Deal pipe line is growing. Win rate is favourable. Product and platform are mostly in monetization phase. Only concern seems competition and macro head wind which is part of the game.Hurdle avery company has to cross to win the race. Optimistic & hold rating

2 Likes

I do not think the PAT will bounce back quickly. The reason is due to the shift from product to platform business.

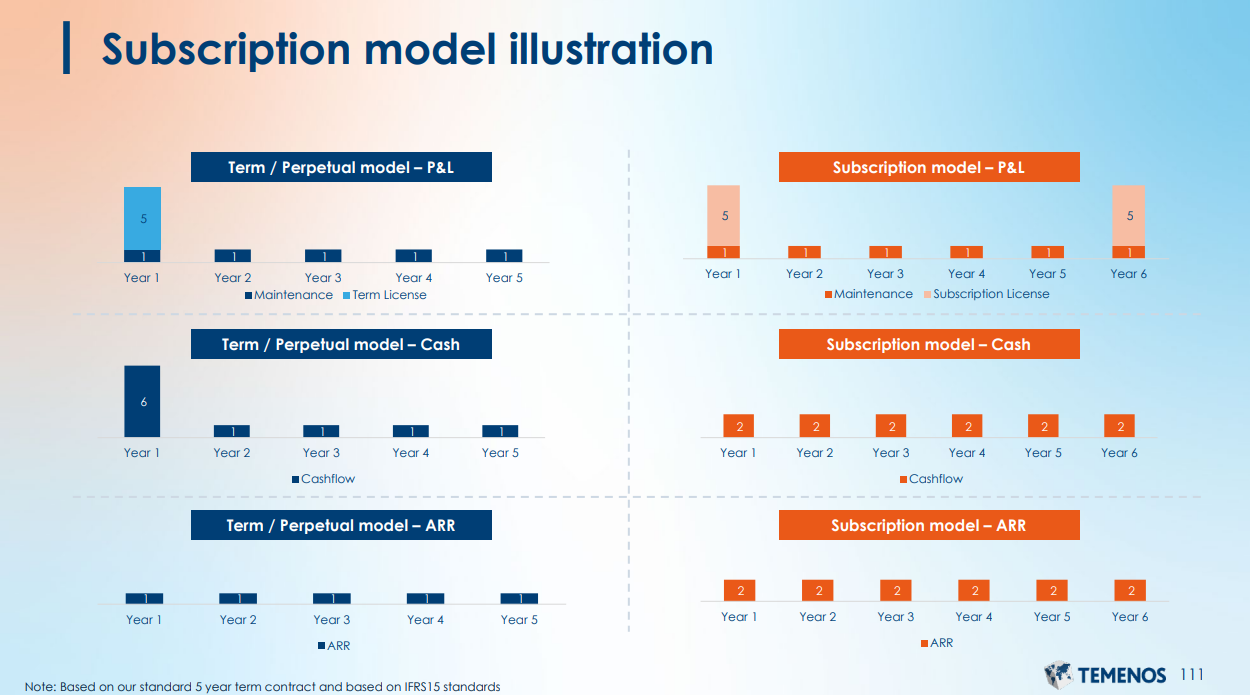

When a product company move licence revenue from one-time licences to subscription-based revenue, it is always a painful journey. I think IDA started it a couple of years back, but now this product-to-platform shift is accelerating, and it will continue to cause a problem for some time.

As per the Temenos calls, this is how they book subscription revenue.

Arun Jain is more or less saying the same time. IDA won products with a linces cost of $2.9 million. Had the sales been a one-time license, their PAT would have been higher by at least $2 million(as licences have very less cost). However, IDA could report only 1 or 2 cr of revenue in the current quarter due to subscription-based revenue. As a result. The PAT slump is severe.

AS more and more clients prefer to use the platform, this impact will be visible for a few quarters at least. The customer they are signing today is likely to be very profitable (75% gross margin business) in 2 to 3 years, but it will be a hard grind until then.

They said earlier that Tier 1/2 clients prefer one-time linceses. If they manage to sign a few Tier 1/2 clients in the next 2/3 quarters, the picture could be different.

In summary, it seems to me that PAT will take some time to recover to an earlier level (80cr + quarters run rate), so this year’s PAT will be considerably lower than FY22.

Some additional notes from Q2 call.

- Aim to maintain 20+ EBITA Margin for FY23. This is the lowest in 2 years.

- $3 million deal has slipped into the next quarter

- Earlier, IDA was dealing with small players. Now we are in the competition going with large boys like Temenos in Europe.

Earlier they did POC and then lots of boardroom negotiations. Now the customer wants us to do real POC covering various geography and countries. Hence it is taking a long time. - Large few years, R&D budget was $20 million. Capitalise $5 million.

- $100 million quarterly sales- 8 to 12 quarter. The margin guidance earlier was 30% EBITA (in the current quarter, EBITA was 15%). Now need to revisit in the next 2/3 quarters.

- We have not considered large deal wins while giving 20% guidance.

- Competitors:

- Thought machine. $50 million revenue valuation at $2.7 billion market cap. Due to TAM high.

- Modern Treasury- $25/30 million revenue - $2 billion market cap.

- TAM on embedded finance on consumer/corporate finance is $1 trillion each. This is a new segment, and this is where growth is happening.

- Platform- It takes around 3 to 6 months before revenue starts billing.

- Data big differentiator in the US. It is 100% subscription base. Subscription revenue is sticking a lot more than we had expected.

- Large deals in Europe- In 3/4 of deals, we have been shortlisted in the last three vendors - Temenos, Thought machine and Intellect. We have not yet any deals yet. If we win, it will be a significant impact on our revenue.

Here is today’s interview on TV18

14 Likes

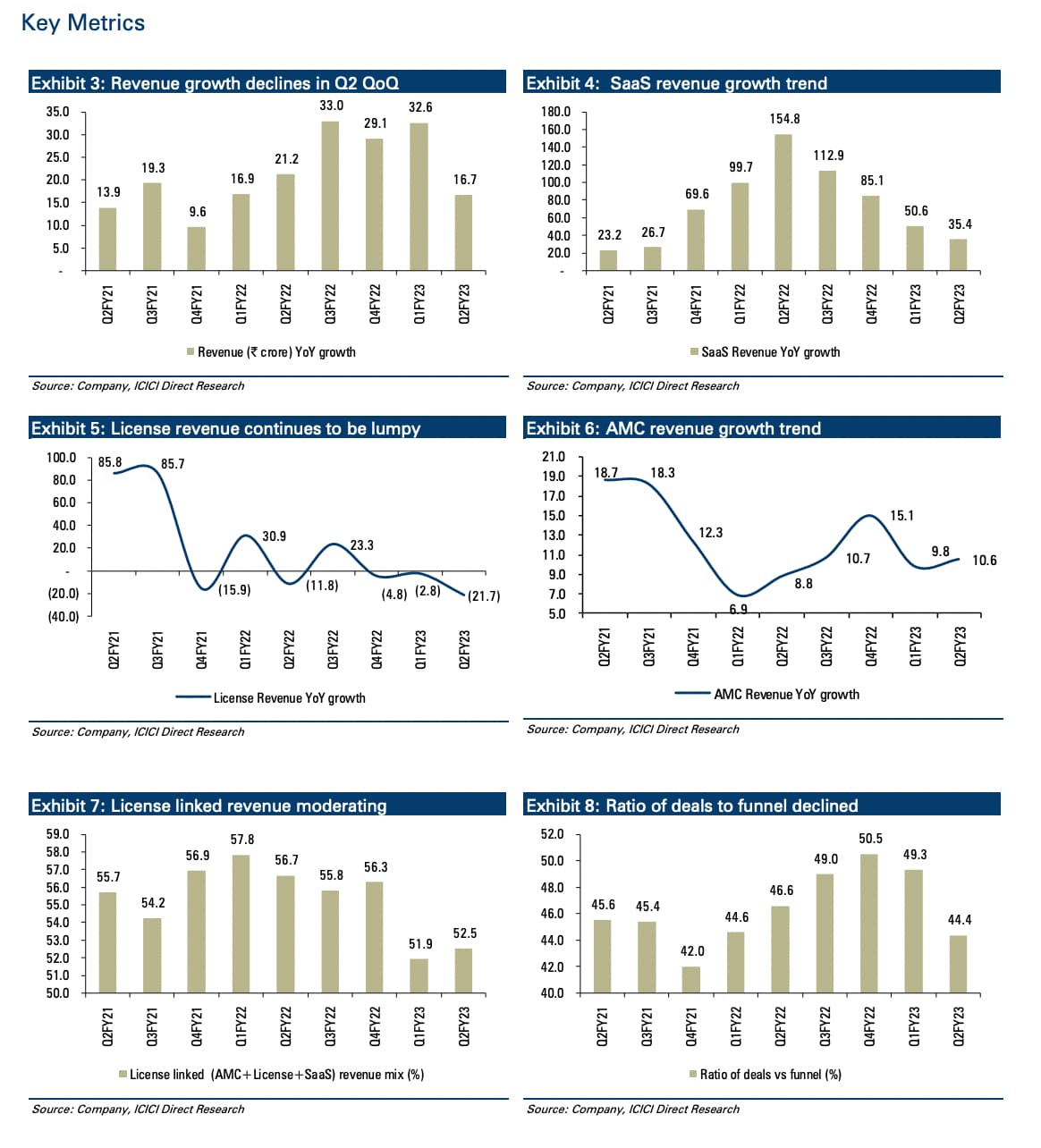

ICICI Direct downgrades Intellect Design from BUY (TP 810) to HOLD (TP 525) on the back of lots of key metrics worsening

Temenos has echoed what the management mentioned about lengthening sales cycles linked to a number of large deals in the pipeline and banks being more cautious in their decision-making given future macroeconomic uncertainty.

7 Likes

A 3-year-old Indian digital lending startup Lentra offering loans as a service was valued at $400 million in a recent funding round. It has more than 50 clients and has processed over 13 billion transactions and $21 billion worth of loans since its launch.

I wonder why Intellect despite its Digital Lending product being rated highly by analysts and having top ranks in sales tables is struggling to attract remotely similar valuations.

Is it because?

a) Its products/platforms are not as good as the ones provided by focused Fintech startups in various verticals.

b) Intellect is trying to do too many things at once. The products and platforms do not get the investment and management attention required to make them successful against well-funded startups in each product segment. e.g. This quarter they launched 3 new platforms viz. Magic Submission, Magic Invoice, and iESG. I don’t see an obvious competitive advantage IDA possesses in the invoice processing space and ESG.

c) The market seems to like focused startup companies but the market is wrong. Platforms and products need investment and time to mature. IDA revenues, margins, and profits will increase exponentially in the next few quarters/years.

On a lighter note, I wish IDA followed its own laws of design thinking in capital allocation

4 Likes

Its unfair to compare valuation of a private company with a listed peer. Once the so-called unicorns hit the public markets, they will get attitude adjustment.

2 Likes

Good coverage, a bit long Intellect Design Arena Full Video | Nandan Madhivwlla | Smart Sync Services #investing #stockmarket - YouTube

6 Likes

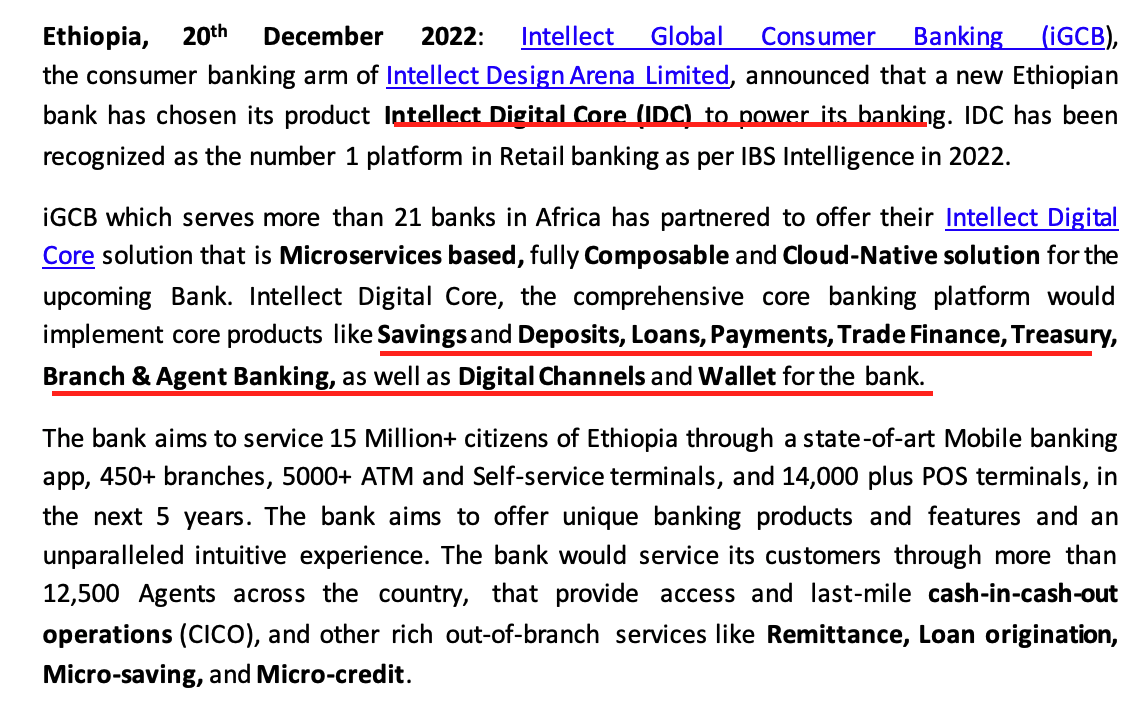

Intellect has announced IDC win. IDC is a core banking products and based on the press release Ethiopian Bank is buying full products. Although it is African bank, which will not fetch as much license fee as Western bank, Intellect is slowly becoming a force to reckon with in African region. This win should bump up license revenue in the current quarter.

10 Likes

Looking at guidance vs performance for the year: At the start of the year, guidance was 20% on revenue and 30% on EBIDTA. They have missed that by quite a lot ( for 2 Qtrs). In the last Qtr, it was revised to 20% for EBITDA, REVENUE & NET PROFIT.

Also, another no was one of the next 2 Qtrs they will hit $75mil revenue.

Just doing some back of the envelop calculations. If they were to achieve the latest guided nos.

They’ll have to do on an average(for Q3& Q4) : 590 Cr in revenue, 194 Cr in EBITDA & 114 Cr in NET PROFIT.

If they can do this stocks makes a case for rerating. However, going by the past history of guidance & actuals I am skeptical.

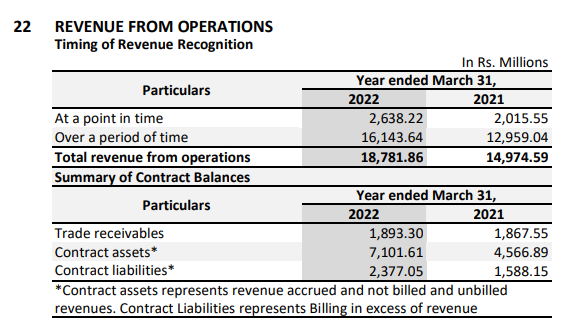

Unbilled revenues are very significant portion of total revenue, and increasing year after year. In my personal view, this is very aggressive accounting practice.

6 Likes

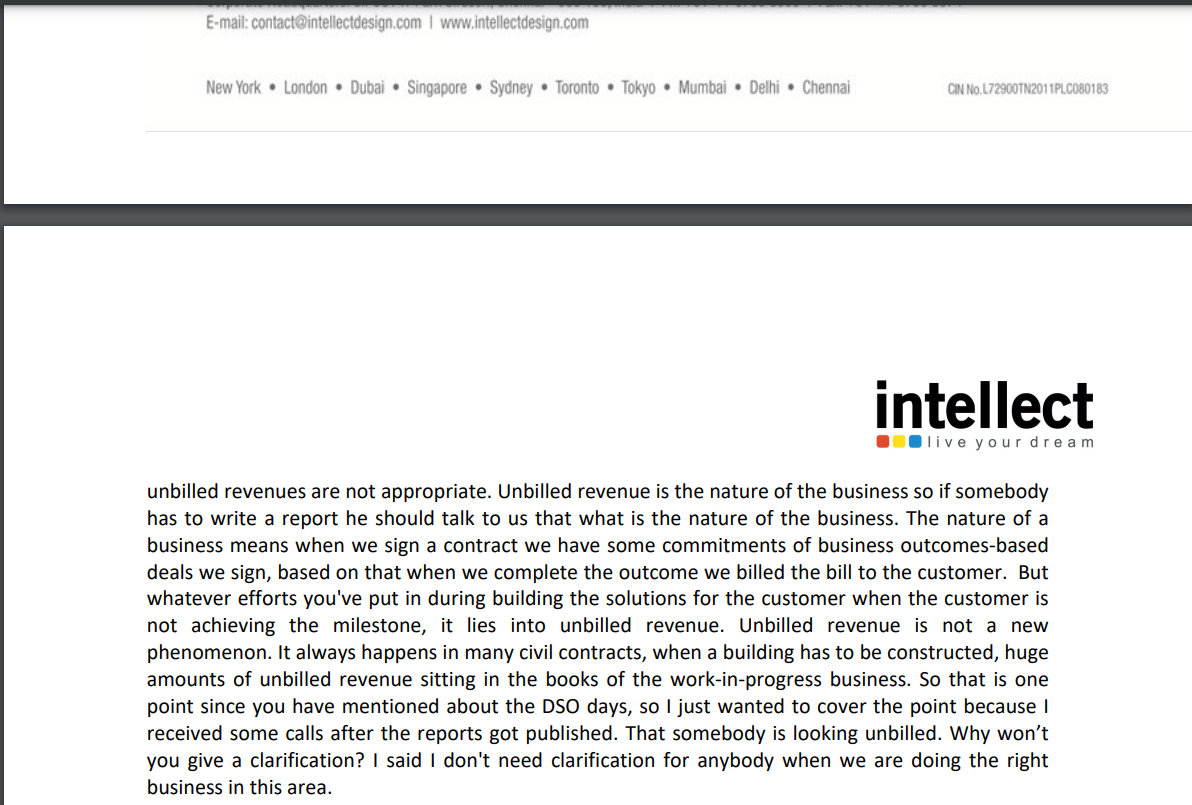

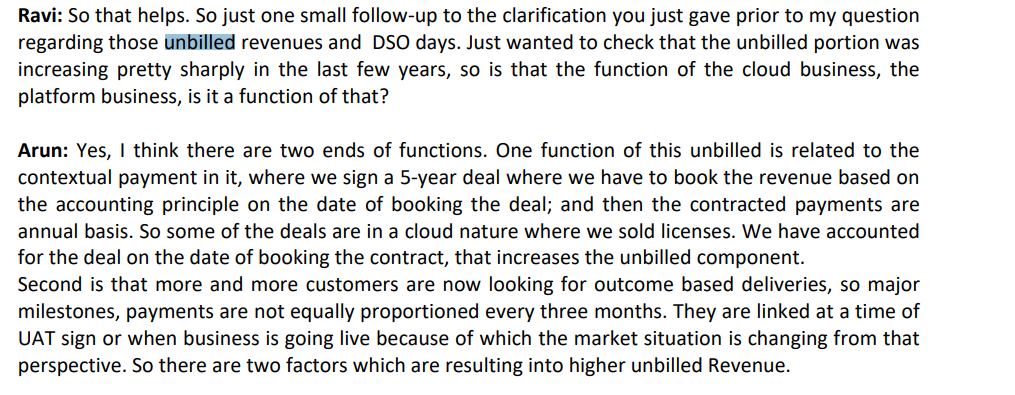

When asked about this, Mr Arun Jain explained saying this is because of PoCs that they do and some of it can also be attributed to the milestone billing where the billing can only be done after a certain stage in the implementation is achieved.

I am not sure how prevalent is this practice in other IT product companies. May be someone here can throw some light on it. Thanks!

1 Like

Just had a cursory glance, I have found similar item in NewGens and Tata elxsi’s annual report. I don’t think it is that big an issue as it is made out to be. Could be confirmation bias .

Disclosure: Invested.

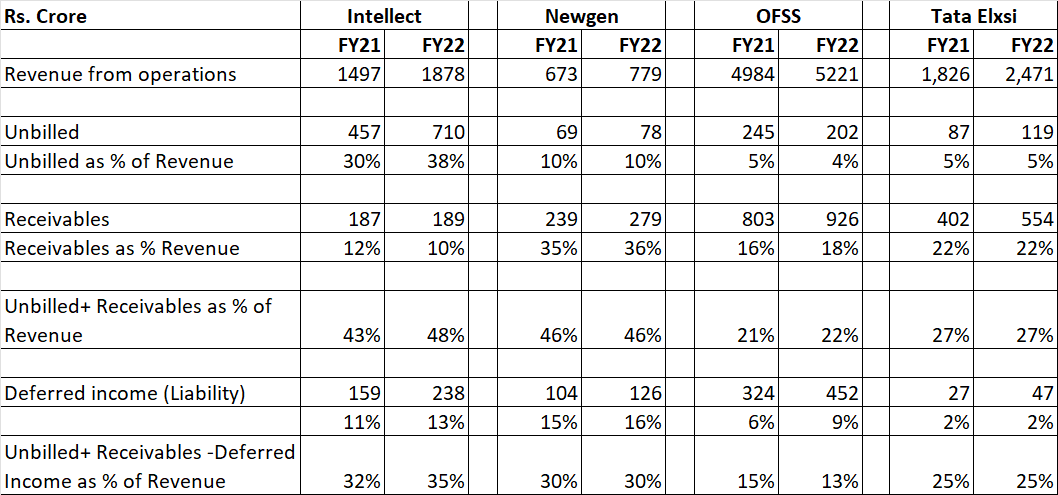

I have compared 3 IT product companies focused on BFSI segment (though products are different) Intellect, Newgen and OFSS and following is the outcome. Since you mentioned Tata Elxsi, I have also included it in analysis.

Intellect has significantly higher Unbilled as % of revenue, while Newgen has highest receivables. This may be within the ambit of accounting standards and logic, but higher unbilled is not a comforting factor. As per my limited understanding, I would rate OFSS at 1, Tata Elxsi at 2, Newgen at 3 and Intellect at 4 in the above analysis (limited to just 1 parameter and surely not comprehensive). Moreover, another aggressive accounting by Intellect is capitalization of product development cost, which both Newgen and OFSS charge to P&L.

Disc: Invested in Tata Elxsi and Newgen

11 Likes

My understanding here for OFSS would be that given that it is not selling a lot of new licenses, it would have lower receivables & unbilled revenues.

For AMC and SaaS revenues your receivables & unbilled are lower. Whereas for new licenses & implementation, unbilled portion is higher as it is linked to completion of some stages of implementation till which revenues associated with that are considered as unbilled.

11 Likes

So, isn’t revenue recognized (in income statement) only when the milestone is met (invoice raised in good faith) ? Of course there may be payment terms like 60 days, 90 days etc., for customer to pay from when the invoice is raised. This way, the recognized revenue from income statement stays as receivables in the balance sheet for those number of days and/or longer if customer hasn’t paid because of a delay/disagreement.

Why should a revenue be realized in income statement (which boosts up income/EPS etc.,) while the balance sheet paints a completely different picture ?

While we all like low receivables, a huge “unbilled revenue” category makes it look uneasy. Let me look at the past years if such a huge 50% is normal for IDA.

Update:

Here’s the clearest definition I got Accrued Revenue - Definition & Examples | Chargebee Glossaries.

But as warned here, 30% → 38% unbilled revenue looks huge

5 Likes

I am working in IT Company for last 17 yrs. Based on my experience Implementation of Proudct is mostly Fixed Cost Project and Billing is based on Milestone as compare to vast majority IT Service company (in India)) Body hopping (T&M) company.

In Fix Cost project Revenue booking is done based on % of Work completion (POCM) based. & there are instance where if milestone acceptance get delayed revenue reversal or low revenue booking against actual cost in later part of the Project completion.

However looking at Intellect % of unbilled is really high. I believe they need to be more coservative in this regards.

Hope this give some perspective.

Note: Invested in Intllect from lower level (Last 5 yrs back) Recently bought few ( 100s. )

5 Likes

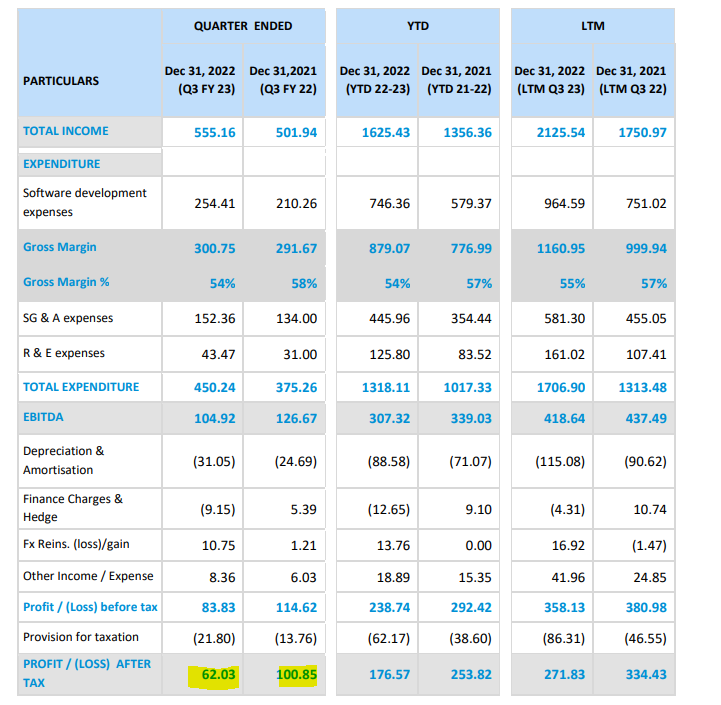

Q3-FY23 result is out. It is not great YOY basis.

Con Call Notes

General

- 5% investment (from EBITA) from product to platform business

- Next quarter will be better than Q3 in terms of EBITA basis. Shall be able to cross Q4 more than $75 millions

- The focus is on Europe

- ThoughtMachine - Invested $550 million USD in creating a core baking platform. -

- Giving a Term license and not giving a perpetual license. This will give revenue visibility after 5/7 years.

- AMC is only for licensed-based revenue.

- SAAS around 100 cr revenue/quarters

GeM- Part is paid upfront. The rest is paid when the payment is made.

Europe

- Our product architecture resonates with a customer

- Word of mouth and referentiality is giving us good traction in Europe (UK & Europe)

US/Canada (Not publishing number for US contribution)

- Started focusing on the US in last two years

- Solid traction of magic submission in the US/Canada.

- Magic submission can grow 50% in the US market.

- Magic submission last year 0.5 USD per deal. Deal size can be 3 million USD ARR per deal

- Clients- Bank 10 Insurance 15

- Will take 18/24 months at inflexion points in North America

GTB- Winning 3 out of 4 deals.

Liquidity- Good traction due to higher interest rate.

- 3/4 deals in France.

- Spain/Italy is in progress now.

GCB

- IDC (Core Banking Platform)

- Every bank needs a Core bank (5000 banks )

- Working on seven deals in Europe on Mac Bond core banking

- Top 3 vendor in Europe marker for many deals

- Deals closing take from 12-24 months

- ThoughtMachine/Teminos are the main competitors for big banks. Not seeing Mambo in large deals.

- iKredit 360- SME/Secured/Insured loans can be processed on this platform.

Quantum

- Slowdown in deals in last 2 quarters

- Deals move from Africa to the advanced market

Intellect AI

- Merged a few units to create this.

- 80% of banks are considering replacing Miles with our Wealth Platform

9 Likes

Hi eyeryone Can someone explain why employee cost is increasing at such a rapid pace for intellect design arena?I follow other I.t companies also looking at competitors the employee cost has remained stable or reduced as a% of topline increased over a period of time.This quarter is stands at 54% of sales despite sales being alltime high.

1 Like

I’ve been invested in Intellect since late 2020, and averaged up in the process. Sadly, have lost a good chunk of my gains during 2022. However, here’s why I remain invested in this scrip:

- India hasn’t produced many product companies. It is indeed commendable that Intellect is able to compete head on with Temenos, admittedly a big player in the banking software space

- It is difficult to compare revenues on a quarterly or even a yearly basis for a company undergoing changes in revenue monetisation, due to a shift away from perpetual licenses to term licenses and SaaS revenue

- However, new bookings and pipeline are the holy grail for any B2B business (be it tech or infra or CRAMS). New wins will materialize into revenue at some point in the future, in a term license or subscription format. The certainty of realising revenue and recovering cash is really high in the tech sector, which when coupled with low capital intensity means these companies deserve to trade at premium valuations (to what extent is another question)

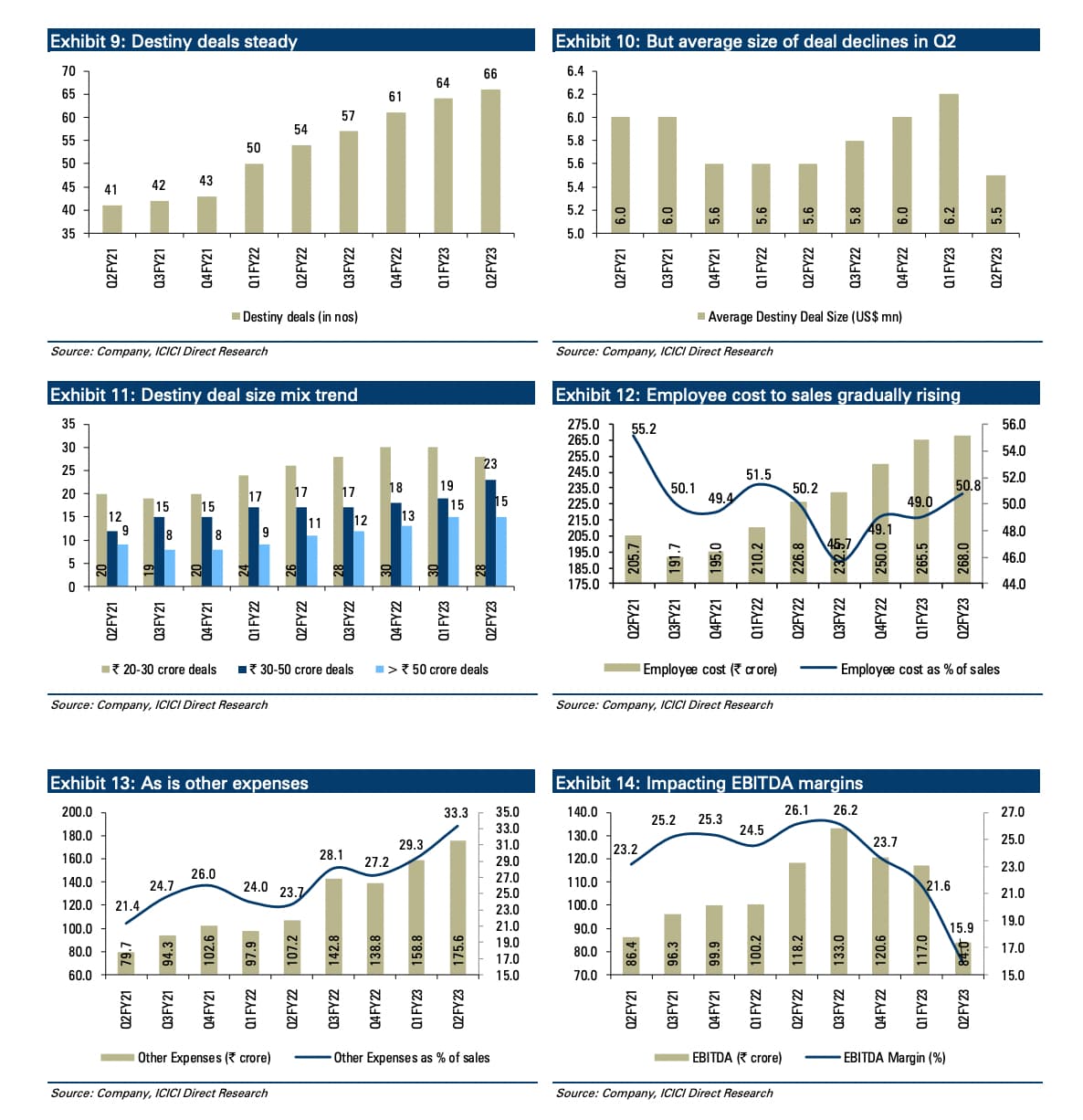

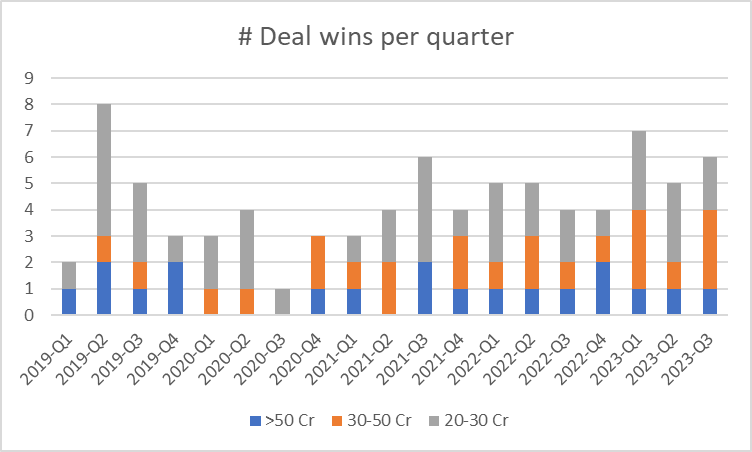

- Here’s how Intellect has been performing on its new wins on a volume basis for its destiny deals (i.e. deals with >20 Cr contract value)

- As we can see, there’s been a steady increase in new wins, in 9mFY23 vs FY22, particularly in the 30 Cr+ category, which is a good leading indicator of future revenue. If you set aside 2019Q2, the trend is pretty positive over the last 4 years

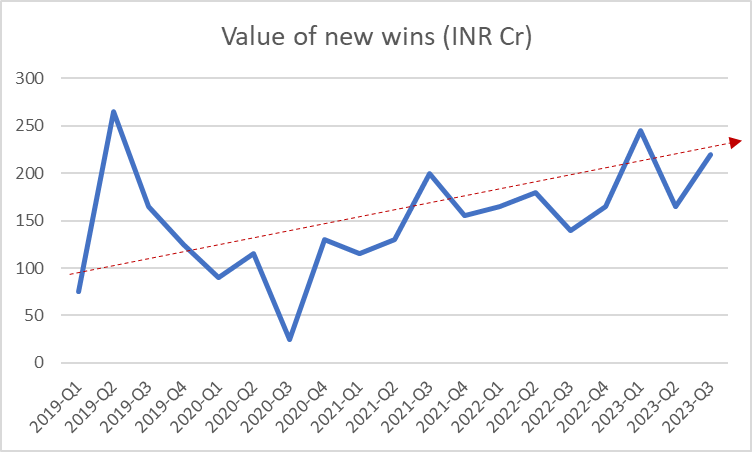

- To see this in value terms, I’ve taken a weighted average of volumetric wins by the respective deal size category (for e.g., I’ve taken 40 Cr as the avg. for 30-50 Cr bucket). This gives us an interesting trend

- Again, there’s been a good momentum in growth in 9mFY23, which continues from the historic growth trajectory and is unfortunately masked in the recognised revenue trend. They could have gotten lucky with INR depreciation, but this shouldn’t be a big factor

- If we look at their pipeline, this has remained stagnant at 500-600 Mn$ during 2019-21. It rose to 600-700 Mn$ levels in 2022, and is now at 855 Mn$. Obviously, the conversion rate may not be as high as in 2021 as Management indicated that sales cycle has elongated and customers have become more stringent in their selection process. However, Intellect seems to have expanded its pipeline considerably in 9mFY23 vs previous years, which could augur well for the future.

- Lastly, there’s the whole discussion on margins. I think the Management had been unnecessarily optimistic in guiding for 25%+ EBITDA margins, when they knew they had to invest into product development. “Quarter se Quarter tak” analyst scrutiny doesn’t help with giving the management some time to invest into product gestation, but they should have been firm and upfront about it. Falling EBITDA margins for a product business is totally fine if it’s into growth, much similar to how we are okay with a pharma / chemical company investing into growth capex. Both these levers have the same impact in terms of RoCE compression. In fact, expensing out investments is what stands out in Amazon’s business model.

- So where does this leave us? I think we’re probably near the bottom of the earnings cycle, especially given the P&L shows full impact of tax. Conservatively, this is trading at a ~22x PE multiple on a runrate basis (adjusted for cash), and has the potential to grow revenue at 15%+ CAGR, and 18-20% EBITDA margins. This is not a particularly bad deal for a business with a healthy cash conversion cycle, limited pricing threat, and good RoCE

- It’s a big deal to build cloud-native microservices products. Strategically, this gives the product company an advantage to cross-sell over the term of the contract, thereby increasing the customer lifetime value. New wins in Europe and America / Canada validate their product proposition. Hopefully, this should translate into 20% CAGR that the Management is guiding towards, but given Managements tend to oversell to over-zealous analysts, 15%+ growth should be a base case assumption

- One risk I see is that the number of new destiny deals added to their pipeline has remained stagnant in 2023 vs 2022, which along with an increase in pipeline suggests that their deal value per deal is decreasing, which requires additional S&M investments. This would be a key monitorable to track - if they can increase the number of destiny deals in the funnel due to US / Europe expansion; else, they may see tepid growth ahead

- As a closing thought, I wish to see a bit more aggressive sales push, through channel partner strategy. Intellect has built (and continues to build) solid products, but it’s no use if they are not aggressive on sales.

Disc: Invested, biased

32 Likes

My two cents on current bank crisis and it’s impact on Intellect.

Lately, Bank and crisis become synonymous (once again). It started with SVB Bank, which suffered losses from holding government bonds. Someone has covered this in detail this blog, thanks to @VFM (the SVB collapses explanation is better than what economist has written IMO)

As per Nouriel Roubini, US Banks are sitting on $620 billion of unrealised losses with $2.2 trillion of combined equity. This is a staggering amount, which means they are starting at losses of more than 25% on the equity, which is supposed to be the safest. Agree not all losses will be realised if the banks hold these securities until maturities. The bond maturities can be one year to 30 years. I am sure Bank would not have parked much money in long-duration bonds of 30 years, but I think Banks would have parked a decent(most) amount on 1-year or short-term bonds. A lot of these losses that are unrealised now may not incur if banks hold them until maturity.

Nevertheless, the unrealised losses are staggering, and the situation is not getting better any time soon as there is an expectation that the US interest rate will rise further in the next few months, with many believing that there won’t be an interest rate cut in 2023. This means that banks will have unsettling time for the next few months. Few of banks may prefer to book partial losses now rather than waiting at a later time as investors become unsettled with the prospect of further capital raising from banks. This means cash has become very valuable in this difficult time for banks, and they will only cut down on their expenses unless they are essential. Buying an upfront product license could be one of the causality of this delayed decision-making.

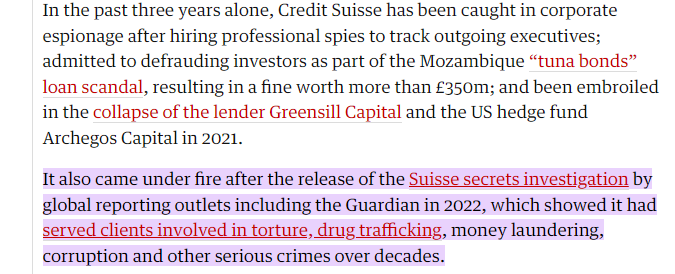

The European situation is slightly different, but Credit Suisse(CS) is making the situation unnerving for the financial market. [Lately, it was involved in one crisis after another.]. (Crooks, kleptocrats and crises: a timeline of Credit Suisse scandals | Credit Suisse | The Guardian). This is prior to the current accounting issues they are going through.

During a financial crisis, the weakest always get the most impacted and the strongest become even stronger. Although CS received emergency funding, it will be interesting to see how long it can keep itself away from further crises. European banks will also be facing a situation similar to what their counterpart in the US is facing, maybe to a lesser extent, as ECB rates have not increased. However, many of the European banks are also operating in the US, meaning they would have exposure to the US bond market and staring at billions of unrealised losses.

The US and Europe’s financial market situation won’t help Intellect. Mr Arun Jain had an ET interview yesterday, and I found it very interesting.

The anchors were interested in knowing the outlook and its impact on BFSI, but Mr Jain was marketing the Intellect AI tool and sidelines the question of impact. He was like a classic politician who says what he wants, irrespective of what the anchor (TV) asks.

If the financial situation is in turmoil, the banks would be keen to focus on their cash and cash reserve to preserve their cash, even if it is safe. This means they will delay the capex decision on purchasing IT software even if it is strategic to their vision. Banks can easily wait for a few months until the situation subsides. Companies like Temenos/Intellect are likely to suffer delayed decision-making, particularly selling on premised license products. Unfortunately, few win or losses define their quarter, as most of the license revenue flow to PAT. Due to the nature of the IT product business, a lot of deals are signed towards the end of the quarter. Due to this, Intellect is likely to have lower license revenue and lower PAT in Q4 and may be in Q1. Teminos has been suffering massive headwinds (CEO/COO/CFO, they are all gone in the last few months) due to lower take from banking clients, and this is before the current crisis.

A few clients might prefer to go on the subscription path for the Intellect cloud business, but it is unlikely to make any dent in immediate quarters as subscriptions take 3 to 4 years to really become profitable.

Banks will be very careful about buying licenses/subscriptions from fintech as they are facing their own challenges due to the drying up of funding. Bank will make sure that the product/subscription they are buying from will be in the market for years to come and will not disappear due to lack of funding. Even if the Fin tech product is good, banks are interested in the long-term nature of the product and will be keen to buy products from companies with solid balance sheets.

When Covid started, Intellect was breaking even, but in the two or three years, it has shown profitable growth with the balance sheet getting stronger without any external funding or debt. What could have been their weakness a few years back is turning out to be their advantage.

To summarise, there will be short-term headwinds for Intellect, but the current situation will help them in the medium to long term IMO.

Note: Long time invested

23 Likes