Innovative Tyres and Tubes Limited (ITTL) is part of the reputed Innovative Group, one of the leading manufacturers and exporters of Bias Tyres in India, with experience of 20 years in manufacturing field. ITTL offers a wide range of products in the Truck / Bus, Agricultural & OTR and Motorcycle / 3-wheeler segments. The company has two manufacturing units- Innovative tyre plant and innovative tube plant- which are located very close to each other. Innovative Group is a diversified business house catering to the automotive market. The group comprises of three companies- Innovative Tyres and Tubes Limited, Future Tyres Pvt. Ltd.and Gaia Batteries Pvt.Ltd.- spread over 4 manufacturing units located near to each other. The group is set to welcome two entrants- Green Batteries Private Limited and Green Tyres Private Limited, both part of a joint venture with Greenfield Inc., part of Nepal-based Vishal Group to cater to the dynamic Nepal market for tyres as well as batteries. Based in Kathmandu, Vishal Group is a business house with interests in a plethora of market sectors-FMCG, education, insurance, hospitality and cement and steel, to name a few.

BUSINESS

Incorporated in the year 1995, we are a tyre and tube manufacturing Company, manufacturing & marketing our products under flagship brand ―Innovative. We started our journey with the acquisition of a greenfield project situated at Halol in auction from Gujarat State FinancialCorporation and State Bank of Bikaner & Jaipur vide agreement dated December 15, 1995. There after we revamped the closed company to our tube manufacturing facility at this property and started manufacturing of tubes in the year 1996. Within a short time after our inception, we were able to successfully get our facility approved by CEAT Limited for carrying out job work activities for them.

As a result of strong business relationship with CEAT Limited, taking the relationship to the nextlevel we set up a greenfield tyre project as a major outsourcing unit in 2003 in a close vicinity of the existing first tube plant in Halol only. While our tube manufacturing facility is spread over 11,200 sq.mtrs, our tyre manufacturing facility occupies an area of approximately 27,833 sq. mtrs. We have an installed production capacity of 12,000 MT of tubes and tyres. We also have a factory outlet for display of our products at Vadodara. The product wise quantity sold during FY 2016-17 is :- Two Wheeler: 3718 MT, Light Commercial: 2343 MT, Truck Segment: 3013 MT and Agriculture & ORT: 669MT.* *includes quantity manufactured on jobwork basis from our group company Future Tyres PrivateLimited.

Company has planned a capex of Rs. 21 cr (Rs. 17 cr from IPO and Rs. 4 cr. from bank) on existing land for manufacturing of OTR, Radial Agricultural Tyres and Tubes. Company plans to start commercial operation from this capex by June 2018. Company intends to expand it’s manufacturing capacity by 8000 MT p.a.

Company has done some interesting work in the past 3-4 years. In 2015 company became the first Indian tyre manufacturer to achieve the PNS Quality certification from DOT, Philippines. In FY17 sales to Philippines were Rs. 21 cr. (15.99% of total sales). In 2016 company entered into an agreement with Gabriel India Ltd. and became the sole manufacturer for their tyres. In 2014 company started manufacturing OTR and tubeless tyres.

MANAGEMENT

Company is promoted by Mukesh Desai and Pradeep Kothari. While Mukesh Desaihas been associated with the Company since its inception, Promoter Pradeep Kothari became a par ot of Company in 2014. Mr. Pradeep Kothari and his family holds 20.51% shares in the company. He invested in the company in 2014 and was then appointed the additional director. He is the driving force of the company in past 3-4 years and is guiding the company in it’s latest expansion and export sales. Mr. Mukesh Desai is responsible for overall management and Mr. Nitinbhai Mankad looks after government work, legal work and new business development.

FINANCIALS & VALUATIONS

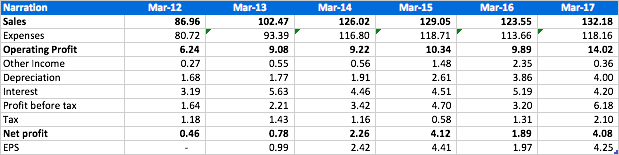

After the IPO the outstanding equity share capital of the company is Rs. 17.99 cr (17991561 shares of Rs. 10 each), Net Profit for F.Y. 2017 is Rs. 4.08 cr. Diluted EPS for FY17 is Rs. 2.26. From FY14 to FY17 company has not shown any growth in sales but operating profits has grown from Rs. 9 cr. to Rs. 14.02 cr at 14.99% cagr. With the coming capex management in it’s prospectus has guided for Rs. 200 cr. sales in FY19. At current price of Rs. 50.30 the MCAP of company is Rs. 90 cr.

Company has shown good sales growth in the domestic market in recent years.

With little sales growth in past three years and low ROE of 11% in FY17 valuations are in line with the peers. Shift from bias-ply to radial tyres with the upcoming expansion and management guidance of sales growth will have to be watched carefully for future earnings growth.

IPO

Company raised Rs. 28.33 cr from the market through issue of 6297000 shares at Rs. 45 each in September 2017. Utilisation of Proceeds:-

Expansion Rs. 17 cr, WC requirement Rs. 4 cr., General Corporate Purpose Rs. 4.83 cr and IPO expenses Rs. 2.50 cr.

Risk

- Shift in Indian tyre market from bias-ply tyres to radial tyres pose a threat to company’s performance as company manufactures bias-ply tyres only. Though the company is making new capex in radial tyres.

- Promoter Holding is low at 24.32%.

- Job Works constitutes 24.62% of total sales, it may not be able to pass on the increase in prices of raw material.

Other Points

- Out of the total revenue for the FY 2016-17, revenue from CEAT Limited contributes 11.37%.

- Company has entered into various transactions with Promoters, Promoter Group,Directors and their Relatives and Group Company. Further, purchases from Group company/Promoter Group Raman Enterprises and Future Tyres Private Limited was 8% and 5%of our total raw material purchases for the year ended March 31, 2017, 17% and 2% of our totalraw material purchases for the year ended March 31, 2016 and 28% and 3% of total purchases for the year ended March 31, 2015.

- We also outsource manufacturing of two/threewheeler tyres to our group company Future Tyres Private Limited and job work charges paid tothem on such account was Rs. 177.64 Lakhs, Rs. 329.17 Lakhs and Rs. 102.91 Lakhs for the yearended 2017, 2016 and 2015 respectively.

- Export order book as on date of prospectus is of 3359.49 MT to be completed by June 2018.

Disclosure: Invested, less than 2%.

Links:

Prospectus