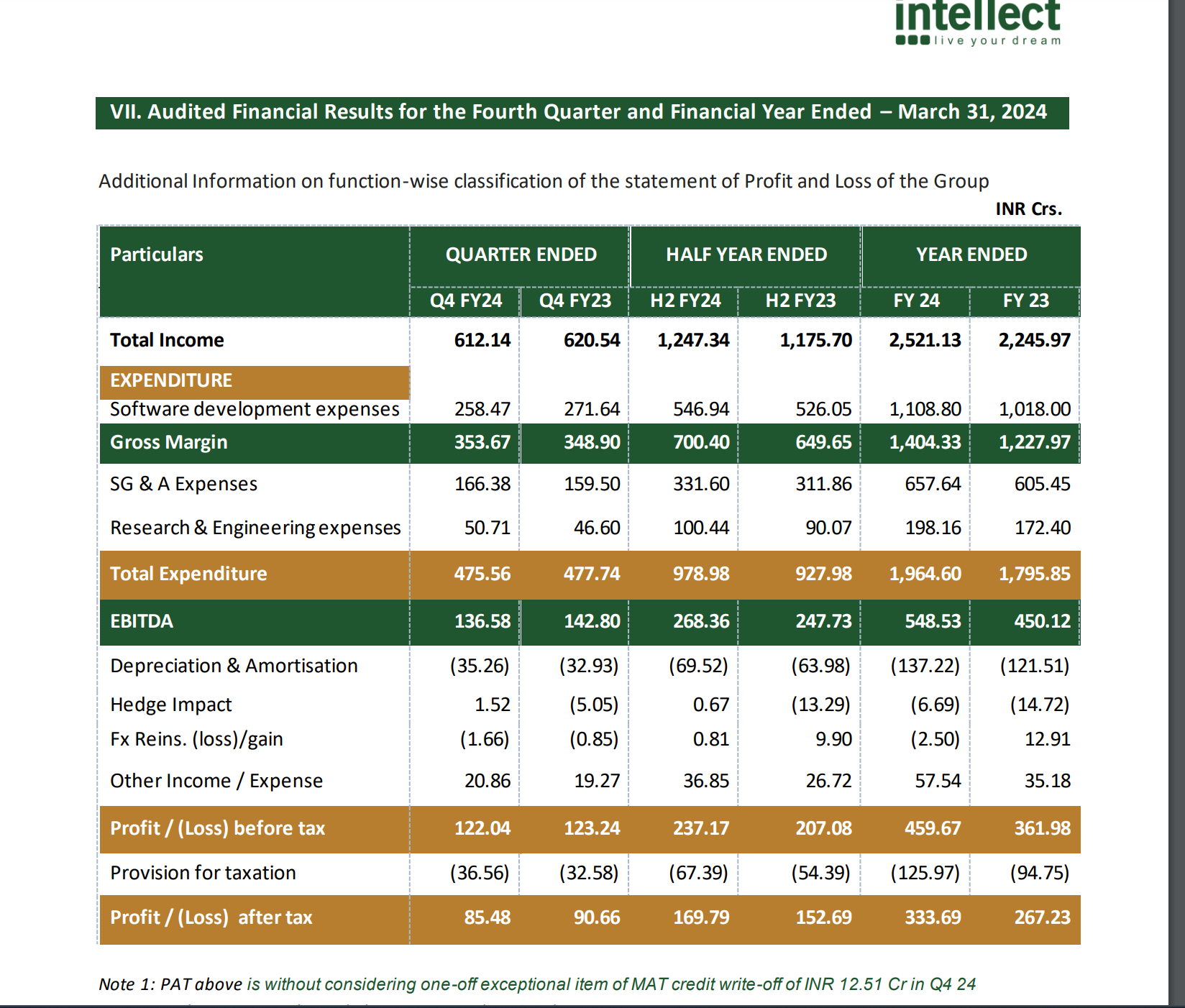

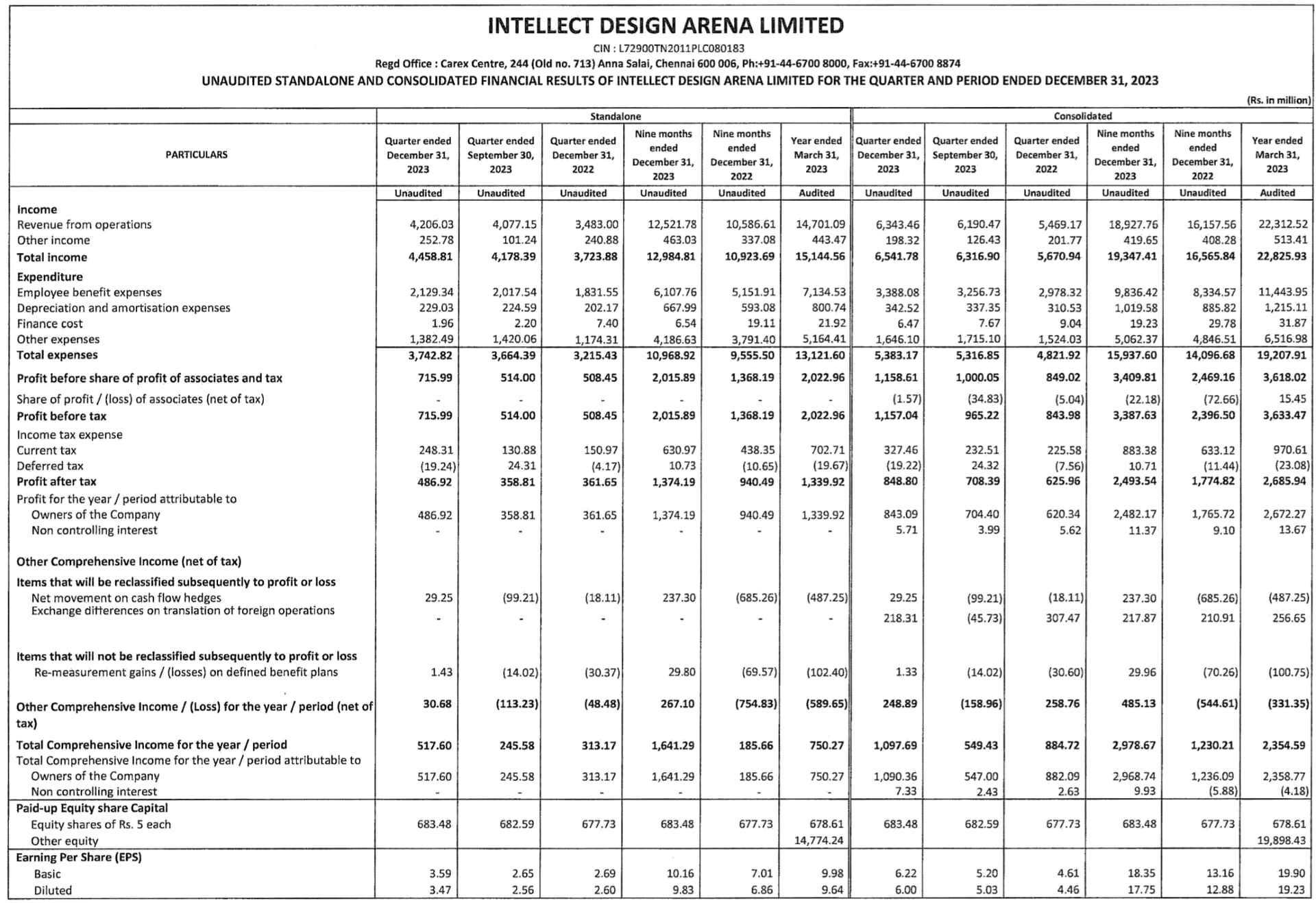

IDA Results

Margins 20% +

detailed q3 concall notes

q3 update intellect design arena.pdf (7.3 MB)

Indian IT cos could gain from woes of Atos, Temanos, says Nilesh Shah (moneycontrol.com)

Troubles at Temenos should Help IDA I Guess.

However looks expensive at the moment.

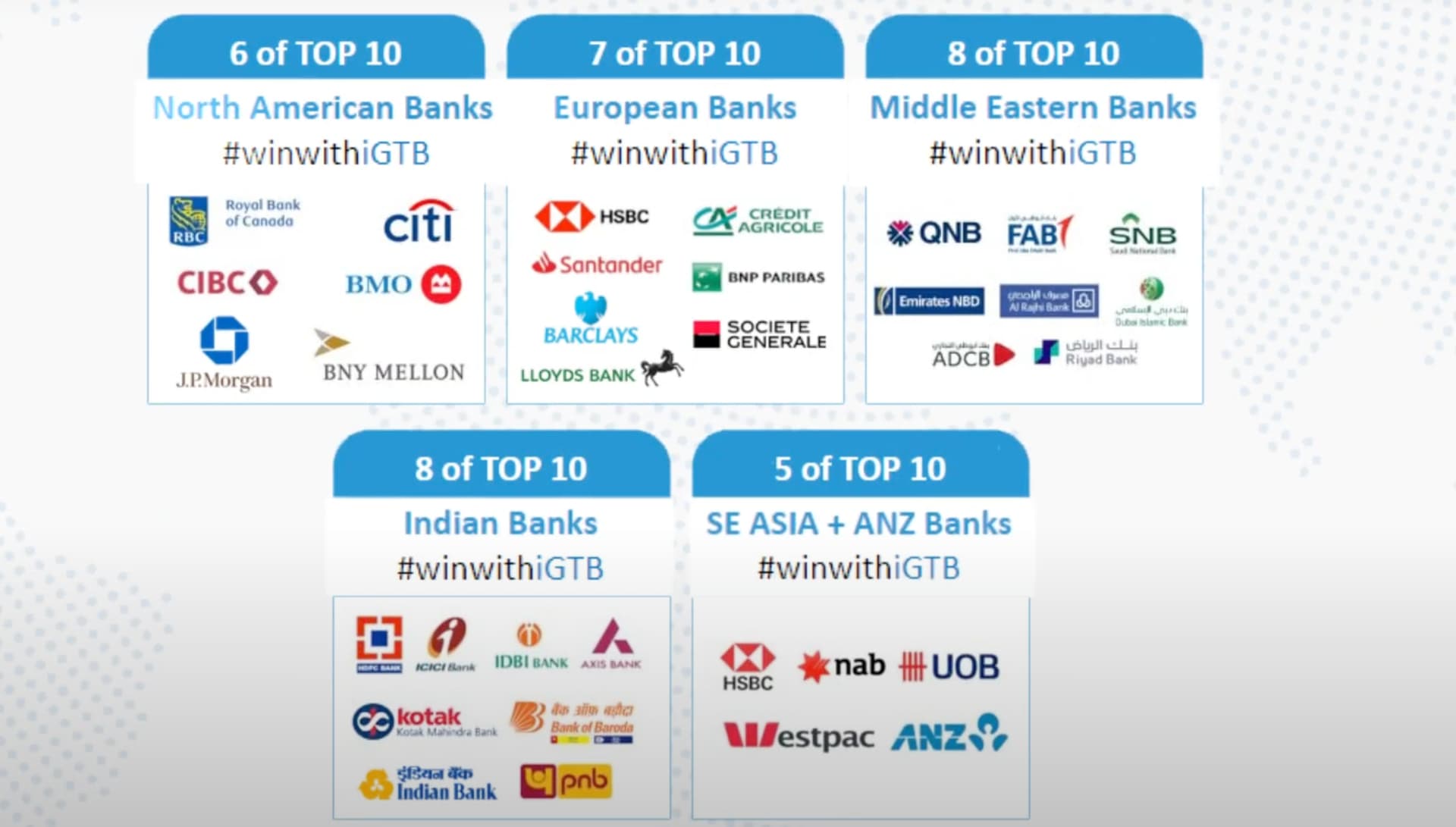

In case you have not heard why Teminos woes Nilesh Shah is referring here it is. This is the best thing that could have happened to Intellect the last few months.

This report will report create doubts in the minds of perspective customer which are being targeted by Intellect as well. Plus Teminos has a large user base in Europe, which is focus area for Intellect.

Key beneficiaries of this will be for large deal. However due to size, it takes long time to seal a deal. Looking at the trouble of Teminos, I think IDA shall report better deal win in the next 3/4 quarters IMO.

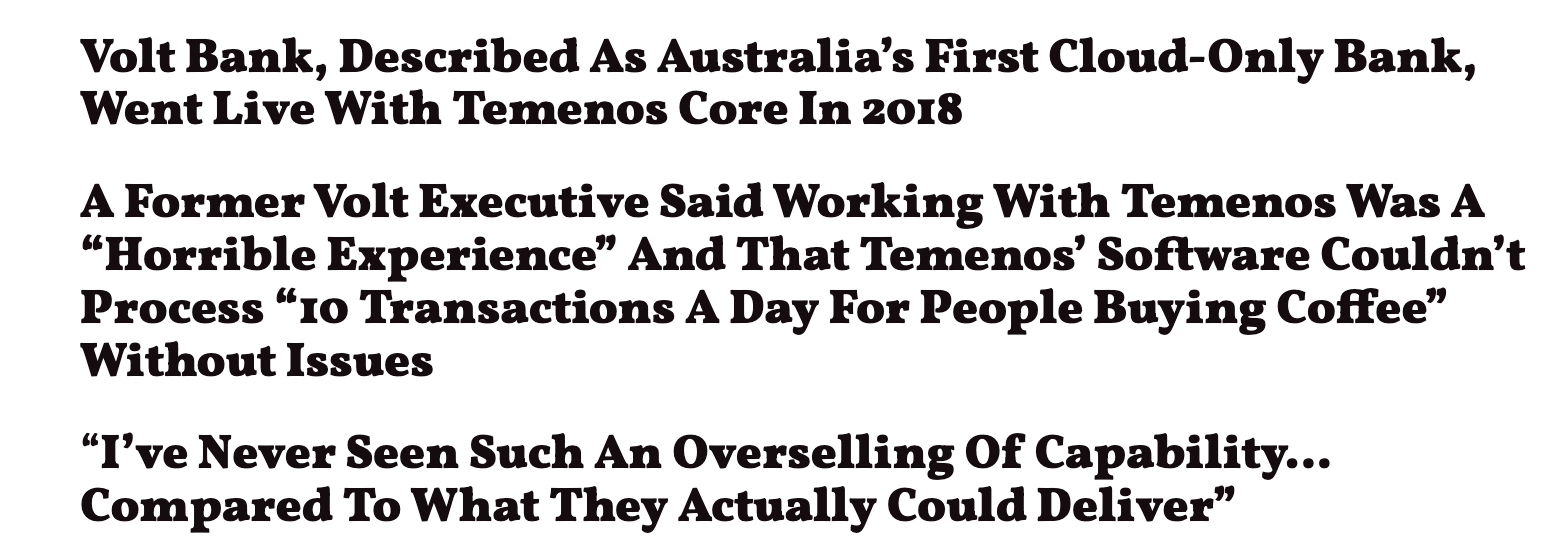

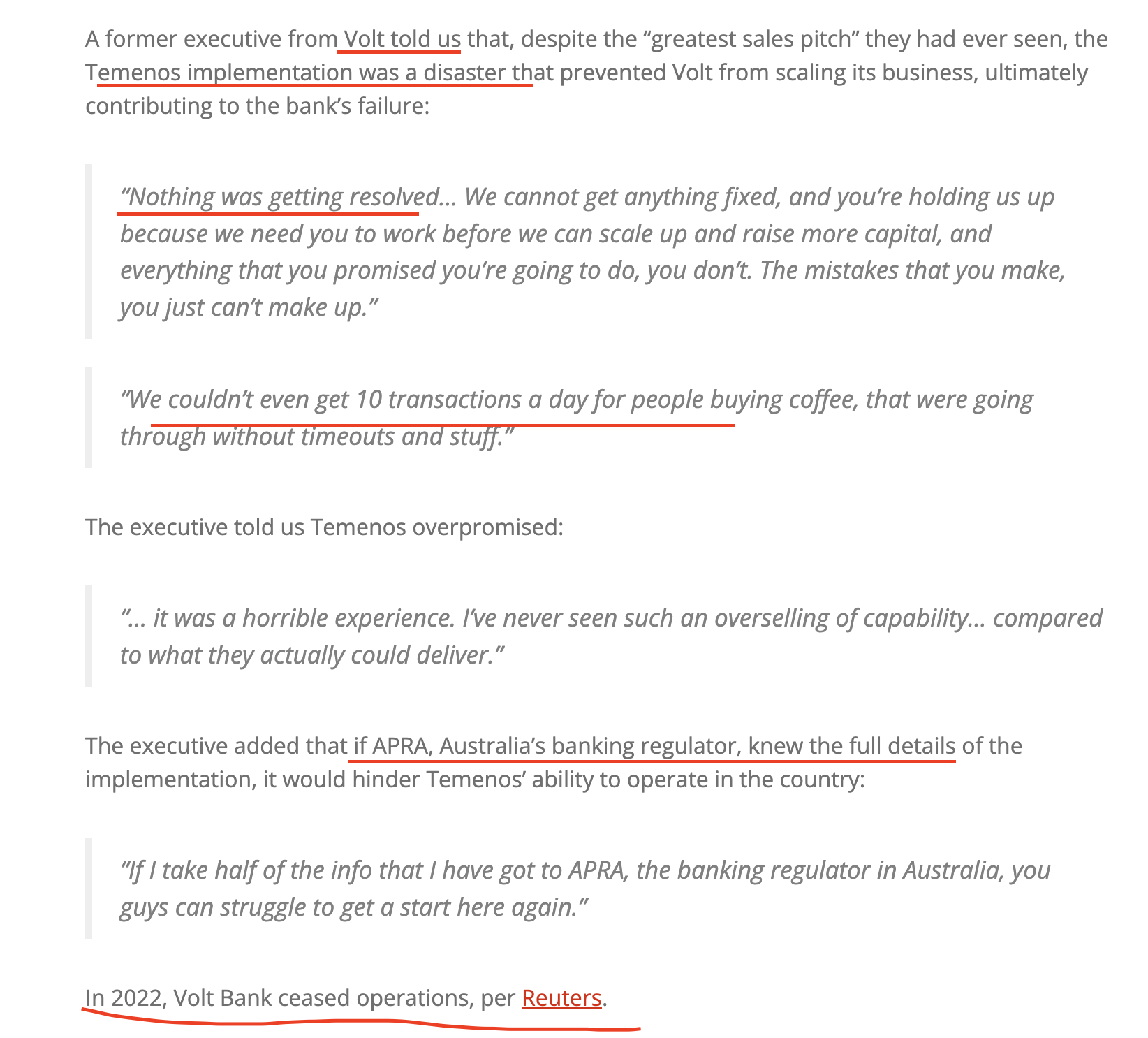

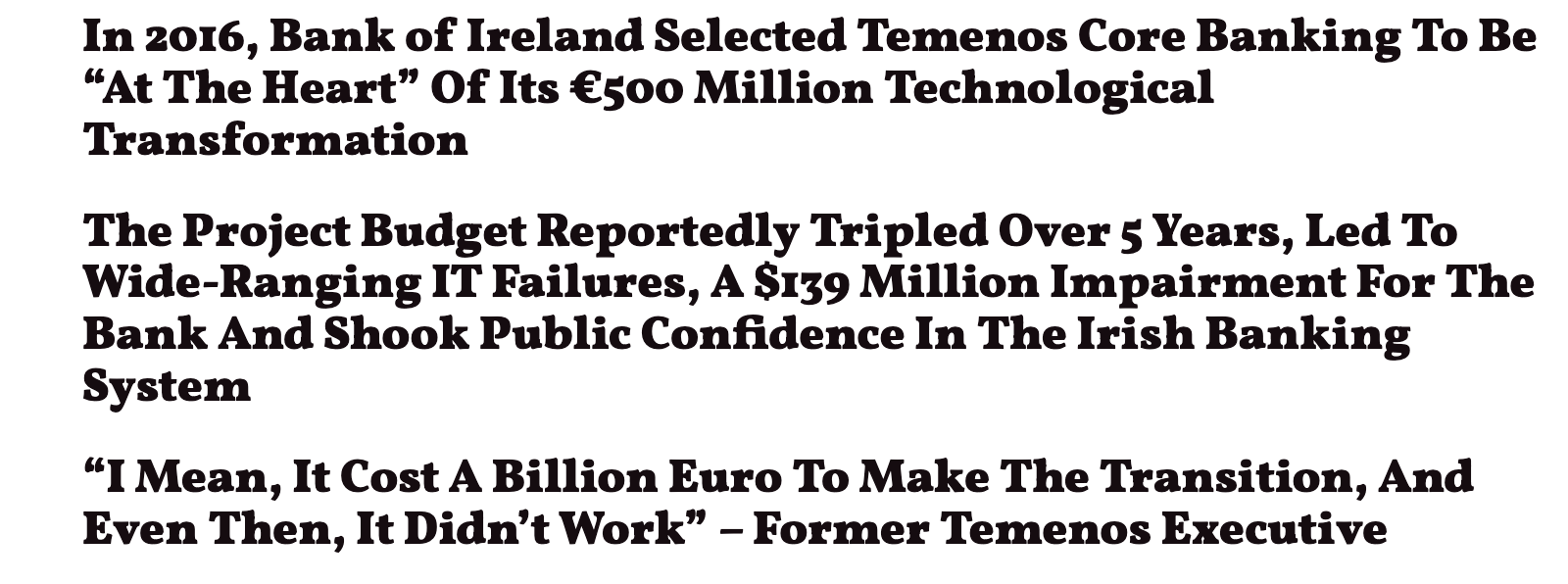

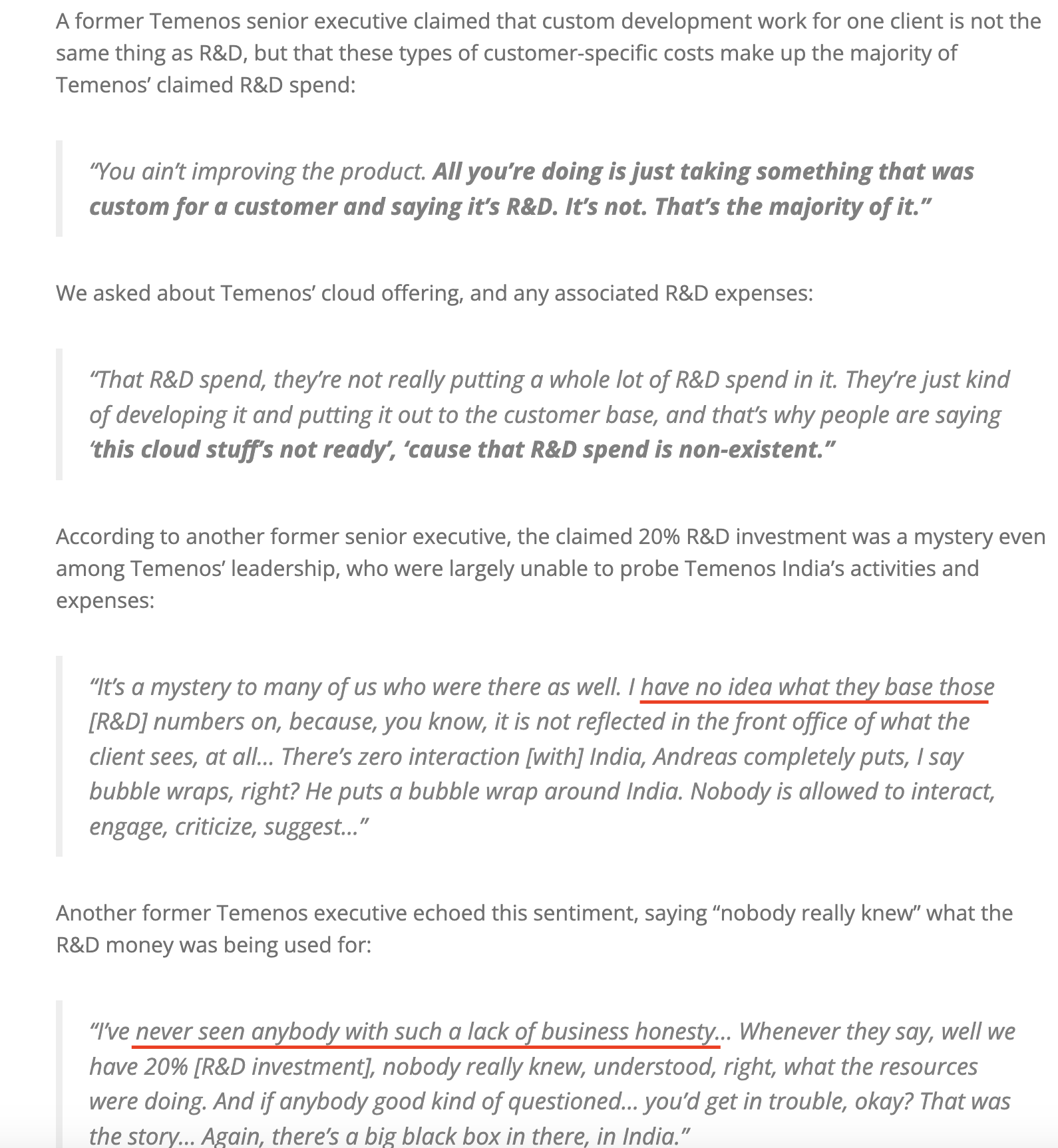

https://hindenburgresearch.com/temenos/

I know the report is huge (may 20/30 pages). Here are snippets from the report, which highlight few important things about them

Bank of Ireland $2 billion

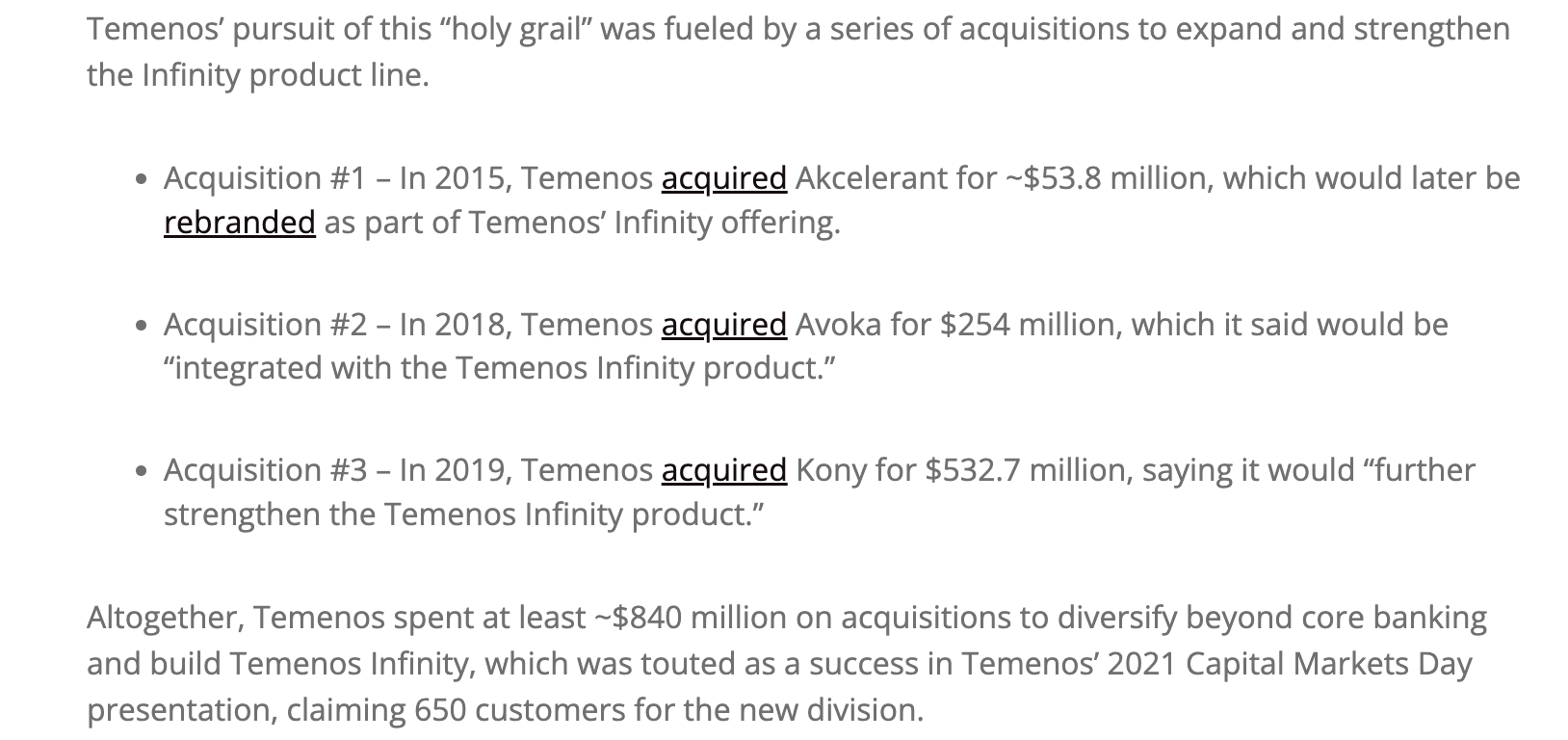

Temions spends fortune in acquisitions

… they planned to invest around 20% of the revenue in R&D. but…

Note: Invested

Lower revenue guidance of 620-630 crores for q4.

Been tracking this company for quite long, been in and out and currently having a tacking position. I still could not figure out the business model of this co.

In the last 2 years, from Q1FY23 to Q1F25 - it has won 105 deals, and went live on 109, with 18 of them at least over 50Cr per deal. That is atleast 900 Cr of new revenue, which should have shown up somewhere?

If we take all the 62 of the destiny deals won in the last 8 qtrs, that should add up to atleast 2300 - 2500 Cr of incremental revenue. At the same time, when we look at the license lined revenues, it has only gone up from 281 Cr in Q1FY23 to 312 Cr in Q1FY25.

Even if we discount the loss of GEM project, doesn’t seem like all these new deal wins are actually translating into the platform or license revenues or AMCs. The AMC was 81 Cr in Q1FY23 and just 121Cr now. The GEM deal was mostly platform deal, as the platform revenues have gone down substantially, from 144Cr in Q2FY24 to 66Cr in Q1FY25.

On an avg, 50% of revenues are license linked, so what’s the remaining revenues? This ratio of license linked vs. others has remained mostly constant for the last 8 qtrs. The SG&A expenses are almost half of the license linked revenues in the last 8 qtrs. The Software Dev expense is mostly constant for the last 8 qtrs.

The investment thesis was that as they sell more of these deals, recurring revenues will increase, cost will remain constant and profits will zoom. Doesn’t look like anything like that is happening. Management guidance for FY25 is 15%-20%, which seems like more of the same. From the numbers, it seems like they need to keep selling these deals just keep the lights on. Would appreciate your thoughts. Thanks.

as per their concall, 480 cr is fixed expense including their current R&D spend what they are doing, and any additional 100 cr income from here will give 80cr to profit. In another 6 months there will be more clarity on their guidance… Even I have the same questions on revenue growth… Didn’t seem anyone asking right question in this quarter concall…

Very valid concerns. Also the management keeps issuing some or the other notification to the exchange to stay in news. Some award won, or some partnership with another firm, some bootcamp. Constantly in the news cycle. Rarely do you have a notice of a large destiny deal won. Previous quarter they said they just missed out on a very large deal. This quarter they said all work had been done for a deal but the bank said they will start in Q4 so expenses are there but revenue not. I think a 30 crore deal.

My Take:

I think they are seeing lot of traction. This does not mean that it will fructify, but they are putting themselves in the right spot at the right time. Earlier many IT companies would believe that they can develop project/product if they implement similar thing for few clients. But Intellect has developed over 30 years of domain expertise with Arun Jain spearheading the operation with full focus on organic expansion.

Intellect was a bit slow on cloud and subscription business but it looks like they spotted AI trend nicely and are riding it. Hopefully it shall result in more client signings and entry in more developed markets.

Market Focus and Strategy

Distribution Market Shift

Recent Developments

Pipeline and Revenue Growth

Product Strategy

Seasonal Trends

Partnership Strategy

Core Banking Insights

Insurance Sector Focus

My Take:

This quarter exemplifies a recurring situation in which product sales do not materialize, leading the management at Intellect to depict a narrative of missing or delayed sales for certain products. Such delays occur with such frequency that it becomes impractical to concentrate excessively on quarterly figures beyond a certain threshold; however, management continues to emphasize this issue repeatedly over the next four to five quarters.

Furthermore, management places considerable emphasis on achieving a compound annual growth rate (CAGR) of 15-20%, which may appear acceptable from a year-over-year perspective but does not translate effectively into quarter-over-quarter results. The second quarter was illustrative of this trend.

Management believes sales of 700 cr+ within the next three quarters.

Intellect is making strides in the U.S. market; however, their performance regarding Banking and Transaction products—central to their operations—has been less impressive.

I express caution regarding their approach to System Integration (SI). They have partnered with major SI companies such as IBM, HCL Tech, Wipro, and Accenture. Unless these firms generate revenues between $30-$50 million through their partnership with Intellect, significant commitments are unlikely. Since many of these SIs are joining simultaneously, it will be intriguing to observe how these collaborations evolve. Ideally, Intellect should have initiated partnerships gradually with a select few SIs before expanding further; instead, they opted for a more aggressive strategy. .

On a positive note, some of these SI partnerships could yield substantial benefits outside the U.S For instance, HCL Tech acquired IBM’s product portfolio four to five years ago and has since established client relationships in over 100 countries. Intellect can undoubtedly enhance its reach through these extensive distribution channels. If Intellect succeeds in improving its sales via SIs, significant margin improvements could follow; however, this will likely involve increased costs over the next two to three quarters.

Intellect has done investor meet about their purple fabric platform. PPT here

Good demo and good Q&A.

Intellect Design Arena Ltd. has recently assumed responsibility for Central 1’s digital banking operations in Canada, taking over the support of front-end and back-end operations for approximately 160 credit unions

This agreement represents a significant opportunity for Intellect to strengthen its presence in Canada and North America, but it also comes with considerable responsibilities and challenges. The company’s ability to execute this transition smoothly and leverage the new capabilities will be crucial in determining the long-term impact of this deal on Intellect’s market position and financial performance (make or break them).

Note: Invested

Given Intellect Design Arena’s significant exposure to the US market, could ongoing tariff tensions, trade wars, and recession risks impact its business growth?

Intellect derives most of its business from the U.S. by selling insurance products(Magic Submission), which is not a significant revenue driver (as compared to other products). The company has been attempting to expand into the banking sector but has faced limited success so far. Recently, it has refocused its efforts on markets in the U.S., Europe, and Canada.

If a recession materializes, Intellect may face challenges as its end customers could be impacted. However, its acquisition in Canada is expected to keep the company occupied for the next 6-8 quarters as it integrates new workforce, evaluates or replaces existing solutions, and explores multiple cross-selling opportunities. Even if its U.S. business does not perform as anticipated, the Canadian operations are likely to sustain Intellect’s growth trajectory.

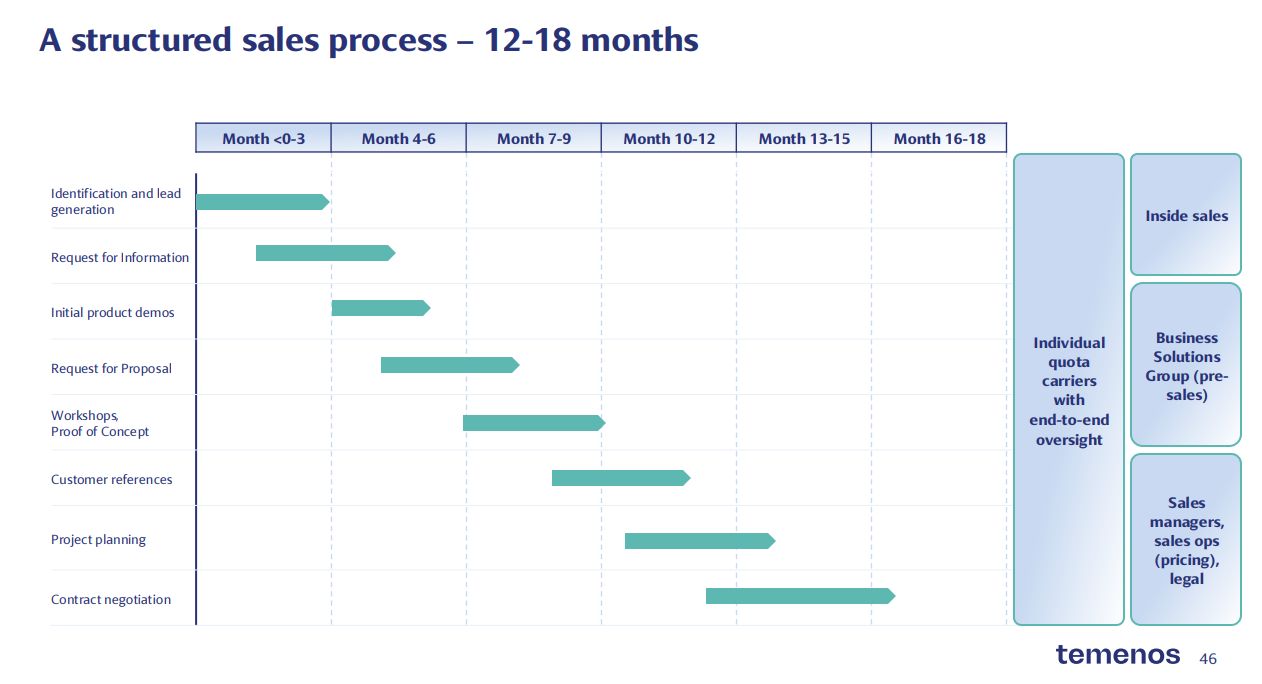

Over the last three quarters, Intellect has signed several distribution agreements with companies like HCLTech and LTIMindtree. According to management, these partnerships take time to establish and become operational. It is anticipated that by the second half of FY26, tangible results from these arrangements will begin to emerge.

Typically, sales cycles in this industry range from 12 to 18 months, as highlighted by Temenos during their Capital Market Day presentation. Intellect’s timelines are expected to align closely with this benchmark, and progress on these partnerships will likely be visible in H2 FY26.

I found the partnership between Intellect Design Arena and LTIMindtree intriguing. According to the press release, this collaboration focuses on the Middle East, Africa (MEA), and Asia-Pacific (APAC) regions. Interestingly, Intellect had recently de-emphasized these markets to concentrate on the U.S. and Europe. Historically, Intellect has achieved significant success in MEA and APAC, but the margins in these regions were relatively lower. Despite this, Intellect maintains a strong presence in many of these markets.

Compared to other banking software providers like Temenos, Intellect’s products are competitive. Banks in MEA and APAC are often price-sensitive, which could make Intellect an appealing choice. Moreover, one of Intellect’s key advantages is its flexibility. While Temenos is known for its comprehensive solutions, some reviews suggest it lacks flexibility in delivery. In contrast, Intellect’s adaptable approach could better meet the needs of customers in these regions.

This partnership with LTIMindtree could help Intellect regain market traction in MEA and APAC while improving margins. Under this model, product licensing revenue would go to Intellect, while implementation revenue would be handled by LTIMindtree. This approach not only allows Intellect to focus on its core competency—developing state-of-the-art products like eMACH.ai—but also enables faster and more efficient deployment through LTIMindtree’s expertise in digital transformation.

Additionally, Intellect’s organically built AI-driven platforms offer a competitive edge over Temenos’ acquired and integrated solutions. This partnership could position Intellect as a stronger contender in these regions by delivering innovative and customer-centric solutions tailored to local needs

UK-based global bank partners with Intellect for a multi-year, multi-million dollar engagement. It looks like the bank will use Intellect’s eMACH.ai platform to expand the wholesale banking with contextual customer experience and insight-driven services.

Disc: Invested.

Results are out for q4 fy 25

https://www.bseindia.com/xml-data/corpfiling/AttachLive/15b6ab63-0a2d-4082-bd9a-12e55d9c9fed.pdf