|

Highlights of the Call by Capital mkt: The Net revenues grew by 16.1% to Rs 226.4 crore YoY to Rs 195.0 crore for the quarter ended September 2014 and PAT grew by 40% YoY to Rs 22.4 crore for the same period.The domestic formulation business revenues grew by 14% to Rs 137.4 crore for the quarter ended September 2014. It has exceeded the Pharma Industry growth rate of 12.3% for the quarter. It has launched six new products in the domestic market during the quarter.The International business revenues grew by 21.1% at Rs 81.7 crore for the quarter ended September 2014. In the regulated markets, contribution of Europe was at 61.9%, followed by US at 21.9%.The favorable product mix bought down the material cost during the quarter. The depreciation / amortization are at Rs 13.1 Crore as against Rs 7.7 Crore for the same period last year. The increase is mainly on account of change in the basis of calculating the depreciation which was necessitated due to introduction of new Companies Act 2013.As per AWACs data, the Indian Pharmaceutical Market (IPM) grew by 12.3 % at Rs 22122 crore in Q2'FY15 as against Rs 19701 crore in Q2'FY14. The growth of 12.3% in this quarter is higher than the growth of 9.5% of previous quarter and also against the growth of 4.3% of corresponding quarter last year. During the quarter, acute segment grew by 11.7 % and chronic segment grew by 13.7 %. Amongst the 20 therapies, the contribution of 5 top therapies was 57% of the IPM market. The Anti-infectives grew by 10.6% to Rs 3803 crore, Cardiac grew by 10.4% at Rs 2596 crore, Gastro Intestinal grew by 13.7% to Rs 2601 crore, Vitamins/Minerals/ Nutrients grew by 12.8% to Rs 2004 crore, Anti Diabetic grew by 23.9% to Rs 1627 crore during the quarter respectively.It has launched a unique Anti-Obesity formulation for the first time in India. The novel formulation comprises of Leucine + Pyridoxine that will revolutionize the treatment of overweight and obesity. It is planning to file 10 Abbreviated New Drug Applications (ANDAs) from its sites during the current year. The UK MHRA (Medicines and Healthcare Products Regulatory Agency) inspected Company's oral (solid and liquid) dosages and creams & ointments facility at Goa (Plant I) in August'14. The facility received MHRA re-approval with no critical and no major observations. During the quarter, approval for two ANDAs was received by Watson (Actavis) and Indoco expects to commence supplies against these approved products (ANDAs) soon. Watson (Actavis) also received a tentative approval for a Para IV application filed from Indoco's site.It expects one or two products approval from US FDA in the H2'FY15. The regulated market grew by 22.8 % to Rs 65.5 crore for the quarter ended September 2014. In the Regulated markets space, the contribution of Europe was the highest at 61.9%, followed by US at 21.9 % and South Africa, Australia & New Zealand put together at 16.2%. Europe, Australia, Africa and Asia registered good sales growth over the same quarter last year.The emerging markets for the quarter grew by 11.2 % to Rs 9.5 crore for the quarter ended September 2014. The Kenya, Tanzania, Myanmar & Sri Lanka registered good sales growth.The Revenues from Active Pharmaceutical Ingredients (APIs) business grew by 10% to Rs 13.5 crore for the quarter ended September 2014. The field force is 2300 as on 30thSeptember 2014. It expects to add 250-300 MR's during the year.The domestic business will continue to focus on brand building, new product launches, concentrated efforts to increase share in chronic segment and penetration in Tier II and Tier III towns, especially in Northern and Eastern Region. Though the domestic formulations business will grow at a much higher rate than the industry average, its proportion to the total revenues will reduce over a period of time due to faster growth expected from international business.Its international business will continue to focus on its core competencies, viz., Research & Development and Manufacturing. The Company will continue to remain the preferred partner, offering complete solutions to generic companies worldwide. Additionally, it will also exploit the larger opportunities through alliances in major markets. Going forward, the US business is expected to grow speedily as ANDAs will be commercialized at regular intervals. While surging ahead in the Regulated Markets, Indoco is also consolidating its position in the Emerging markets through active brand promotion. Part of the emerging market is exploited through distributors appointed by Indoco and the other part through alliances.The R&D expenses are Rs 4.9 crore (2.2% of net sales) in Q2'FY15 as against Rs 3.8 Crore (2% of net sales) Q2'FY14. The R&D expects to go to 3% of next 3-4 quarter and expects to 4% of sales in next 3-4 years.The EBIDTA margins are sustainable on the back of business expansion in domestic and international market going forward. It further indicated when revenues reaches Rs 1000 crore margins will be 21%.The tax rate expected to be 27-28% going forward. |

Attended AGM of this company. Year 2015-16 seen lot of investment in R&D (yearly expenses doubled) and manpower (went up by 30%). Hence profit growth were muted this year although sales grown by 18%.They have 2 API plants and 2 formulations plants USFDA approved. Next year Capex planned 200 Cr out of which 85 Cr will go for API plant and 111 Cr for Formulations plant. 10.5% of the products under price control. Company bought land in Patalganga, Aurangabad, Baddi and Goa for future expansions. Plans for more ANDA filing after acquiring CRO unit from Piramal last year. Working on front end supply chain in US.

Positives : Transparent and open management, Low Debt, conservative approach, FDA approved plants. Investing for the future.

Negative - Seems lack of focus as trying to grow exports and domestic at the same time. Hired 500 MRs last year. Too much diversified across theraupeutic categories for company of this size (1000 Cr Topline) , Low ROCE

In nutshell, very conservative and ethical pharma company. But hence bit slow growing. Can be a good long term bet if one has patience.

Disc : Invested from Nov 2015 onwards

US FDA 483 to Indoco Goa plant II. Inspection done in response their ANDA filing. Management is confident to close these observations within 3 months.

I was looking at Indoco again after a long time. The company has had a chequered record with regulatory compliance with various agencies.

As of now the revenues are in the range of 1000 crores and market cap is around 1700 crores. After posting net losses in June and Sep 2018 quarters, company posted marginal profit of 5 crores in Dec qtr. If one looks at the last 3 quarters beginning June 2018 there has been good improvement in topline q-on-q and improvement in operating profit nos.

In the concall the main explanation to poor results has been about the company being on the wrong side of regulators and hence poor utilisation levels at the export plants leading to negative effects of operating leverage.

Now with announcement as on March 2019, USFDA changed its status from official action initiated to voluntary action initiated. This is in Plant 2 at verna indl estate.

As per announcement dated 24 april 2019, Goa plant 1 got official action initiated from usfda and according to this, pending anda approvals are affected but the sales of the existing approved products continues.

And as on May 8, UKMHRA gave a clean chit to its Baddi oral dosage plant.

Results are due on 29th May 2019 and it seems nos not likely to be something to get thrilled about.

The company has been in troubles with regulators since a long time and in Dec 18 results concall management guided about resolving most of the issues within 3 months.

This is a company that promised much but delivered little due to poor compliance track record. The exciting part of the business is the ophthalmic products and injectable products. If and when they get okay with regulators these products can be exciting for the company but as of now one needs to watch how things progress in terms of regulatory approvals.

Plus with this kind of track record one needs to be very wary of further issues from regulators.

Would like to keep this company on the watchlist but I think with most pharma companies in the dumps the whole sector might take some more time to make a comeback.

Company is not proactive in collecting the Revenue as the debtor day are increasing . the inventory turnover is below the mark as compare to Venanti and Ajanta .

Not paying the tax and low operating margin will act as a high boulder in sinking boat .Suresh Khare’s multi-faceted personality does not enable him to focused in pharma but Ms Aditi’s techno-commercial skills is the one that can be bet On .

Sensodent=K company claimed this is no 1 but as per the data sensodyne ( GlaxoSmithckline ) it No 1 in Dental products

disc : not invested

73rd AGM proceedings and management reply for shareholder queries.

Indoco Remedies wins tenders worth Rs 140 crore for supply of kidney stones treatment drug in GermanyIndoco Remedies said that it has won tenders worth Rs 140 crore in Germany for supply of Allopurinol tablets, used totreat gout and kidney stones. The company said the revenue expected from this business is Rs 70 crore per annum.The supplies to Germany will begin from January 2021 and continue till end of 2022. This is Indoco’s first own labelproduct in Europe. Germany is totally tender business and Indoco has won almost 80 - 85 per cent tenders forAllopurinol. This is a tender order for supplies spread over two years.

Q3FY21 results. Good set of results

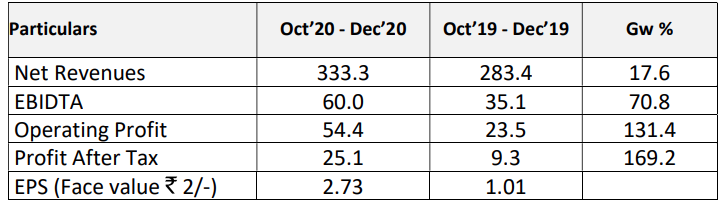

PRESS RELEASE

EBIDTA Jumps 71 %, Revenue Growth @ 18% for Indoco in Q3FY21

Mumbai, 9th February, 2021: During the third quarter of FY 2020-21, Indoco

Remedies revenue grew by 17.6 % at 333.3 crores, as against 283.4

crores, same quarter last year. EBIDTA to net sales for the quarter is 18.0 %

at 60.0 crores, compared to 12.4 % at 35.1 crores, same quarter last

year. For the quarter, the Profit After Tax to net sales is 7.5 % at 25.1

crores, compared to 3.3 % at 9.3 crores, same quarter last year.

For the 9-month period ended Dec’20, the Company’s revenue grew by

13.0 % at 922.6 crores, as against 816.2 crores for the same period last

year. EBIDTA to net sales is 18.3 % at 169.0 crores, compared to 11.0 % at

90 crores, same period last year. The Profit After Tax to net sales is 7.3 %

at 67.5 crores, compared to 2.3 % at 18.8 crores, same period last

year.

Commenting on the 3rd quarter FY21 results, Aditi Panandikar, Managing

Director, Indoco Remedies Ltd., said, “While the revenue from

International business has registered a robust growth of 73%, we are yet to

see revival in the Domestic business. Uptrend in EBIDTA has continued in

the 3rd quarter at 18% of net sales, which is highly encouraging”.

For the quarter ended Dec’20, the financials are as under: ( in Crores)

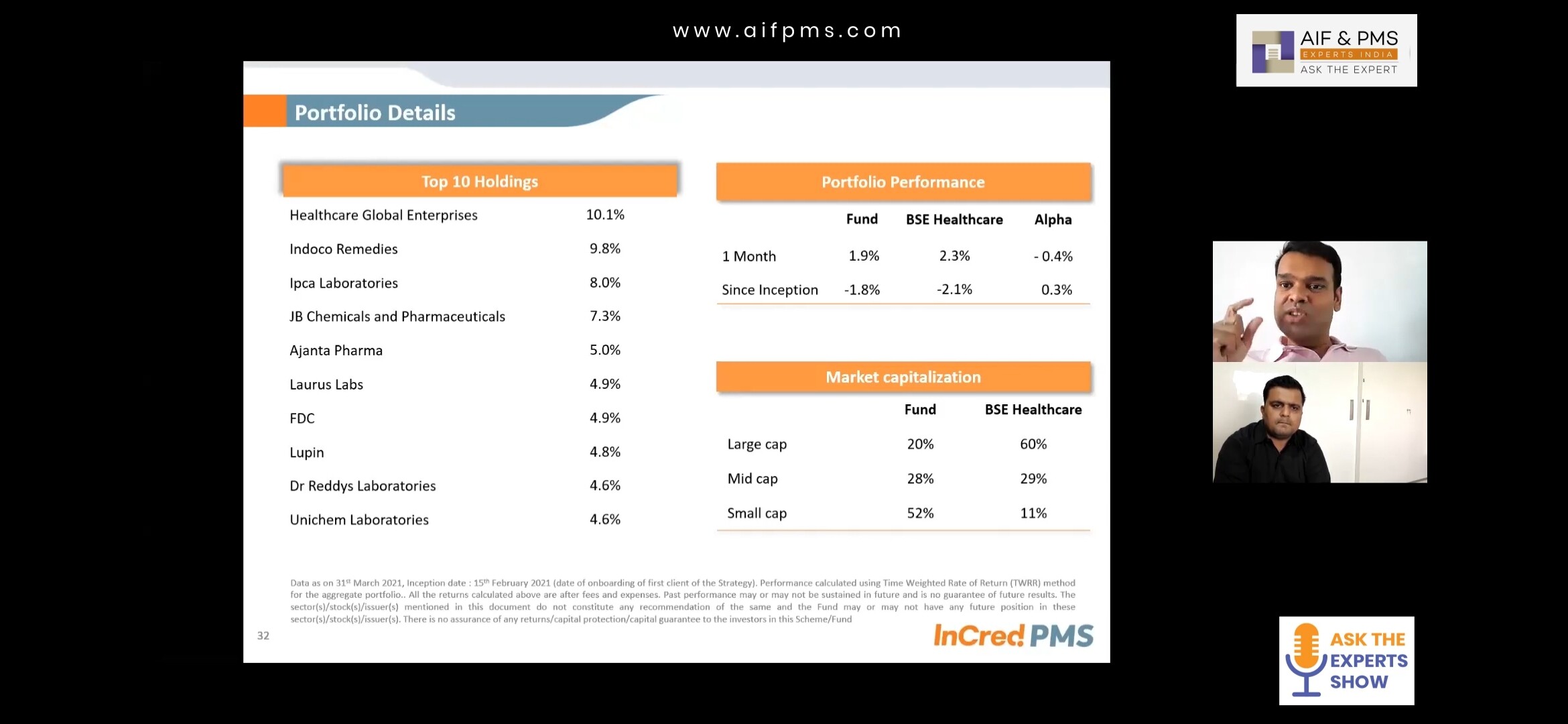

Indoco Remedies has got second highest allocation @9.8% in Healthcare focused Incred PMS Managed by Aditya Khemka (known for his performance in DSP healthcare fund). There has to be some reason for such high conviction. I am unable to find it in this thread.

Fellow members are requested to share their feedback

I am not able to find any source or Aditya interview mentioning this allocation. He recently said he has 6% allocation in Laurus but nothing about indoco

@hitesh2710 sir are you still follow this company/ wht is future perspective about comapnay

Indoco’s Revenue Growth at 12%, EBIDTA Jumps 64 % in Q4FY21.

The results were stable and concall is on May 25th

fin-press-release-4QFY21.pdf (225.4 KB)

Disclosue: Tracking Position

https://www.indoco.com/inv-fin-concall-transcripts.asp

The concall transcript of 26th May, 2021 for Q4

Conference Call Highlights

(icici sec report)

Domestic/international sales were impacted by the Paracetamol ban, supply chain issues amid Covid-19. There was an impact of 9.5 crore on export sales (postponed shipment) and of | 6 crore on domestic sales

FY20 revenue bifurcation – India: | 683 crore (vs. | 606 crore in FY19), exports: | 296 crore (vs | 233 crore)

US: | 56 crore vs. | 25 crore, Europe: | 154 crore vs. | 106 crore, SA-Australia-NZ: | 7 crore vs. | 29 crore and Emerging market: | 79 crore vs. | 73 crore

API: | 86 crore vs. | 82 crore, CRO & Analytical: | 11 crore vs. | 19 crore

India – The company launched eight products in FY20 – five in cardio, two in diabetic, one in derma

Court proceedings in the Apixaban case have been delayed due to Covid-19

US – Has got approval (from Goa) for FTF Para IV – Olapatadine HCl in the quarter, will have 180 days exclusivity when launched (no date as of yet)

12 ANDAs have been approved, seven to be filed in FY21

Currently manufacturing facilities working with 70-80% attendance, CRO working at 50% capacity utilisation

The Patalganga API facility received EU certificate of suitability (CEP); Hyderabad CRO got WHO desk approval

Paracetamol accounts for 25-30% of Europe exports

Higher Q4FY20 other expenses was due to increased domestic MR incentives and promotional spend while increase in GM was

attributable to US milestone payments and product mix

Q1FY21 travel expenses and promotional expense will be lower but partially offset by cost of digital initiatives

MR activity in India was virtually negligible for nearly the first half of Q1FY21

In Goa Plant-I, remedial procedure with US consultants is ongoing to resolve the concerns raised in the warning letter

Long term debt: | 155 crore (priority repayment), short-term debt: 105-120 crore; repaid ~ | 34 crore in FY20

Acute portfolio continued seeing demand for legacy products, sub-chronic most impacted, Chronic – repeat purchase

FY21 related management guidance-

~14% of EBITDA margins (18% in three years), 70% gross margins

API segment may achieve 20% YoY growth, Europe could achieve | 225 crore in sales while US sales is likely to grow to 150 crore (with two product launches in Q3FY21)

Capex of | 50-60 crore (mostly maintenance)

R&D spend of | 14-15 crore per quarter

YoY growth in employee expenditure to be not more than 10%

Indoco Remedies Con Call Q4FY21

Business:

• Revenues grew by 12% YOY & 12.8% for FY21 at ₹ 1,217 crores as compared to ₹ 1,079 crores last year. EBITDA to Net Sales for the quarter is 18.5% at ₹ 54.6 crores compared to 12.7% at ₹ 33.3 crores last year. For FY 21, the EBITDA Grew by 18.4% at ₹223.6 crores compared to 11.4% at ₹ 123.3 crores last year. PAT to Net Sales for the quarter is 8.4% at ₹ 24.9 crores as compared to 2.1% at ₹ 5.4 crores and for FY21, the PAT is 7.6% at ₹ 92.4 crores as compared to 2.2% at ₹ 24.2 crore

• Indian Pharma Industry is showing signs of recovery & has registered a sale of ₹ 38,253 crores with a growth of 5.3% in Q4. During the quarter, Indoco has registered a sale of ₹ 231 crores de-growing by 1.6%.

• The company is ranked 29th in the IPM with market share of 0.61%.

• Indoco reflects Prescription de-growth of 20% during Jan-Feb 2021 with Prescription share of 0.70%.

• Revenues from Domestic Formulations business de-grew by 13% YOY & for FY21, the revenues de-grew by 9.8% at ₹ 619 crores as against ₹ 686 crores last year.

• Revenues from International Business posted a robust growth of 65.7% YOY & for FY21, the revenues grew by 66.2% at ₹ 492 crores as against ₹296 crores last year.

• Revenues from regulated markets grew by 75.3% YOY & for FY21, revenues grew by 83.8% at ₹ 400 crores as against ₹ 217 crores last year. Revenues from the US business from the quarter grew by 23.5% at ₹ 33 crores as against ₹ 27 crores last year. For the year ended March 2021, the US revenues grew by ₹ 162.3% at ₹ 148 crores as against ₹ 56 crores last year.

• Brinzolamide suspension was launched in the US in March 2021 in partnership with Teva as the first generic

• Revenues for Europe for the quarter grew by 120% at ₹ 69 crores as against ₹ 31 crores for the same quarter last year & for FY21, the revenues grew by 55.5% at ₹ 239 crores as against ₹ 154 crores. Revenues from South Africa, New Zealand & Australia for the quarter are at ₹ 2.5 crore as against ₹ 1.6 crores last year & for FY21 at 12.2 crores as against ₹ 7 crores

• Revenues for the emerging markets grew by 36.4% at ₹ 27 crores as against ₹ 20 crores for the same quarter last year & for FY 21, the revenues grew by 17.5% at ₹ 92 crores as against ₹ 79 crores

• Revenues from the API business de-grew by 1.6% YOY & for FY21, revenues grew by 9.3% at ₹ 94 crores against ₹ 86 crores

• Revenues from CRO & analytical services for the quarter grew 13% at ₹ 3.8 crores against ₹ 3.4 crores & for FY21, revenues grew by 10.9% at ₹ 12 crores as against ₹ 10.9 crores last year.

• The entire de-growth is attributed to 2 categories in acute- 1) Anti-infective 2) Respiratory. For much of the year most of the acute segments were de-growing but by Q4 we made up in GI which is Cyclopam leading the way (one of the main brands. However, Febrix Plus in respiratory & Oxipod in anti-infectives are largely responsible for pulling the growth down. The categories have also heavily de-grown for the Pharmaceutical industry.

• In the Chronic segment in particular there is a marginal growth & in sub-chronic, mostly dental has done decently alright however, the base is too small so when two of the largest brands de-grow very heavily. What you saw in Q4 was largely led by an unfavourable environment in business & possibly a demoralised field force.

• For Brinzolamide, the customer (Teva) wanted a critical mass in their warehouse before they could launch the product so we have shipped about 4 months of inventory. Right now what is reported is COGS + manufacturing margin. Going forward as Teva’s sales pick up then Indoco will start receiving profit share.

• Our payables had partly suffered in previous years because of the cash flow issues that we had after the MHRA & FDA problems. Those got sorted out in the last 12 months & the cash flows have been very solid and as a result we had to make up for our payables which were lagging behind. Now all the payables are online. We had to do that because otherwise we would not have got good rates going forward for the purchases & the confidence in the market place had to be built up.

• Typically for Covid, we have a basket used for prevention, we have a basket used for treatment & we have a basket of products which are used post covid for any other infection. The key brands that we have is ATM (Azithromycin brand) and it is the 3rd highest brand growing right now in Azithromycin segment for the industry & today it is the largest brand for us as a consequence for that. Other then that we have Karvol Plus which is used as a nasal decongestant & which is moving very well. It is used for steam inhalation. We have got Rexidin mouthwash with Warren ( Dental Division) which is doing well. We also launched two ancillary products in our covid basket- 1) Coviclean (Mouth-gargle) which is gradually taking shape 2) Zimun CD (Zinc with Vitamin C & D) which is at a nacent stage in launch. Besides this we have got Favipiravir which is used for treatment.

• This year we plan to file 5-6 products in US & launch 5-6 products

• The capex for this year will be close to ₹ 80 crores & next year also should be a similar number

• Capacity utilzation for Badi 3 is at 73. Plant 1 is running at 85% & Plant 2 which is the sterile plant is running at almost 70-75% capacity

Management:

• MD: Ms.Aditi Kare Panandikar, Joint MD: Mr. Sundeep Bambolkar, CFO: Mandar Borkar

• In this year, we are expecting to generate a CFO of ₹ 300 crores

• After FY 2023, typically we do new product launch of 3-4 products per division, so we should be able to do 20 products in a year going forward.

• We should be able to work at the existing gross margins because our business mix is evolving so if you observe this year itself in International business, it has moved from the pure contract manufacturing for Europe more towards supply to US & even for domestic as the per person return increases. The product mix is also getting better.

• For the domestic business is targeting to do around ₹ 850 crores in top-line & the US business should do close to ₹ 250 crores, Europe is expected to do around ₹ 300 crores & ROW expected to do ₹ 100 - ₹ 200 crores and another ₹ 100 crores for API. (Total of around ₹ 1,650 crores)

• We will do around 19% + EBITDA margin for sure

• US business is going to be very bullish for Indoco. The order book is very very firm.

• Expect to do 20% growth in the API business

• In the semi-regulated markets, this year we have done ₹ 91 crore & next year we would definitely do around ₹ 119 crores. This will be driven by better penetration in the existing markets, new products to be introduced in the existing as well as new markets.

Risk:

•Impact on the domestic business due to covid

Indoco’s Clinical Research Organisation – AnaCipher receives

accreditation from UKMHRA

** AnaCipher CRO, based in Hyderabad, is a USFDA inspected clinical research facility and is spread over 30,000 sq. ft area with 98 beds and staffed by experienced professionals providing clinical trial solutions and conducts Bioequivalence and Bioavailability (BA/BE) studies at its facility.

** The CRO also has expertise in Bioanalytical work for new chemical entities (Phase I-III studies) for pharmaceutical companies globally. The CRO has successfully completed more than 500 studies in multiple therapeutic areas such as, cardiovascular, diabetes, oncology, anti-retrovirals and antacids.

26 Aug Concall

- 75 years of operations. Aditi is 3rd generation in biz.

- 55-60% topline from India biz. Branded generics. 99% ethically driven. 8-10% from APIs. 40% from international formulations.

- Regulated is generics: Contract manufacturer, cost + profit, own filings.

- Branded Emerging market biz in Asia and Africa.

- 6k employees. 2300 field sales officers.

- R&D center has 250 scientists. Various stages. Processes for APIs, manufacturing APIs, regulatory filing, product formulation development filing ANDAs etc.

- 3 manufacturiung in Goa all approved, 3 in badi 2 approved by regulated. 1 in aurangabad approved by emerging markets.

- 3 API sites: 1 is kilo: rabale. KSM in rabale. Patalganga has larger API site.

- Aditi MD since 2012.

- One of fastest to turn around from USFDA warning letter.

- 65 product and process patents across world.

- Goa oral solids facility (plant 1): Very key site for us. Largest site for supply to europe. Small supplies to US. Completed all commitments to FDA regarding improvements. FDA accepted that expectations side its done. But inspection has not happened yet. Several requests for e-audits. FDA Considering. Warning letter has not stopped us to supply products. 2026 beyond products are impacted. Next 3-4 years are not impacted. USFDA will start inspections in September in general.

- India biz: Last 15-18 months most unexpected work condition. 99% we depend on Prescription generation. 1st wave complete shut down. We degree 8% almost equivalent of industry. We have larger contribution by acute which got impacted very big way. Anti infectives; respiratory segments are doing well. 2nd wave was handled better by medical community. All other products are also doing very well now. Industry growth itself had slowed down in last 4-5 years.

- Sub-chronic is our strength. Mass speciality like dental, Ophthalmologist, ent, gynae, establishing ourselves in superspeciality like cardiology, diabetology.

- We have 8 marketing divisions. Cover broad category of doctors. Cipla is in respiratory, torrent and sun in CNS. We are ranked 29th in retail audit. 21st in prescription audit. Generate prescriptions equivalent to glenmark, but

- From 90% acute decade ago now it is 40% acute, 10% chronic, remaining sub-chronic. Greatest achievement has been creation of this biz.

- Confident of growth. Cyclopam, fabrix+ ar 100cr brands. We have many mid sized brands. And few of them will go to 100cr+. Good amount of brands between 20-50cr.

- We get 65% sales from west and south. Has got to do with sales capability. Lot of work has been done in last few years. Biggest change is the way we have totally ramped up and changed strategy in india biz. Created CMO position. New introductions + making them successful. One area of weakness was growing brands. Next agenda is growing the brands. Lot of hard and soft changes made inside organization.

- Profitability of international biz will continue to go up. Nature of european biz is changing. 5 yr ago we were contract manufacturers. Now we are doing AOK: File holders, our dossier in front end, our API in backend. Profitability will only go up from now.

- Can do 450-500cr ebitda by FY24.

- 2 of Teva’s launches will happen after 14 m from today. After 3-4 more months 2 more launches. Contract manufacturing for Teva (generics) right now. Talking to other cos for other contracts. 1st signing with teva was when we were very small. Now signing is on product to product basis. 1 injectable project we have signed. Confidentiality. Attractive project. Filed in June 2023. Product to product disclosures wont be done now.

- Freight rates have gone up in last 1 week. Partners understand our situation. Sharing all costs with them. All contracts are ex freight costs.

- Will put in 40cr into patalganga plant. Part of guided capex. 8-10m itll be over.

- All our 1st to files in US have come from our CRO. We may consider expansion. We manage it as a boutique sized CRO. 50-60% capacity we use internally. Ramped it up from capability perspective, but not size yet.

- Bihar, UP difficult terrain for us. In 1-2 year we will be on firm ground. Working at grassroots level.

- Our WC debt has come down significantly. 110cr now. From 130cr. Depends on biz. Long term debt we dont have any plans to increase Its around 120cr. Large part of debt retiring in Sep. 2 big foreign currency loans being repaid. (Badi 3 loan) + patalganga loan. One dollar one pound loan. 5.8% interest cost. Interest rate lower now. ICRA reinstated our rating. Best we can get for our size. If biz needs needs money, we will borrow at 4% and make 18-20% ROE. effective interest rate should be around 4-5% right now. Will stick to capex guidance already given. Patalganga we are expanding again.

- When we got into regulatory hassle, to correct w underwent major restructuring. CTO position (chief technical officer). Compliance is a new form function under her. It continuously audits all our sites and functions. More stringent than any regulator. In our remediation exercise, an overarching plan take any learning and apply it to all sites. Regulators are happier knowing you have a structure in place to catch the issues before they happen or catch it when they happen. They have a bigger concern if you dont have a system to catch the issues. Greatest learning for us. Automated software like Trackwise is installed and being installed. Makes auditing easy. We have started sorting information. Data crunching. Indication of hotspot inside site. Anticipating issues before they happen.

- Unit 2 has 3 lines and 3 kind of products: steriles, thick inspections, end sterilization, and injectables. They will come down each time a new kind of product is taken on a new line.

- One complex solid is awaiting approval of USFDA. We are churning out lot of data. Whether they will come down to inspection is up to them. One minor CRL is open.

- Ophthalmic and injectable filings in US. Some XR oral solid filings we are working on.

- We have graduated beyond simple vanilla solids. Focus on complex injectables, suspension ophthalmics, XR solids. Difficult to develop and manufacture consistently. Already have 3-4 suspensions pending approvals. Market is in Billions of $.

- MR productivity will go up in north now. Focus is doctor who is writing 3 of your products should write a fourth one. You can do this by doing brand extension, or new product. 1 MR reaches out to 180-200 doctors over a quarter. 11 calls a day. 26 working days.

Disc: have tracking position, studying.

Seems like an interesting informal discussion it’s in marathi. Since marathi is similar to hindi, I understand maybe 30-40% but still there is a congnitive overload. If someone who knows marathi could please watch it (only if you are interested in indoco) and share key takeaways or learning would be very very helpful to me as well as forum. ![]()

almost 5 years later, the observation is still not closed. Very interesting.