@Apurva_Dubey : In hindsight, finding reasons is a no brainer ![]()

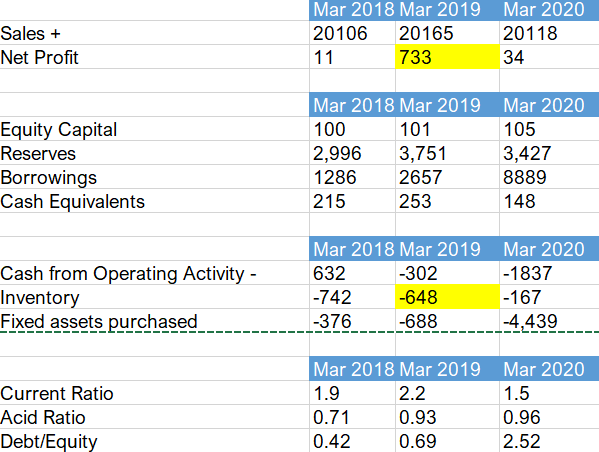

Good question as this needs a view on all the 3 statements. Just on the face of FY19 balance sheet, nothing stands out as ‘Killer’ items.

‘END’ values of the standard ratios -Current Ratio (2.2), Acid Ratio(0.93) and total debt to equity ratio (0.69) - look reasonable, both absolutely as well as relatively. But, upcoming deterioration of these ratios could be inferred as soon as one shifts focus to ‘MEANS’ leveraged to manage these ratios.

On the Income statement, 90% of the net profit (733 Cr.) is the result of Inventory buildup/gain (648 Cr.). Also, Sales growth in FY19 is NIL.

What’s the point?

- The above lever increased the total equity by that much amount. Consequently, the total debt to equity ratio did NOT slide to 0.84 from 0.69 …

Well Managed !!! - Above action sucked away 60% of the ‘Cash from Operating Activity’ …

Super Harmful !!!

Let’s do some Pre-mortem at the end of FY19:

FY20 starts → Business is a going concern. → Cash is needed to support expenses, working capital and growth/capex. → To raise funds, borrowing or diluting equity are the only options. → Ratios would have no choice but to deteriorate.

Business did both:

| Mar 2018 | Mar 2019 | Mar 2020 | |

|---|---|---|---|

| Proceeds from shares | 148 | 1 | 1,266 |

| Proceeds from borrowings | 0 | 1,329 | 5,999 |

‘Cash from Operating Activity’ worsened in FY20. Beside standard ratios, I look at another ratio that ties PnL with Cash Flow Statement:

| Mar 2018 | Mar 2019 | Mar 2020 | |

|---|---|---|---|

| Interest Coverage Ratio: Interest Expense/Free Op. Cash Flow | 0.68 | -0.23 | -0.07 |

Note:

- Never studied this business.

- Above narrative is based on numbers shown on our beloved

screener - I might be drawing bulls eye around my inferences.