CMP 102

Marketcap 280cr

Overview of Innovassynth Investments Ltd

Business Model:

Innovassynth Investments Ltd serves as a holding company, deriving its income primarily through dividends from its stake in Innovassynth Technologies Ltd.

It has no direct operational products or services.

Stake and Operations of Innovassynth Technologies:

Innovassynth Technologies operates in R&D, CDMO, and specialty chemicals.

The company runs a 70-acre facility in Khopoli, Maharashtra.

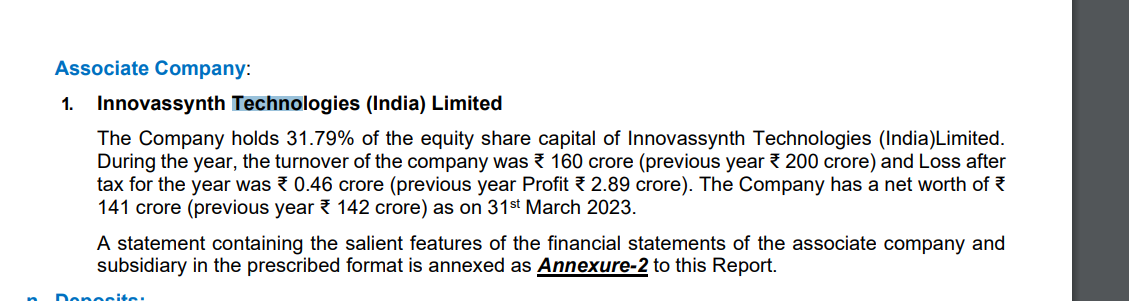

Financial Performance for Innovassynth Technologies

Revenue:

FY 2022: ₹200 crore

FY 2023: ₹185 crore

In FY 2022, Innovassynth Investments Ltd received approximately ₹15 lakh in dividend income from Innovassynth Technologies.

Leadership and Management

CEO: Hardik Joshipura, an industry veteran with prior experience at Merck, was appointed two years ago to lead Innovassynth Technologies.

The Rajan Raheja Group oversees the operations after acquiring the company from the original promoters, the Ghai family.

The plan, as per the announcement, is to implement a reverse merger, absorbing Innovassynth Technologies into the listed Innovassynth Investments Ltd. Post-merger, the promoters, the Rajan Raheja Group, are expected to own approximately 72% of the consolidated entity.

Details of the Merger/Reverse Merger

Current employee strength of 600 in Innovassynth Technologies with Facility in Khopili and recently in Pune

Interestingly, Rakesh Jhunjhunwala initially held a stake in the firm back in 2010. This stake was later transferred to Utpal Sheth, his right-hand man and the current CEO of RARE Enterprises, Jhunjhunwala’s investment firm. Utpal Sheth is also the founder of Trust Mutual Fund and owns approximately 12% of the stake under the name of Chanakya Services Ltd.

The primary promoters, the Rajan Raheja Group, are also associated with other prominent companies, including Exide Industries, Supreme Petrochem, EIH Associated Hotels, and Sonata Software.

From a technical perspective, the counter has shown significant volume growth and price movement over the past six months.

Regarding the merger and its post-merger valuation, it is anticipated that the consolidated entity will generate approximately ₹200 crore in revenue, as stated in the IRCA report.

As per the listed entity they have already applied for NOC to BSE and next step will be NCLT which might take around 12 month

Clearly the management has improved its outlook to the company and focus on business which is under Innovassynth Technologies but how would it translated to Innovassynth Investment and merger/post merger

The future outlook also hinges on the management’s vision(promotors), which clearly reflects their ability to handle multiple priorities effectively. The group has consistently demonstrated strong performance across its portfolio companies.

Open to further discussion and perspectives.