Like

Hi all, majority of my portfolio around 70% are in mutual funds. I want to know how do you select an equity mutual fund for long term investment? what parameters do you check ?