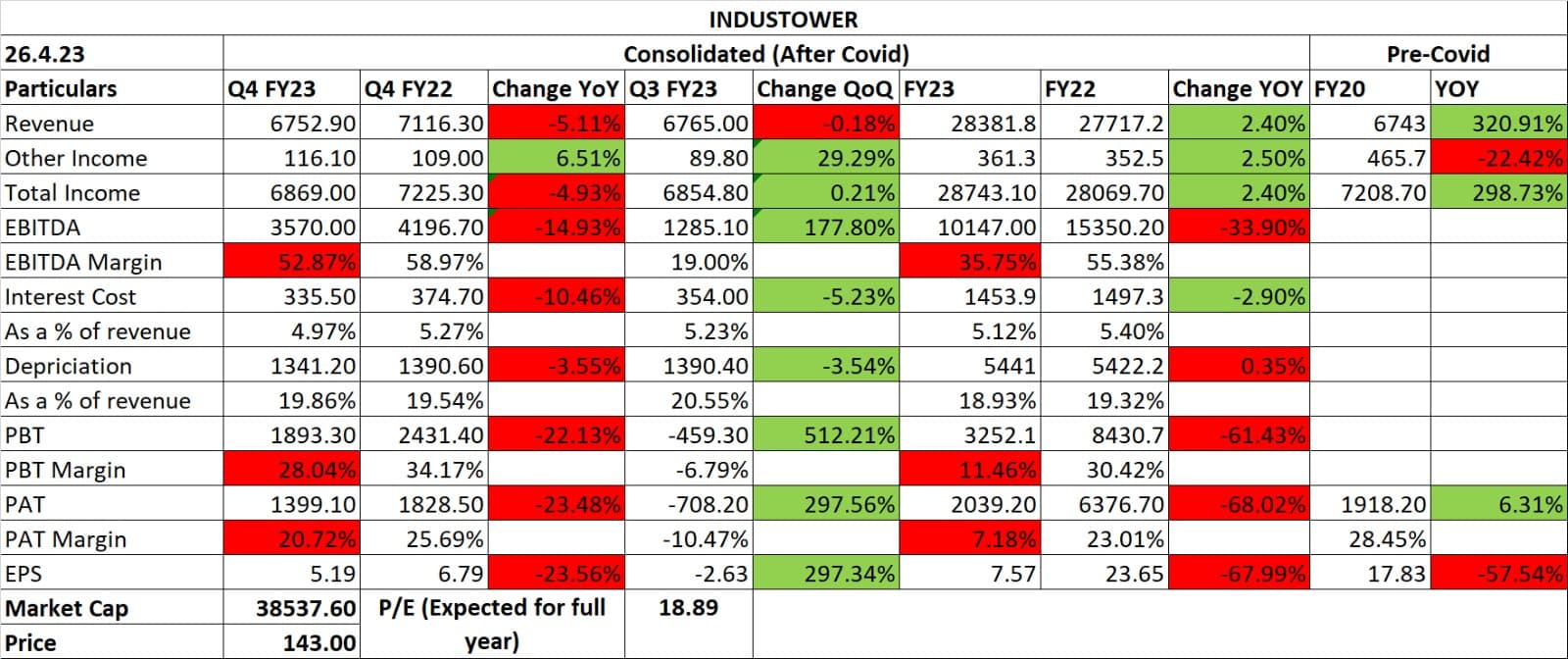

INDUSTOWER Q4FY23 Result Update:

- 5G rollouts in full swing with plans for a Pan India rollout in the next 12 to 15 months. Increased demand seen for 5G equipment seen at existing sites as well as new sites.

- Leaner towers are Capex and Opex economical, and the return profile is better than macro towers at a single tenancy level.

- Tenancy addition accelerated with net add of 3,396 despite 512 exits.

- Lean tower addition was 1,235 in Q4FY23 vs 1,408 in Q3FY23. The company expects single tenancy lean towers to have better RoCE vs macro towers.

- VIL has made entire payment due for Q4 FY23. There is Nil Provision as of now. Earlier dues are still pending though.

- Capex was Rs15.3bn (22.7% of revenue) in Q4FY23, and it was at Rs41bn (14.7% of revenue) in FY23.

Brokerages are putting a HOLD on the stock with Expected Revenue of 29000 crs and Expected PAT of 59000 crs.

2 Likes

Indus towers posted Q1 results, management seems to be handling the VI crisis fairly well and have added 5k towers this quarter (+3% tower count): Indus Towers Q1 Results: Net profit surges 182% to ₹1,348 crore, revenue up 3%; ESOP declared | Mint

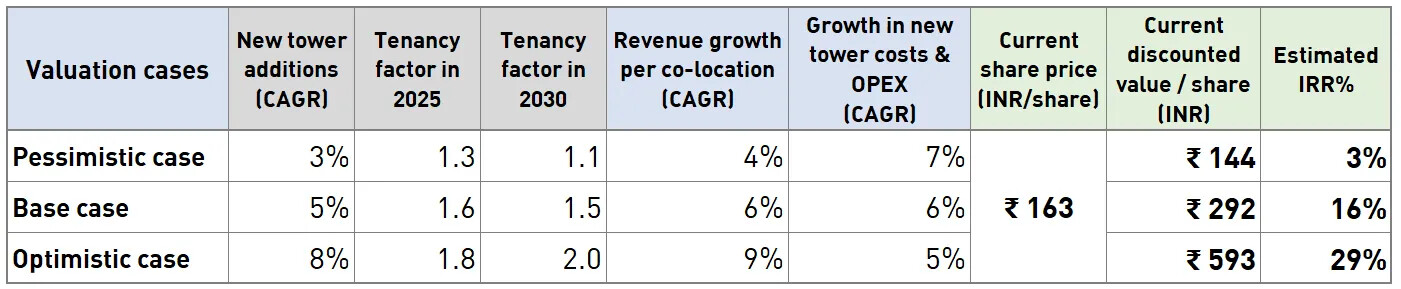

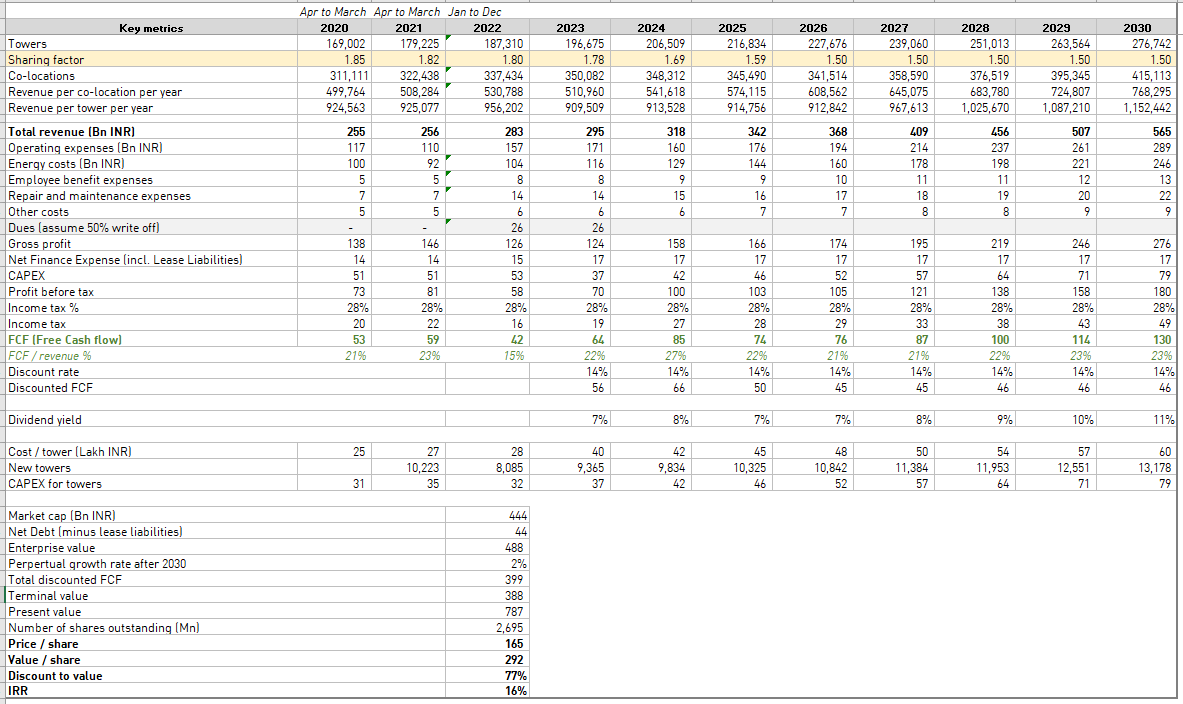

I had done a valuation earlier this month (see below), which sill seems valid, although stock price has gone up slightly since then:

The detailed assumptions are below for the base case valuation:

Feedback / opinions on way forward appreciated!

Disc: invested

6 Likes

The Results for Q2 FY 2023-24 is out!!

Revenue Down 10% YoY at Rs.7,133 crores

EBITDA Up 23% YoY at Rs.3,456 crores

PAT Up 49% YoY at Rs.1,295 Crores

A Mixed set of results is what i feel after going through the same…

Positives :

- Good Turnaround with regards to PAT

- VI Paying the amount equivalent to monthly billing from january 2023 is a good sign, but still no clarity regarding the amount standing due till December 2022 the payment for which has not yet been materialised as per the Notes to F.S.

- Achieved 2,00,000 Macro Towers , a pretty good milestone!!!

Negatives :

- Why did the revenue fall despite data usage peaking every month?

- Need Clarity on the revenue aspect (Will Update after the ConCall(If Conducted))

- Finance Income has almost increased 10x…Need clarity on where the excess funds are being invested by the company.

- The extraordinary jump in Net Profit can be attributed to the low base in Sep 22 quarter during which the provisions were charged equivalent to Rs.17,706 Mn against Rs.1,335 Mn charged in the Sep 2023 Quarter…Except this Profit would have fallen since revenue has fallen and all expenses have increased this year

Overall, A Mixed Set of Results…No Big Positive Surprises and Negative Surprises either…

Disc : Invested…And Am an amateur…So kindly correct if i am wrong on any front…

Thanks

Link for accessing the Results & Press Release :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f2dd0f8e-c444-43ed-a3a0-d4fa252dadcc.pdf - Detailed Results,Notes & Audit Report

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c9f14d04-0a2e-40a7-902f-9d70de20c6f5.pdf - Press Release

6 Likes

The revenue for Q2 FY23 included a benefit of Rs. 1,076 Crores from deferred recognition of

revenues arising from the settlement of old dues with the customers. The same quarter also had an impact of Rs. 1,771 Crores due to provision for doubtful debt.

Net net, the revenues are up YoY if you remove the last year deferred recognition adjustment.

Good results in my opinion.

4 Likes

hi

what about debt issues in the company. Will they be addressed in near future?

More like a receivable issue from financially struggling VI. Even the stock price moves in tandem with VI.

As of September 30, 2023, Vi owes Indus Towers Rs 7,351 crore in receivables. This delay in collections has impacted Indus Towers’ financial performance, and the company has made a doubtful debt provision of Rs 5,000 crore against Vi’s receivables. Vi is currently in the process of raising funds to improve its financial health. However, it is unclear when the company will be able to clear its dues to Indus Towers.

3 Likes

great piece of information

1 Like

Anyone from telecom domain here who can shed light on direct-to-cell technology?

Will it be possible for such tech to make cellphone towers redundant? The tech as it is requires the phone to be outdoors but if we are to use some kind of forwarder/booster just outside a building, will it be able to act as an intermediary between phones inside the building and the satellites? If so and if telecom companies can fool people enough into buying such equipment for themselves then in long run telcos could wiggle out of having to pay for towers.

I’m not a telecom expert, but am an investor in Indus. Just read about this: Starlink could theoretically be a threat to Indus and the Telecom industry in the far future (10 years+), but it is still pretty far from getting there, due to the following:

- Starlink is still not fully approved in India - it could be a few years before it is approved for commercial usage

- After approval, it would need to apply / bid for spectrum allocation - which could be a significant cost for Starlink, which is currently loss-making. So, I’m not sure if they have sufficient funds to bid for spectrum

- Based on costs in other parts of the world, I doubt this solution would be cost effective when compared to Indian mobile and broadband costs in big cities and towns: " As per industry estimates, the pricing of satellite Internet services is expected to be around Rs 8,000-10,000 per month along with one time set-up cost. This is significantly high, compared to affordable home broadband plans of Rs 399 per month by telcos such as Reliance Jio."

- Based on the current download speeds, it is probably at the lower end of 4G: 60~90Mbps. So , would not be a great solution to stream videos / download movies etc. However, it might be quite a good solution for remote areas without cell tower coverage (e.g. mountains / forests).

So, in conclusion, I think it is a solution that will complement existing mobile and broadband coverage in India, especially to remote locations where is it not economical to set up towers and lay data cables.

Sources:

7 Likes

Starlink can not give same bandwidth. We are used to such high data consumption, no one will go back to low data speeds. Also Starlink will have latency issues (Light coming from a satellite vs from tower nearby). It is good for connecting far-flung and sparsely populated areas like mountain, north-east where cost of tower infrastructure is too high per consumer.

A different topic:

Recent spurt in stock price is direct consequence of Brookfield deal to buy ATC towers in India. Indus was undervalued compared to deal price.

5 Likes

I checked the second point - stock definitely seems to have reacted to that. But it looks like Indus is not very undervalued based on Brookfield’s acquisition price (If we assume ATC and Indus have the same type of towers).

Brookfield paid US$ 2.5B for 77k ATC towers, which is around US$32.4k / INR 27 lakh per tower. If we multiply Indus’ 204k towers by INR 27 lakh, we get an enterprise value of INR 55,080 Cr. This is slightly lower than current EV of Indus : 55,960Cr. market cap + 4,500 Cr. net debt = 60,460 Cr. EV.

However, I think ATC towers may not be as valuable as Indus based on the tenancy factors (1.54 for ATC vs. 1.79 for Indus). This points to Indus having more large towers (ground-based towers) compared to smaller ones (feather sites and antennas). If I multiply the EV by this factor (1.79/1.54), I get a total EV for Indus of 64,021 Cr. (slightly higher than current EV). Note: this is only my speculation, without having done a thorough asset scan of both companies.

However, one other tangible advantage for Indus is that there are fewer competitors in the field and more expectations for rational pricing (knowing that Brookfield would look to get a good return on acquisition price). So, there are probably lower chances of a price war now.

Sources:

4 Likes

That’s good news considering the stock was mirroring VI in price movements for a long time now.

It meant it was undervalued. It has moved more than 20% in one week based on this deal thus bridging the undervaluation gap.

Also, we are looking for duopoly in market now. Indus and Brookfield.

1 Like

Given the new equity raise approved for injection into Idea, does Indus get any of their unpaid receivables paid through this year?

1 Like

I don’t think the fundraising is to pay off Indus. It has more to do with 5G infra buildout and debt servicing.

Disc: Although the stock is performing strongly, I was not comfortable with rising debt levels. Exited this week.

As per screener interest payment is down substantially from 246 to 11. Dont know its a mistake.

Disc - bought in last three days.

1 Like

What are your thoughts on stake sales plan of Vodafone? Will they pay off the debt at least partially?

Potential impacts for Indus from the VI stake sale:

-

Outstanding VI dues can be paid off in full: estimated VI dues based on accounts receivable and online reports is around ₹6,000~₹7,000 Cr. VI’s stake in Indus is worth ₹19,330Cr. Of course, VI also owes other people a lot of money, so not sure whether Indus’ VI dues will be fully cleared after the stake sale, but I expect a big part of the dues to be paid off.

-

If there is a lot of demand for the stake at current prices, that will provide the market assurance that Indus Towers’ share price is not overvalued. However, if there is no demand or less demand than VI expects, it could have the opposite effect.

-

FII/DII purchasing VI’s stake could mean a board re-jig, with VI board members replaced by the new FII/DII representatives. I view this as positive for common shareholders, as the new board members will be incentivized to increase shareholder value more than VI board members (will reduce some of the existing conflict-of-interest within the board). If Airtel buys vodafone’s stake, then it will have the opposite effect. More Airtel board members and stake will effectively make Indus a subsidiary of Airtel, which I don’t view as favourable (as then board has incentives to favour Airtel rather than the Indus common shareholders)

Disc. : invested / potentially biased

PS: I had valued Indus approximately 1 year ago, in July 2023. The shares seem fairly priced now (a bit higher than the “base case”):

Thanks,

Sharad

OpenSourceInvestor @ Substack

7 Likes

Indus stake is not owned by VI but the parent Vodafone…

3 Likes