What’s happening here, huge traction

It seems to be moving since the Annual Report came out

On quick look, one interesting thing in this year’s Annual Report is:

During the year the company has started installation of new plant of boric acid derivatives at the current location of the plant at Pithampur, The installation of the plant expected to be completed by the end of September, 2023 and the actual production expected to be start from the November, 2023.

Though this was first announced on 15th Sept 2022 (https://www.bseindia.com/xml-data/corpfiling/AttachHis/21798132-5d12-40ca-8648-6961366c3e91.pdf)

Them finally putting in money towards the expansion of their core business and possibly some new products is definitely a positive; though no info yet on exactly which products and no indication of the size of capex. We do know that it’ll entirely be funded by internal accruals and the cash on books of 80cr is actually a good number, absolutely no idea on how big the capex would be but even 20cr towards expansion into derivate products might be great and maybe that is what’s making the stock move? (P.S. Just thinking out loud based on the data available, they haven’t given out any more info publically yet)

No signs of that expansion being into Lithium Hydroxide though, because this is clear that it’s just boric acid derivatives.

5 Likes

Its of Rs 10 to Rs 15 cr only

1 Like

They do not have any plan to start this product again.

1 Like

Where did you get this info?

I called the company. Got the number from annual report.

1 Like

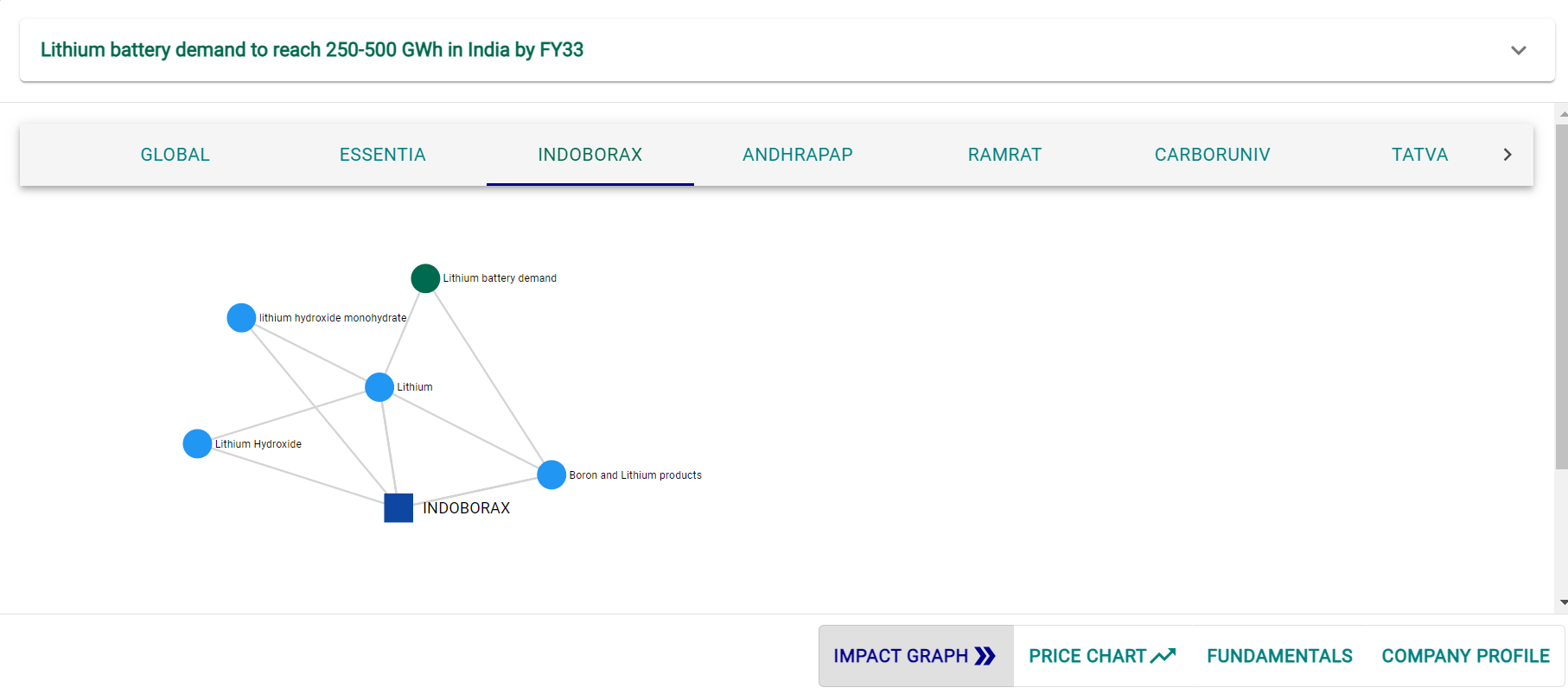

Lithium Battery Demand Surge in India Expected to Bolster Indo Borax and Chemicals Stock

India is poised for a monumental surge in lithium battery demand, and Indo Borax & Chemicals Limited (NSE:INDOBORAX), a manufacturer and seller of boron and lithium products, stands to benefit significantly. With projections indicating that the demand for lithium batteries could reach between 250 to 500 GWh by fiscal year 2033, the company’s prospects are looking brighter than ever.

The recent report, titled ‘EV Batteries: Battle to control EV supply chain’ by Axis Capital, has highlighted that achieving a 250 GWh battery demand would necessitate incentives of INR 1.8 trillion over the period of fiscal years 2024 to 2028, along with an initial capital expenditure (capex) of USD 30-33 billion. This forecast is in line with India’s ambitious goals to electrify its transportation sector and reduce its carbon footprint.

So, how exactly is this bullish forecast going to positively impact Indo Borax & Chemicals Ltd’s stock price?

Increased Demand for Lithium Products : Indo Borax & Chemicals Ltd manufactures and sells lithium hydroxide monohydrate products. With the rapidly growing demand for lithium batteries in India’s electric vehicle (EV) market, the company’s lithium products are likely to be in high demand. This uptick in demand can potentially lead to increased revenues and higher profits.

Positioned for Growth : Indo Borax is already established in the Indian market and has been providing quality lithium products for years. This positions them well to capture a substantial share of the growing market, given their experience and track record.

Market Confidence : A booming industry and an established player like Indo Borax can instill confidence in investors. As they see the company benefiting from India’s electric vehicle revolution, it can attract more investment and drive up the stock price.

Favorable Regulatory Environment : As the Indian government provides incentives and support to the EV industry, it indirectly benefits companies like Indo Borax. The conducive regulatory environment can create a positive atmosphere for the company to thrive.

Strong Financial Performance:

In addition to these promising forecasts, Indo Borax boasts impressive financial credentials that make it a compelling investment opportunity.

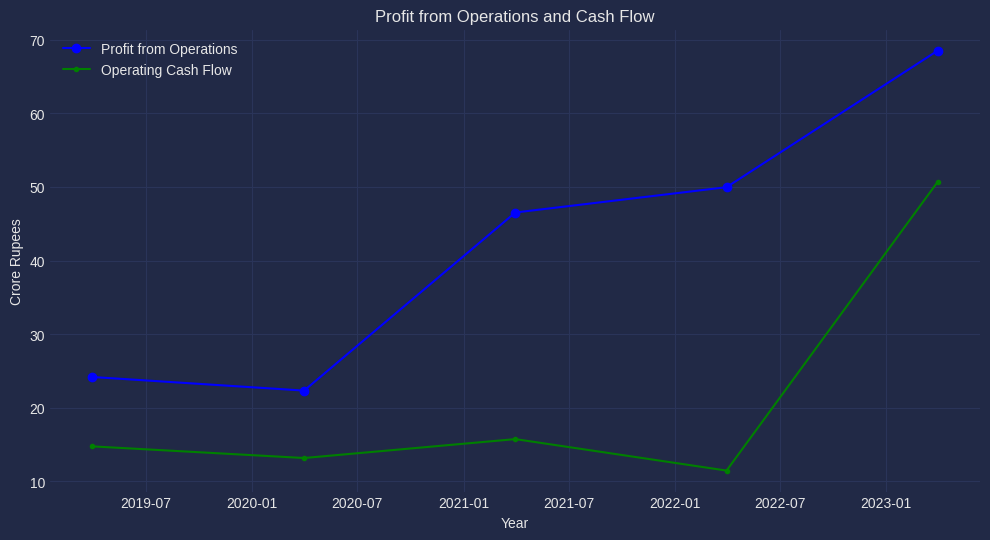

The above figure shows operating profit growth for the last 5 years.

Robust Profit Growth : Over the past five years, Indo Borax has demonstrated remarkable profit growth, with a staggering 243% increase. This equates to a compounded annual growth rate (CAGR) of 28%. Such consistent profit growth signifies a company that is efficiently utilizing its resources and generating value for its shareholders.

Strong Cash Flow Position : The company maintains a healthy cash flow position with a consistent 183% growth over the last five years and a CAGR of 23%. This strong cash flow not only ensures operational stability but also provides flexibility for investments in research, development, and expansion.

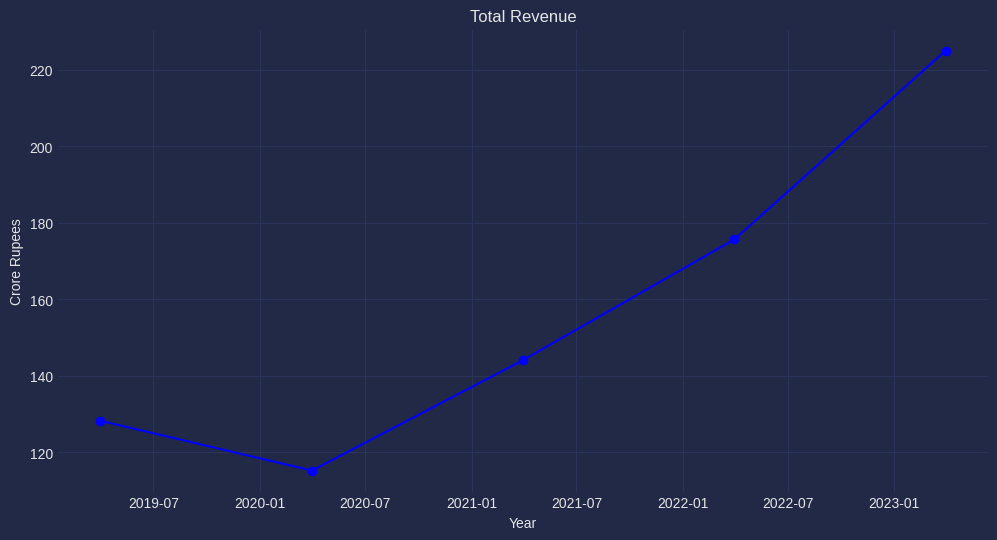

The above figure shows the revenue for the last 5 years.

Impressive Revenue Growth : Indo Borax’s revenue has surged by 75% over the past five years, demonstrating a CAGR of 11.89%. This growth highlights the company’s ability to capture market opportunities and meet the rising demand for its products effectively.

Attractive Valuation Metrics : The company’s PEG (Price/Earnings to Growth) ratio stands at 0.5, well below the typical threshold of 1. A PEG ratio below 1 suggests that the stock may be undervalued relative to its growth prospects.

Favorable Valuation Ratios : Indo Borax boasts a Price/Book (P/B) ratio of 2, which is below the industry median. Additionally, the Price/Earnings (P/E) ratio is a modest 10.7, also below the industry median. These metrics indicate that the stock may be attractively priced compared to its peers.

Debt-Free Status : The company’s debt-free status is a significant advantage in a potentially high-growth industry. It means that Indo Borax does not have substantial interest payments or debt-related risks that could hinder its growth or financial stability.

Conclusions

In conclusion, the surging lithium battery demand in India is expected to have a positive impact on Indo Borax & Chemicals Ltd. In light of Indo Borax & Chemicals Ltd’s robust financial performance and the burgeoning demand for lithium batteries in India’s electric vehicle market, the company is well-positioned to thrive. These factors, combined with a favorable regulatory environment and established market presence, bode well for the company’s future. The company is well-positioned to capitalize on this trend, potentially leading to increased revenue and growth opportunities.

Reference: Lithium battery demand to reach 250-500 GWh in India by FY33

Disclaimer: The article is not a recommendation or advice as to whether any investment is suitable for a particular investor.

3 Likes

Your comment on this?

1 Like

If there are Chemical Engineers or industry insiders available in this forum, their inputs will be really helpful.

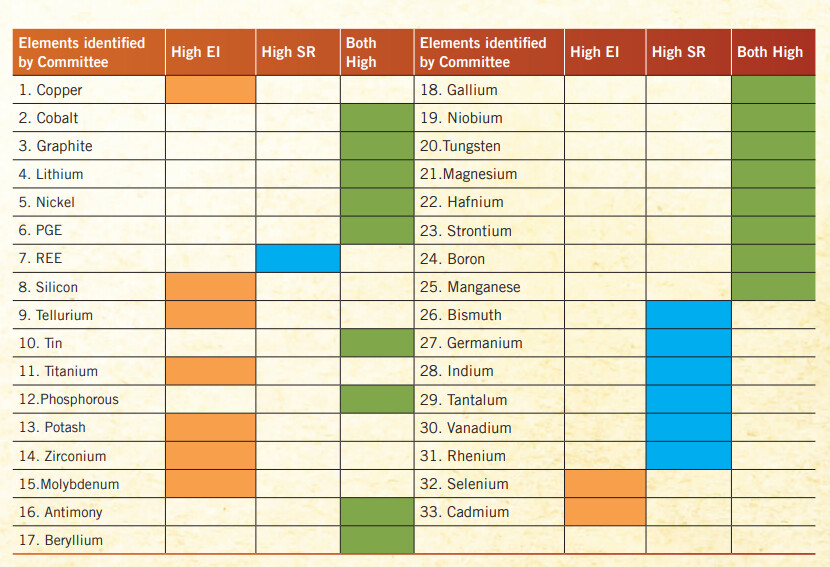

I was trying to understand why there is a high import restriction on Boron and related raw materials in India, but couldn’t find any valid reason (I did find many articles on GOI backing up their stance on the restriction, but not a proper reasoning behind it).

In fact, in the report ‘Critical Minerals for India’ published by the Ministry of Mines in June 2023 (https://mines.gov.in/admin/storage/app/uploads/649d4212cceb01688027666.pdf), they highlight Boron as a raw material with ‘High Economic Importance as well as High Supply Risk’. This further feeds the confusion around the high import restrictions on the same.

Indo Borax’s competitiveness is clearly visible in their high Margins, ROIC and the little to no Capex requirement to grow at high double digits. Understanding the reasoning behind GOI’s adamant stance on import of Boron could contribute to unravelling Indo Borax’s Competitive Advantage and more importantly, whether it’s Sustainable or Unsustainable.

6 Likes

The company is faring well. But every quarter promoters are selling. The number of shareholders have gone up from 23k to 27k.

I had exited and have no position.

I am looking for opportunity to re-enter but continuous promoter selling (distribution) is a concern. Also, no Institutional buying.

What I was able to find so far:

-

I couldn’t find a direct quote or reference. But it seems like Boron is highly dangerous even in small quantities and it’s also used in nuclear reactors. That sort of makes sense as to why there are high import restrictions for Boron.

-

There are only 4 large firms with the IS 10116 certification (Requirement to produce Boric Acid in India) - see below. While Avantor seems to be a really big firm, the rest of them are at the same size of Indo Borax more or less. So my assumption is that this is the reason behind Indo Borax’s above average and sustaining Operating Margins and thereby RoCE.

-

Of course, as per their AR, they’re the only manufacturers of IP Grade Boric Acid in India. Based on my cursory Google search, I was not able to confirm this. But taking them on their word, and the fact that the major raw material has severe import restrictions, these couple of points could be the source of their Sustainable Competitive Advantage.

Interesting company, to say the least. I just wish the Annual Report offered more information. It’s quite shallow in terms of giving out details on the industry structure and a view of the competition. Even the future guidance is limited to ‘Company will grow well, its product are of high quality’.

References

List of India firms with IS 10116 BIS Certification (Might be dated): https://www.services.bis.gov.in/php/BIS_2.0/bisconnect/knowyourstandards/Indian_standards/downloadLicenses/ODc0

IS 10116 1982 Document: https://law.resource.org/pub/in/bis/S02/is.10116.1982.pdf

IS 10116 2015 Document (Needs login to download): Bureau of Indian Standards - e-Sale Search Result

9 Likes

Someone monitoring ? In latest result cash equivalent Rs 120 cr against Mcap of 531 cr at price of Rs 166 and property investment of Rs 77.62 CR which is now giving rental income and zero debt . Last year EPS is 12.15 and P/E is 13.6 . As chemical sector is bottoming out argus well for this cash rich company.

Further inventory is reduced to Rs 22 CR from 58 CR last year.

Am I missing something ?

Also last year cash flow Rs 68 CR against Rs 60 CR last year

All data is as per screener

Hi All,

Company Name: Indo Borax & Chemicals Ltd

In AR 2025, cash flow from operating is negative -72cr. When I go through balance sheet of company, there is increment of 80.88cr in “Other financial Assets”. Checking notes, company kept FD with corporates, no information about which corporates? Any thoughts on this?

INDO BORAX AND CHEMICAL

Indo Borax’s acquisition represents a control transfer from a niche promoter-led setup to a PE-backed strategic platform, aiming to scale boron chemicals from commodity supply to higher-value specialty applications.

Indo Borax & Chemicals Ltd (IBCL) is an Indian manufacturer of boron-based industrial chemicals.

The company operates in a niche segment with limited domestic competition.

Its business was largely promoter-driven, focused on stable operations rather than aggressive expansion.

Growth and margins were constrained by raw material import dependence and limited downstream integration.

Key Products

| Product | Description |

|---|---|

| Borax Pentahydrate | Industrial boron compound |

| Borax Decahydrate | Detergents, glass applications |

| Boric Acid | Glass, ceramics, pharma, agriculture |

| Other Boron Compounds | Specialty industrial uses |

| Industry | Use of Boron Chemicals |

|---|---|

| Glass & Fiberglass | Strength, heat resistance |

| Ceramics & Enamels | Durability, finish |

| Detergents | Cleaning efficiency |

| Agriculture | Micronutrient (boron) |

| Metallurgy & Flame Retardants | Industrial processing |

The promoters of Indo Borax & Chemicals Ltd agreed to sell their controlling stake, resulting in a change of control.

The acquisition was announced on 15 December 2025.

Acquiring Entities

| Entity | Role |

|---|---|

| Zenrock Chemicals Pvt Ltd | Lead strategic acquirer |

| India Special Assets Fund III | Financial investor |

| ISAF III Onshore Fund | Financial investor |

| Special Situation India Fund | Financial investor |

Stake & Shareholding Detail

| Particulars | Details |

|---|---|

| Shares acquired from promoters | 1,63,00,230 |

| Percentage acquired | ~50.80% |

| Nature of transaction | Change in control |

| Item | Value |

| Price per share | ₹256.30 |

| Shares acquired | 1,63,00,230 |

| Approx. consideration | ~₹418 crore |

Mandatory Open Offer

| Item | Value |

|---|---|

| Open offer size | 83,43,400 shares |

| Percentage | 26% |

| Open offer price | ₹256.30 |

| Open offer value | ~₹214 crore |

Boron chemicals are essential industrial inputs and are required continuously across glass, ceramics, detergents, agriculture, and metallurgy. Demand for these products is largely non-discretionary, making the business relatively stable.

India has very few domestic manufacturers of boron chemicals. Because of this limited local capacity, any established producer becomes strategically valuable for buyers looking to enter or expand in this niche segment.

The acquisition gives the acquirers a ready manufacturing base in specialty chemicals. Instead of starting from scratch, they gain an operating plant, existing customers, and market credibility.

Control over production allows better pricing power and supply reliability. This is especially important in boron chemicals, where raw material availability and imports influence margins.

From a financial perspective, private equity partners see scope to improve margins through better scale, cost control, and efficiency. The company also offers opportunities for balance-sheet optimisation and disciplined capital allocation.

Zenrock Chemicals Pvt Ltd

Zenrock Chemicals Pvt Ltd is incorporated on 8th April 2025 Indian private company that became publicly visible after leading the acquisition of a controlling stake in Indo Borax & Chemicals Ltd. The company is promoted and directed by Sunil Malhotra and Radhika Sunil Malhotra, both of whom have long experience in corporate governance rather than a single-sector operating background. Sunil Malhotra has over two decades of board-level experience across multiple private companies in industrial, hospitality, trading, machinery, steel, and advisory businesses, including a stint as an independent director at a listed electrical company, indicating familiarity with compliance, strategy, and oversight. Radhika Sunil Malhotra has close to two decades of experience as a director and designated partner in several private limited companies and LLPs, mainly in hospitality, industrial, and advisory ventures, reflecting strengths in governance and business administration. Together, they appear to function as professional promoters and governance leaders, using Zenrock Chemicals as a strategic acquisition vehicle—backed by private equity funds—to take control of Indo Borax and drive its future scaling, professionalisation, and value creation rather than as operators of a long-standing standalone chemical manufacturing business.

India Special Assets Fund

India Special Assets Fund III (ISAF III) is a private equity / special situations fund managed by Edelweiss Alternative Asset Advisors and backed by institutional investors such as global pension funds, insurance companies, family offices, and HNIs who commit capital to Edelweiss-managed funds. The fund does not disclose its investors individually or its exact performance publicly, which is normal for private equity. While ISAF III’s own realised returns are not publicly available, earlier special-situations funds run by the same Edelweiss platform have shown strong value creation, and funds in this strategy typically target high-teens to low-twenties IRRs (around 20%+ IRR) over a multi-year period, though these are targets rather than guaranteed or reported returns.

ISAF III Onshore Fund

ISAF III Onshore Fund is an Edelweiss Alternative Asset Advisors–managed AIF that follows a special situations and structured investment strategy. Like most private equity and AIF vehicles, it does not publicly disclose its past return numbers, such as IRR or CAGR, and performance data is shared only with its investors. Public information only indicates that earlier Edelweiss special situations funds have delivered strong value creation through successful exits, but there is no specific, publicly available return history for ISAF III Onshore Fund itself.

Special Situation India Fund

Special Situation India Fund is a Category I AIF focused on special situations such as distressed assets, turnaround opportunities, and stressed companies where traditional capital is scarce. Like most AIFs, it does not publicly disclose its actual past return figures, and performance is shared only with investors. Industry information suggests that funds following this strategy typically target high returns (around 23–25% gross IRR), but there is no officially published return data for this specific fund.

Profit and Loss Statement

| Income Statement | FY21 | FY22 | FY23 | FY24 | FY25 |

|---|---|---|---|---|---|

| Revenue | 144 | 176 | 225 | 191 | 175 |

| Cost of Goods Sold (COGS) | 62 | 77 | 108 | 102 | 82 |

| Gross Profit | 82 | 99 | 117 | 89 | 93 |

| Expenses | |||||

| Employee Benefit Expenses | 10 | 12 | 14 | 12 | 14 |

| Other Manufacturing Cost | 9 | 11 | 13 | 10 | 0 |

| Power, fuel and water | 6 | 9 | 10 | 9 | 0 |

| Selling and Distribution | 13 | 18 | 17 | 14 | 0 |

| Other Expenses | 1 | 1 | 1 | 1 | 33 |

| Short/Long term Provision | |||||

| EBITDA | 44 | 48 | 62 | 43 | 46 |

| EBITDA Margin | 31% | 27% | 28% | 22% | 26% |

| Depreciation & Amortization | 1 | 1 | 2 | 2 | 3 |

| Depreciation on Tangible Asset | |||||

| EBIT | 43 | 47 | 60 | 41 | 43 |

| Less: Interest (Long Term + Lease) | 0 | 0 | 0 | 0 | 0 |

| Add: Other Income | 4 | 3 | 9 | 12 | 16 |

| Profit Before Taxes and JV | 47 | 50 | 69 | 52 | 59 |

| Exceptional | |||||

| JV | |||||

| EBT | 47 | 50 | 69 | 52 | 59 |

| Taxes | 12 | 14 | 18 | 13 | 16 |

| PAT | 34 | 36 | 51 | 39 | 43 |

Sales turnover for the year is Rs. 19,130.30 lacs as compared to Rs. 21,496.93 lacs in the previous year. Profit before tax and depreciation is Rs. 5,376.12 Lacs as compared to Rs. 7,010.16 Lacs in the previous year. During the year there is decrease in sales and profit due to lower realization on boric acid in the financial year 2023-24

The Middle East crisis has disrupted logistics and shipping, making it harder and more expensive to import boron raw materials.

This affects production costs and supply planning for Indo Borax because it relies entirely on imported raw materials.

FY24 ( AGM)

| Particulars | Quantity (MT) | |

|---|---|---|

| Installed Boric Acid Capacity | 20,000 | |

| Boric Acid Production | 18,829.96 | |

| Boric Acid Sales | 18,902.06 | |

| Product | Quantity (MT) | Sales Value |

| BA IP Powder (PR) | 721.672 | 8.364 |

| BA IP Granular (GR) | 148.015 | 1.8176 |

| BA Technical Powder (PR) | 17,308.88 | 172.33 |

| BA Technical Granular | 723.5 | 7.1826 |

Indo Borax has an installed DOT manufacturing capacity of 6,000 MT per year, indicating significant headroom for growth, as current production and sales are still very small compared to capacity. This suggests that DOT is a future growth product, where demand can be scaled without major additional capex

Balance Sheet

| Balance Sheet | FY21 | FY22 | FY23 | FY24 | FY25 |

|---|---|---|---|---|---|

| Liabilities | |||||

| Borrowing | 0 | 0 | 0 | 0 | 0 |

| Trade Payable | 5 | 5 | 3 | 4 | 5 |

| Other Liability | 12 | 10 | 17 | 14 | 16 |

| Liabilities | 17 | 15 | 20 | 18 | 21 |

| Shareholders’ Equity | |||||

| Share Capital | 3 | 3 | 3 | 3 | 3 |

| Reserves and Surplus | 170 | 204 | 252 | 290 | 332 |

| Total Shareholders’ Equity | 173 | 207 | 255 | 293 | 335 |

| Total Liabilities and Shareholders’ Equity | 190 | 222 | 275 | 311 | 357 |

| Assets | |||||

| PPE | 89 | 91 | 96 | 99 | 101 |

| CWIP | 1 | 1 | 1 | 1 | 1 |

| Investments | 30 | 4 | 9 | 43 | 57 |

| Inventory | 30 | 65 | 58 | 22 | 47 |

| Trade Receivable | 9 | 10 | 13 | 14 | 16 |

| Cash and Cash Equivalents | 3 | 36 | 86 | 120 | 40 |

| Other Assets | 28 | 15 | 12 | 12 | 95 |

| Total Assets | 190 | 222 | 275 | 311 | 357 |

Ratio Analysis

| Ratio | FY21 | FY22 | FY23 | FY24 | FY25 |

|---|---|---|---|---|---|

| Revenue | 144 | 176 | 225 | 191 | 175 |

| Revenue Growth | 22% | 28% | -15% | -8% | |

| Gross Profit Margin | 57% | 56% | 52% | 46% | 53% |

| EBITDA Margin | 31% | 27% | 28% | 22% | 26% |

| EBIT Margin | 30% | 27% | 27% | 21% | 25% |

| PBT Margin | 32% | 28% | 31% | 27% | 33% |

| PAT Margin | 24% | 21% | 23% | 20% | 24% |

| FA Turnover | 1.60 | 1.91 | 2.31 | 1.92 | 1.72 |

| WC Turnover | 4 | 3 | 3 | 6 | 3 |

| Trade Receivables Days | 22 | 21 | 21 | 26 | 33 |

| Inventory Days | 75 | 135 | 94 | 43 | 98 |

| Trade Payables Days | 13 | 10 | 6 | 7 | 11 |

| WC Days | 84 | 146 | 109 | 62 | 120 |

| Total Asset Turnover | 1 | 1 | 1 | 1 | 0 |

| D/E | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Financial Leverage | 1 | 1 | 1 | 1 | 1 |

| Interest Coverage | 478 | 781 | 465 | 1350 | 240 |

| ROE | 20% | 18% | 20% | 13% | 13% |

| NOPAT | 54 | 60 | 76 | 51 | 55 |

| NOPAT Growth | 10% | 28% | -34% | 9% | |

| NOPAT Margin | 38% | 34% | 34% | 27% | 31% |

| ROCE | 31% | 29% | 30% | 17% | 16% |

| ROIC | 44% | 37% | 46% | 38% | 35% |

| Reinvestment Rate | 26% | 61% | -87% | 25% | |

| Cash Conversion(5 Year) | 0.34 | ||||

| FCFE | -38 | 37 | 53 | 38 | -79 |

Business Model and Value Chain

Indo Borax & Chemicals Limited operates primarily as a manufacturer and seller of boron products and lithium. The company earns its revenue through the sale of manufactured chemicals and, to a lesser extent, traded goods like sulphuric acid. In the industry value chain, the company acts as a downstream processor; it is dependent on importing basic boron ores because these are not naturally found in India. In case of boric acid, this company’s share is more than 50% of total domestic market

The company serves a large number of customers across various parts of India. Its contract structure is characterized by an absence of long-term contracts, and it does not utilize derivative contracts. Most sales are domestic, as the company reported zero foreign exchange inflows for the 2024-25 financial year.

The boron product industry in India is characterized by a structural reliance on imports for raw materials. There is limited reliable published data specifically for this sector in India. However, the domestic market for these chemicals is expanding annually.

The industry growth outlook is supported by two key drivers:

• Agricultural Demand: The Indian government is actively encouraging the use of Boron in agriculture to enhance crop yields, as Indian soil is largely boron-deficient.

• Industrial Expansion: Increasing use of boron products in fused products like glass, ceramics, and enamels, as well as in metallurgical operations and nuclear applications.

Product Portfolio and Operating Segments

The company operates in a single reportable segment: the manufacturing and selling of chemicals.

• Portfolio: Includes Boric Acid (Technical Grade and IP Grade), Di-Sodium Octaborate Tetrahydrate (DOT), Boron Oxide, and Lithium Hydroxide Monohydrate.

Competitive Advantages:

• Market Leadership: Indo Borax is the market leader for Boric Acid in India.

• Sole Manufacturer Status: It is the only manufacturer of IP grade Boric Acid in the country and holds a valid FDA licens

Globally, demand for lithium hydroxide monohydrate is rising rapidly due to the shift toward high-nickel battery chemistries and accelerating EV adoption. However, production of battery-grade lithium hydroxide requires tight quality control and is capital intensive, making supply concentrated in a few regions, especially China. India currently has limited domestic capacity and remains dependent on imported lithium raw materials.

In India, companies such as Tata Chemicals, Neogen Chemicals, and Indo Borax & Chemicals have entered or are entering the lithium chemicals space. Indo Borax operates at the upstream chemical stage, supplying lithium hydroxide monohydrate to cathode manufacturers rather than making batteries itself. This positions the company as an early-stage participant in the EV value chain, benefiting from EV growth while avoiding the capital-heavy risks of cell or battery manufacturing.

Indo Borax’s key advantage lies in its ability to manufacture IP-grade, FDA-approved boric acid, which allows it to serve highly regulated customers such as pharmaceutical, healthcare, and personal care companies.

“We are concentrating on our core business i.e. Boric Acid and now on DOT. With regards to lithium hydroxide we had already informed that due to the high cost of raw material, wildly fluctuating market prices and very thin margin we are now concentrating on our core product i.e. Boric Acid and now DOT.”

In India, Gujarat Boron Derivatives Pvt Ltd, Singhania International Ltd, and a few smaller boric acid producers compete with Indo Borax mainly in technical-grade boric acid and borax, where pricing is more competitive and entry barriers are lower. However, Indo Borax faces very limited domestic competition in IP-grade, FDA-approved boric acid, which gives it a strong edge over Indian peers.

2 Likes

I have tried to find out why Edelweiss has bought stake in Indo Borax, but I am not able to understand why they have bought , because business economic is been worse since last 2-3 year but since last 3 Quarter there is been moderate growth. If anyone have some different information please share