Yet another stellar performance in an otherwise inflationary environment. It is amazing that the management just walks the talk on QoQ basis.

Discl: Invested at very low levels.

Yet another stellar performance in an otherwise inflationary environment. It is amazing that the management just walks the talk on QoQ basis.

Discl: Invested at very low levels.

Quick notes from Q4 Fy22 ConCall

Key highlights of the last quarter

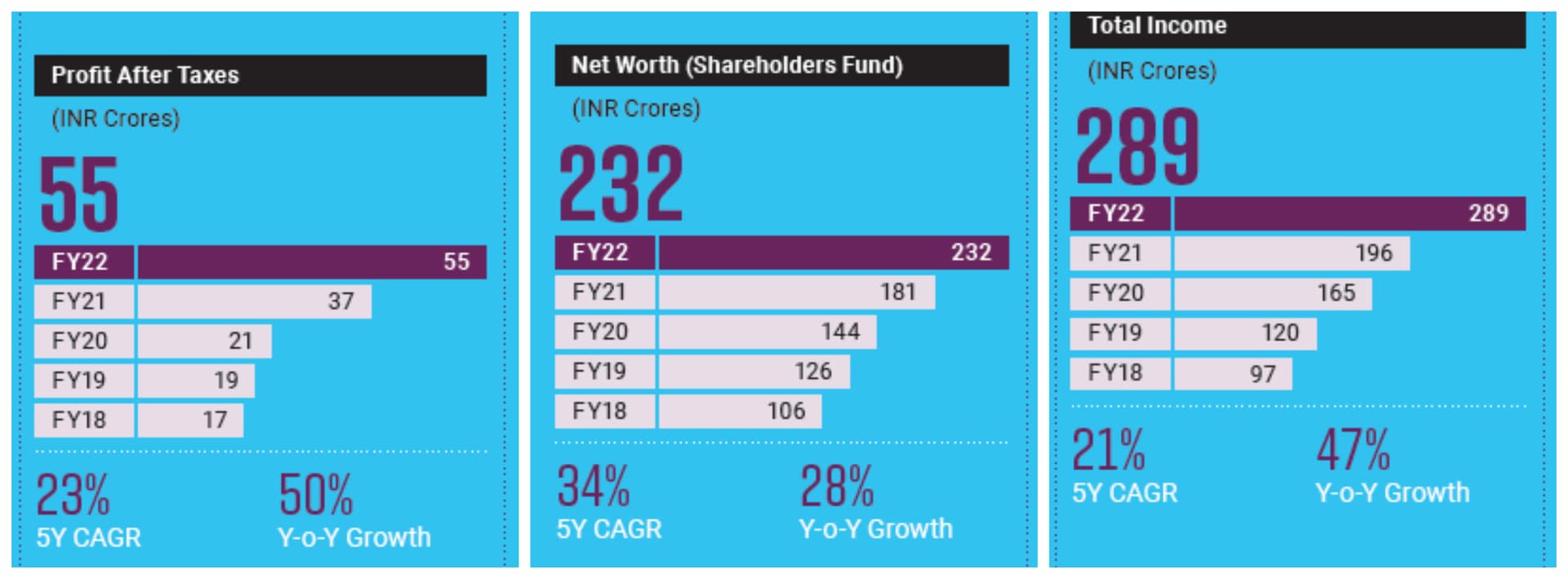

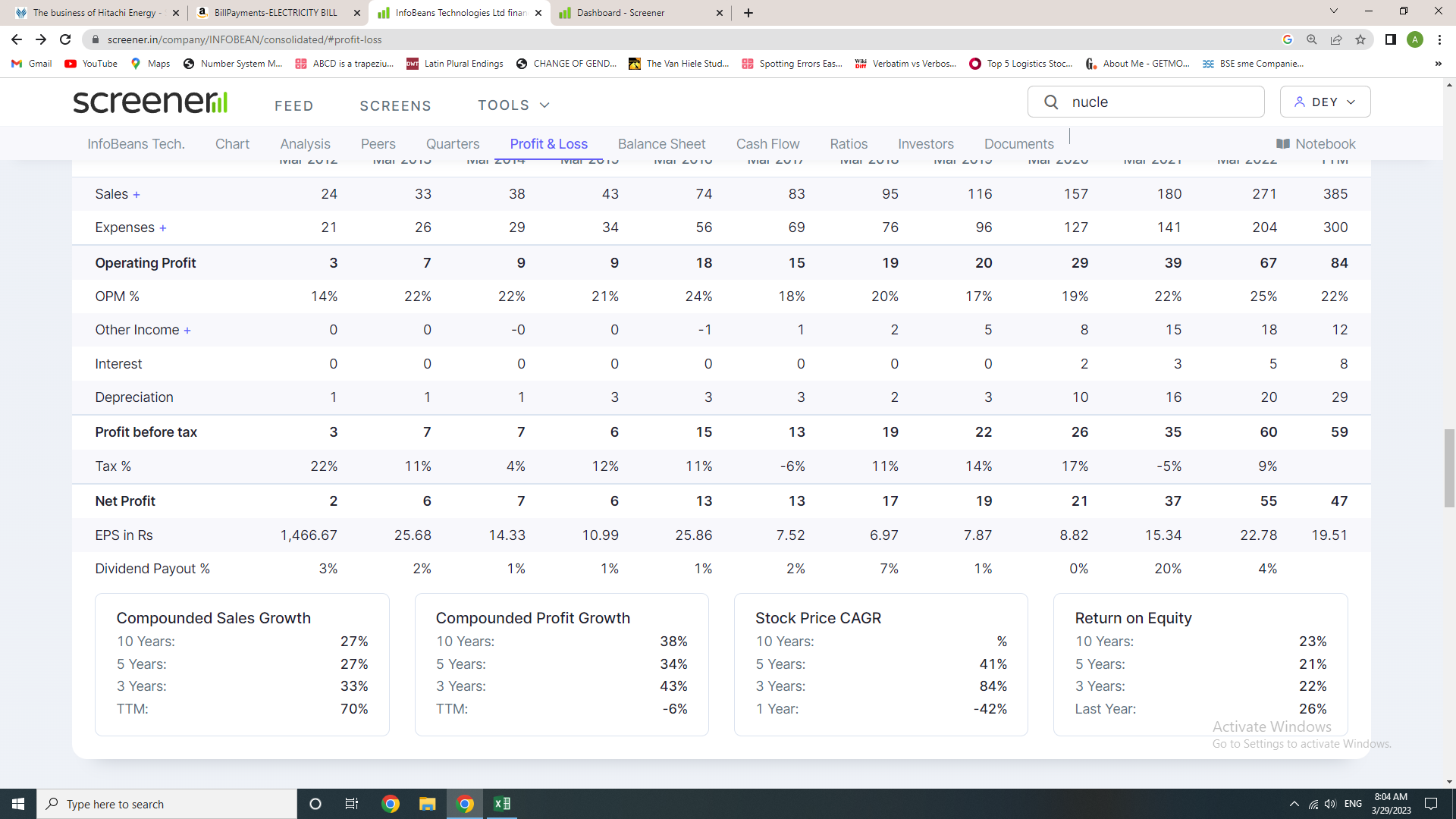

Revenue and margin performance for last year FY22

Employees

On future guidance – will try to grow around 25% every year, and will try to double every 3 years, will grow 20-25% y-o-y organically and remaining with acquisitions.

Attrition – Main concern is the employees who joined in last 2 years where attrition is around 14%, employees who are with InfoBeans from more than 2 years, attrition is 4%.

InfoBeans is constantly trying to built more encouraging and employee friendly environment to reduce attrition rate, top performing employees are rewarded in innovative ways to create win-win situation for both employee and the company.

Current demand environment – Demand is looking strong, InfoBeans is relatively small and opportunity size is big, currently doing digitalisation, cloud automation and product engineering and is looking to foray into other domains by doing acquisition.

On Acquisition – from 2017 acquired 2 companies, Philosophie was very successful acquisition and new acquisition Eturnus solutions is also doing well.

On margins – Currently margins are high, in future will try to sustain net profit margins above 15%.

Tax will be low for nest 5 years.

2 standouts for me other than the numbers and guidance:

The question to which i am still seeking answer is why institutions are not interested in this even after such prolonged good performance.

I have a question. How is Infobeans, a ~1700 Cr. company, able to tap into Fortune 500 Clients? Do their partnerships with Salesforce and ServiceNow help them get these clients or are these their own sales effort?

Infobeans is an expert in Salesforce and ServiceNow implementations. The fact that they have onboarded multiple high profile clients has nothing to do with thie market cap. It’s simply the quality of products that Infobeans has consistently been able to deliver in turn enhancing confidence in corporates to partner with them. Hope this helps!

Hi

Can anyone share AGM notes

(i will delete this post after I receive the reply)

Hi, can anyone please share Q1 FY23 Concall recording?

Hi

Can anyone please share the latest pdf for investor presentation?

Thanks.

How would one look at the money received by the promoters?

First Method

For Siddarth Sethi and Avinash Sethi for FY22:

Remunerations = Rs. 47,78,400 + Rs. 49,48,296 = Rs. 97,26,696

Performance Incentives = Rs. 1,25,00,000 * 2 = Rs. 2,50,00,000.

Dividends

Avinash Sethi Dividend = Rs. 178 lacs

Siddarth Sethi Dividend = Rs. 180 lacs

Total money get by the above two persons = Rs. 705 lacs.

PAT for FY 22 = Rs. 5410 lacs

Total Money/PAT = 13%.

Second Method

For Siddarth, Avinash, and Mitesh for FY22:

Director’s Remuneration = Rs. 348 lacs

Dividend = Rs. 508 lacs

Total Money/PAT = 15.8%

Shares sold by the three promoters = (51,000) shares * Rs. 200 ( Minimum approx Price for Fy 22) = Rs. 102 lacs.

Total Money/PAT = 17 %

But overall shares 17,000 shares were bought.

It is interesting to look at like aggressive mutual funds houses that try to beat the market while taking high management fees.

Disc. Invested.

Almost 75% of the company is owned by them.

So out of 5410 lakhs PAT , 75% is 4057. Out of which 358 is dividend, is only 8.8%. Looks fine to me.

They are taking a salary of around 4 lakhs per month each . Rest should be incentive.

Though the median remuneration increased, the salary of the directors has not increased.

Disc. Invested.

Does anyone know why the company release its quarterly result for 2021 today 17 Jan 2023?

Q2 concall discussion condensed here.

What is the order book?.Any idea on new projects…

Disc: Tracking after hitting 52 w Low

They have some SEZ benefit at the Indore location

I have made position and seen results are not great. Can anyone suggest if i can still invest in it or move to some other stock

Waiting for other midcap results… Especially saksoft … If similar kind of pain in results and margin across mid cap IT then its buy opportunity…

Disc: Invested