This thread seems to have gone cold. I was wondering if the massive tariff cut on GSPL will have some negative impact on IGL as well. Does IGL also operate High-Pressure (HP) pipelines that could be impacted by similar tariff cuts?

I recently started studying IGL - got interested in it after the fall it has seen due to the Delhi Electric Vehicle policy and also the reduction in gas supply via the Administered Price Mechanism (APM). I only have a small position and have been thinking if I should scale up. Personally, I think EV impact is overstated. Further reduction in APM might be a challenge but that will apply for all CGD players, so at an industry level, my sense is it may not impact much as I expect they will pass on the cost increase. However, I am less clear about the impact of this regulatory decision. Given their NCR monopoly is over, if this price cut will happen to their pipeline infrastructure, then it will be a double whammy, no? Can someone provide additional clarity? Thanks!

Based on this interview, it looks like GAIL may also see a downward revision in HP pipeline tariff in the near future. That will bode well for IGL which receives its gas from the HVJ pipeline of GAIL. However, it is quite possible that the regulator may also ask IGL to share their city pipeline infra at lower cost if another player starts operations. I can’t seem to find any information about potential new CGD entrants in NCR. If someone’s tracking this and has some idea, please do share.

Out of 8.33 MMSCMD around 75% is contributed by CNG and remaining from PNG. Delhi government has issued notice to Cab aggregator companies to convert their cars to EVs in a phased manner. By 2027 100% of cars need to be only EVs. This will create a lot of pressure in terms of volume to IGL

Thank you for the reply. I believe the EV policy date for Delhi is by 2030, and not 2027. However, my assumption on volumes is based on 1) IGL’s own growth forecasts for gas sales, they expect to end FY25 at 10 MMSCMD 2) Conversion of inter-state transport and possibly, other heavy vehicles (IGL talks about dumpsters) to gas 3) Chances of EV transition being slower 4) IGL expansion to other geo areas.

That’s my rationale for being a bit more sanguine about volumes. I could be wrong, of course. However, I am less convinced about price/margin pressures. I would love to get some perspective on that.

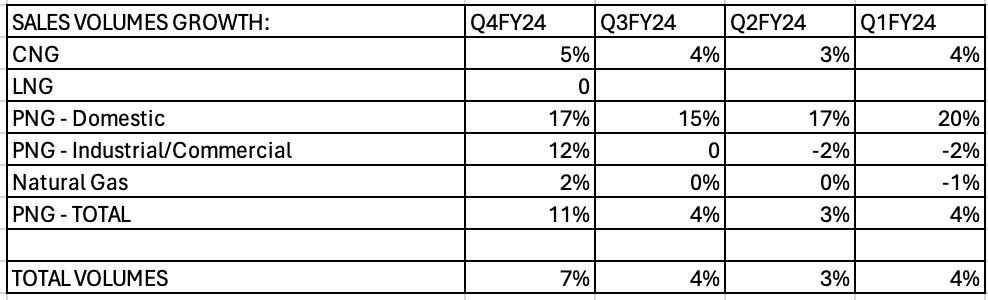

Initial reaction to Q4 results - a mixed bag, but more negative than positive given they had guided for better numbers in the Q3 earnings commentary. Volumes were up, but lower than expected. PNG growth (both domestic and industrial/commercial) has been quite good QoQ, and domestic growth has been particularly strong YoY. CNG growth is steady - the good thing is they are still growing here despite the headwinds around EV adoption.

However, clear margin pressures seen across both CNG and PNG. EBITDA margin down 1.2% QoQ and EBITDA per SCM was only Rs. 6.58, much lower than the Rs. 7.5 they are targeting for FY25. Given CNG prices were cut in March, chances are it will fall further in Q1 FY25. Haven’t listened to the earnings call yet - wonder what was the reason for this fall in Q4.

While valuations are ok, some more caution warranted here, I guess. Not clear to me what is the growth trigger even if margins bottom out in Q1.

Got around to listening to the earnings call, and there were some one-offs in Q4 Opex that led to the lower margins. That was good to hear. Not much has changed materially. They still expect to achieve 9.5 MMSCMD on average in FY25, mostly driven by new GAs CNG sales in commercial segment, and Industrial/domestic growth in older GAs. LNG and CBG sales will also contribute and possibly offset the CNG sales loss to EVs. The EBITDA per SCM range shared was quite broad - between Rs. 7 to Rs. 8.5. I am guessing it’s because APM allotment continues to come down and it’s hard to predict spot price which in recent years has fluctuated wildly.

Overall, it was a reasonably positive update in my opinion. If gas prices stay low, the stock should do well, given the reasonable valuation. I don’t foresee much of a downside risk unless there’s some major policy change (always possible) or unexpected competition (seems unlikely as of now).

Disclosure: I am invested, may add or reduce anytime. I am not making any recommendations here. Just sharing my thoughts.

Perception wise, this should be good for IGL though the article also does say that the regulator may move to declare those licensees who have long passed exclusivity period as common carrier. So it’s a bit ambiguous.

the fact that ppfas mf has been constantly adding , has really got my eyes here , any substantive thing here in the pipeline in the next 5 years, valuations seem great , but dont know where the incremental growth comes from at a large scale , anyone can higlight some triggers or things that could help build a bull case here ?

Incremental growth will be from new GAs (geographies) and if they can do better in the industrial segment. How strong that growth will be is anyone’s guess. There are 1-2 other growth areas but those are more uncertain or will not contribute in a significant way.

The problem with the government companies is these kind of Regulations and Control. The margins will definitely hit to some extent but they will be able to reduce some impact by increasing the prices.

Such instances have happened multiple times over the past decade but profitability has never been impacted (as seen in the EBITDA/SCM chart).

When company has had to raise prices significantly, volumes growth remained healthy.

Each of these adverse external events have been a buying opportunity.

10-year average PE multiple is 18.46, and is now available at a PE of 12.82 (one-year forward).

General Thoughts/Questions Based on the Above

How much does the narrowing of price gap between petrol/diesel and CNG impact IGL’s ability to pass-on price increases? (Key considerations - cost of vehicle, mileage and prices).

Any roadblock from government/regulators in terms of CGD companies increasing prices?

If there isn’t (seems so, going by the PNGRB Act?), this sharp correction looks like an overreaction, especially with IGL’s past track record of maintaining profitability? Any perspectives on this?

Fully agree and with environmental situation in Delhi, IGL volumes are poised to grow… company has a proven track record to weather these storms and agree this is a good buying opportunity… I prefer IGL over MGL

But can this APM allocation be considered equivalent to 2010-December gas cost hike and other instances like Ukraine war, etc.,?

Is this APM issue not a policy change and going to impact the sector’s fundamentals forever?

Agreed on your first point. But isn’t the question here really whether IGL can pass-on the higher cost (and to what extent) and maintain profitability without hurting volumes?

And given that both these metrics - EBITDA/SCM and volume growth - have remained stable over such a long-period despite significant volatility in gas cost, should this time be different?

Gas cost was 10 Rs/SCM in 2010 and now it is 32 Rs/SCM which is 10% CAGR. It is nothing abnormal. This cost increase can be easily passed on to customers & hence company can manage/plan & regulate OPM.

But now, government has decided that APM is going to be abolished in the long term and the initiatives are aggressive in the past 2 months. Hence both gas cost hike and APM abolition are going to affect the fundamentals forever. These are not short term issue like war or any other issues which fades away within a year. If all the cost increase need to be transferred to the customer, then what is the advantage of using CNG for a customer. Definitely, customers will look for alternatives like EV or even petrol.

The government has taken this decision because gas production has declined and imports are increasing. In US, coal to gas transition was due to price competitiveness of gas over other fossil fuels. So the cost advantage of gas over coal does not exist in india.

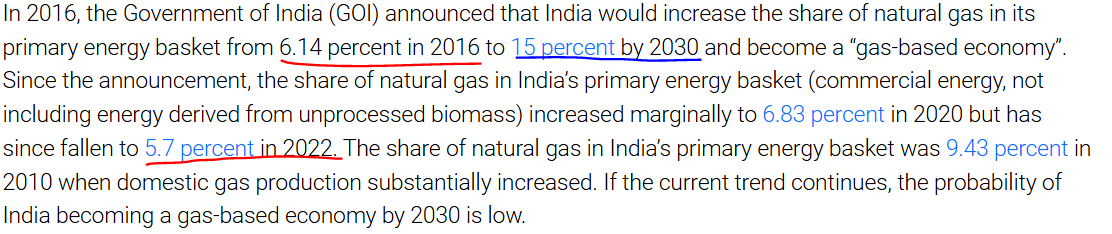

This link https://www.orfonline.org/expert-speak/india-as-a-gas-based-economy-six-years-to-go provides some insights about production vs consumption of CNG.

we cannot have a scenario where production decreases and consumption increases for a long time. This is against economic laws. Then pressure is on government to bear the loss which this government will not.

The entire case is based on ability of IGL to increase gas prices. It could do this successfully in the past however the current circumstances need to be investigated to determine the probability of history repeating itself. Some things have changed as against the past this time. I see 2 problems-

The officials in petroluem and gas ministry believe that these companies are already charging hefty margins and hence can easily absorb additional costs to get gas from new fields. They cite example of IGL making 11% as against companies like IOCL who make 4.5% . So they are asking for break up of final price In short , we will see resistance from government.

2.I am quoting some paras from the article whose link is provided below-

Earlier, on Oct. 25, the PNGRB had issued a notice to CGDs with a proposal to declare 73 networks as common carriers. The notice implies that entities other than CGDs can enter and provide CNG services.

Also read this - Predicting that at one point of time, the allocation from Mumbai High could touch nil, Singh explained, “Initially, priority was given to power, fertiliser and all other sectors.” And now, those sectors don’t get it. Instead, city gas distributors were given priority. However, he said that "overall volume is declining. At one point, maybe in 2–3 years time, it will go down to nil."

Then this– He added that due to the entry of new firms into the gas distribution business, customers are likely to benefit from the increased competition vis-a-vis a reduction in prices.

The article states that production from Mumbai high will go to nil at some point in 2 to 3 years which means IGL gets nothing and has to buy from new wells just like any other company. Now this business will be a commodity business because you get gas at price just like any other company and you also have competition. How can there be a price hike in such a case?

How much does the narrowing of price gap between petrol/diesel and CNG impact IGL’s ability to pass-on price increases? (Key considerations - cost of vehicle, mileage and price differential).

Any roadblock from government in terms of CGD companies increasing prices?

On the flipside, also worth mentioning:

Per kilometer running cost is important to the pricing decision and as mentioned in the newsletter: “Even if the gas cost rises by Rs.5 per kg, the cost per kilometre rises to Rs.2.40 per kg (i.e., an increase of fifteen paise per kilometre).”