Chennai (India), September 21, 2022: Intellect Global Consumer Banking (iGCB), ranked #1 in the world for Retail Banking by IBS Intelligence, announced that the Cathay United Bank, one of the leading banks in Vietnam, has chosen to implement iGCB’s acclaimed digital credit platform – iKredit 360 to power the next growth stage of their lending business

As I understood from their concall they are now in process of transforming their solutions and client to cloud. Banking companies do not go easily on cloud and IT support/consultants and Technical analyst have to support these clients. Not every project is a new implementation/Upgrade.

We are positioned between the best of both- Thought machine(usability) and Temenos (depth of product)

GTD has good reference ability- 90+ accounts in GTD.

1200 people R&D team

All products have composability by using API, and products(Liquidity, core banking, lending, credit card) can be assembled using different API. Temenos does not have the common capability on open architecture for all products (they do lots of M&A)

Every few quarters, we will migrate a product into the platform.

Platform is sharp and country-specific, with 97% capability of the product.

Platform business DO NOT cannibalise the products business.

There are two types of customer

- who wants to invest upfront- go for a product license.

- Others prefer platform services.

Customers in the EU/US look for a platform. If the cost is substantial over ten year period, then they convert into licences plus AMC (AMC is 20% of license cost)

We try to make it a subscription base, but we are flexible

Underwriting Platform - Out of 300 insurance companies (in US), we have a lead of around 20 customers at the moment, and we are signing it off at an accelerated pace. - The underwriting platform is gaining a lot of traction in the US. Hence we are saying the US will grow faster this year.

Platform revenue is anything between 300k/per month to 1 million/month, but this is backloaded, meaning less revenue at the start and more revenue as they progress.

Product license cost USD 3 million over 10 years but in subscription, it is around 10 million… 3 times more than license revenue

Cycle time for the platform is 60% less than a product. If the focus is cost, then the client may be inclined to go with the platform stack.

Profitability:

- Travel cost up, Talent cost up, tax cost up (around 25%).

- Need to invest more in platform/R&D.

Our growth, compared to the competition (e.g Temenos), will be market leading. The organisation is geared for 20% growth. This growth requires investing in our IP and remaining relevant.

Will grow without diluting our capital.

When we launched the product iKredit/Auto, there was a powerful pull from the market; hence we launched the platform now. We could have delayed the investment but preferred to do it now.

Global Recession market-

- Nice businesses like us which cater to specific needs will remain relatively insulated. Our costs are small as compared to the banking budgets of clients.

- Some of the destiny deals (~ 60)- will come to know if they are getting funds by Nov.

Big banks are not delaying the decision based on the macro environment. However, the smaller player whose funding depends on the stock market may be impacted.

EU/US banks need to upgrade their technology to reduce costs.

Europe is ahead of the US in terms of cloud adoption.

America first wave of cloud adoption .

Europe- New core banking solution is in demand.

Asia Pacific- Product-based model

Middle east- slowly getting into cloud products but mainly product based.

Focus is to build deals in Europe, Canada and US. Noth America will be faster growth this year.

Gartner- look at the number of deals signed in the last 3 years. Forrester look at the product architecture. Hence we moved from Gartner.

Banks which have agility are winning in the market. Others are finding it difficult to traverse the market.

Best Matrix to look at it- License link revenue.

Product Implementation :

- Kept implementation in-house (Temenos is not the case)

- DID NOT Give implementation- We were building the brand earlier so keeping it necessary was necessary.

- Partnerships are becoming important.

Subscription-based revenue

- Suppose we book 1 million USD product- 1 million is shown in the book

- subscription- Only 3 months of revenue is shown for the product.

- Tier 3/Tier 4 customers are going for platform products.

-Bigger clients prefer for an upfront license.

Product Platform- Costs us $5-6 million/per year.

- First-year revenue may be around USD 1 million/per year

- It takes 6 to 8 quarters for the platform to break even (1 million to 6 million).

- When the platform revenue becoomes 30 million - my platform cost will be USD 8 million. That is when License link revenue will move into 65% range.

- In 3 to 5 years, we will generate around 30 million USD revenue (individual platform)

-GeM - we have reached 30 million as a number

Azure/AWS- Work in Progress. It may take 6 to 9 months before we jointly announce a deal

Why 20% growth aspiration- Inspired by HDFC Bank and focus is on predictability.

Dividend/Buyback- We want around 1000 cr in our book before we become aggressive on payouts. We should have the protection of 3 to 6 months of the cost structure. With 400 cr per quarter, we need around 3 quarters of cost taken care of. Hence we are looking at 1000 cr before being aggressive on buyback/dividend.

My take:

Overall next few quarters will be challenging as they are investing more into platform business. Considering that nature of the product business, it may impact their near term profitability if they fail to sign up customer. However, Intellect a world leader in their field across different products and kind the investment they are making augurs well in medium to long term. I am invested and my views could be biased.

CRISIL Ratings has upgraded the long term ratings on the bank facilities of Intellect Design Arena Limited (Intellect) to ‘CRISIL A+/Stable’ from ‘CRISIL A/Stable’ and reaffirmed its rating of ‘CRISIL A1’ on the company’s short term bank facilities.

The upgrade reflects CRISIL Ratings’ expectation that Intellect’s business risk profile will continue to benefit from higher market acceptance and maturity of its product suites, and its strong order pipeline (over Rs.6000 crores), which will ensure healthy double digit revenue growth over the medium term. Increasing share of revenues from cloud platform, Software as a service (SaaS) and annual maintenance contract (AMC), besides cross selling of product suites and new product launches, will support revenue growth. Operating profitability is expected to sustain at healthy levels of over 20%, driven by better cost absorption through expanding scale of operations, and increase in software license revenues emanating from continued deal closures. Earlier, in fiscal 2022, revenue grew by over 25% compared to previous year, driven by timely closure of digital transformation deals. Higher contribution from license revenues (7% higher over fiscal 2021) as well as SaaS and cloud revenues (112% higher over fiscal 2021) led to improvement in operating profitability over 25 % during fiscal 2022 (from ~24% in fiscal 2021).

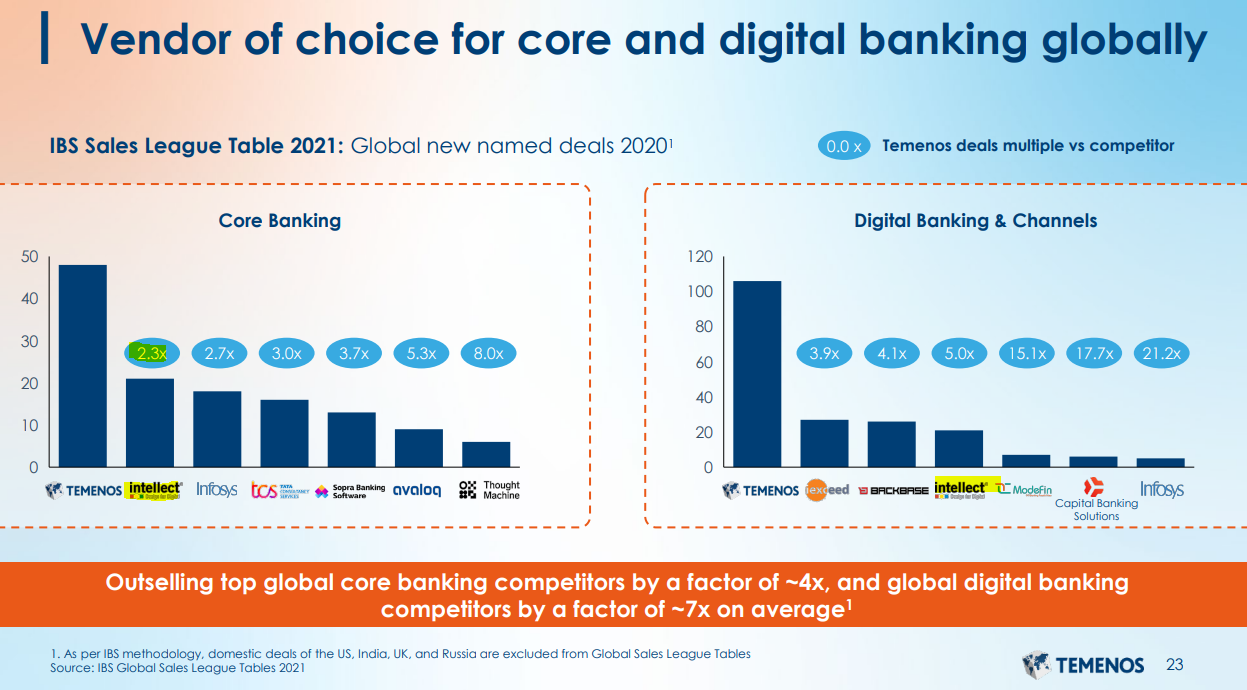

I found some snippets from the Forrester report from Teminos web site (available publicly after registration).

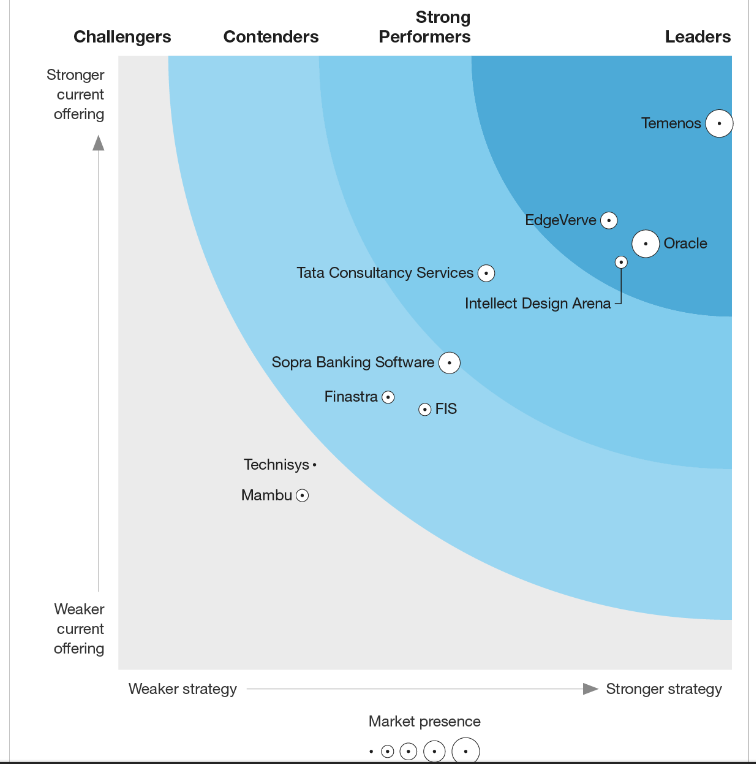

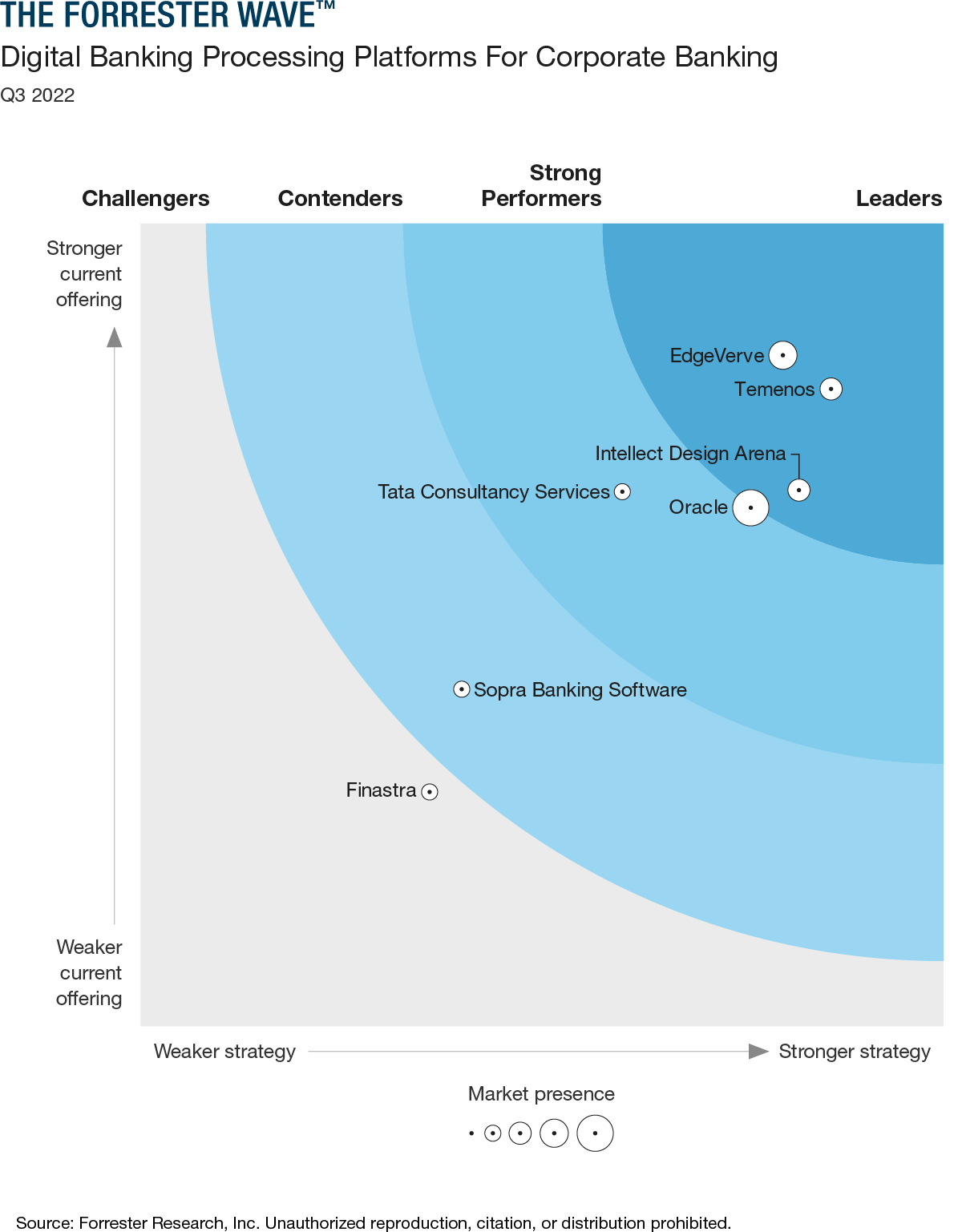

First- Retail Banking rating and comments from the reports.

Intellect has scored nicely on both reports (based on 2021 data). However, I think the Gartner data, which removed Intellect from their ratings, was based on 2020 data so the Forreseter report seems more upto data.

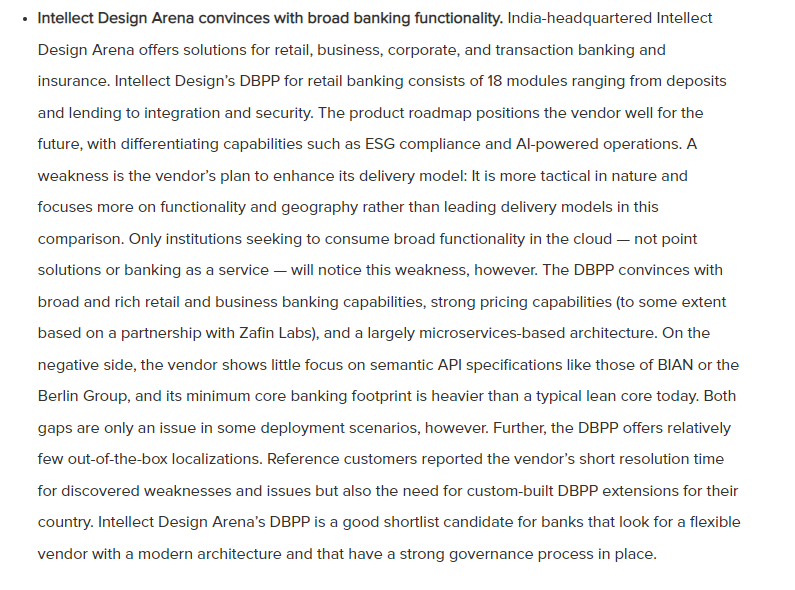

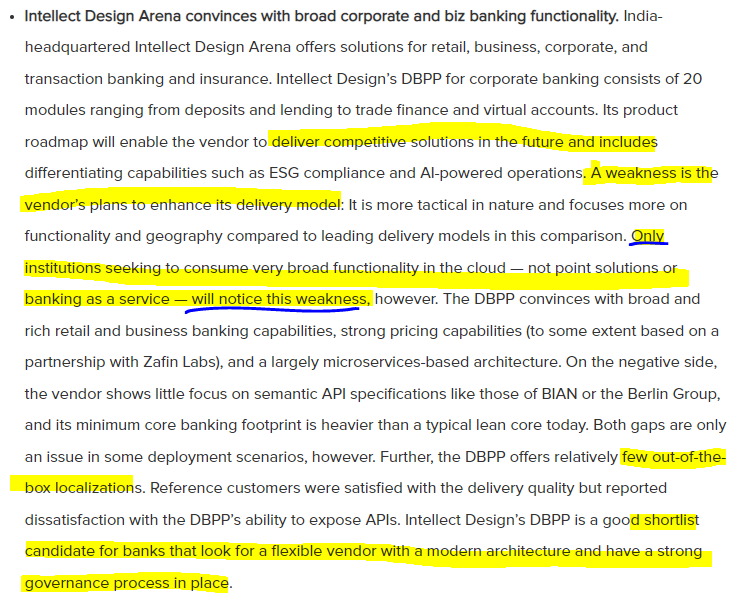

As we can see Intellect has a smaller bubble size due to less number of live installations. I think this should improve considerably in 2022 report (which will be published in 2023) as Intellect has won quite a few deals (assuming the trend continues). As Intellect improves live installation, it will enhance it’s reference, which will drive more product sales. IMO Intellect is well placed to win more clients in Retail and Corporate Banking products.

Note: Invested and Biased. You can see a snapshot of the report by going to Teminos site and register.

The information is very useful. I am new to the thread and have few doubts in the opportunity size of IDA… I want to understand the opportunity size of IDA. Like how much percentage of banks have moved from mainframe to cloud based platforms and how much are yet to migrate and what are the new sectors IDA could diversify outside BFSI… They do have 2 subsidiaries which focus on HR related software and another one is retail related…

As per Forrester’s report (above post), Temenos products have no weakness- rich in functionality, a large number of installations and Temenos investing a huge amount in R&D.

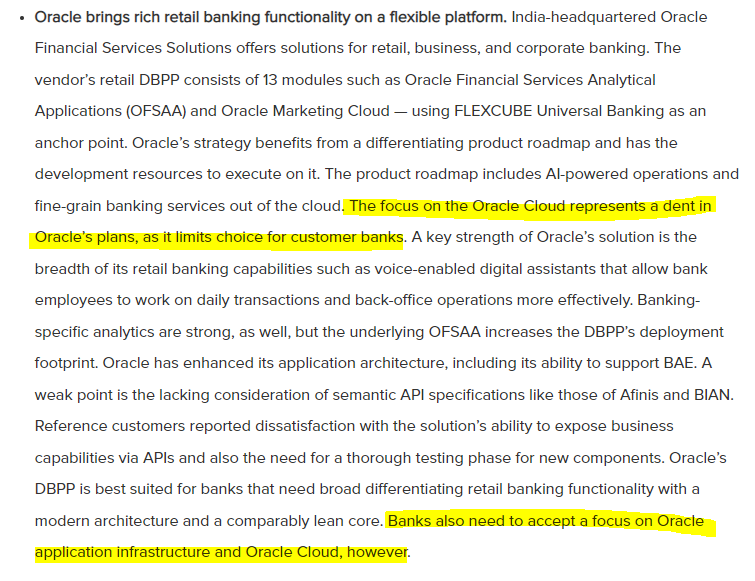

The report cannot say the same about Oracle (Oracle Financial Service). They have a number of Tier 1/2 clients and a large number of installations, but their product is a little behind in embracing the latest technologies. However, the major constraint - in my view- is that clients have to use Oracle Product/cloud if they want to use this product. This is a major game changer from a client’s perspective. If the client is already using Oracle extensively, then they are the major contender. Otherwise, Oracle is constraining clients’ ability to use the underlying platform (e.g AWS, Azure) of their choice. Also, Oracle is known to be extracting a lot of value out of their licenses (they are expensive), so from a client’s point of view, this is a major issue, and I get the impression that Oracle may be losing deals due to this cause.

Intellect’s products, on the other hand, use the latest technologies/architecture, putting them in a prime spot regarding technical capability.

Intellect has become (consistently) profitable only last year (Fy21). When a major bank wants to select a technology platform for their core business, amongst other things, they also look for the vendor’s financial stability. Large deals commit banks for the product for a number of years (maybe decades). For example, some of the major banks in the US are still using legacy IBM mainframes (30 + years old technology) for their core banking operation. Hence they want to see if the vendor can withstand financial difficulties and continue to invest in upgrading products. Until last year (prior to FY 2021), Intellect was barely profitable, and its balance sheet was rather weak. Lack of financial firepower could be their weak point earlier, but they have been reporting decent profitability for the last couple of years. So weak balance sheet may not be much of an issue now IMO. Mr Jain repeatedly mentions that Intellect is one of the fin techs which is profitable.

Even from the competition’s point of view, Intellect is rated very highly. In the 2022 Analyst day meet- Highly recommend, Temenos rated Intellect as the nearest competitor.

Future of technology is what you can read and understand. Company depends on promoter, market and employee retention. I would rather like it to go I-Flex way…

Few years back, Intellect was talking about Products. Last 3/4 years everything is moving towards clouds so they starting moving all of their products to clouds.

Looks like they saw success in Govt Platform, and now they are talking about moving all/most of their products to platform. So far they are talking about 6 platform, but soon they will be talking about more as they see the benefit.

In my view Mr Jain is technocrats and he loves developing more and more products. I think he has enough run way for Banking products so he is unlikely to go away from BFSI.

The magic invoice product/platform can be replicated to non financial sector- essentially it is reading the document, reading data and making senses of data. So they can venture into adjacencies but Banking have enough runway.

Microservices based approach using domain based modelling was a paradigm shift and the talk of the last decade. From product architecture standpoint they certainly seem on the right path.

Thanks to the members for amazing insights!!

I believe that Intellect is very strongly positioned today given the

• Breadth of its product offerings - High TAM,

• High quality of its product offerings - leaders accepting Intellect as a close competitor,

• Global reach well accepted by clients - derisks the business while ensuring growth,

• Improving financial strength - increasing cash on books,

• Stable management bandwidth – to manage growth.

What it lacks is the belief from investor community about the stability and predictability of its business and financial performance.

Frequent changes in its guidance on business format (product-platform-eco system-to what not) as well as financial metrics do not help.

It will take some time to erase these elements.

100%+ conversion of EBITDA into operating cash flow

Expected FY 2022 tax rate of 18-20%

For reference, the previous guidance was as follows:

ARR growth of 18-20%

Total Software Licensing growth of 16-18%

Total revenue growth of at least 10%

EBIT growth of +9-11%

100%+ conversion of EBITDA into operating cash flow

Expected FY 2022 tax rate of 18-20%

Q3-22 business update

Lengthening sales cycles linked to a number of large deals in the pipeline, subscription revenue of USD 17.2m significantly below expectation

Banks more cautious in their decision making given future macro economic uncertainty

Term license revenue of USD 16.6m in line with expectations, mainly driven by deals closed early in the quarter that had not moved to the subscription pricing model

Sales execution also impacting deal closures; action on sales leadership taken, the Chief Revenue Officer has left the business effective immediately

Accelerating growth in SaaS revenue from mix of new business and additional consumption from existing clients, with no visible impact on decision making by non-incumbents and smaller banks from macro economic uncertainty

Good growth in ARR in the quarter, up 16% (c.c.)

Services returned to growth this quarter, still impacted by accelerated shift to partner model

Cost increases driven by combination of wage inflation and increased services costs driven by incremental partner costs around a number of implementations

Underlying operational costs in the quarter were as expected

EBIT decline of 53% impacted by lower subscription revenue and cost increases

FY-22 guidance revised and de-risked to reflect macro impact, sales execution and services costs

Revised FY-22 guidance (constant currency) of ARR growth of 17-18%, Total Software Licensing growth of 0% and EBIT decline of 25%

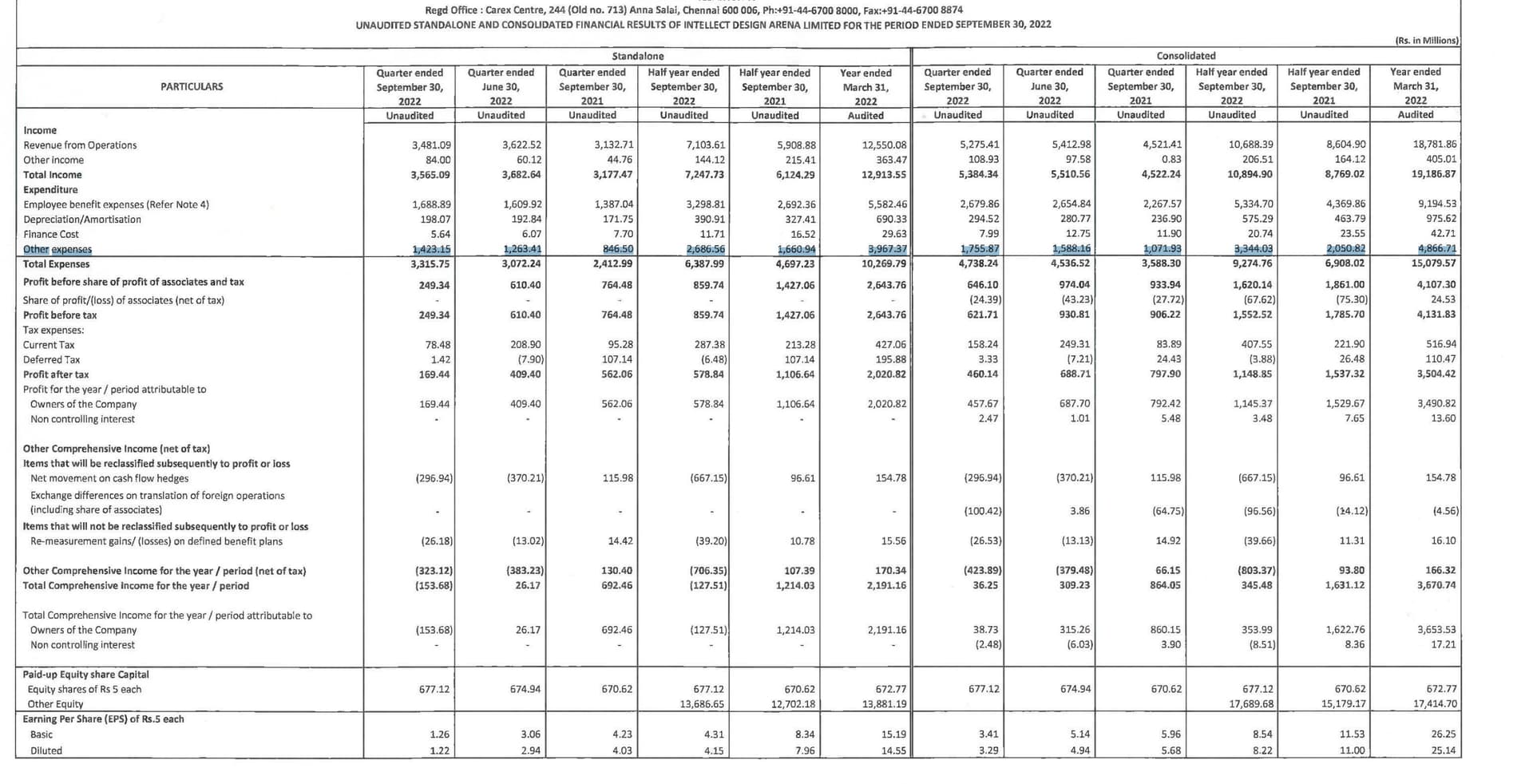

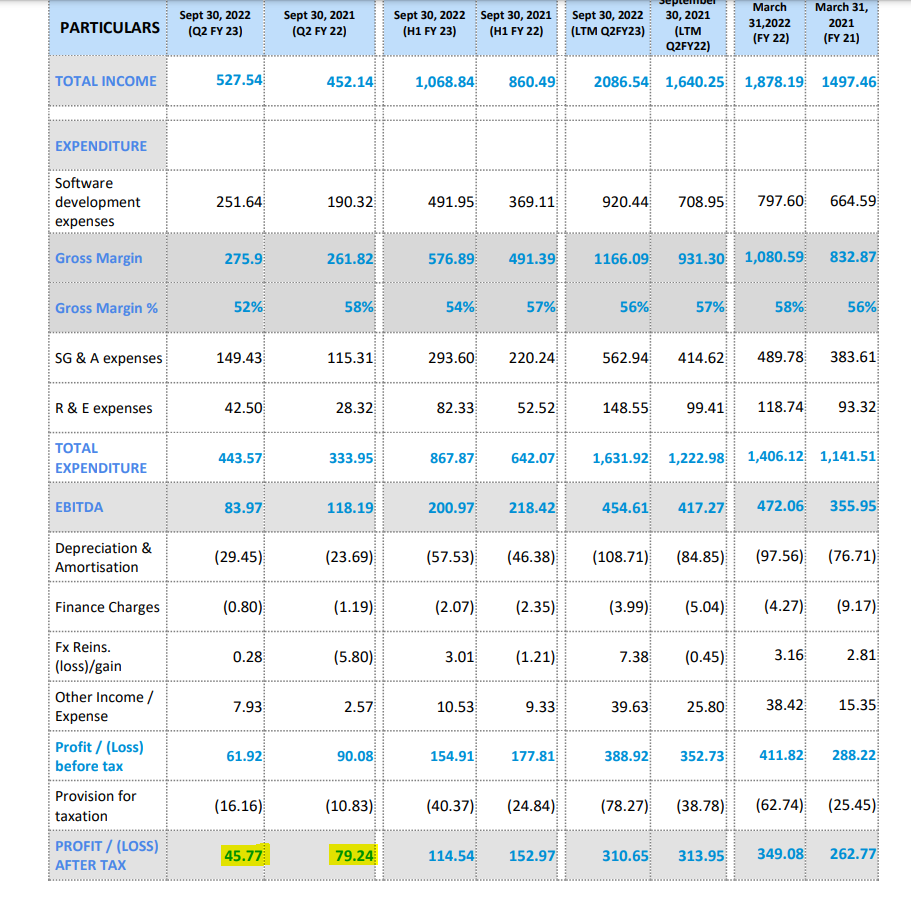

Based on the earlier commentary, I thought it could be bad, but PAT of less 50 cr is really disappointing. No wonder they posted results after market hours on Friday.

IDA announced the Q2 Results, I attended part of the Investor call today (dropped off at 6.10).

Results were disappointing, but we can not look at product companies like we do for service companies, revenues will be lumpy. However one major concern is the margin drop, and reduced margin guidance over the last few quarters, need to watch this carefully. Arun does tend to be a bit of an optimist, but he would not have built this product and business if he were a pessimist or even a realist !

Arun started with acknowledging that investors would be disappointed by the quarterly results, but he underscored that IDA has consistently talked about looking at a longer timeframe, and the right lens is LTM trend which is encouraging.

Revenue Shortfall was about $6 Mn, costs were inline. There was a Deal worth $2.9 Mn, but it is a Platform deal so only 100K was reflected and in subsequent quarters also it will be similar, so . Another 3.1 was from a deal that closed, but not contracted by sept 30, hence not reflecting in the results.

Macro Cost pressure- Decision making is slowing down, Cost structure remains high, Tax rate increasing from 16 to 25 %.

Unbilled revenue related analyst report- Clarified again, milestones based revenue recognition happens, due to this there is Unbilled revenue.

Revenues & Margins

Revenue Growth expectation is still 20 %, this quarter was an aberration. More platform deals will lead to lower optical revenue growth. Typically 20 with variation of 5 % is quite likely.

EBITDA margin expect 20 % + for the full year, cant commit to 24 % which was the historical margin. This is the second reduction, earlier they had moved form 30 % to a 25 % estimate, now it is 20 %. Need to watch this.

Cost base is now normalized- People, travel and infra are done. There will be additional hiring costs2-3 Mn / qtr for senior sales/marketing people.

R&D $ 20 Mn/qtr( Rs 150 Cr), capitalize 25 %, and expense the rest.

Target of $ 100Mn runrate in 8-12 quarters, no projection on margins due to market volatility, but expect it to be better in future.

Products & Platforms

Wide Window Moment-Exciting revenue growth with these products in phases led by GTB then 2nd wave GCB and 3rd wave Intellect AI (SEEK+Wealth Mgmt)

ESG win against American and European companies - No revenue for this quarter, but is lead indicator of future prospects.

Core Banking- Now credibly competing with Temenos, ThoughtMachines etc on high value Destiny deals, and have left OFSS, Infy-Finacle, TCS-Bancs, Finastra behind esp in Europe market.

GTB- Consumerization of Corporate banking with Business one one side and End consumers on another eg Uber and Drivers

Implementation cycle time going down with iTurmeric, this reduces implementation revenue, but accelerates cross sell. Lic:imp was 45:55 now is 70:30 , and Lic is a higher margin business compared to implementation. Earlier implementation time was about 6 months, now is 2-4 months.

GCB and GTB both have big opportunities ahead based on the TAM. Startups are burning investors money, IDA is still going for organic growth. Data Opportunity is big for the platform business.

Disc: Invested since a long time and adding on dips at reasonable valuations. IDA has definitely out-executed OFSS and Nucleus, both of which I hold in small amounts and track as peers to IDA.

I feel the numbers are bad and the next two quarters will look weak too on a YoY basis. However, I also feel that (based on guidance), numbers should begin to improve sequentially from here on. If one has a slightly longer term horizon (say 2-3 years) it seems quite interesting.

Pipeline has held up well; 2) Platform revenue is already higher than license revenue (thus impact of that transition or mix change on growth and margins would be lower in coming years); 3) Growing market segment and Intellect’s product acceptance within it; 4) Margins should pick up as costs woulnt rise in line with revenues.

Although, margins would be volatile becuase being a product company they will have to keep re-investing because if they dont a new competitor will do to them what Temenos did to the likes of OFSS or ThoughtMachine is doing to Temenos. Margins should pick up but improvement should be more gradual and probably settle in mid-20s (thats just my guess) than in 30s.

Thats my read - would request other members to share their thoughts if they have contrasting views.

One of the twitter experts keeps on criticizing the management. I have read about the case of insider trading which seems to have been settled after due payment of fine.

Does anyone else know of any ‘Red Flags’ for the management apart from that?

I very much said that its my read and my “guesses”.

However labeling it as “hope investment” without discussing/understanding the other person’s arguements also is quite ignorant.

Just to share my reasons on why numbers could possibly improve from hereon: Full year EBITDA margin guidance of 20% - for them to achieve that (or even come close to that), margins should pick up sequentially; Furthermore, the higher investment in platform development would ease up a bit; we would also have a higher revenue base. Looking further out, a gradual margin uptick in a product company is expected (as development costs are much lower and already developed products earn incremental revenue and margins with lower investment).

As I said in my original post as well - no way there is a gurantte for a steady margin rise but seeing history of Temenos that played out. This is my read as I look at it for next 2-3years. How next quarter or next 2/3 quarters play out is impossible to guess ofcourse.