Indo Amines is a specialty chemicals manufacturing company. It has been around for a long time (IPO in 1994. Indo Amines Ltd - One of the largest Manufacturing company in South Asia)

From the annual report -

“Your Company is a leading manufacturer of Specialty Chemicals with diversified end-uses into Agrochemicals, Pharmaceuticals, High Performance Polymers, Paints, Pigments, Printing Inks, Rubber Chemicals, Additives, Surfactants, Dyes, Flavors & Fragrances, Home & Personal Care applications, etc. Your Company makes continuous efforts to explore and innovate new products & processes in all

segments. This diversified end-user base helps the Company to reduce its risk from downturn in any individual business segment andalso to capitalize on the growth opportunities in each of the end-user segments”

It has 6 manufacturing sites in India with 4 under construction (https://indoaminesltd.com/). Their website claims to be one of the largest manufacturing companies in South Asia.

They seem to have 3 product lines of chemicals - fine, specialty and performance (Indo Amines Ltd - Manufacturer - Fine, Specialty & Performance Chemicals). I couldn’t understand the technicals but broadly it is manufacturing chemicals which has end use in a significant number industries.

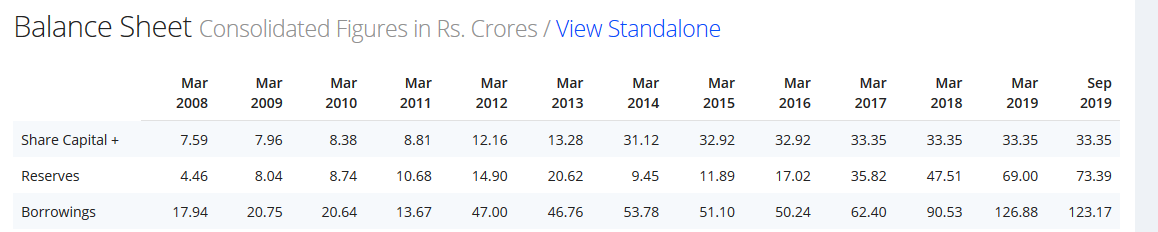

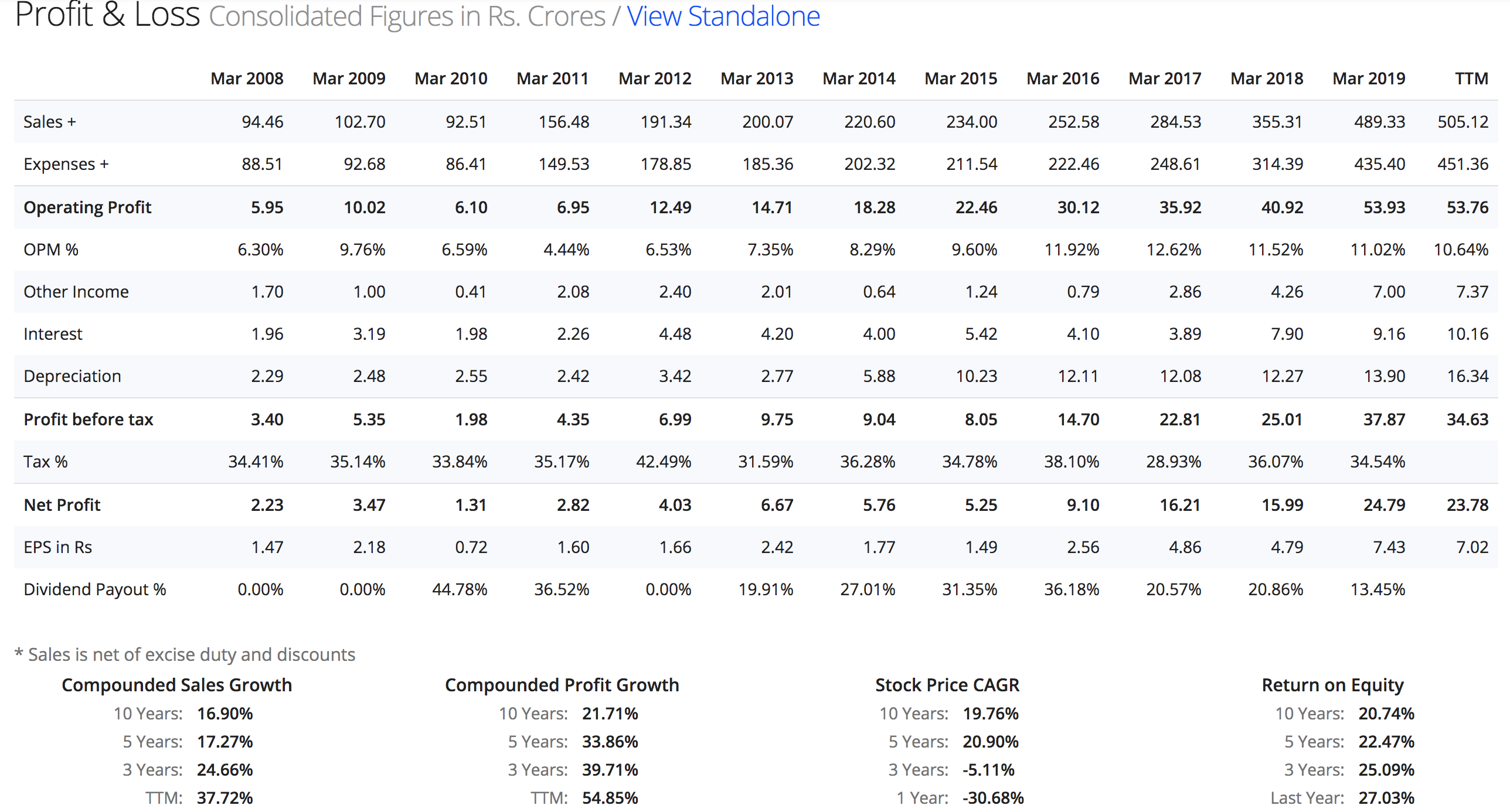

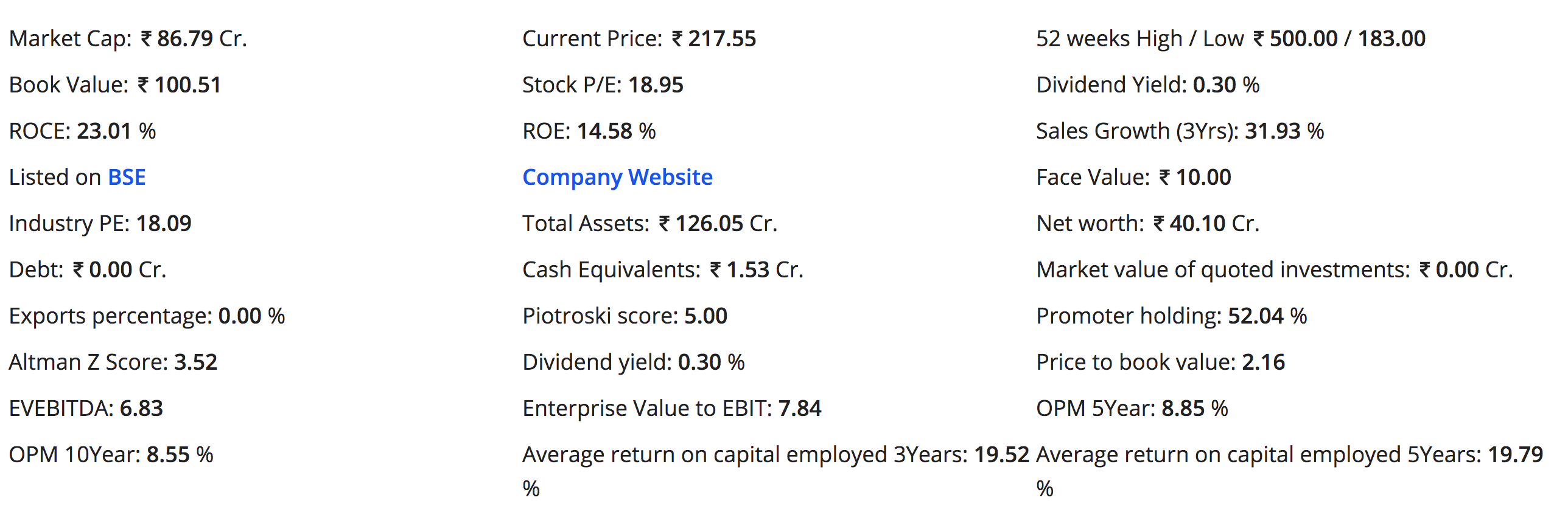

Financials from screener.in:

Pros:

- Good dividend payout in the last 10 years (~15-20% of profit can be expected as dividend going by history)

- Greater than 15% profit and sales growth in the last 3, 5 and 10 year periods

- Reasonable low valuation of PE - 7.85, Enterprise Value to EBIT: 6.71

- Good ROE and ROCE of > 20% consistently

- Promoter holding is high at 73% (Would love to hear more about promoters as I couldn’t find much…)

Cons -

- It is a very small market cap company - 187 Cr mCAP

- Debt seems to have increased - 123 Cr currently (Would have been great if it had grown without taking on so much debt)

- Annual report is not great to understand the business properly

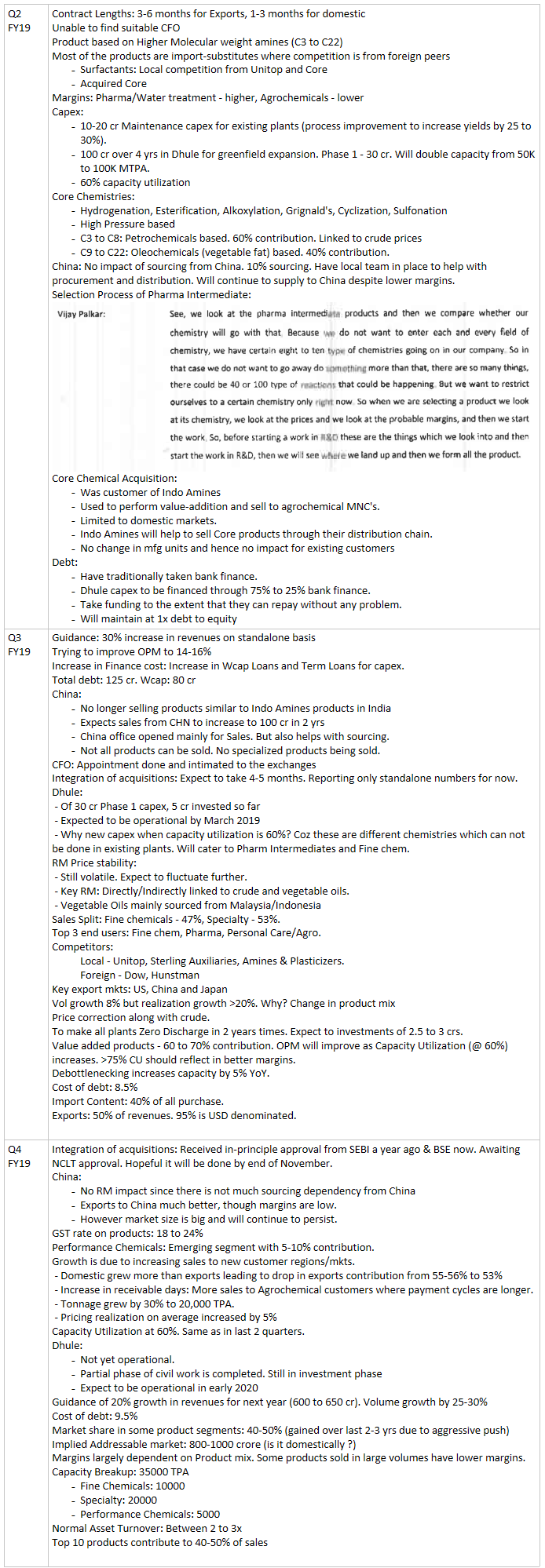

- Don’t know the global threats to this business as I guess, its customers could buy from China etc… Don’t understand competition also

- Employee review of the company is not great (Indo Amines Reviews by 113 Employees | AmbitionBox, Working at INDO AMINES LTD: 6 INDO AMINES LTD Reviews | Indeed.com)

- The promoter family (Palkars) are getting > 1 Cr salary while other key personnel are not getting good salaries

Why I am thinking of investing?

Growth seems good… for this type of growth, PE seems very less and the stock should appreciate significantly if the last 10 year trend continues for the next 2-3 years in my opinion

Please share your views.

(Note: The stock price went up significantly last week unfortunately when this post was removed by moderators. Please check the valuation numbers again whenever you read this. I have not yet invested)