Dont know what kind of stocks your looking for here.But you should add a line for promoter holding.

A subsidiary cannot be seperately traded since people who own the parent stock automatically hold rights over the subsidiary.Hence a subsidiary cannot have seperate floating shares.

Dont look at a single year’s CFO or FCF ,you should look at average of multiple years.If the average fcf is negative over a few years,it is a negative as the company seems unable to sustain it’s operations without having to invest in infrastructure.

2 Likes

No I was asking that can we get the physical copy of annual report of the subsidiary also?

I do not know of any such company which makes a seperate annual report for it’s subsidiary.

In general the company may not even reveal the financials of it’s subsidiaries if they are not substantial in terms of assets.If they are substantial it may only hand out a minimal version.

If it has then it must give a soft copy.BTW which company are you talking about.

I am analysing some of the Growth Mid and Small Cap companies. I am seeing for a good number of the companies Operating Cash Flow is less than Net Profit. I am illustrating some of them below:

- Avanti Feeds: 7 out of 10 times in the past 10 years.

- Bharat Rasayan: 4 out of 10 times in the past 10 years.

- AIA Engineering: 8 out of 10 times in the past 10 years.

- NESCO: 4 out of 5 times in the past 10 years.

- VIP Industries: 6 out of 10 times in the past 10 years.

- Vinati Organics: 7 out of 10 times in the past 10 years.

If i sum the total for 10 years, even then total CFO < Net Profit. This is a breach of a financial Shenanigan.

Is this leading to the Equity Dilution for some of the above companies (Avanti, Bharat Rasayan)?

A lot of experienced and knowledgeble investors in this forum are invested in some of these companies. Can you help me understanding?

1 Like

I am mentioning my accounting notes for Avanti Feeds:

CFO has been ~80% of net profits (over the last decade). For argumentation sake, lets consider the management is overstating accrual profits. This can be verified by looking at whether cash taxes match accrual taxes. Cash taxes over the last decade is ~680 cr. whereas accrual taxes is ~674 cr. A company which is faking profits will not pay taxes over the fake profits. Tax rate as a % of PBT comes ~33% which is fair. This removes my doubt over cash flow conversion

Another thing to look at is what happened to the cash generated over the last decade.

CFO ~ 1035 cr.

Dividend ~ 232 cr. (22%)

Debt + interest repayment ~ 80 cr.

CAPEX (approximately equal to fixed asset purchased) ~ 340 cr.

For the list of liquid investments, please look at the FY19 AR.

Listed NCD ~ 66 cr. (these include HDB Financial Services Ltd Sr A/O(Ml)/1 Br NCD, Mahindra And Mahindra Financial Services Ltd As2018 BR NCD & Tata Capital Financial Services Ltd Sr Tr A 2018-19 Tr I BR NCD)

Debt mutual funds ~ 472 cr. (none of the debt funds look like a problem, look at Pg: 128-129 of FY19 AR)

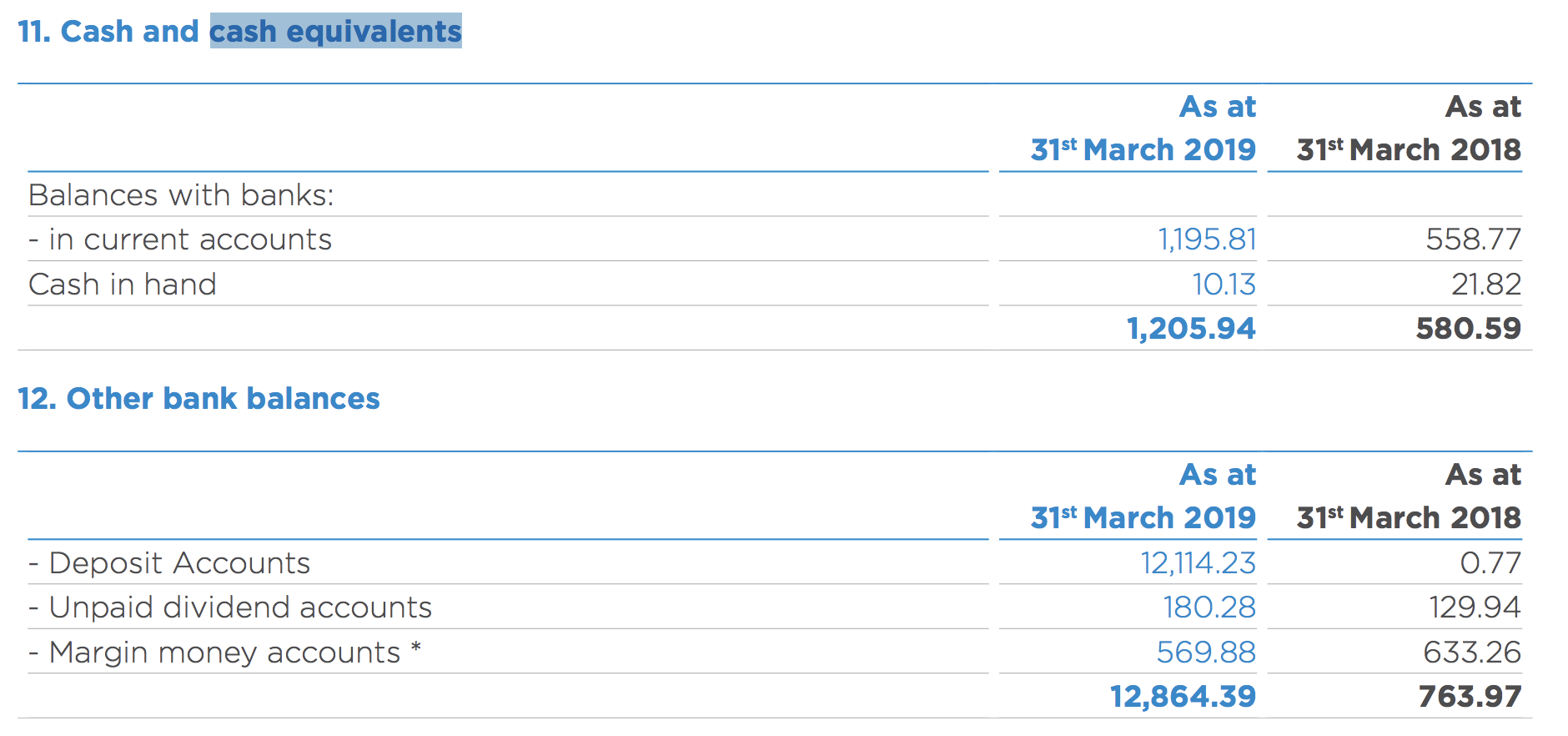

Cash in bank ~ 130 cr. (look at image below)

In essence, they have ~670 cr. of liquid investments in bonds + debt funds + cash. So the profits generated over the last few years have made the company a net cash balance sheet.

Key monitorables

- CFO/EBITDA has always been low (at ~50%).

This is something which I haven’t been able to fully understand. I have let this pass because inventory, debtors & working capital have gone up in-line with growth in revenue (not every year, but on average). Plus they have been able to convert profits into cash in bank. So, its unlikely that there is financial shenanigan going on over here.

10 Likes

Recently I was thinking about the cash and cash equivalents section in balance sheets. How can one verify it?. Companies can always claim X amount in a few random debt funds and some amount in current account. In fact the same concern for the tax paid in P&L. So ideally dividend is the only thing that cant be fake.

Of course we all know what happened in Satyam.

PS: This is not related to avanti or any company. But a general concern. Wanted to know if we can cross check anything to verify

One can look at other income as a % of investment. If it is around risk free rate and goes in-line with changes in investments, its a low-likelihood event that the cash is fake. Bajaj auto comes to mind, they always generate close to risk free rate on their cash equivalents. Other than that, we have to trust the auditors and independent directors & diversify at a portfolio level.

3 Likes

I get your point. But they can fake that too right?. I mean just calculate the other income accordingly and state it. ( I think, in satyam they forgot to do this. Not smart enough). Also, this is for current account/FD etc. What about debt fund investments?. They can just just mention some Mark to Market value. So I am wondering how one can verify all these?

2 Likes

A note from a credit rating agency also includes details about cash & cash equivalents. For a rating withdrawal, credit rating agencies need to have a NOC issued directly by the bank. But I don’t know if they check cash & working capital limits directly with the bank.

In the broader context, we can always get trapped by a maverick. In general, I have noticed that there are more red-signs visible in companies with significant financial shenanigans. However, in my opinion there is no full proof method.

1 Like

So ,you are saying that the credit agencies need to get a NOC (no defaults) to issue a rating ?Also doesn’t the accountant check the certificates for liquid investments like mutual funds,fds,shares etc.I mean most companies invest in a lot of mutual funds if they have cash,often more than 10 MFs.They wont produce a fake certificate for each one of them every year ,can they?

Generally if the company is paying good taxes,which are about 33 percent of the PBT and good dividend payout(about 15-20 percent of PAT) and you can verify some other expenses etc like duties or marketing expenses like whether there are tv ads etc,the company is in the safe zone.You can also check whether their inventories/receivables change proportionately with revenues(subject to a margin of error and other income considerations that were just mentioned above.But it better to diversify at the portfolio level in order to avoid any bizarre shenanigans.

Rating agencies need a NOC if a rating is to be withdrawn, however I don’t know if they also need a certificate when a rating is issued.

Reinvestment of Earnings.

Each year a good stock generates cash, which is given as dividends or re invested in the business or Buybacks.

If one were to measure how much cash has been reinvested, how would one go about?

This can be done by taking the delta in earnings from one year to other and delta in capital invested ( or for longer period… say 3/5/7/10 years)…

Capital Invested, is there such a heading in BS?

you can calculate it the similar way you calculate the ROIC. [ Working Capital + Net Block ] or Equity + Long term Debt - Cash… you just have to use the delta for ROIIC.

2 Likes

Hi,

My question pertains to arbitrage funds - a few fund managers have begun dissuading clients from buying their arbitrage funds given the bear market scenario claiming the ‘negative carry’ doesn’t offer arbitrage opportunities.

However, one AMC declared that even so, they are able to find ‘reverse arbitrage’ opportunities in the present market, and hence their arbitrage funds will still offer similar returns as in the past.

From your earlier explanation, I find that selling presently in the cash market and simultaneously buying futures amounts to a reverse arbitrage transaction. Please clarify:

a. To carry out a reverse arbitrage transaction, does 1 need to be holding quantities of the stock/asset in question, given that it is being shorted in the cash market?

b. If the answer to the above is yes, does this not limit the reverse arbitraging opportunities available to the fund?

c. If the answer to a) is no, can reverse arbitrage transactions be carried out endlessly so long as such opportunities present themselves?

d. Lastly, would you recommend parking funds temporarily in arbitrage funds (out of one’s fixed income allocation, or funds being parked until they’re deployed towards equities)?

Many thanks in advance,

Vishal

Reverse arbitrage is not allowed as MFs are not allowed to short sell shares

2 Likes