Q1’20 results review for IGL:

-

Strong Net sales growth at 22% aided by both pricing & volume improvement YoY (especially in CNG segment) implying that last year’s natural gas price increases have been successfully passed on to the CNG pumping stations. (Might we see further improvement here?)

-

Stable EBITDA margin (~25%) & Net Margin (~14%)

-

Higher interest cost is a watch out item - need for Capex has probably caused the company to take out debt

-

Share of profit from associates (50% stake in MNGL & CUGL) is ramping up well

I like how the story is unfolding as IGL ramps up Capex for coming years and establishes dominance in Delhi & adjacent areas of UP & Haryana as the sole CGD company.

Disclosure - Invested

Nirmal Bang Report on Indian City Gas Sector

We are taking a negative stance on the Indian city gas sector, as it enters a transition phase that will bring current networks in Delhi and Mumbai under open access subject to regulated tariff, even as end-consumer prices of compressed natural gas (CNG) and piped gas (PNG) are left free.

Includes Report of Indraprastha Gas

Funny how the stock prices of IGL and MGL spat in the face of Nirmal Bang analysts price targets.

But if the recent trend is anything to go by, a leader in the space deserve to remain a leader only if it can defend its turf successfully.

It would be good to understand from boarders here, that even after open access is granted to various players, what factors would give us comfort that IGL can defend its turf and continue to grow reasonably from here on in.

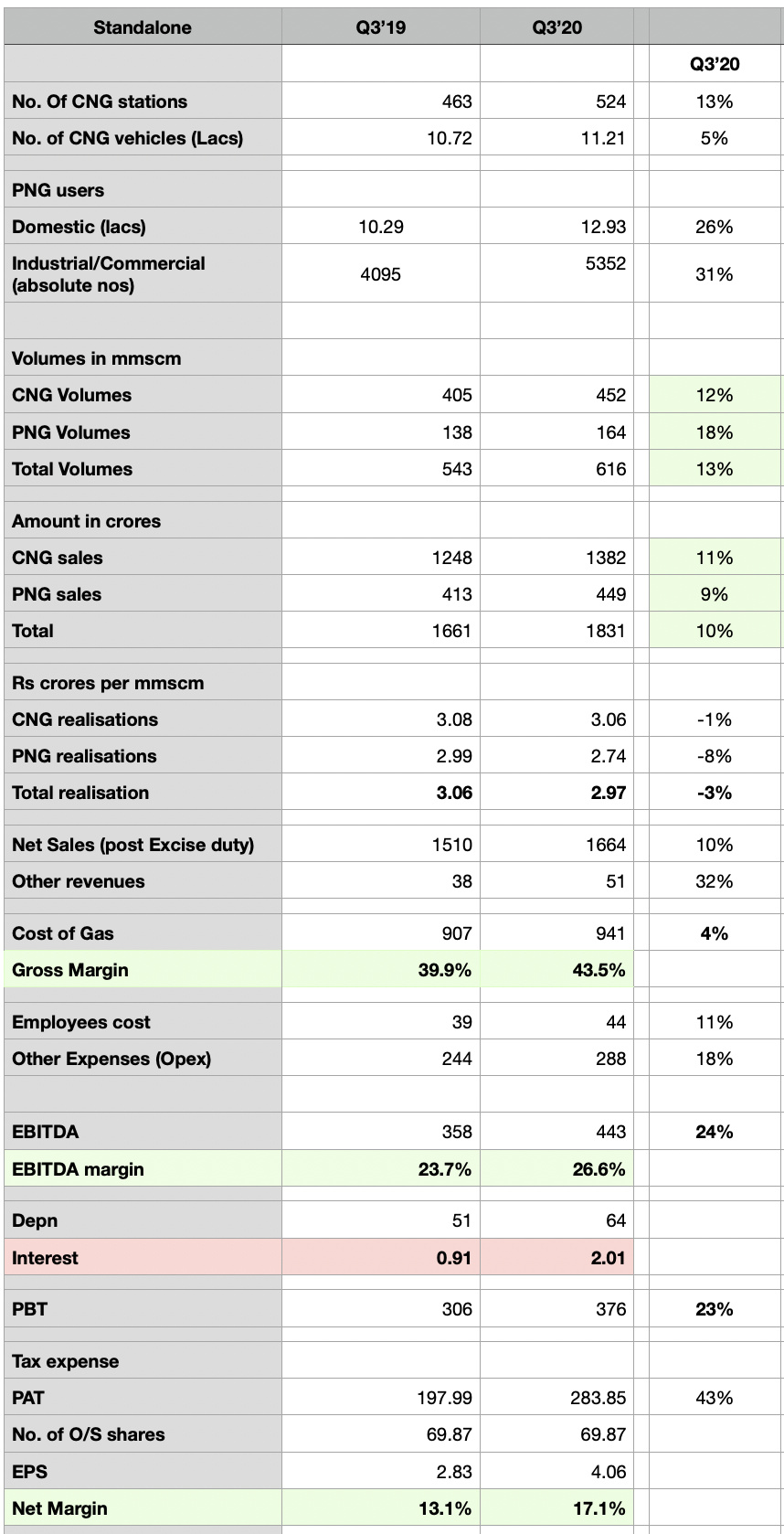

Q3’20 results review for IGL:

-

Added 11 stations in Q3’20 taking total CNG stations to 524 (+13% YoY). CNG vehicle growth @5%. PNG domestic users @ 12.93 (+26% YoY) & I/C users at 5352 (+31% YoY)

-

Net sales growth at 10% Volumes up by 13% (CNG +12%, PNG +18%) & Avg. realisation down by 3% (CNG -1%, PNG -8%). PNG realisation erosion & strong volume growth in the segment indicates that the company is offering some discounts on new connections as it expands in newer GAs (investigating this point further to be sure).

-

Gross Margin @ 43.5% (2% improvement sequentially) EBITDA margin @ 26.6% & Net Margin 17%. These margins might stay high in Q4’20 but normalise from Q1’21 as company has recently cut its prices (link)

-

Share of profit from associates (50% stake in MNGL & CUGL) @ 29 crores

Q4’20 results will be interesting because of Covid-19. On the one hand, CNG volume & I/C usage would take a hit as travel/commercial activity is closed. On the other hand, PNG domestic usage should grow strongly as more people stay home longer & housewives/househusbands spend more time cooking/eating. ![]()

Disclosure : Please treat this as biased opinion since I might be invested in the stock discussed above.

In terms of packing order, sectors like utilities (in particular gas utilities) could be classified in least impacted sectors.

(a) Survival is not an issue a company is debt-free and this is a necessity

(b) Ideally people will not default on utilities payments as it is the last smallest ticket spend generally + they collect deposit upfront + they can easily disconnect the supply which is last thing a consumer would want

In terms of interesting developments in the company recently, lot of details are covered in rating report which came out this month.

IGL is expected to do a Capex of INR 1000 crore in FY20 and INR 1500 crore in FY21 which is to be funded through internal accruals backed by over INR 1000 crore GCA per annum. This is huge if we compare this to yearly operating cashflows of last couple of years + interesting thing is - all is from internal accruals without taking any debt.

This at ~30% incremental RoCE could ensure sustainable growth momentum for next few years. No wonder TTM profit growth ~50%.

IGL has expanded its area of operations in Rewari district, Gurugram, Karnal, and the sales volume in this area is expected to increase gradually with the rollout of increased infrastructure. Further, the company won one GA in 9th round, namely, Meerut (Except areas already authorized), Muzaffarnagar & Shamali Districts (U.P.) and three GAs in 10th round, namely, Kaithal District (Haryana), Ajmer, Pali & Rajsamand District (Rajasthan) and Kanpur (Except area already authorized) District, Fatehpur & Hamirpur Districts (U.P.)

In terms of price volume action also it has shown good divergence and almost recovered fall from its highs.

Overall, interesting to watch-out for this company for next few years, particularly in the near term when all companies would be bleeding and this can post healthy growth.

Disclosure: Tracking; Not a buy/sell recommendation, kindly do your own due diligence

Generally utilities are one of the least impacted segment. But this would not be the case with CGDs because of following reason -

- There major volume and profit driving segment i.e CNG is having negligible sales (upto 60% of the volumes are from CNG). Also CNG is the most profitable product segment. CGDs earn up to Rs 20/Unit of CNG sold. High volume High Margin business. With the sale of CNG nearly hit badly due to stop of commercial transportation there would be a big hit on profits in atleast Q1.

- Even the commercial and industrial demand is hit as restaurants and industry are also closed down.

- ONly PNG segment is not hit but the volumes are very low in PNG ( around 10% of total volumes). Also PNG is one of the least profitable segment.

Expect a dismal Q1 for CGDs.

Taken from moneycontl article

- The lockdown has halted industrial activity and hit transportation

- Domestic PNG consumption is expected to remain stable/grow

- IGL and MGL derive a substantial portion of their revenue from the badly hit CNG segment

- Exposure to Delhi and Mumbai could hurt earnings due to longer lockdowns

- Lower gas prices and healthy balance sheets are positives

In the first nine months of FY20, nearly 72 percent of IGL’s volumes were coming from the CNG segment with a 13 percent exposure to the industrial PNG segment and only 6 percent volumes coming from the domestic PNG segment. Only 55 of the 155 CNG stations of the company in Delhi NCR are currently operational.

This puts IGL in the high risk category and substantial adverse implications could be seen on the company’s sales volume in Q1FY21 due to the current lockdown. Moreover, aided by the steep fall in LNG prices and revision of domestic LNG rates, IGL has taken a price cut recently of Rs 3.2 to Rs 3.6 per kg in the CNG segment and Rs 1.55 per scm (standard cubic metre) in the domestic PNG segment from 1 April. This would lead to lower per unit realizations.

Sector trends

Dip in LNG prices – a positive:

Lower price of alternate fuel – negative:

Lower conversions – negative: The countrywide lockdown is resulting in lower travel and lower availability of workshops. This will affect the CNG conversion rate.

Strong balance sheets – positive:

I was looking at IGL as an investment prospect as it has been an excellent compounder over the past five years.

Two mains concerns I had were

- Laggard stock performance from 2012 to 2015

- CNG shift to EV

Based on some study I’ve done, let me try to share my thoughts on that.

Laggard stock performance from 2012 to 2015:

In April 2012, PNGRB came up with some regulations capping the amount IGL can charge its customers. It not only capped the amount but also asked IGL to return the money it earned above the cap from 2008 to 2012.

This was rejected by the Hon’ble High Court of Delhi, however, PNGRB has taken the petition to Hon’ble Supreme Court of India. This petition was resolved in favour of IGL in 2015 and hence the market didn’t re-rate the company over the period of 2012-15 and the company traded at laggard valuations of 10-15 PE.

Once the petition is resolved, the company is re-rated to valuations of 25-30 PE and the regular business momentum ensured that profits are up 2x over the past 5 years.

More details on the case here:

Supreme Court’s ruling here would ensure that IGL retains its pricing power. I have done some analysis of how the cost / revenue / spread on per unit natural gas has moved for the company.

Pasting below my table on NG volumes:

| 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | ||

|---|---|---|---|---|---|---|---|---|

| CNG (mmscm) per day | 4.39 | 3.87 | 3.47 | 3.07 | 2.94 | 2.81 | ||

| PNG (mmscm) per day | 1.51 | 1.31 | 1.11 | 0.93 | 0.90 | 0.97 | ||

| Total (mmscm) per day | 5.90 | 5.18 | 4.58 | 4.01 | 3.84 | 3.79 | 3.67 | |

| Volume per year (mmscm) | 2155.33 | 1891.17 | 1674.51 | 1465.05 | 1403.57 | 1383.65 | 1339.55 | |

| Volume Growth | 1.13 | 1.12 | 1.14 | 1.04 | 1.01 | 1.03 | #DIV/0! | |

| Total Cost of Gas (cr) | 3397.89 | 2491.81 | 2083.98 | 2275.37 | 2340.98 | 2681.43 | 2197.75 | |

| Cost / natural gas (cr / mmscm) | 1.57 | 1.31 | 1.24 | 1.55 | 1.66 | 1.93 | 1.64 | |

| Total Revenue from Operations (cr) | 6361.87 | 5071.57 | 4222.51 | 4064.21 | 4059.64 | 3922.16 | 3366.99 | |

| Revenue / natural gas (cr / mmscm) | 2.95 | 2.68 | 2.52 | 2.77 | 2.89 | 2.83 | 2.51 | |

| Spread / natural gas (cr / mmscm) | 1.38 | 1.37 | 1.28 | 1.22 | 1.23 | 0.9 | 0.87 |

As one can see, the company is able to increase the price whenever the price of natural gas increases. It did pass down the price whenever there is a decrease in its costs, but the spreads it is earning on the gas is in a strong uptrend.

CNG shift to EV:

As per Ind-Ra Report released on November 2017, 2/3rds of CNG volumes are driven by buses even though they form only 5% of the vehicles. Probably because of low mile-age of buses and they run for the whole day. This implies 50% of the revenues of IGL are from buses.

And general expectation is that buses would be the first ones to adopt EVs. We can also see that Delhi govt already released tenders for 1000+300 buses last year, as mentioned in this article.

To put things in perspective, total number of buses owned by Delhi Transport Corporation (DTC) is 3800 as per Wiki. As per above article, Delhi govt is planning to increase the fleet size to 5500. This incremental addition of buses seems to be coming from E-buses over CNG buses and can impact growth for next 2-3 years.

Having said that, there was a big positive development on conversion of Diesel vehicles to CNG vehicles for “Inter-city” buses. Technology has been developed to fill buses with CNG which will enable them to be driven for 1000 kms in just one single fill. This will open new bus markets for IGL around Delhi. Below article has more details and it says buses to Delhi from Chandigarh, Dehradun, Agra and Jaipur can run on CNG with this technology.

IGL owns rights for strategic GAs for buses connecting Delhi to Chandigarh, Dehradun, Agra and Jaipur. GAs which IGL has won recently include Kaithal, Ajmer, Pali, Rajsamand, Kanpur, Fatehpur, Hamirpur, Rewari, Karnal, Meerut, Muzaffarnagar, Shamli. So a very good eco-system for CNG public transportation can be built around this area.

Delhi to Chandigarh => IGL has rights for Kaithal and Karnal GAs

Delhi to Dehradun => IGL has rights for Shamli, Meerut and Muzaffarnagar GAs

Delhi to Agra => No rights in Delhi to Agra route GAs but has rights to Kanpur, Fatehpur and Mirpur GAs which come after Agra

Delhi to Jaipur => IGL has rights for Rewari in this route. Other districts like Ajmer, Pali and Rajsamand come after one crosses Jaipur.

My personal opinion is that Govts may push Electric Vehicles for intra-city public transportation but highly unlikely that we will such push for inter-city public transportation. The incremental markets which IGL can penetrate onto over the next 10 years look huge if the inter-city CNG public transportation picks up.

Coming to the other 1/3rds of CNG volumes, they should be coming from private cars / autos / taxis. I think the trend should continue here. Lots of auto companies are rolling back their EV investments amid the virus crackdown.

Ind-Ra Report which claims that 2/3rds of CNG volumes are from buses:

https://www.indiaratings.co.in/PressRelease?pressReleaseID=29766&title=india-ratings-affirms-indraprastha-gas-at-‘ind-aaa’%3B-outlook-stable

Thanks!

Some extension of my previous post:

As per IGL’s investor presentation, there are 26k buses using CNG in NCR.

If DTC has buses in the order of 4k to 5k, other buses must be private buses. But 20k+ private buses sound a bit too high. In fact 26k buses for NCR also sounds quite high. If anyone can post their thoughts on the bus numbers, it would be very helpful.

Look at Slide 14 of this PPT.

I have never been to NCR.

Discl: No holdings. Studying. Please do your own research.

DTC could never cope with demand, it is always operating at loss and in no position to spend on fleet expansion, so the govt allowed private operators to run services alongside DTC, exactly on the same routes, almost no difference in their operations, except ownership.

This happened about little over 2 decades ago and soon private operators (under this scheme called stage-permit) totally overwhelmed the DTC which likely took the opportunity to scale back its loss making operations.

Realize that Delhi had no rail system, compared to the other 3 metros then, it was totally dependent on buses for public transport. Delhi has grown vastly and even with metro the bus network size seems correct.

There are so called chartered services for offices, school buses, they all count. All public transport was made 100% CNG about more than a decade ago.

Has anyone studied several possible bear cases for this stock?

-

What if the govt allows competition to come in aka private players to use OMC network of stations to market CNG?

-

How will margins be impacted if the subsidised 110% allocation of domestic gas to CGDs goes away and IGL has to pay a higher rate to procure gas?

-

What if the prices of natural gas increase (very unlikely in the current scenario but worth exploring)?

-

What if PNGRB figures out another way to control IGL’s prices?

-

What about new more efficient modes of transportation viz. EVs, shared mobility, metros etc?

Would love to read a report that addresses these questions in detail! If not, I’ll myself work on each of these points and share my findings here.

Very good set of questions @AKGupta . Let me try to answer those.

-

CGD players have marketing exclusivity for some time and until then no other player can sell CNG / PNG in that GA. After the marketing exclusivity period is completed, they will still have infrastructure exclusivity as long as the CGD player is able to meet their targets. So the competitors will have to pay additional tariff to infrastructure owners in that GA to use their pipelines, implying that the GA bid winner will always be able to sell the gas cheaper than new players. How much cheaper is a question I have too, but the real point is the GAs owned by CGD players are so under-penetrated that everyone is better off focussing on their GAs than invading other CGD players’ GAs

-

Margins will definitely be impacted in CNG and Domestic PNG businesses. Company has history of being able to pass down the prices to consumers but if 110% allocation benefit is removed, the hike in input costs would be too much to pass down to consumers in my opinion but at the same time I think this is a very low probability event

-

Natural gas price keeps moving over time and IGL has always demonstrated their ability to pass down the price increase to consumers. If you look at the spread they are earning per mmscm, it is in a secular trend. Tagging a post I made above:

- Yes, this is the reason I’m not buying at current valuations. PNGRB lost the case with IGL at Supreme Court but they might come up with some other witty rule to curb the pricing power being enjoyed by CGD companies. As pointed by industry veteran @sharrmasks, it is not in the Govt’s interest to continue the current situation between producers, mid-stream distributors and consumers. Look below at his post.

- EVs I believe would first affect Diesel and Petrol players. I think given the status being given to NG by govt, highly unlikely that it will kill this infrastructure for EVs whose technology is yet to proved in India. Also most transport corporations have dual fuel policy like they should not be depending on a single fuel (Eg: BEST in Mumbai). In my personal opinion, EVs and CNG transportation would co-exist. One second order impact is that all the OMC players may convert themselves into CNG players once diesel and petrol vehicles are not visible on the road and this could increase competitive intensity. Though infrastructure exclusivity would help the CGD players, I’m not sure yet how much tariff they can charge and how much of an impact it would make

Discl: No holdings. I like IGL but not buying at current valuations. The biggest risk for me in this business is regulatory risk

@AKGupta I did not get your second question regarding subsidised gas. Can you please elaborate.

Points to note from the CARE Rating

- Due to high level of entry barriers, no competitor has come up in Delhi/NCR till date.

- The PBILDT margin of IGL declined in FY19 to 22.99% from 25.37% in FY18 (238bps) on account of increased cost of APM Gas.

- Companies in the CGD space have the flexibility to increase the price of CNG and pass the rise in cost of raw material to customers through marketing margins, the increase will only be to remain competitive in the market against other alternative fuels.

- IGL is expected to do a Capex of Rs. 1000 crore in FY20 and Rs. 1500 crore in FY21 which is to be funded through internal accruals backed by over Rs. 1000 crore GCA per annum => Huge growth tick

Only short term issue is the subdued demand for CNG as transportation as a whole is in shutdown mode, we can take hints from other European countries as to what will happened to the transportation industry in the near term.

Anyone with how much will this effect the sales?

For point No 1 ,regarding competition using existing player’s gas network. The draft that PNGRB uploaded and model PNGRB is thinking is giving access to only 20% capacity of the Gas network.Rest 80% volume will be with the existing company. Its not like competitor will come in a GA and sell as much as they can.Almost 1 year back the draft paper was uploaded by PNGRB.But that was the thinking.Page 5 clause No 7.NF_22082019 (1).pdf (264.0 KB)

I am trying to figure out how the JV with GAIL and BPCL works for IGL in terms of operation in the GA’s allocated in the recent bidding to BPCL & GAIL?

Also if one could help me understand the growth perspective in terms of GA in which IGL is wishing to expand upon, 11th round of bidding is in near term, I couldn’t find out the complete result of the latest bidding, or is it just these 4 areas as mentioned in the below article?

This article by liveMint did state that IOC was the biggest winner, but then IGL don’t operate in Bihar or Jharkhand or nearby areas.

Also as per the current allocated GA’s how much growth opportunity is there for IGL for the next 8-10 years given that it doesn’t win any more further bidding?

You statement reaffirmed by this article

Different states charge different VAT on CNG. For example, while Delhi completely exempts VAT on CNG, the same in Uttar Pradesh, Maharashtra and Gujarat is as high as 12.5 percent, 13.5 percent and 15 percent, respectively

Is this because NCT Delhi is 5% holder in IGL?

How could they do it abruptly!!!

Companies don’t need city gas license to start LNG station, says regulator

Read more at:

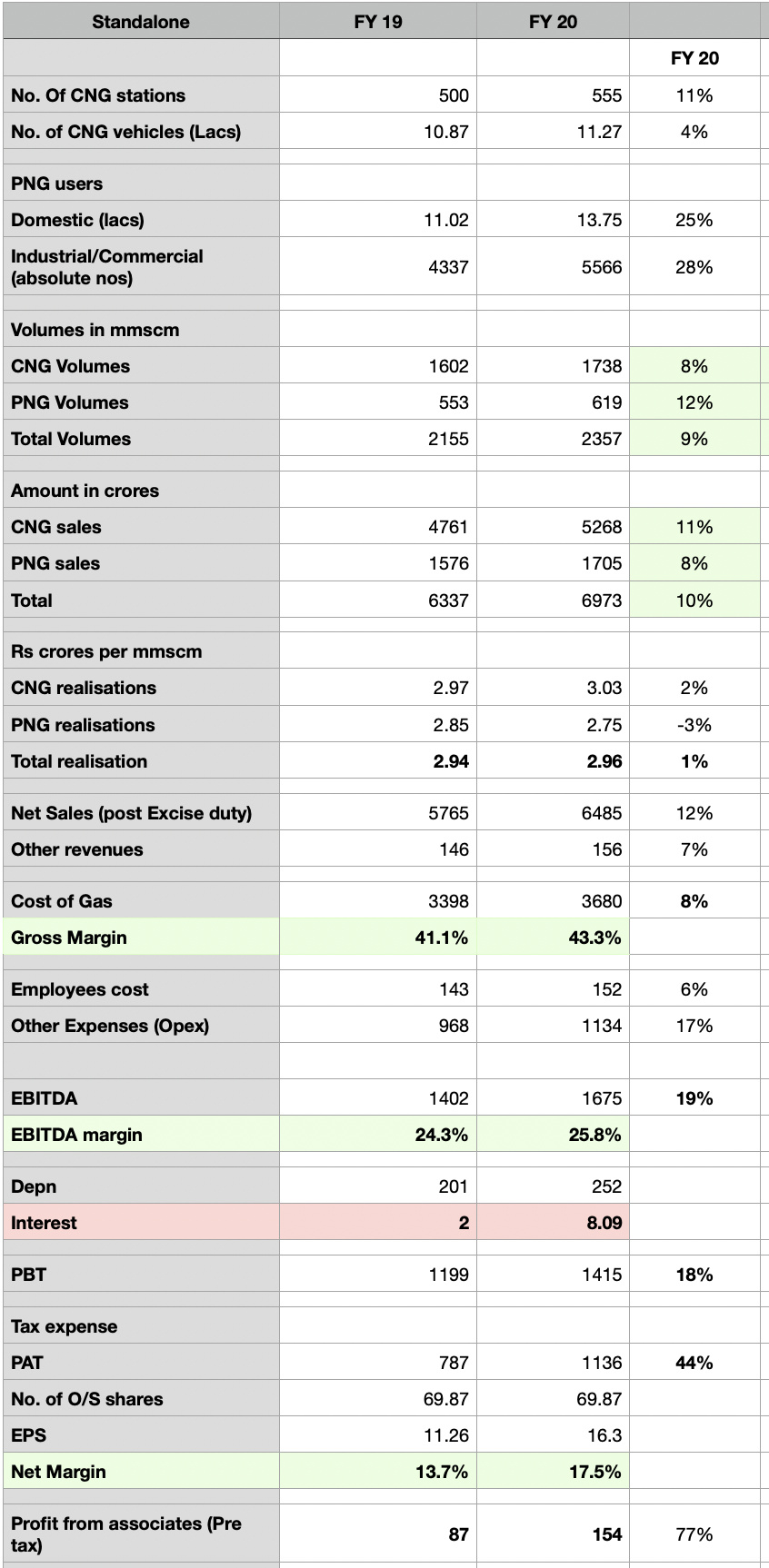

Update on Full year FY20 results : (All numbers are standalone)

-

No. of CNG station are up 11% to 555 while no. of CNG vehicles increased by only 4%. CNG sale volumes are up by 8% to ~1700 mmscm. (4% vehicle population growth is worrying)

-

No. of PNG users are up 25% to 13.75 lacs households. Industrial/Commercial users are up 28%. PNG sale volumes are up by 12% to ~600 mmscm.

-

Total sale volumes are up 9% to a little over 2300 mmscm and average realisation is up 1% to Rs. 30 / scm. Total sales are up 10% to ~Rs. 7000 crores while Sales (net of excise duty) are up 12% at ~6500 crores.

-

Cost of gas is up 8% to Rs. 3700 crores resulting in a Full year Gross Margin of 43% (better by 2% vs last year). EBITDA margin has also improved by 2% to 26% YoY. Total EBITDA is at ~1700 crores.

-

Interest cost is at Rs. 8 crores up from Rs. 2 crores in FY19. (I checked the Balance Sheet and apart from lease liabilities of Rs. 77 crores, there is nothing on long term debt). Still given an EBITDA of ~Rs. 1700 crores, Rs. 8 crores in interest in puny to warrant extensive analysis.

-

Profit before taxes are up by 18% to over Rs.1400 crores (Looking at PBT is better to normalise for impact of mid year corporate tax cuts). Net Profit margin at 17.5%.

-

The 2 associate companies - MNGL and CUGL - have contributed 150 crores to IGL’s net profits (up 77% YoY).

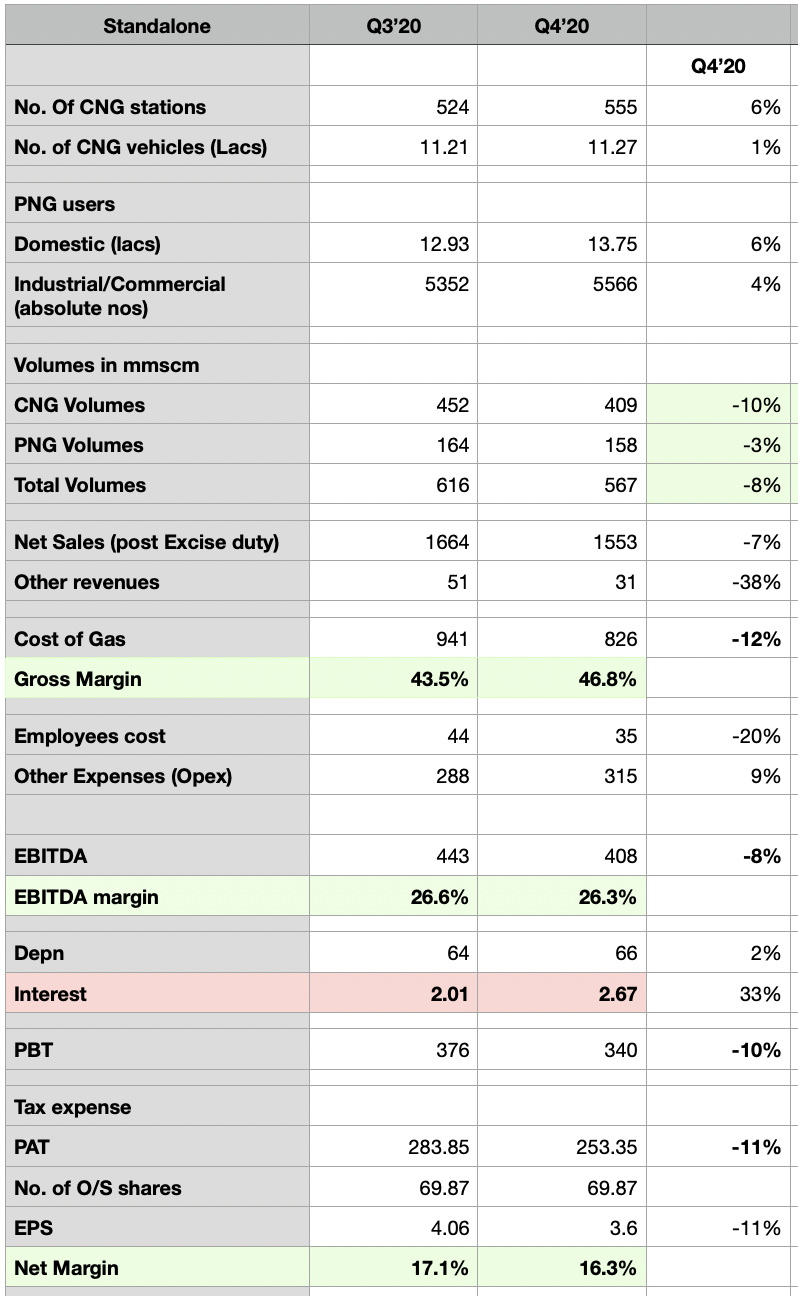

Perhaps more interesting is to look at Q4 performance vs Q3 (so that some impact of city wide lockdown is captured) : Volumes are down 8% sequentially and Net sales (post excise) are down 7% while cost of gas is down 12%. EBITDA is down by 8% while PBT is down by 10% to 340 crores for Q4. Given that CNG still makes up 75% of IGL’s business, I expect sales volumes to decline further in the coming quarter (Q1 FY21).

Disc. : Have a tracking position