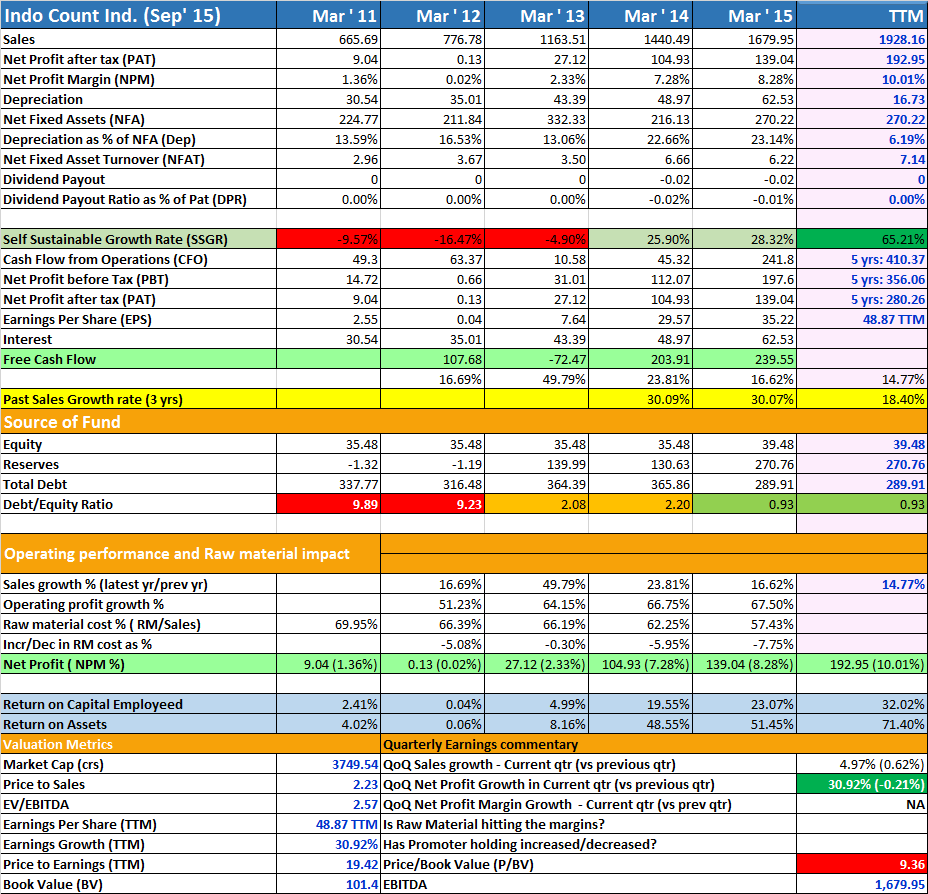

Good company with good growth rates. Good Self Sustainable Growth Rate. Debt reduced. Fantastic RoA and impressive RoCE.Valuation wise also at 2.23 levels is not horribly high. 9 times BV.

Recently bumped against Indocount and came to know about it’s growth story, after digging a little more I found the entire cotton spinning/textile industry boomed explosively in last year and half. I see nice bit of data here but I had a couple of questions which I find no one explains properly:

What changes in demand or supply or production or pricing brought in such a magical surge that it flew from Rs10 to Rs1000 in less than 2 years.

And more importantly will that kind of growth be sustainable, is there any reason to expect it to be Rs 20k or Rs30 per share in two more years. Maybe we can understand all that if we understand the reason of such an explosive growth and how much untapped growth opportunity is still open.

Disclosure: Hold small position, purchased between Rs800-900 but in a dilemma whether yo hold or exit in 2016

Its eps has grown from 7.6 to 49 in last 2 and half years,coupled with rerating stock has gone up multi folds…and also it has discounted future earnings due to its expansion…IMHO.

Thanks Akshay, exactly on those lines are my questions.

Whatever I have read is that textile is a cyclical industry where India and China swap winning position every four or five years[1][2] but when I tried to validate this theory I couldn’t find out the multi-baggers of the earlier cycle, Vardhaman textiles surged in 2005 & 2006 but Phonex mills surged in 2007 & 2008, at that time Vardhaman textiles was correcting. Secondly I found people try to relate success of Indocount, Welspun India , Lambodhara with that of Page, Kitex , KPR but we all know that Page Industry and the like started their dream journey lot earlier even when cotton spinning industry was in doldrums(i.e. 2011,2012,2013).

Sorry guys at this time I have more questions than answers.

[1]http://rakesh-jhunjhunwala.in/porinju-veliyaths-latest-stock-pick-looks-inspired-by-dolly-khanna-prof-sanjay-bakshi-kenneth-andrade-anil-kumar-goel/

[2]http://www.indiantextilejournal.com/News.aspx?nId=L6TbCr/tpyio3Omofi90Lw==

Good to see a thread on Indo Count. I think the company is uniquely placed as compared to some of the other textile players:

Asset light model; can scale up fast. High return ratios allow scaling up through internal accruals

Not highly labor intensive (like Kitex); so can scale faster

Most of the capacity is being built up in spinning; IndoCount has little exposure to spinning

Good growth expected on the revenue front - investing in building customer relationships, backend capacity addition (whatever capacity they’re adding is getting utilized in 2 years time frame).

Even if cotton prices go up - Indo Count is REASONABLY INSULATED as the hit will be taken mostly by spinners and weavers where overcapacity lies

Went through various research reports and previous available con calls. This might be one stock to watch out for in next few years. Despite strong returns in the past still trading at TTM 20 PE with good topline and bottomline growth prospects.

Disclosure: Invested ~6% of PF, looking to add more.

I would like to share a report prepared by me on Indo Count. I have read the AR of last 3 years. Had a talk with the Investor relations officer couple of times and went through the investor presentations and management interviews of last couple of years. I also had a talk with IR to arrange a meeting with the management of the company. She will come back in short time. I have even made some digging in the B2C model of the company. Mgmt is going to float a new subsidiary wherein, Indo count will hold 85% and Mr. Asim Dalal will hold 15% and will be taking care of the marketing activities. Mr. Asim dalal is a good businessmen but has been inquired by SEBI a couple of times for market manipulation and like. His father bhupendra dalal has been convicted by Supreme court in the Harshad mehta scam. Though bhupen dalal’s part was very small in the total scam. His brother was also convicted for manipulations in past. But, on business front, these brothers are just fantastic. They hold brands like Food&Inns, The bombay store (recently sold to Radhakrishna damani) and Elephant brand, etc.

My research report contains all these details. Company is in a very good position and has a lot of growth in its pipeline for next 3 years, after which, it will be B2C.

Lets, dig this company further. I am planning to meet the mgmt in couple of weeks time. This is a good story and lets try to concentrate more.

1). Are the increased OPM sustainable? What led to such a huge increase in margins?

2). Most of the home textiles companies have performed well in past? Is the growth of this company also related to the sector tailwind? Why will it not go back to normal?

As per my understanding of the company’s business model, it is based on a asset light model. Even if the cost of the raw material increases, the spinning division will have limited exposure as the entire production is used by Indo Count itself. Also there is no dearth of spinning mills in india, so sourcing of additional raw material for their value add part of business is also (kind of) unexposed.

In addition to the above, they are focusing on creating a B2C brand for themselves through company owned stores. This also provides them with the insights on further product development.

Having said the above positives, I think for any business their margins will start to stagnate at one point and probably decline after that. The question in the Indo Count is, in which stage are they. I feel that there is still some room for growth in this market, then again my views might be biased.

I hope my answer has been of some help to you.

Disc.: I am invested in Indo Count at 800 level and my views might be biased. Please do your own due diligence before investing.

I feel that Alok was always a major player in this segment and fall of Alok has a great share in growth of other companies in this sector. Further, ofcourse, Indo count is a great company with asset light model, and will continue to do even better as it goes to B2C model.

I think that the OPM of 21% is not sustainable. This might be because of mix of low commodity prices and better margin products (brands/patented products). The latter is sustainable, but the first reason can anytime reverse the growth in OPM once the commodity trend reverses. But, again as per the latest interview by KK Lalpuria, company is confident of retaining their OPM in range of 20-21%.

Sales 456.68 Cr 525.03 Cr. 14.96%

EBITDA 87.1 Cr 116.31 Cr. 33.53%

PAT 28.03 Cr 65.98 Cr. 135.39%

(ICIL paid CDR recompense amount 25 Cr in Q4 last year, that is why huge diff in PAT)

New EPS for 2016 is 63.5

Declared final dividend of Rs 1 per share.

Board has proposed the capex of Rs 300 Crs for phase 2 of upgrade and it will be met from internal accruals and debt. The recent fund raising proposal is differed.

Any idea why this stock has been falling since going past 1000 in April?

Sales have grown 17% & 15% for the Dec’15 and March’16 quarters compared to previous years respectively. And if you look at historical quarters, September quarter is their biggest by a big margin. So good days are ahead.

Read their latest AR. They are increasing their production capacity by almost 30%. Plus they are planning to replicate their USA business model in Europe and Australia. In addition they are planning to introduce their products in India, which I think in the long term will add more value. So long term it seems to have good potential.

The only small negative I noticed was their planned capex coming up in the next year to replace old machinery/equipment. But again to me, that should bring in more efficiency.

I would really appreciate if anyone can point the negatives that I am missing here?