These ^^ are my feelings since having invested in Indigrid. I just don’t understand why the price keeps falling even with a good pipeline of ROFO assets, SEBI proposing to increase leverage limits, stability of underlying assets etc. Is there something that we don’t know?

Is debt the only way an InvIT can add more asset to it’s portfolio?

Approximately yes since 90% of cash flows need to be mandatorily distributed as per Sebi norms. Idea is that they could raise debt very attractive rates due to their AAA rating and buy infra assets from other owners at attractive IRR rates of ~10-12% making cool spread of 3-4% enhancing IRR for the unit holders.

2 Likes

This indirectly implies RBI is not onboard with InvIT structure. This does not make any sense, we need to look at the source, sometimes news article does not interpret circulars/notices correctly.

Broadly, InvIT cannot fail. India need massive investment in infra power lines, roads, warehouses, optical fibres.

Edit - 1

-

Initial regulation envisaged subsequent funding for reit/invit by follow-on offer, right-issue or qip. (Why it was envisaged like this initially?)

-

But regulation mentioned in point 1 was given away by Sebi notification dated 15-Dec-2017. SEBI circular dated - 13-Apr-2018 regarding Guideline for issuance of debt. (Why this condition was given away? What are the risks associated with issuance of debt by reit/invit?

Edit - 2

What are the risks associated with issuance of debt by reit/invit?

Basic assumption associated with the design of reit/invit is providing minimum risk return to investors.

In case of bankruptcy of invit/reit, who will have first right on assets of trusts? Unit-holders or banks. I think raising debts by invit/reit defeats the basic purpose of their design. If such was the case all these assets could be assimilated in a holding company and that could have been listed.

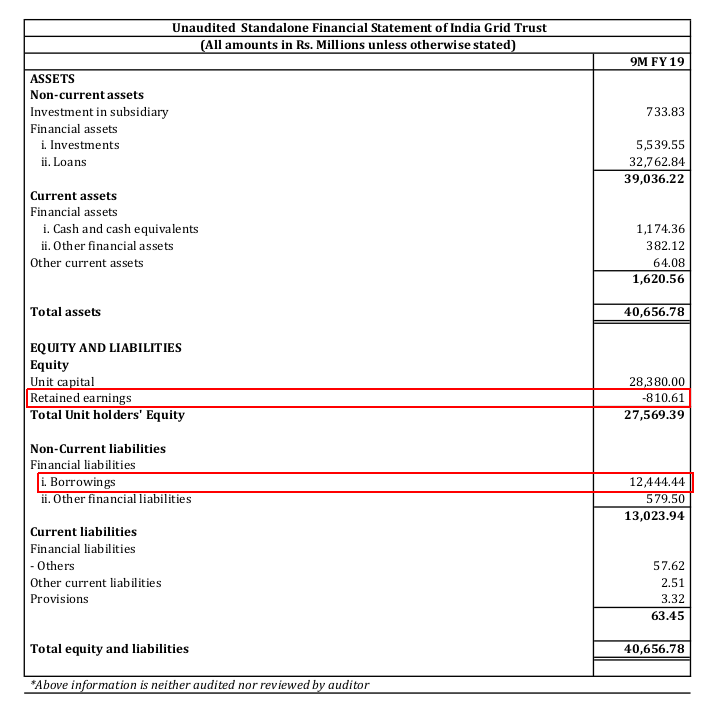

Indigrid has borrowing of 1244cr at standalone level and negative retained earning of 88cr.

Edit - 3

What is the difference between invit/reit and a company (holding company)?

The main difference between a holding company and Invit is how they are regulated?

Company is governed/regulated by Companies act and regulator is Ministry of Corporate Affairs whereas Invits are trust set-up under Indian trust act and regulated by SEBI.

1 Like

What about the other InvIT - IRBInvit? I have IRBInvit at 73. It’s currently at 67. They have been regularly paying out every few months.

There is a separate topic for IRBInvIT. Please ask on that topic.

same here, dont know why price keeps falling, yield at CMP of ~82 even more attractive!

Main difference is : they have to share free cash flows with unit holders (min 90 %) i believe. This makes it like actually owning the revenue generating asset. In holding company investors get only dividends declared (ie post tax post depreciation). Here you are getting more but giving up growth (in terms of vertical integration, new business etc). Max they can buy more assets with associated debt.

First right to assets would be bond holders and lending banks, unit holder is secondary like equity.

They keep rolling over the medium term bank loans and ecbs (taken before asset was added to invit ) with long term (10yr NCDs). Thus I believe, reducing interest costs and rollover risk (no. of time debt needs rollover). Only risk is higher interest rates at rollover / non-availabity of funds at rollover.

Its a smart way of financing the huge projects by diluting your equity stake (ie 25%) at the same time keep control of company though self appointed asset manager.

As long as manager acts in favour of unit holders and purchases future assets with prudence and arms length with sponsor / third party, and doesnt face liquidity crunch at rollover (high int rates) they should be making money.

discl: not invested in, but keen on investing (timing), invested in Reit

2 Likes

According to this filing made by Indigrid on 15th March, 3 institutional investors - DWS Investment Management Americas, Inc., DB International (Asia) Limited and RREEF America L.L.C - disposed of 57 lakh shares of Indigrid between 26th July 2018 and 13th March 2019. The sale was done through the market (i.e. no block deals). The shares sold constitute about 2% stake in Indigrid.

If you look at the price & volume chart of Indigrid, the price was quite stable (around Rs 95-96) till July 2018 (month when the above entities started selling) and daily volumes are relatively low (rarely crossing 2 lakh). Volumes picked up in July and August 2018 and have been relatively low since then. So I am guessing most of the selling happened in July and August 2018.

Would this explain the consistent drop in price of Indigrid or am I drawing the wrong correlations?

1 Like

1 Like

"

₹2,560 crore of primary capital through a qualified institutional placement (QIP) beginning Wednesday

The proceeds of the QIP will be used to acquire transmission assets. IndiGrid has signed agreements to acquire five more transmission assets from Sterlite Power worth ₹11,500 crore, subject to the approval of unitholders, the person mentioned above said on condition of anonymity.

KKR has also expressed intent to be a sponsor of IndiGrid alongside Sterlite Power, after which KKR and Sterlite Power will co-own SIML, the investment manager of IndiGrid.

"

Better corporate governance after KKR is involved?

Disclaimer only own Embassy REIT, still analysing indigrid

2 Likes

Great news. Market has two major concerns with regards to the IndiaGrid Invit - Maintenance / Growth of DPU and Corporate Governance

- With Fund Raising scheduled for completion from marque names - they should now be able to complete the asset acquisitions and grow/maintain the DPU. Without acquisitions the DPU starts to fall as operating expenses start increasing over time (nature of Transmission assets business)

- Corporate Governance concerns (considering market had a bad view of Sterlite) should also reduce if KKR becomes part the Sponsor (I was anyways happy with the way IndiaGrid management used to conduct themselves)

Ideal time to load units - DPU of 12 gives a pre-tax yield of ~14.25% which is just phenomenal.

1 Like

Indigrid has officially announced:

- The opening of preferential issue, for amount upto Rs 2560 Cr. The floor price is set at Rs 83.89 per unit.

- Definitive and framework agreements for acquiring 5 assets from the sponsor. The total enterprise value of these assets is Rs 11,539 Cr.

- Considering and approving designating Esoteric (an affiliate of KKR) as a sponsor of lndiGrid (along with the current sponsor - Sterlite Power Grid Ventures Limited).

See this announcement in detail here -https://www.moneycontrol.com/stocks/reports/indigrid-invit-fund-outcomeboard-meeting-15222261.html

Few questions arise:

- What are definitive and framework agreements? When would the assets become a part of Indigrid?

- I am not sure what to make of the floor price, which is set at Rs 83.89. Most of the holders of the units would have purchased them at a significantly higher price.

- I am not sure of the impact of the ‘investment + asset purchase’ on the DPU. Will it go down/up in the short term?

Any thoughts?

The new fund raising seems to have smoothened return expectation for a long time to come. They are promising DPU of at least Rs 12/unit for the next 10 yrs which means yield of 14%+ pre tax @ CMP. Additionally, I don’t expect further erosion in the unit value after KKR is on board now. Yieldwise this asset seems to be better than Embassy for the next many yrs to come.

Disc: don’t own it but Invested in family accounts

1 Like

I think only thing negative was that the LTV was raised to 67% which means the rating would go down and increase the cost of capital. This would also reduce the future headroom for growth.

Future dilutions would hopefully also be DPU accretive.

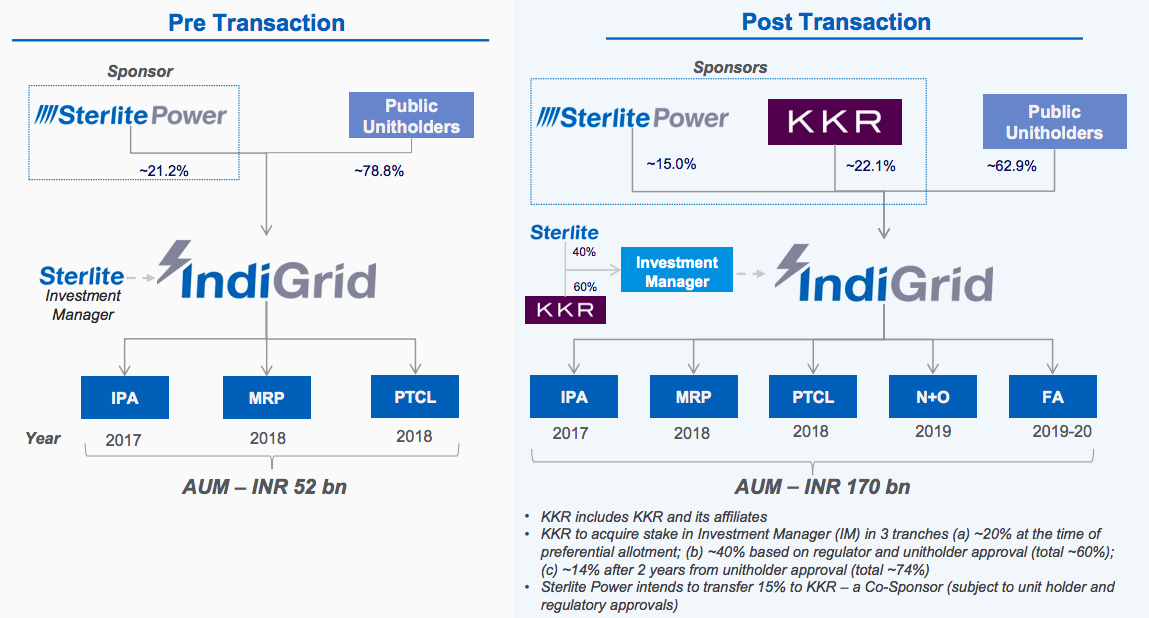

The presentation is quite detailed. This is how the holding structure looks now:

If you read the notes it says that:

- KKR plans to increase stake in the investment manager to 74% (in 3 tranches)

- KKR will buy out 15% of Sterlite Power in Indigrid i.e. Sterlite Power will completely exit as a unit holder.

With Sterlite Power’s exit, the InvIT could then look at assets other than those owned by Sterlite.

Even though Singaporean sovereign wealth fund GIC has participated in the preferential issue, it does not feature in the above graphic. I think that is beacuse it is now clubbed under public unit holders.

The pair will invest 20.64 billion rupees ($295 million) for a 42% stake in the trust via a preference equity issuance, the people said.

Source: [Livemint] KKR, GIC betting on India’s power sector with $400 million investment

Sterlite has invested about 450 Cr to maintain the minimum regulatory requirement of 15%. This 15% will later be acquired by KKR as mentioned above. This will take KKR + GIC stake to 57%.

Also the assets have now increased to 11(from 6). This includes 2 assets which have been acquired (so present total is 8) and 3 frame work assets which will be acquired after commencement of operations. The acquisition price for these 3 assets has been locked. AUM has become (or will become after the transactions have completed) 17000 Cr from 5200 Cr. Net debt/AUM will be 67%, was 47% earlier.

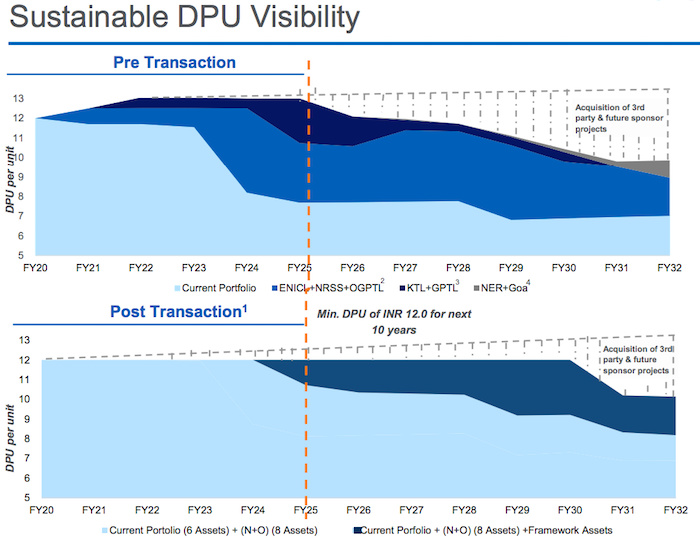

Here is the best part, DPU visibility:

DPU of 12/year till FY24.

3 Likes

Indigrid held the conference call yesterday. It was mostly about the new fund raise and the acquisitions. The management ran through the presentations shared with the exchanges. Here are the key points.

- DPU guidance for FY20: minimum Rs 12.

- The new SEBI regulations regarding the lot size: SEBI has given 6 months to comply with the regulations. Indigrid plans to complete this by June.

- Regarding recent media reports about non-refinancing of InvIT debt by banks: Indigrid is working with the regulators and the government for more clarity on this. If banks don’t refinance then they will choose the debenture option. Since Indigrid is AAA rated there won’t be problems in issuing debentures.

- Revenue profile of new assets: Not all assets have a reducing revenue profile. Some assets have a fixed revenue profile (i.e. revenue does not change as years pass), some have a increasing revenue profile, while some have a reducing revenue profile. Management shared which assets were which, but I did not note it down.

Investors raised a few concerns:

1. Preferential issue price

Atleast 3 people asked Indigrid about the low issue price (Rs 83.89). Unit holders who subscribed to the IPO at Rs 100 felt this was unfair to them. When NAV is around Rs 96, why did Indigrid raise funds at almost a 13% discount to the NAV? Also why were not existing unit holders given an option to participate in the preferential issue? To this the management countered with these arguments:

- SEBI regulations say that only QIBs can participate in the preferential issue (I haven’t verified this claim). They did approach existing institutional unit holders to participate in the issue. Others (retail investors) could have acquired units from the market, since prior to the issue the trading price was lower.

- Base price for the issue is dictated by the trading price of units, which was beyond Indigrid’s control.

- Indigrid could have waited for the unit price to correct (i.e. move upwards) and then go for the fund raise. However that would have put the DPU in the near future at risk, since without acquisitions it would have gone down. The fund raise has given 2 things: well capitalized for growth for the next 2 years (without the fund raise, raising AUM to 17k Cr would have been impossible) and DPU visibility for the next 10 years.

- The AUM growth and DPU visibility would accrue to existing investors as well.

- After the IPO, the Sponsor (Sterlite) acquired additional units at a higher price (If I remember correctly that was around Rs 90). So IPO unit holders are not the only ones.

My opinion: I feel a fund raise as large as Rs 2500 Cr (almost equal to the market cap of Indigrid) could have been done at a higher price. KKR could not have acquired units at this rate from the market without affecting the trading price. However I think, lack of interest from other institutional buyers lead to the low issue price.

2. Acquisition Details of the Investment Manager

In parallel, KKR has also acquired stake in the investment manager. The details of this acquisition have not been disclosed. One investor questioned whether this was a conflict of interest. Management said that they will evaluate this request, but insisted that the amount involved was insignificant as compared to the preferential issue.

My opinion: Remember that the investment manager is responsible for deciding the acquisition targets for Indigrid. Since Sterlite plans to completely exit as a unit holder, it makes sense for KKR to become the investment manager. This will be in interest of all unit holders, since this will ensure that Indigrid won’t look only at Sterlite’s assets for growth.

7 Likes

I also attended the call. Congratulations for an excellent summary.

1 Like

Indigrid has completed the acquisition of assets worth 5025 crores from Sterlite Power. See Press Release.

India Grid Trust (“IndiGrid”), India’s leading infrastructure investment trust, today announced closure of the acquisition of two power transmission assets, NRSS XXIX Transmission Limited (“NTL”) and Odisha Generation Phase II Transmission Limited (“OGPTL”), from Sterlite Power for an enterprise value of ~INR 5,025 crores. IndiGrid had signed definitive documents to acquire the two assets in April 2019.

The acquisition has been funded through the preference unit issuance worth INR 2,514 crores, subscribed by KKR, GIC and other capital market investors in May 2019. The remaining amount has been funded through debt raise at IndiGrid and OGPTL. For this purpose, IndiGrid has issued INR 1,400 crores of AAA rated debentures and INR 200 crores worth AAA rated Market Linked Debentures, first of its kind issuance by an InvIT in India. A loan of INR 550 crores at OGPTL has also been extended by Axis Bank. Post-acquisition, IndiGrid’s net debt to AUM is below 49% and significantly lower than the permissible leverage cap of 70%, leaving significant debt headroom for future acquisitions

It looks like KKR has taken control of the board of the investment manager. See Press release.