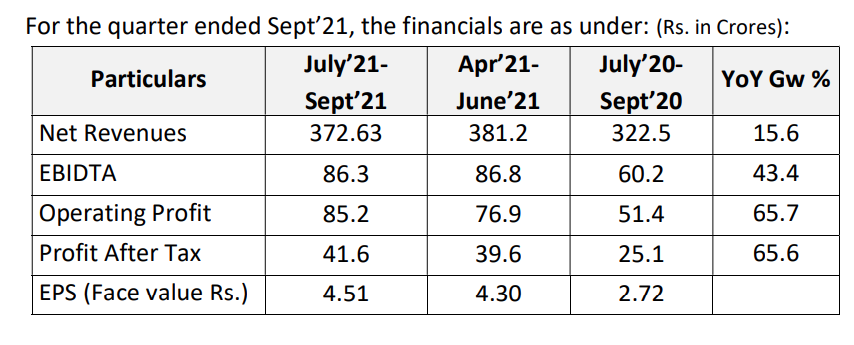

Indoco Remedies Q4 concall highlights -

Revenues - 428 vs 409 cr

EBITDA - 65 vs 81 cr

EBITDA margins at 15 vs 20 pc

PAT at 30 vs 36 cr

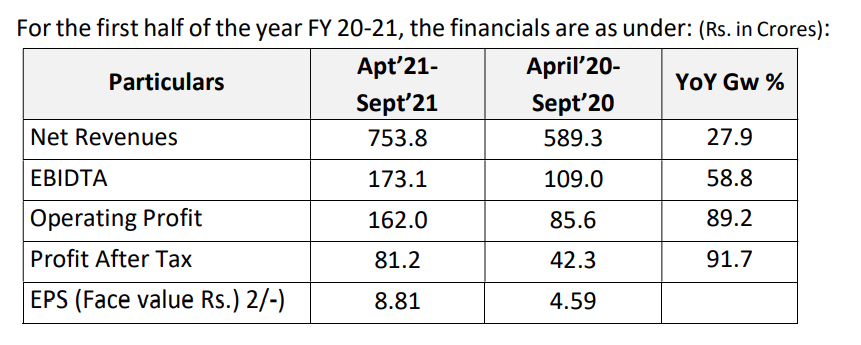

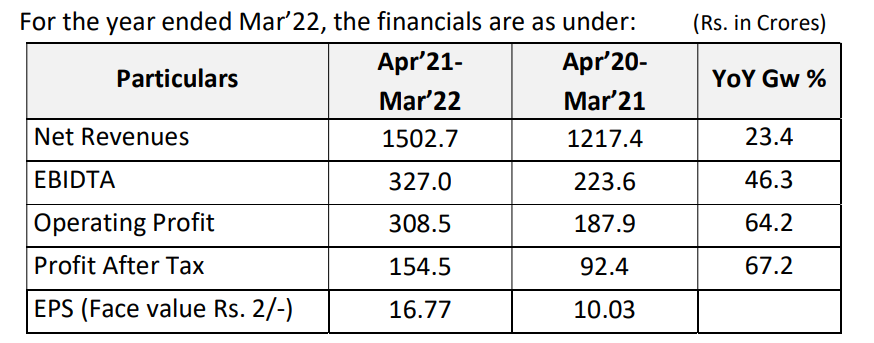

For full FY 23 -

Revenues - 1669 vs 1541 cr

EBITDA - 286 vs 328 cr

EBITDA Margins at 17 vs 21 pc

PAT at 142 vs 150 cr

Base was very high due COVID related sales in FY 22

Domestic brand Cyclopam (used to relieve cramps) grew at a rapid pace

New product launches generated aprox 30cr sales

Top 20 brands of Indoco India generated double digit prescription growth

Two of company’s brands are in top 300 brands in IPM. Cyclopam jumped 27 ranks in FY 23

Company has three brands that generate > 100 cr and 04 brands that generate > 50 cr sales

Launched a D2C division this year for a few OTC dental brands

Plant-1’s import alert lifted by FDA

Plant-1 (solid dosage facility), now can export to US

In Europe, garnered 30 pc and 20 pc Mkt share for Lacosamide (to control seizures) tablets and Injections respectively

In Germany, company’s Allopurinol (to manage gout that causes intense joint pain) has 70 pc Mkt share

Business promo & marketing spends back to pre Covid levels

IPM rank at 27

Formulations-

Q4 India formulations sales at 185 cr, down 4 pc

FY 23 India formulations sales at 797 cr, down 1 pc

(India business had a big Covid base)

Q4 Intl formulation sales at 216 cr, up 14 pc

FY 23 Intl formulation sales at 754 cr, up 21 pc

Within Intl Mkts -

Q4 Revenues from regulated Mkts grew 5 pc to 163 cr

FY 23 revenues from regulated Mkts grew 21 pc at 610 cr

APIs -

Q4 API business grew by 75 pc to 23 cr

FY 23 API business grew by 12 pc to 71 cr

ndoco CRO operations-

Q4 revenues at 4.5 cr,down 5 pc

FY 23 revenues at 17 cr,up 12 pc

Base yr’s Covid sales in India were around 40 cr because of which company could not grow this year in the domestic market

Post clearance of Plant -1, US sales should also pick up next yr

Growth in advertising and sales promotion likely to moderate next year

Legal cost incurred this yr (aprox 5-6 cr) is unlikely to recur next yr

Company confident of doing 18-19 pc EBITDA for FY 24 and 25 ( that’s a descent jump from Q4 levels )

FY 24,25 growth expectations at 15 pc plus CAGR ( plus margin expansion )

US business has healthy order book. Likely to grow US business by 25-30 pc this yr

2.5 pc of domestic sales from new products (launched within last 2 yrs)

Expect the toothpaste business ( medicated ones ) to do better due to the D2C push initiatives that company shall take in FY 24

Attrition in MRs is an issue that company intends to resolve this year

Expect 3-4 approvals in US this yr - mostly in ophthalmic space

Expect a price hike of 5-6 pc in domestic mkt for FY 24

Company has overpromised and underachieved in the past 2-3 yrs. Mrs Parandikar was mindful of that. Intends to correct this in FY 24. The proof of the pudding will be in the numbers though

Ophthalmic and Injectables supplies to US involve very complex manufacturing practices. Company has been learning this over the last few years

Capex plan for FY 24,25 - aprox 125 cr

Disc: holding a tracking position. Hope to see an improvement in business momentum next year