They look like employees who are constantly cashing in on ESOPs

3 Likes

Breaking out of a 12 month consolidation band.

Good to see that the up move is backed by solid fundamentals.

Disclosure: Invested from lower levels and added more during last few months.

AJ

3 Likes

Intellect bags a major transformative deal from VPBank!

7 Likes

Looks like Intellect will start paying dividend

4 Likes

- Decent results. YoY Growth for Q4 Fy22 vs 21: Revenue 28%: Growth for AMC 14% and SaaS 84%, License reduced -6%.

- EBITDA Margin 23.7% (was 25 %) ,PAT: 25% Margin pressure is still there on account of employee costs, though seems to be flattening now.

- Total Product development capitalization is same as last year 115 Cr.

- And they have declared a dividend of 2.5 which is good.

- Four Destiny deals won, of which two were in the 50 Cr+ category. Two deals lost out of the total of 57 deals, which is a good sign, but also a reflection of how slow the decision making is for these deals.

Investor PPT: https://www.intellectdesign.com/investor/intimations/Intellect-Q4-and-FY-22-Investor_Deck.pdf

I missed the Conf call due to a work meeting, did anyone attend and can share the updates ?

Disc: Invested since a long time and adding on dips

3 Likes

Few notes from the concall:

- They now are capable of converting 50 million dollar deals as shown with the rbi. Converting these new deals needs almost a full village of people. Hence why head count and employee costs has been increasing and will continue to increase. However, they are not as dependant as other service based companies for head count so it won’t be as high as industry level

- Strategy continues to be to enter a country and target top 3 banks in that country and then use that as proving point and move into smaller banks

- Moat that is developing is that while usually the process of transforming a bank takes 18 to 24 months that have spent on design thinking and have now brought the time down to just 6 months. Noone else can do this atm

- MS azure could have picked anyone on the planet… yet picked IDA. Collaboration will help

- They confirmed the loss of a big deal regards a Russian bank in Germany plus a smaller deal in Ukraine. These deals were never placed on the balance sheet though so will not lead to any tangible losses. Just that the revenue would have been 4 million higher had they booked the Russian bank deal.

- Even with current macro factors they are comfortable with continuing to target 20% growth. Targeted 20 for FY 22 and hit 25 percent

- License linked revenues crossing 1000 crores was a big milestone.

- Tax rate will be at 26 percent next year. They can no longer show cumulative losses

- Overall margins and profits should not be looked at QoQ since the business is a product based business and if a big deal is booked in one quarter it will obviously show higher vs other quarters. Have to look at the business on a YoY perspective.

- Lots of deal wins … these are mentioned in the presentation so i won’t type here.

Note: As is the case with almost all IDA concalls the management and investors seem to be on different wavelengths so i usually leave the call after Mr. Arun Jain speaks. For eg… after everything said above by management regards projections for FY23 and regards not comparing quater on quarter the first questions after Mr. Jain mentioned all of the above was , "What is your target growth for FY23 considering the macro situation? Can margins of Q4 be extrapolated for every quarter? Q4 this vs Q3 that etc? " …

So i may have missed some things later in the call lol

Disc: Invested. Top 3 allocations in my PF. Not a sebi advisor

13 Likes

Not sure how going back to 26% tax rate will affect the stock negatively or not

Otherwise the company seems to be a doing a decent job and their business structure seems better suited to manage attrition of the tech talent.

@Wizard_apprentice

This was expected to happen though… and could be easily calculated considering cumulative losses… so should be baked into the current reasonable valuations for a product based company. It’s the unknowns that could derail the stock price(That being said in this current environment anything could derail a stock price). Main unknown for me was regards ukraine Russia… and I’m very satisfied with their answer regards that.

They did mention regards how they will still be charged 17 to 18 percent tax on their cash balance for a reason i can’t remember. And that bigger players will suffer more due to Russia Ukraine and interest rate rises while they won’t. So listening to the entire concall recording may help Clear some minor doubts.

I would also recommend listening to the concall to understand how they are creating their 6 months vs 18 months project completion via design thinking moat too and how they target top 3 banks in a country and leverage that to move to smaller banks+ how they handle sales for 50 million dollar deals and have the capability to continue doing so in the future. Fantastically explained in the concall and just a small note by me doesn’t do it justice.

4 Likes

yeah and they are not guiding but hinting at aiming to grow ebit at 30% and revenue they are guiding 20% but can shoot to 25%. The SAAS based model also helps them scale up while keeping the costs somewhat same .Considering those numbers and now that they are moving to bigger deals, decent cash conversion cycle. The fact that so many banks are trusting them and they have been able to cut the delivery time by half is a great advantage too. Considering those facts the company seems reasonably valued if not cheap .

Just would like to clarify one aspect … collaboration with MS for Azure hosting is a standard stuff and every other provider has established that relationship. Most of the providers are cloud agnostic and can be hosted in AWS, Azure or GCP.

Partnership with Azure is only going to help them have lower cost on Azure components which is also a standard industry feature and not any competitive advantage.

13 Likes

Thanks for the concall updates. I’d created some charts to visualize data, Posting the updated data with key insights, hope it’ll add perspective to the thesis.

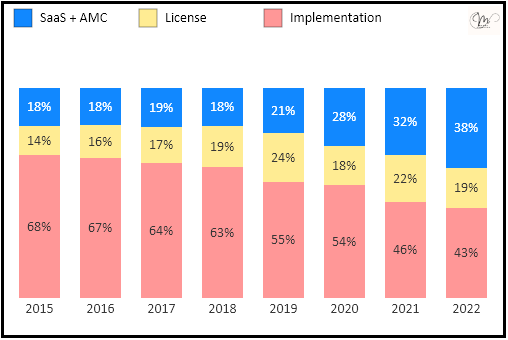

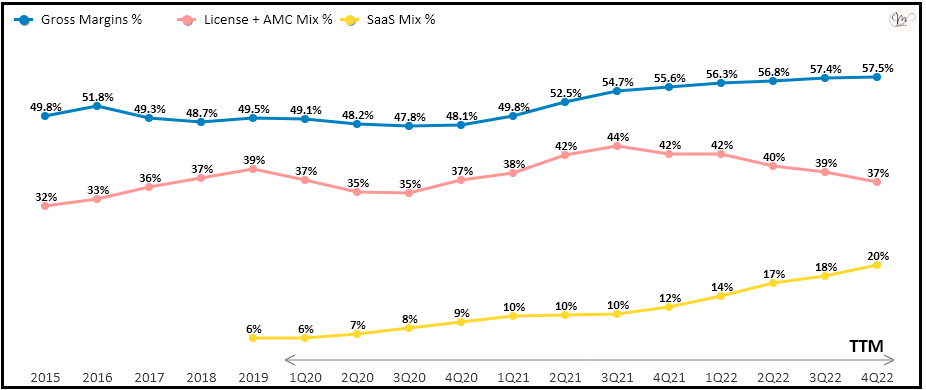

- Recurring Revenue Portion is increasing which is the major part of thesis in Intellect. Hopeful for it to reach 55-60% of the total in next 5-6 Years.

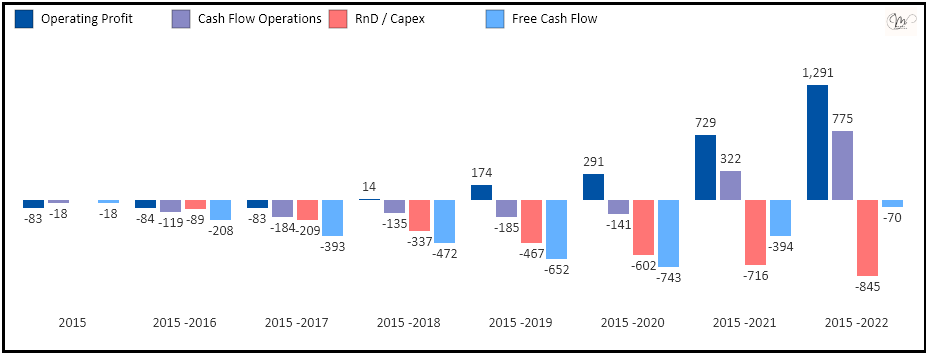

- Cash Flows are getting better each year. Below shows cumulative profits vs CFO vs FCF since 2015. FCF has also started growing as the RnD expense is constant.

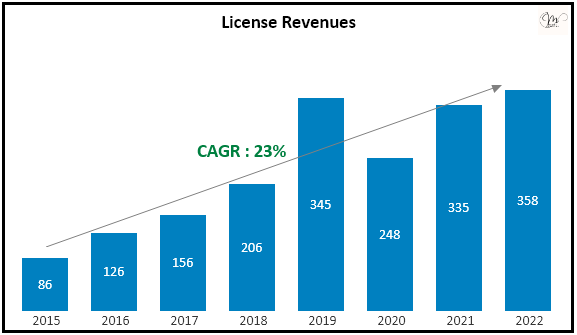

- License Revenues Growth has slowed down as Cloud / Subscription is taking part of the pie, Still maintaining a decent CAGR over the years.

- Excellent Growth in Recurring Revenues over the years and continuous 8-12% QoQ growth since last 5 Quarters.

- License Linked Revenue in % Mix is ~ 57% with Increasing SaaS in that Mix, causing the gross margins to inch towards aspirational 60% in upcoming years.

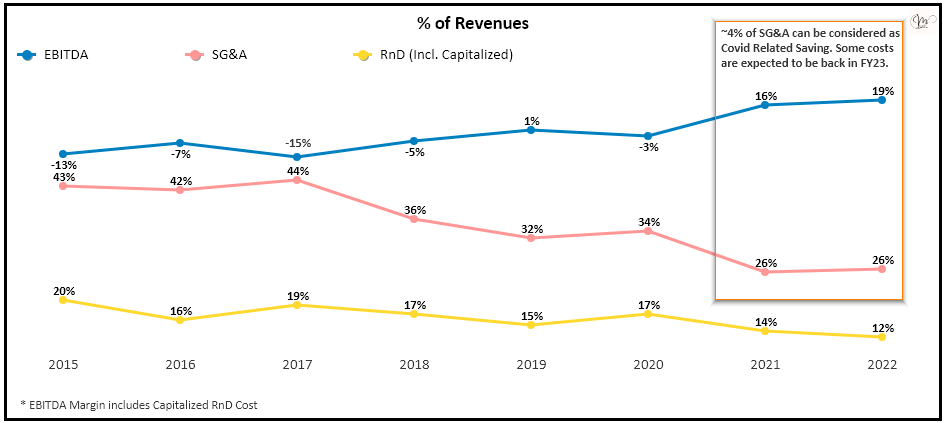

- Other Costs are continuously declining as a % of Revenue leading to operating leverage. However, around 60 Cr. in FY21 seems to be Covid related saving which can cause SG&A and EBITDA margins to look optically higher currently and can adjust ~3-4% if the costs will be back.

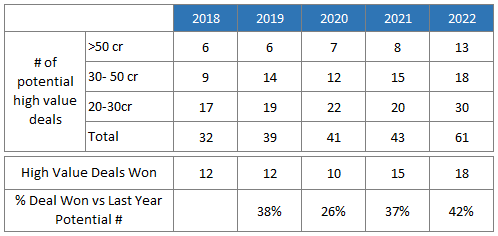

- Lastly, the # of potential deals has increased to 61 with % ratio of winning deals as 42% for last year’s potential. If the trend continue, it can support the growth targets mentioned by management.

28 Likes

agreed - nothing special here.

Disclosure: Not invested

- I liked the fact that intellect is serving the crème del a crème of the Indian banking sector including RBI (RBI in a Rs 400 Cr deal). The company has also made inroads into the top tier in multiple economies in both the developed (Europe, US and Canada) as well as developing (MENA, Malaysia etc)

- intellect has 12 products, 5 platforms over 4 technologies. Target market increases to near infinite levels basis this kind of product bouquet

a. the fact that Microsoft has chosen intellect as its partner for GTB not just means validation from the highest levels but business flows as well. - The management has been categorical about designing the organisation to a 20% revenue growth and a 30% ebitda margin. It’s achieved the former but failed the latter. I find it difficult to assume that this 20% growth in revenue can become 35% and the 30% ebitda can happen when the actual was 25%

- The other point is the company consuming its b/f losses resulting in the tax rate going up to 26%. This would consume a significant part of the PBT growth going forward. However, on cash basis the impact will be 18% due to available MAT credits

- From a PE of 38~ its come down to 26~ at present. So, at a PE of 25x with 25% revenue growth and 27% EBITDA margin, the price comes to 765

1 Like

My understanding is a little different. MS cloud has its own Banking team for selling its cloud… They will exclusively sell only GTB… As explained in the call

2 Likes

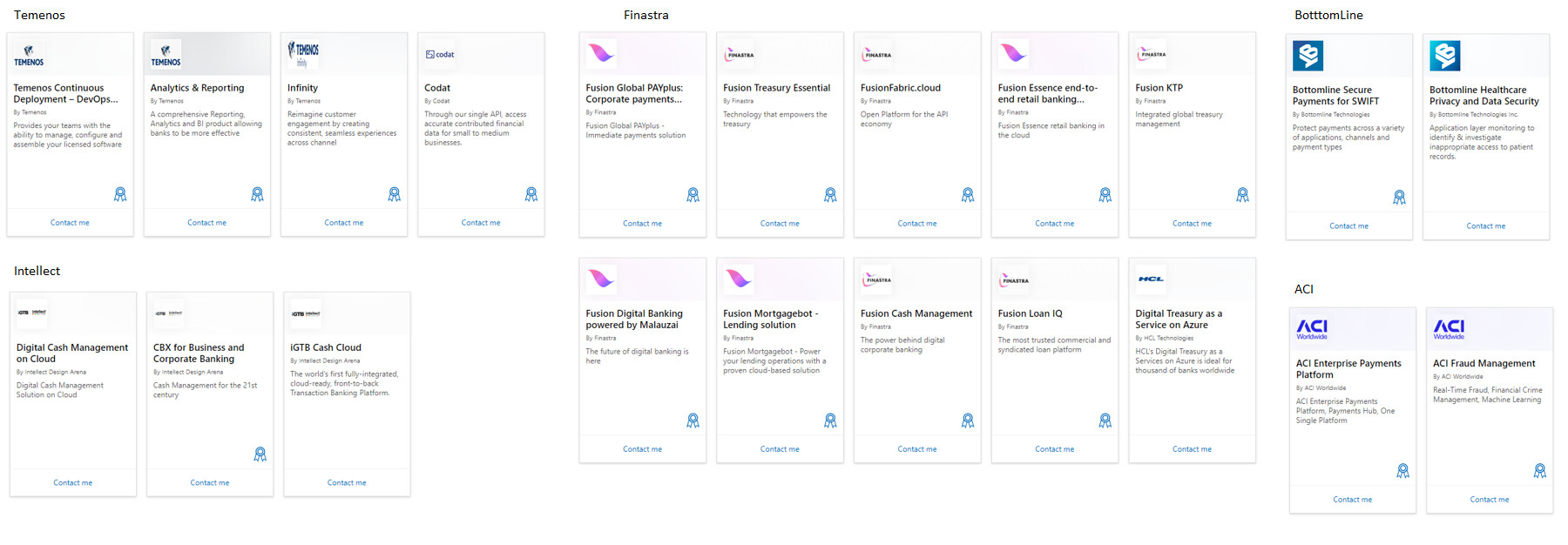

All major competitors - Temenos, Finastra, ACI, Bottomline are partners with Azure and similar products are listed / promoted by azure on their marketplace. Though, it is a good thing for Intellect and will improve it’s visibility in market but not sure about the exclusivity part.

Data is from Azure market place site : https://azuremarketplace.microsoft.com/en-us/marketplace/apps?page=1&search=transaction%20banking

5 Likes

I was part of FInastra and we have got customers hosted on Azure but services managed by us for our clients. Finastra and Azure has got organization level tie up and Finastra is a much bigger firm than IDA.

There is no exclusivity that they can sign because anyone can utilize Azure to host their applications. Additionally, we have partnered with MS to pitch for RFPs where MS solutions and Finastra solutions would complement each other. Obviously, i cannot tell the client name and the outcome of the proposal submission

And an additional insight on the sales cycle : Infrastructure providers like MS or Amazon should have basic banking use cases supported in their solution since that increases their proposition for that industry. However, they are not involved at the start of discussion with banks. They are mostly just an infra provider with each bank having their own choices (some are very keen on Azure, some on AWS). The evaluation is done on the strengths of application provider and providers who have multi cloud support have a slight edge (if customer cloud preference is hardwired). Additionally, quite a few big banks have multi cloud strategy and with evolution of Core Banking as a Service, they may have their Core banking on Azure but DWH in GCP and their other applications on AWS.

To summarize, i dont think they have exclusivity and even if MS pushes IDA solution, there would not be too much of an impact on the sales cycle because of MS push because other providers can also use same infrastructure.

15 Likes

Very difficult for me to understand the business of Intellect design arena. Is there any simple way to understand the business of such company. I do not know what is Saas or analytics or cloud?

1 Like

@thakurvi If you really want to understand the business then you’ll have to understand these technical terms. Otherwise your understanding won’t be complete.

That being said, I think understanding these terms shouldn’t be that complicated. These are just some big buzzwords and sound really complicated, but if you go to understand these terms individually you should be able to do so in a week or so if you put in a couple of hours worth of research a day. (Google and YouTube are your friends if you want to do this.)

Then after that, just read the last few investor presentations & concalls and see if your understanding has improved.

Rinse & repeat afterwards.

If you think this is too much of a hassle, then there must be other businesses which lie in (or near) your circle of competence. You can study those - you don’t have to understand each and every business under the sun.

8 Likes

Does anyone know why there are different CEO’s for each business? And how is the company making decisions?