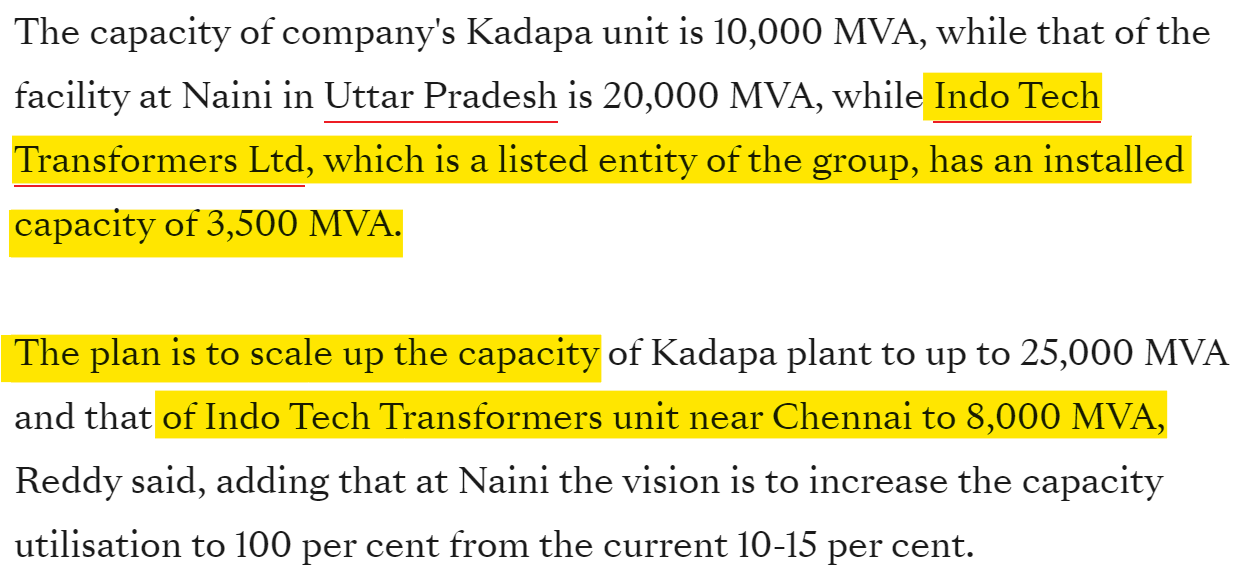

About the company -

Indo Tech Transformers Ltd was, established in 1976 is one of the leading transformer manufacturing Companies situated in Southern India having manufacturing facilities at Kancheepuram in Tamil Nadu. Over 56000 Transformers of different ratings up to 245 KV are in service in various Substations and Industries across India and around the world.

The Company’s facilities are established keeping in mind the best available infrastructure and with state of the art equipment’s for manufacturing and testing. The Extra High Voltage (EHV) transformers facility is totally dust free to enable manufacture transformers under very sterile conditions. The testing lab accredited by NABL equipped to carry out all routine and special tests as required by various national and international standards.

Indo Tech Transformers Limited is engaged in the business of manufacturing Power, Distribution, Invertor, Convertor special application transformers, catering to various industries like Transmission, Generation, Hydro, Wind, Solar, Steel, Cement, Textiles, Utilities, DESCOMS etc.

Among our clients are some of the renowned companies like TNEB, NTPC, ADANI, L & T, ABB, SIEMENS NLC, VESTAS, DVC, GAMESA, BGR, SUZLON, TATA PROJECTS, KEC INTERNATIONAL, REGEN POWER TECH, RELIANCE, WALCHAND, TKIS, DOOSAN, GE etc. and leading Hotels, Hospitals, Steel and Cement Plants etc. Our transformers are in service at many Ferrous and Non-Ferrous metal industries throughout the country. Some of our main customers include companies like JSW steel, Jindal Steel and Power, BALCO, Jayaswal Neco Industries etc. Additionally, we have served industrial clients through various leading electrical consultants like M.N. Dastur & Co, EIL, Mecon, Fichtner, PGCIL, Avant Garde, TCE etc. We are also approved by leading Inspecting Agencies like RITES, LLOYDS, CPRI, BUREAU VERITAS, TUV, SGS etc. (1)

Promoter Change

In Sept 2020, Shirdi Sai Electricals Ltd (SSEL) acquired 69.3% stake in the Co from Prolec GE Internacional, the erstwhile promoter. Consequent to the change in controlling stake from Prolec GE to SSEL, the Co has entered into a Transitional Trademark License Agreement for using the brand name “PROLEC” and shall pay 2.5% of the turnover as royalty for the brand usage to Prolec GE Internacional. [2]

| Narration | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Trailing | Best Case | Worst Case |

| Sales | 93.86 | 156.91 | 189.87 | 148.81 | 220.17 | 213.39 | 205.33 | 206.00 | 280.07 | 370.90 | 417.32 | 491.19 | 412.79 |

| Expenses | 108.83 | 166.39 | 190.80 | 151.74 | 221.37 | 215.47 | 203.43 | 194.72 | 257.96 | 334.57 | 373.19 | 439.25 | 398.61 |

| Operating Profit | -14.97 | -9.48 | -0.93 | -2.93 | -1.20 | -2.08 | 1.90 | 11.28 | 22.11 | 36.33 | 44.13 | 51.94 | 14.18 |

| Other Income | 10.89 | 16.69 | 12.76 | 1.79 | 4.55 | 1.24 | 5.42 | 2.92 | 1.69 | 2.66 | 4.27 | - | - |

| Depreciation | 2.99 | 5.18 | 5.35 | 4.82 | 4.74 | 5.19 | 4.79 | 4.82 | 4.52 | 4.82 | 5.31 | 5.31 | 5.31 |

| Interest | 11.73 | 5.77 | 2.45 | 3.11 | 2.30 | 2.36 | 2.43 | 3.02 | 6.80 | 8.47 | 3.79 | 3.79 | 3.79 |

| Profit before tax | -18.80 | -3.74 | 4.03 | -9.07 | -3.69 | -8.39 | 0.10 | 6.36 | 12.48 | 25.70 | 39.30 | 42.84 | 5.08 |

| Tax | - | - | - | 2.21 | - | - | -1.82 | 0.07 | 0.29 | - | 5.55 | 14% | 14% |

| Net profit | -18.80 | -3.74 | 4.02 | -11.27 | -3.69 | -8.39 | 1.92 | 6.29 | 12.19 | 25.70 | 33.75 | 36.79 | 4.36 |

| EPS | -17.74 | -3.53 | 3.79 | -10.63 | -3.48 | -7.92 | 1.81 | 5.93 | 11.50 | 24.25 | 31.78 | 34.64 | 4.11 |

| Price to earning | -3.38 | -49.44 | 49.62 | -19.50 | -48.45 | -13.19 | 40.30 | 14.55 | 18.84 | 7.09 | 29.87 | 29.87 | 17.59 |

| Price | 59.90 | 174.45 | 188.20 | 207.35 | 168.65 | 104.40 | 73.00 | 86.35 | 216.70 | 171.95 | 949.30 | 1,034.84 | 72.22 |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.93% | 5.48% | 7.89% | 9.80% | 10.57% | ||

| TRENDS: | 10 YEARS | 7 YEARS | 5 YEARS | 3 YEARS | RECENT | BEST | WORST | ||||||

| Sales Growth | 16.50% | 10.04% | 10.99% | 21.79% | 32.43% | 32.43% | 10.04% | ||||||

| OPM | 3.43% | 4.35% | 5.61% | 8.14% | 10.57% | 10.57% | 3.43% | ||||||

| Price to Earning | 26.71 | 22.13 | 22.13 | 17.59 | 29.87 | 29.87 | 17.59 |

Risks

Power sector is a highly capital-intensive business with long

gestation periods before commencement of revenue streams,

especially for projects using conventional technology. The

major risk factors affecting the Company are over capacity in

industry, non-lifting of ready materials due to constraints at

customers’ end thereby building inventory and creating liquidity

issues. Increase in receivable positions due to delay in payment

by certain customers and uncertainty in execution of low fixed

price orders. Other notable concerns include:

1. Raw material price volatility

Copper and Electrical grade Steel (technical shortform CRGO)

are the major raw material which contributes more than 60%

cost of total raw material.

Adverse price movement of both commodities can impact

the margins of the Company. The Copper price is determined

by the London Metal Exchange (LME). The wide fluctuation

of rupee against US Dollars also affects margin since the key

raw materials, viz. copper, transformer oil, special steels for

lamination, etc., are of import origin.

2. Overcapacity in industry

Due to the entry of large number of players during

favorable time, overcapacity continues to be a major negative

factor in the industry as a result aggressive pricing is undertaken

by some of the Transformers manufacturers, which could

impact margins.

3. Financial Health of State Discoms

The financial health of electricity DISCOMs is an area of

key concern threatening the very viability of the power sector.

DISCOMs are the weakest link in the electricity supply chain and

have been suffering on account of operational inefficiencies;

inadequate investments in distribution network as well as lack

of timely and adequate tariff revisions to help recover costs.

4. Delay in payment to IPPs by EBs

There is considerable delay in payment to Independent

Power Producers (IPPs) by Electricity Boards (EBs). This delay

affects financial health of IPPs and in turn affects cash cycle of

Original Equipment Manufacturers. OEMs have to be choosy

in accepting orders from such IPPs and this affects year to year

growth.

5. Utility Orders

The transformer industry largely depends on the spending

from transmission and distribution utilities and recent tenders/

ordering activity by utilities clearly demonstrate the downward

trend. Lack of funds is one of the key reason behind it. All

Contracts awarding by the utilities are based on low price (L1)

bidder which resulting in price war with unorganized players

without compromise on the quality is the challenge for the

organized quality driven Companies. The payment terms of

utilities are generally high credit period compared to private

parties which impact the Company’s cash flow.

6. Increase in working capital borrowings and high working

capital intensity

Lower cash accruals, delayed payments from clients including

state power utilities and private players and delays in project

execution results in tightening of liquidity. Further, the

operations of manufacturers in India are more working capital

intensive mainly due to relatively higher inventory holding and

receivable period, lack of adequate mobilization advances.

This is mainly due to lack of product standardization, delays in

processes of testing and issuance of completion certificates and

delays in receipt of payments

Disclosure - Invested