I am mentioning my accounting notes for Avanti Feeds:

CFO has been ~80% of net profits (over the last decade). For argumentation sake, lets consider the management is overstating accrual profits. This can be verified by looking at whether cash taxes match accrual taxes. Cash taxes over the last decade is ~680 cr. whereas accrual taxes is ~674 cr. A company which is faking profits will not pay taxes over the fake profits. Tax rate as a % of PBT comes ~33% which is fair. This removes my doubt over cash flow conversion

Another thing to look at is what happened to the cash generated over the last decade.

CFO ~ 1035 cr.

Dividend ~ 232 cr. (22%)

Debt + interest repayment ~ 80 cr.

CAPEX (approximately equal to fixed asset purchased) ~ 340 cr.

For the list of liquid investments, please look at the FY19 AR.

Listed NCD ~ 66 cr. (these include HDB Financial Services Ltd Sr A/O(Ml)/1 Br NCD, Mahindra And Mahindra Financial Services Ltd As2018 BR NCD & Tata Capital Financial Services Ltd Sr Tr A 2018-19 Tr I BR NCD)

Debt mutual funds ~ 472 cr. (none of the debt funds look like a problem, look at Pg: 128-129 of FY19 AR)

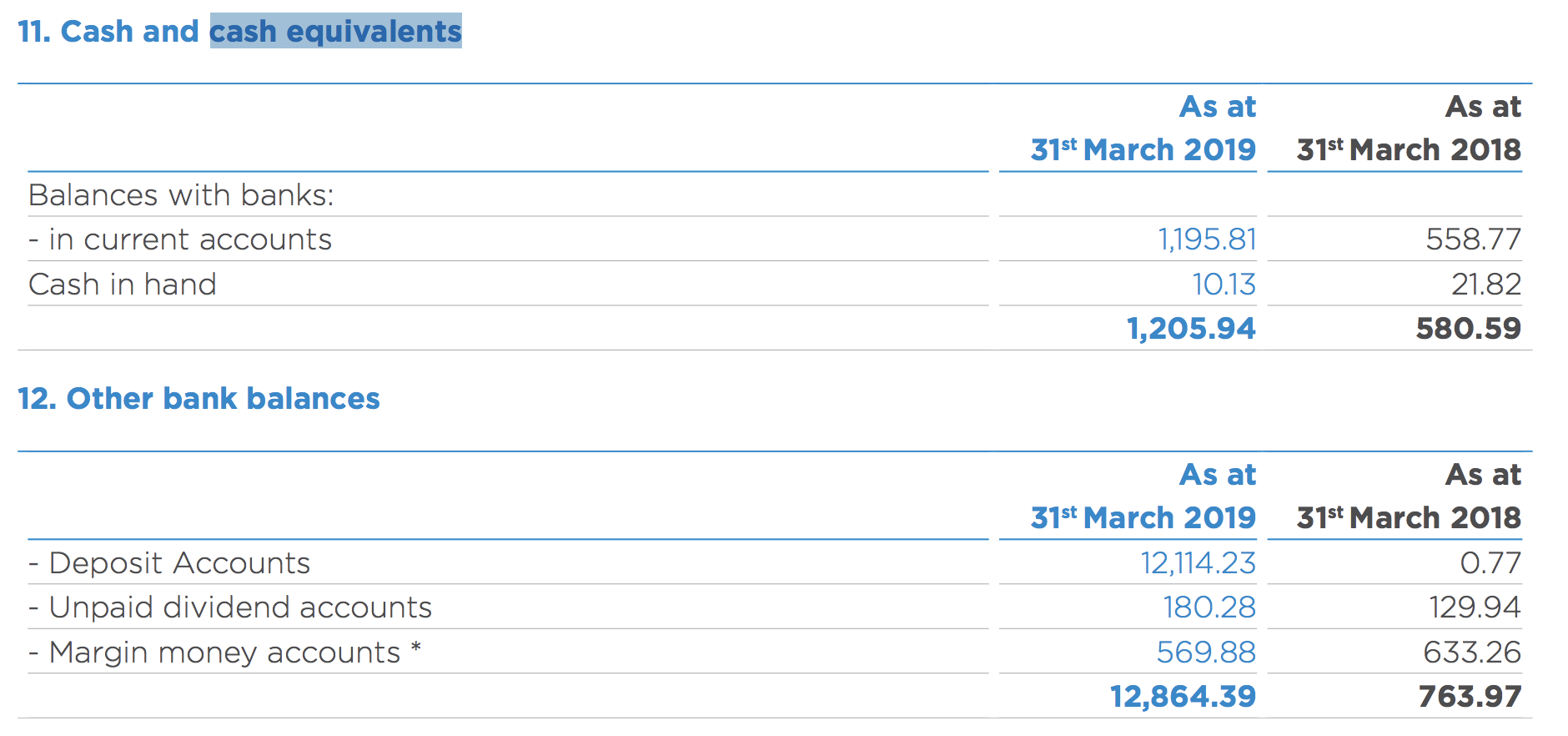

Cash in bank ~ 130 cr. (look at image below)

In essence, they have ~670 cr. of liquid investments in bonds + debt funds + cash. So the profits generated over the last few years have made the company a net cash balance sheet.

Key monitorables

- CFO/EBITDA has always been low (at ~50%).

This is something which I haven’t been able to fully understand. I have let this pass because inventory, debtors & working capital have gone up in-line with growth in revenue (not every year, but on average). Plus they have been able to convert profits into cash in bank. So, its unlikely that there is financial shenanigan going on over here.