Company: Influx Healthtech Ltd

Sector: Nutraceuticals Pharma/CDMO

Exchange: [NSE Emerge]

Company basic info and IPO Details

• Market Cap: ₹380 crores

• Issue Price: ₹ 96

• Listing Date: June 25, 2025

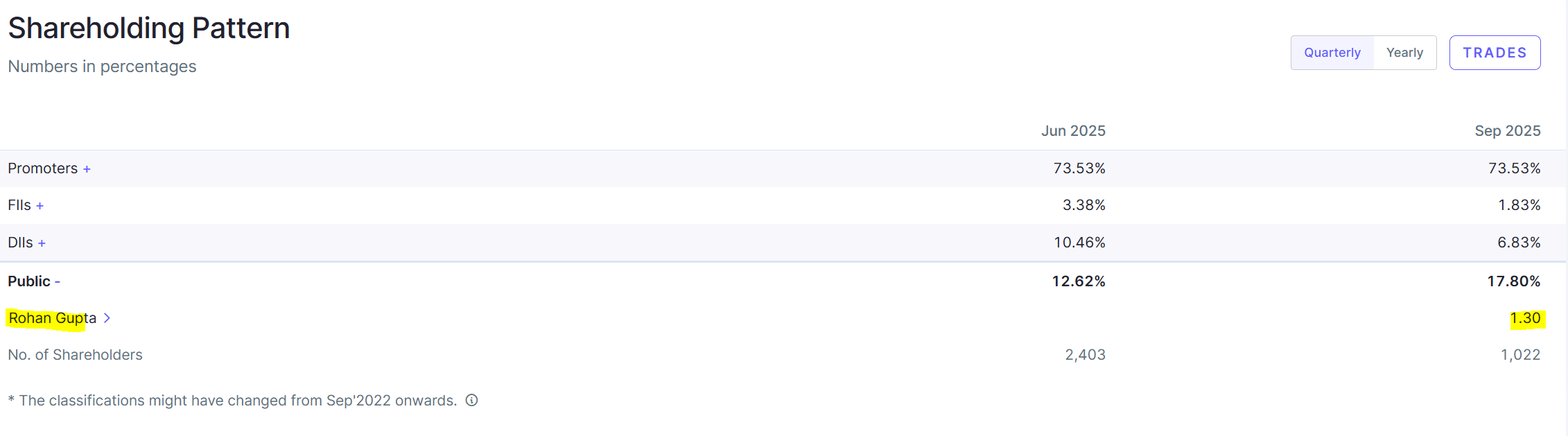

• Promoter Holding: 73% (post IPO) , FII+DII hold another 14% as per screener.

The Company raised 48 cr from ipo, majority of this is by fresh issues of shares and minor part of OFS by promoter.

The IPO is solely lead managed by Rarever Financial Advisors Pvt. Ltd., and Maashitla Securities Pvt. Ltd., is the registrar to the issue. R K Stockholding Pvt. Ltd., is the market maker. In SME listing. its important to know who is the lead manager as we can track their history of companies taken for IPO and their performance thereafter. In the prospectus Company lists Sudarshan Pharma, Quest Laboratories, as their peers.

Company is a 3rd party manufacturer of the below products.

Corporate Presentation :

Financial Highlights

• Revenue (Latest FY): ₹105 crores fully domestic , exports less than 1%.

• Net Profit: ₹13 crores

• ROE: 45%

• Debt-to-Equity: no debt

• Revenue Growth (3-year CAGR): 20%

Its notable the company was able to grow without having any debt and came to ipo for purely growth and not clearing any old debts.

Business Overview: Influx was founded in 2020 by Dr. Munir Chandniwala. It is CDMO company specialising in nutraceuticals, cosmetics, petcare, and homecare products catering to around 600+ customers. Marquee clients include Novus life ( which is the famous CF carbomide forte for supplements ) , Davaindia (listed Generic pharmacy having 450+ stores) etc.

The company has three manufacturing facilities in Thane, Maharashtra, each covering an area of 9,676 square feet, 13,000 square feet, and 14,000 square feet, respectively. These facilities are certified to international quality standards, including GMP (Good Manufacturing Practice), HACCP (Hazard Analysis & Critical Control Points), ISO 22000, and Halal certifications, ensuring adherence to the highest standards of safety, quality and regulatory compliance.

Following are the developments made by company to achieve better product portfolio over the previous three years:

Key Products/Services: Company manufactures around 3500+ products in nutraceuticals or nutritional supplements, cosmetics, ayurvedic/herbal formulations, veterinary feed supplements. The company offers products for various segments, they are Dietary/Nutritional 3018, Cosmetics 371, Ayurvedic/Herbal 103, Veterinary Feeds 71, and Homecare 7.

Business verticals 2025

- Nutraceuticals: 90.74%

- Cosmetics: 5.21%

- Ayurvedic: 2.92%

- Veterinary: 1.08%

- Homecare: 0.05%

Companies offers the following products to its clients:

1. Dietary/Nutritional Supplement Product portfolio includes dietary and nutritional supplements in various forms:

• Tablets, Capsules, and Powders

• Liquid Orals and Softgels

• Lozenges, Jellies, and Gummies

• Oral Dispersible Films (ODFs)

• Effervescent Tablets and Liquid-Fill Capsules

• Candies and Gym/Sports Supplements

2. Cosmetics Diverse range of products for men and women, including:

• Skin Care and Body Care Products

• Hair Care and Beard Care Solutions

• Face Masks and Soaps

3. Ayurvedic / Herbal formulations Company produces ayurvedic and herbal formulations in the following forms:

• Tablets, Capsules, and Powders

• Liquid Orals and External Applications such as Ointments, Creams, and Lotions

4. Veterinary Feed Supplements Veterinary feed supplements are available in multiple formats, designed for animals such as dogs, cats, horses, birds, cows, chickens, pigs, buffaloes, squirrels, and goats. The product range includes:

• Tablets, Liquid Orals, and Oral Sprays

• Powders, Boluses, and Gels

• Ointments and Creams

5. HomecareCompany has variety of homecare solutions, including:

• Bathroom Cleaners

• Floor Cleansers

• Phenyle Liquids and Other Household Cleaning Products

Management Quality

• Promoter Dr. M.A. Chandniwala aged 44 yrs is the first gen Entrepreneur with an industry experience of more than 2 decds , he holds Phd in HR, MPhil, Diploma in Nutrition and Post graduate degree in Management and Business & Bachelor of Pharmacy from the University of Pune.

Investment Thesis

Expansion plans and capacity utilisation :

Current capacity utilisation is very high. Company did some debottle necking in packaging where they had issues with moving to automation and now that is complete without using any ipo proceeds they are able to go upto 200 cr top-line without using the IPO proceeds for capex. With the IPO proceeds they will be able to do 500 cr top-line.

Management confidence of 200 crore topline possibility this year supported by the debottle necking which had restricted their growth last year. Once the Planned capex is live they wont need much capex to hit 500 cr topline.

https://www.youtube.com/watch?v=hMOBbk7UJF4

From IPO proceeds company plans to invest in

- Manufacturing of Oral Dispersible Films :Oral dispersible films (ODFs) are strips that dissolve in the mouth for direct absorption. Product in this category include vitamins and mineral supplements (e.g., vitamin C, calcium), probiotics,

energy boosters, sleep aids, and pain relief products.

2. Expanding the Line for Snacking, Protein Bars and Protein Powder: Currently operating on a small scale, this segment will benefit from significant capital investment in automated

machinery, enabling large-scale production and greater efficiency.

These upgrades will allow to:

• Satisfy the increasing demand for high-protein, health-focused snacks.

• Broaden our customer base and market reach with larger production volumes.

• Ensure consistent quality and innovation in our offerings.

3. Introducing a Beverages Line into the Portfolio: : Currently company does not manufacture any liquid supplements, and intends to introduce tetra pack and liquid supplements in sports and clinical nutrition. This expansion will allow to offer a variety of liquid products under nutraceuticals and health supplements.

Expansion cost breakup 22 crores is fro nutraceutical division and 11.5 crores for veterinary food division.

Positives: Company is into High growth segments , nutraceutical segment in India is expected to grow at 10% cagr for next 5 yrs. Company is Backed by an young and active promoter , long runway for performance.

Concerns and risks:

- This is a highly competitive industry with no entry barriers.

- Recent IPO with no proper history, hence difficult to ascertain management guidance.

- Listed in SME exchange and has lower Compliance standards.

- Available in only lots and liquidity is low.

- Major revenues is derived from only 3 states of Maharashtra, Gujarat, and Karnataka.

- Business is dependent on maintaining GMP, HACCP, ISO 22000, and Halal certifications. Any suspension/non-compliance may restrict operations.

- Heavy reliance on a limited number of manufacturing facilities in Thane posing geographical risks if any arise in future. Any disruption (fire, accident, regulatory action) would materially impact operations.

- Dependency on CDMO clients. Loss of key customers or contracts would affect revenues.

- Exposure to price fluctuations in raw materials (nutraceutical, herbal, and pharma inputs) which can affect margins.

- Competition in CDMO and nutraceutical manufacturing is high; pricing pressure could erode profitability.

Valuation :

I am hopeful Company will be able to grow 20-25% for next few years and since there is no need for additional capital till they hit 500 cr topline. If they grow 25% they will hit 200 cr at Fy28 and at 15% margins 30 cr profits Company is trading at 12-13 PE for Fy28. Companies that grow at 25% usually trade at 20-30 PE.

Disclosures: Have tracking position.

Sources : DHRP, company presentations and publicly available promotes discussions on youtube.

Disclaimer : This is not a buy/Sell recommendation. SME stocks carry higher risks due to their smaller size, limited operating history, and relaxed regulatory requirements. This analysis is for educational purposes only and should not be considered as investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.