yes , I see merit in your point in recent buy back. IT stocks are still under pressure due to various reasons.

But when we talk long term of 10 years , we need to evaluate for all the past 10 years, though I don’t have ready made data to mention here.

Anyway , it is a personal choice. i am comfortable both in large and midcap.

You have a valid point.

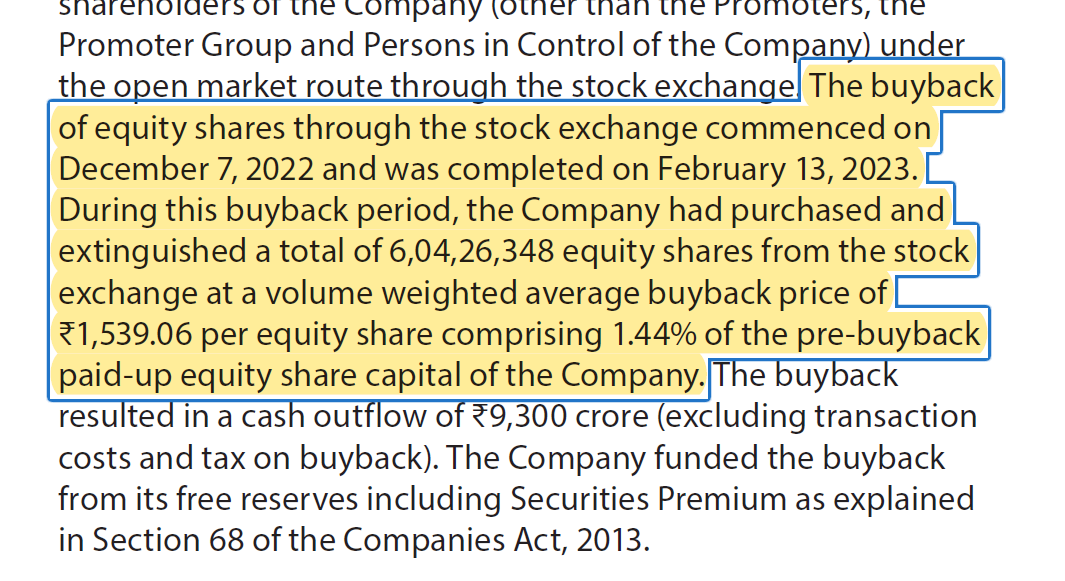

Infosys did declare the buyback with a maximum cap of Rs.1850 per share. However, as per 2023 AR page 305, they ended up executing the buyback at Rs.1539 per share.

If we look the period when the buyback was executed (7th Dec’22 to 13th Feb’23), the stock traded at ~ Rs 1560 → went to Rs 1470 → Back to Rs 1560. Considering the average buyback was executed at Rs 1539, I think the company did not overpay.

The question is not at what they prices the ended up buying but up to what price where they comfortable buying at? Had the market not obliged and prices in general trended up, they would have indeed ended buying at closer to the indicated cap of Rs1850. And in that context, one should question if the Rs1850 was a prudently low enough valuation in relation to long term valuation range and upcoming earnings outlook (which turned out to be weak and the market already pre-empted) - buybacks are great value when done at attractively low valuations and only in that case they add value to the non-selling shareholders. Otherwise, they are little else than theatrics - help to support the stock, reduce share dilution via ESOPs and return some cash to selling shareholders at the expense of non-selling shareholders.

I wonder when the management was ready to pay up to Rs 1850, what was the intrinsic value as per them and also what growth, discount assumptions they used.

Has deep ties with many hot AI product companies in US

Twilio - Infosys has a competing solution called Cortex

UIPath - all indian vendors have tie ups, but Infosys has deeper ties (3500 trained engineers)

(ARK has invested in Twilio and UIPath)

Just wondering what explains this consistency. (Pedigree and continuing role of NN partly, comes to my mind. Even the CEO has beena around for a while now.)

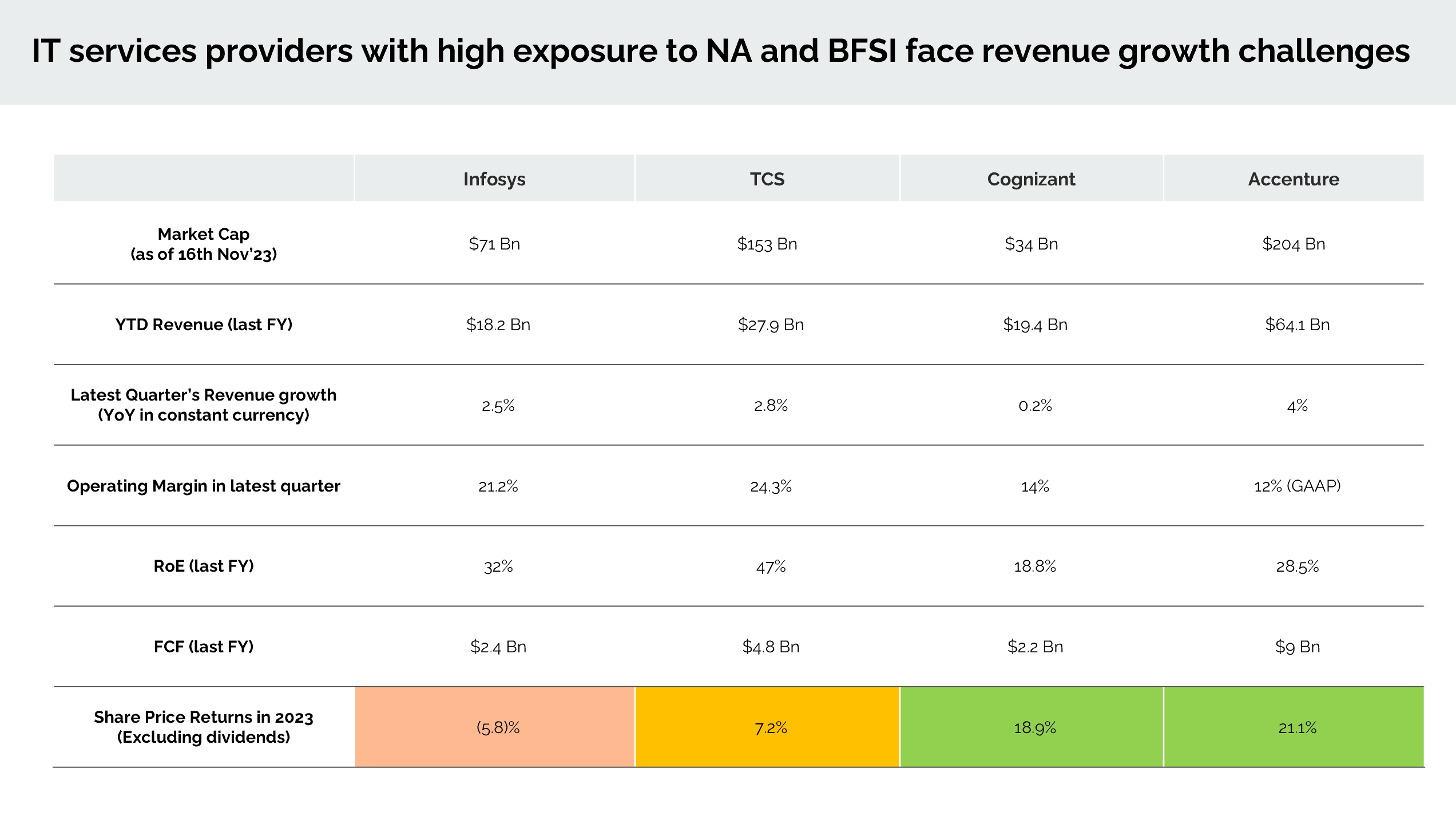

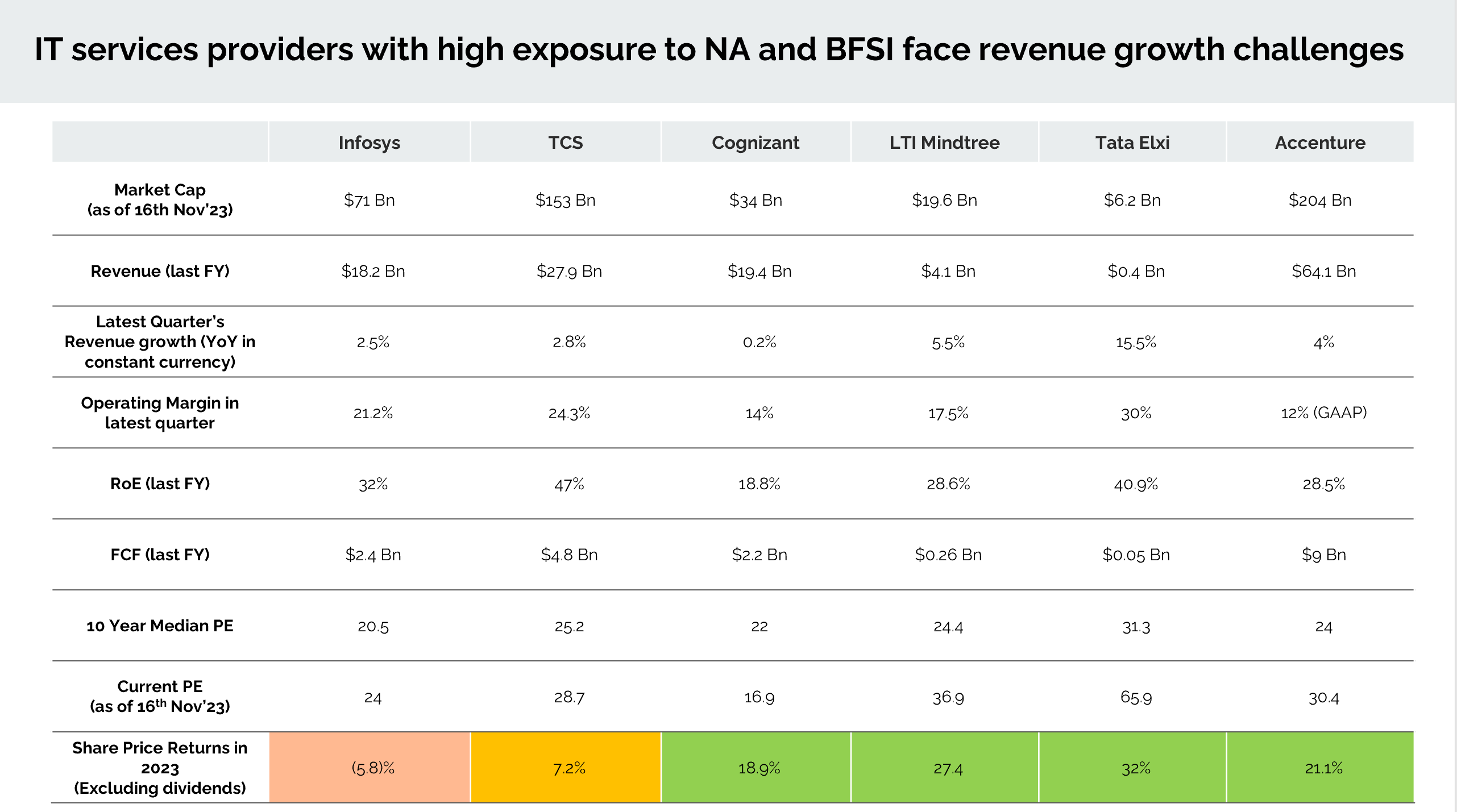

Revenue growth is low at 2.5% YoY in constant currency terms which has slowed down due to global slowdown which includes low spending towards digital transformation and slow decision making by clients.

Except manufacturing vertical, management sees uncertainty of growth pick up on all other verticals.

Management reduced the guidance for FY 24 revenue growth to 1% to 2.5%. It was previously 1% to 3.5%.

Operating margin was 21.2% which increased by 40 bps over the last quarter. Cost optimization and better utilization led to the margin increase.

FY 24 compensation hikes are going to be rolled out from November 1st. It means Q3 and Q4 margins may be down unless utilization improvement compensates for it.

Current utilization is at 80.4% (including trainees). In past the company has managed to bring it up to ~82.5% which happened in FY22. Net headcount is negative compared to last quarter.

All in all a dull quarter apart from headroom to improve utilization slightly. Growth in NA and in BFSI are key factors to watch out for.

Peter Lynch defines a “stalwart” business as a large, mature business growing earnings at 10% to 12% with negligible debt (from his book “One Up on Wall Street”). In my opinion, this is a classic example of a business that fits in the bucket of a “Stalwart”. I feel comfortable getting into Infosys either when the growth comes back or when it falls significantly below its 10-year PE of ~25.

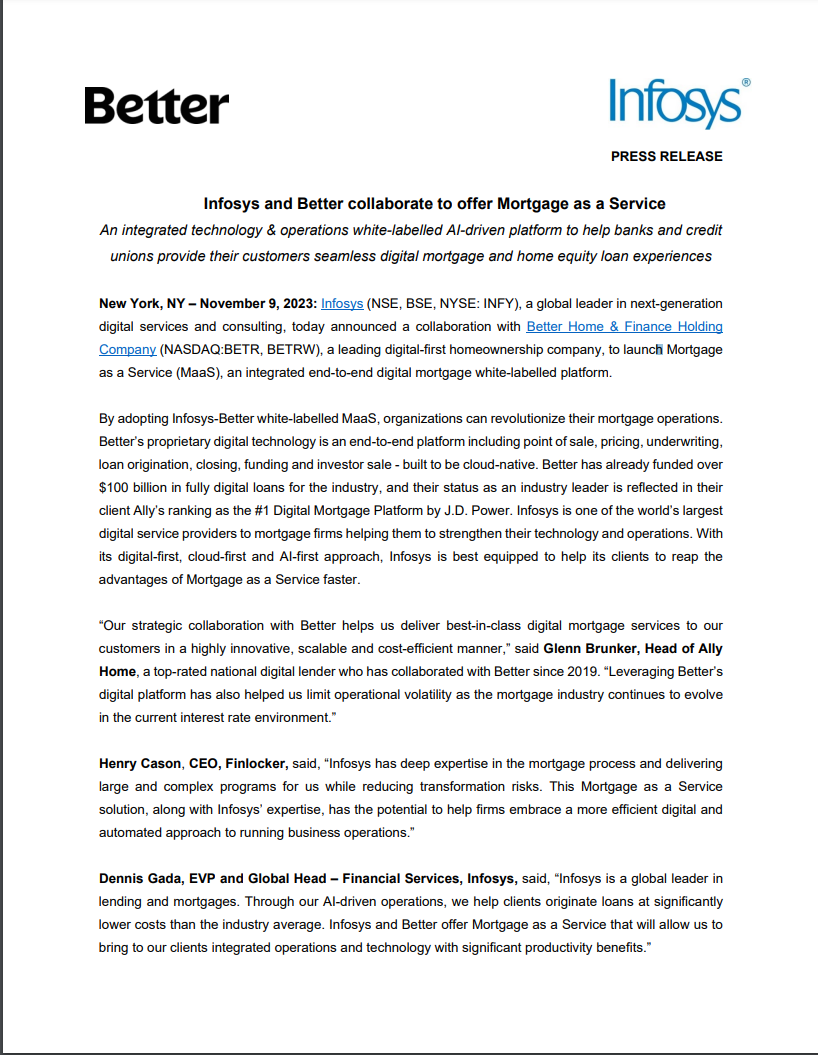

Infosys, a global leader in digital services and consulting, is partnering with Better Home & Finance Holding Company, a digital-first homeownership firm, to launch MaaS.

Mortgage Revolution: MaaS is an integrated technology and operations platform that enables banks and credit unions to provide their customers with a seamless digital mortgage and home equity loan experience. It offers an end-to-end solution for point of sale, pricing, underwriting, loan origination, closing, funding, and investor sale, all built to be cloud-native.

Benefits: The white-labeled MaaS platform by Infosys and Better aims to revolutionize mortgage operations for organizations, making them more efficient and cost-effective. Better’s proprietary technology, which has already funded over $100 billion in fully digital loans, and Infosys’ expertise in digital services combine to offer productivity benefits.

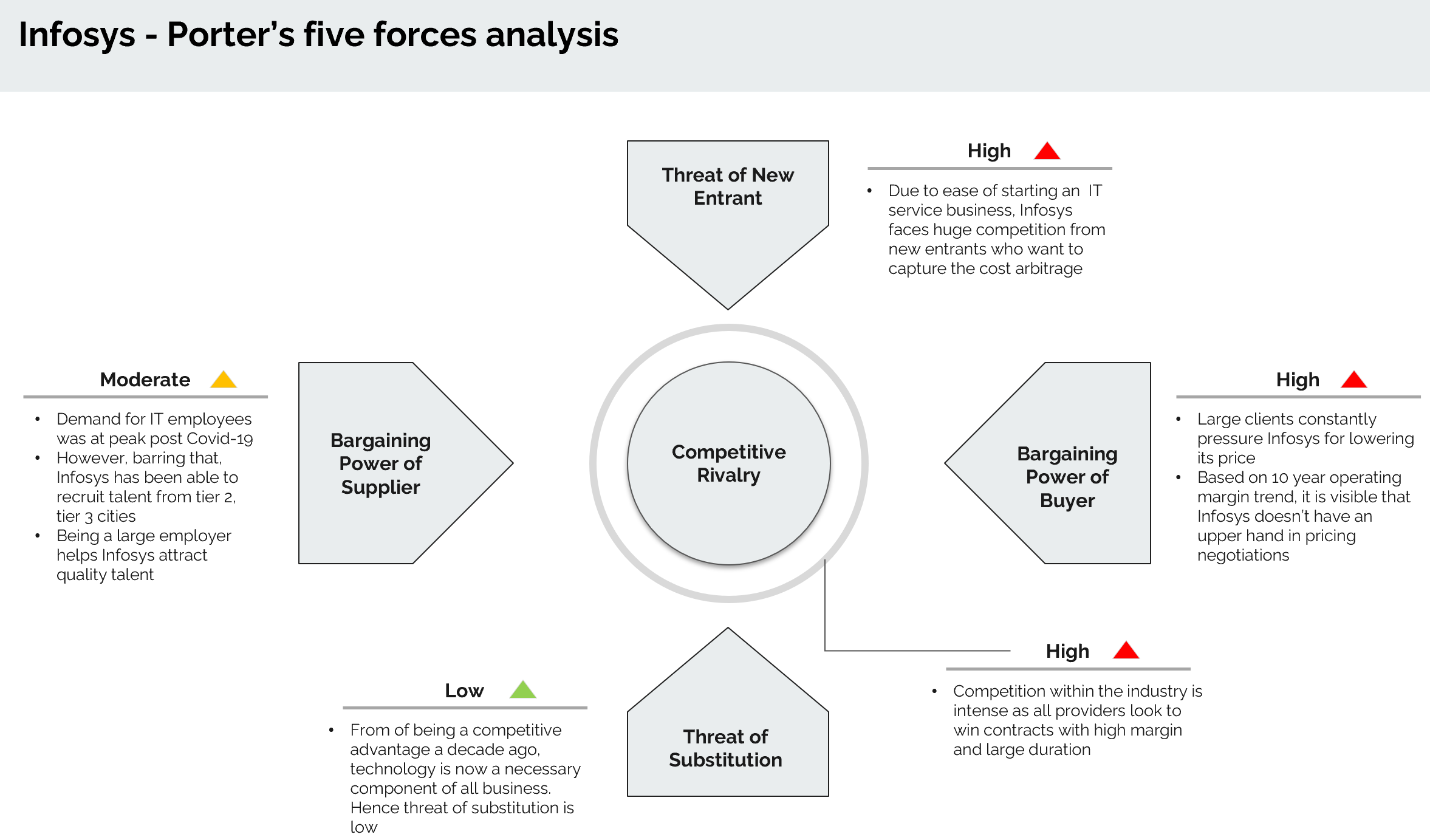

“Bargaining power of the Buyer” has always remained the concern for all IT service companies in India.

The competitor is always ready to offer services/software at discounted price as compared to your price, which erodes the OPM of IT service companies. Buyers will mostly ask for Fixed Price contracts or contracts based on Function Points which ensures that, pricing is based on the software delivered to the customer.

As such there is no Moat in IT services companies hence investing for very long durations like 20+ years could be a challenge.

With positive cash flow and good dividend yield, IT stocks can be used mainly as Dividend stocks for the portfolio. Only exceptions could be emerging companies offering disruptive technologies.

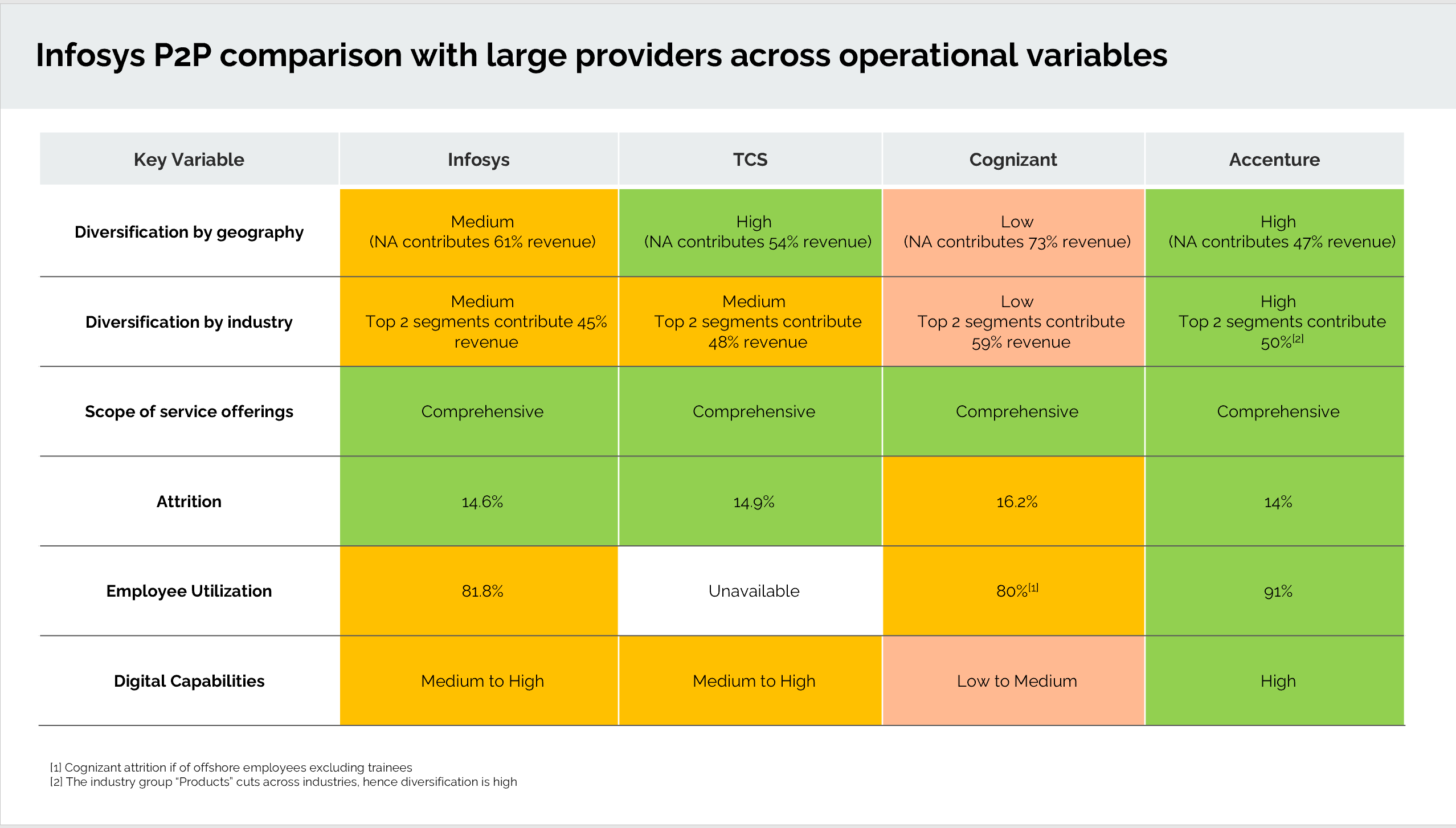

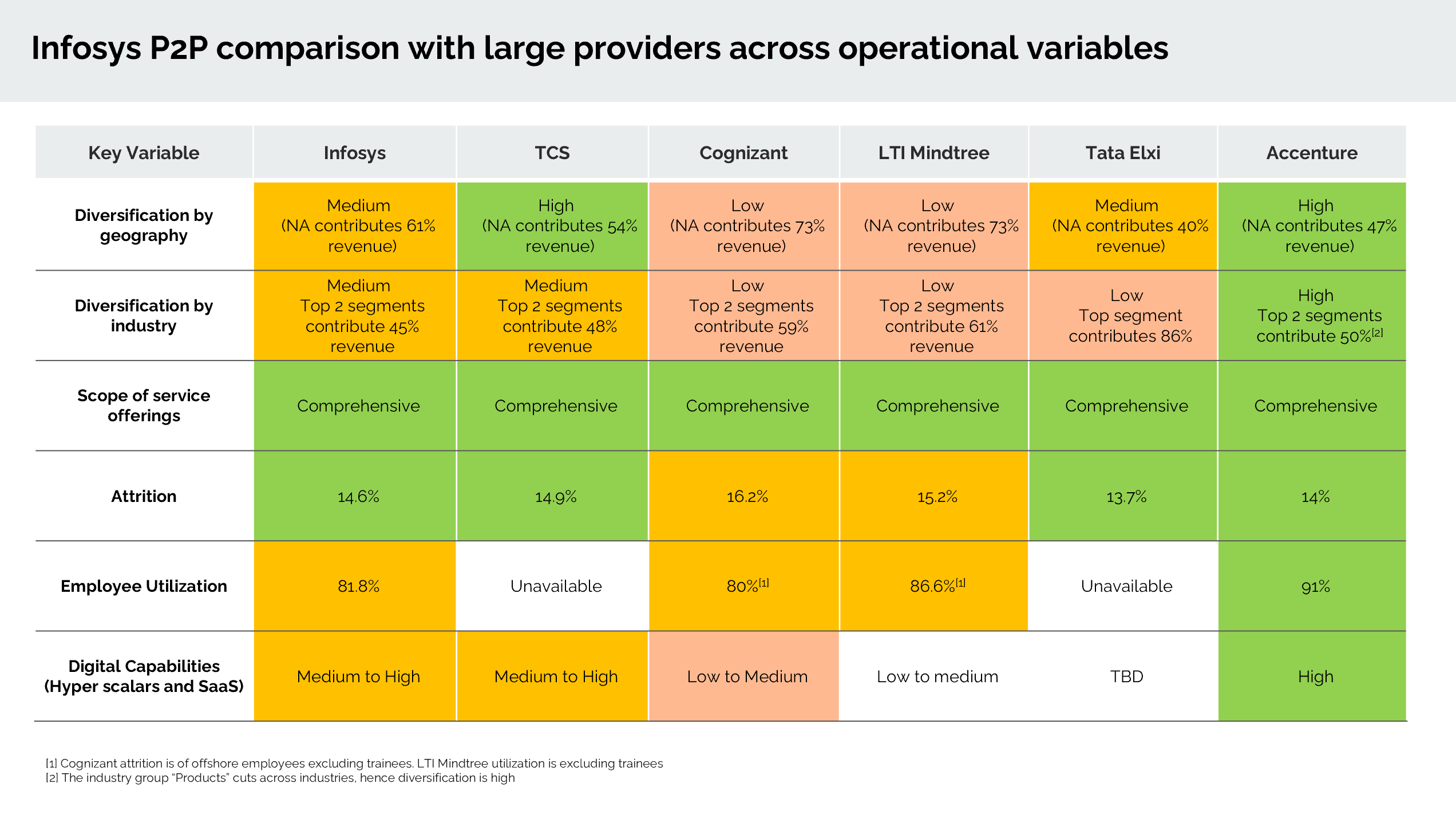

In case of diversification by industry, even though Accenture top 2 segments are contributing to 50% still diversification is shown high in green, while in case of Infosys and TCS , top 2 are contributing 48% and 45% , still their diversification is medium…how come? Or I am reading in wrong manner?

That’s because Accenture’s top segment called “Products” contributes 30% to the revenue but it cuts across industries. So in that sense it does not rely on a particular industry.

I’ve added comment at the bottom(2nd one) about it but forgot to add reference number in Accenture’s diversification box.

Your observation is spot on , thank you for pointing it out.

Palantir was the client as per an internet source. The company is controversial and recently won an NHS contract from the Rishi Sunak Government despite many protests and opposition. Maybe this deal loss is related to Rishi Sunak being linked to Infosys.

Infosys Limited has approved the acquisition of in-tech Holding GmbH, a leading Engineering R&D services provider focused on the German automotive industry. The acquisition is expected to strengthen Infosys’ Engineering R&D capabilities and expand its footprint across Europe. The acquisition is expected to close during the first half of fiscal 2025, subject to customary closing conditions and regulatory approvals.