With MFI its usually not the cycle, its the event risks - political interventions, waivers that are the cause for concern. The going remains good until it stops to do so.

SKS Microfinance was a case in point. Going remained good, Vikram Akula’s dream vision was totally in progress until an outside force decided to wholly interrupt it and till date AP / Telangana form less than 2-3% of total MFI loans in India.

There’s also survivorship bias when you exemplify something that’s been successful.

One should also look at examples that were successful until they really really struggled and equity investors were wiped out. Case in point: Basix India just after Andhra MFI Crisis - https://knowledge.wharton.upenn.edu/article/vijay-mahajan-rebuilding-a-stronger-microfinance-sector-in-india/

Businesses are resilient inherently, but external blows end up killing them - especially when the blows are powerful (sitting politicians, rural / semi-urban leaders with large influence) and large (people have tendency to stop paying at the slightest hint) - for e.g. in one annual report there was a mention that during a past MFI crisis, people said they willing to borrow and pay as long as:

- There’s regular lending

- Others are paying - This one is really ignored. The lemming-like / herd-like behavior due to lack of education.

Then finally, what happened with Basix - was liquidity crunch - banks not willing to lend and in India (unlike in Bangladesh), NBFCs cannot fund their assets with deposits from common people.

This all said - while current situation might not be as grim as past crises, these should ideally not be ignored - as these have the potential for permanent capital erosion. - i.e. a probability of say 5%, but a loss of 95% - 100% if the event occurred.

2 Likes

This time it seems like RBI was proactive in curbing overlending before it got more out of hand.

Based on the growth, stress, credit costs, and number of lenders per borrower figures it seems like the culprits were the small newcomers, probably funded by PEs, hungry for growth at any cost. The biggest listed ones seem to have it under control for now. They didn’t have any control over what the borrower did after their loan.

Now it seems like the sector is becoming more competitive despite the number of lending institutions reducing, the new guidelines of max 3 lenders has everyone reducing interest rates. If the troublesome, grow at any cost, lenders are leaving the industry, this should help with employee attrition as well.

Yes things can take a turn for the worse from here if additional catalysts develop. From the commentary seems like the management cannot wait long enough to be amply diversified away from unsecured MFI. Getting valuations through stable ROA, and for raising growth capital is a necessity for such institutions.

Interesting times ahead, in 3 yrs the sector will look a lot different.

1 Like

A good listen for some understanding of the ground realities of people who likely constitute the microfinance customer segment

1 Like

https://www.business-standard.com/opinion/columns/the-phoenix-of-india-s-financial-system-microfinance-s-path-to-recovery-125020900373_1.html

The question is: If the Bill is targeting the unregulated entities that have been mimicking MFIs on the field, shouldn’t the word “micro finance” be replaced with some other word? Indeed, microfinance is all about micro loans but since the MFIs primarily disburse such loans (banks of course do too), they get the blame and cannot escape the fallout as most of the borrowers don’t distinguish between regulated lenders and the unregulated ones.

(Emphasis added by me, not in original article)

Interesting. Its just amazing how many times the same cycle is playing again and again and again, and in each cycle, those that didn’t bother studying history or witnessed it firsthand but forgot it conveniently, end up being taken for a ride. - both, from lending and investing perspective.

1 Like

Could you please post a summary as it is behind a paywall.

I am one of the uninformed ones. Can you share more insights on this or share useful links to read? The history and cycle.

Here are the articles -

https://www.financialexpress.com/business/banking-finance-rbi-expresses-concerns-over-small-finance-banks-rising-asset-quality-stress-says-mergers-best-way-to-mitigate-risks-3730885/

basically for the next 2-3 quarters most Microfinance lenders will report high NPA’s and write off bad loans. Some are already reporting losses like ESAF and Utkarsh. Muthoot Microfin is just above water, but might slip into negative next quarter.

1 Like

Today, we observed strong momentum across several stocks with exposure to the microfinance (MFI) sector. Notably, there have been developments around Fusion Microfinance (YouTube link) that may have contributed to the positive sentiment.

Stocks such as Spandana Sphoorty, L&T Finance (LTF), CreditAccess Grameen, IndusInd Bank, and IDFC First Bank showed a notable upmove.

Given the recent price action and renewed investor interest, can we now consider that MFI-related stocks have potentially bottomed out?

3 Likes

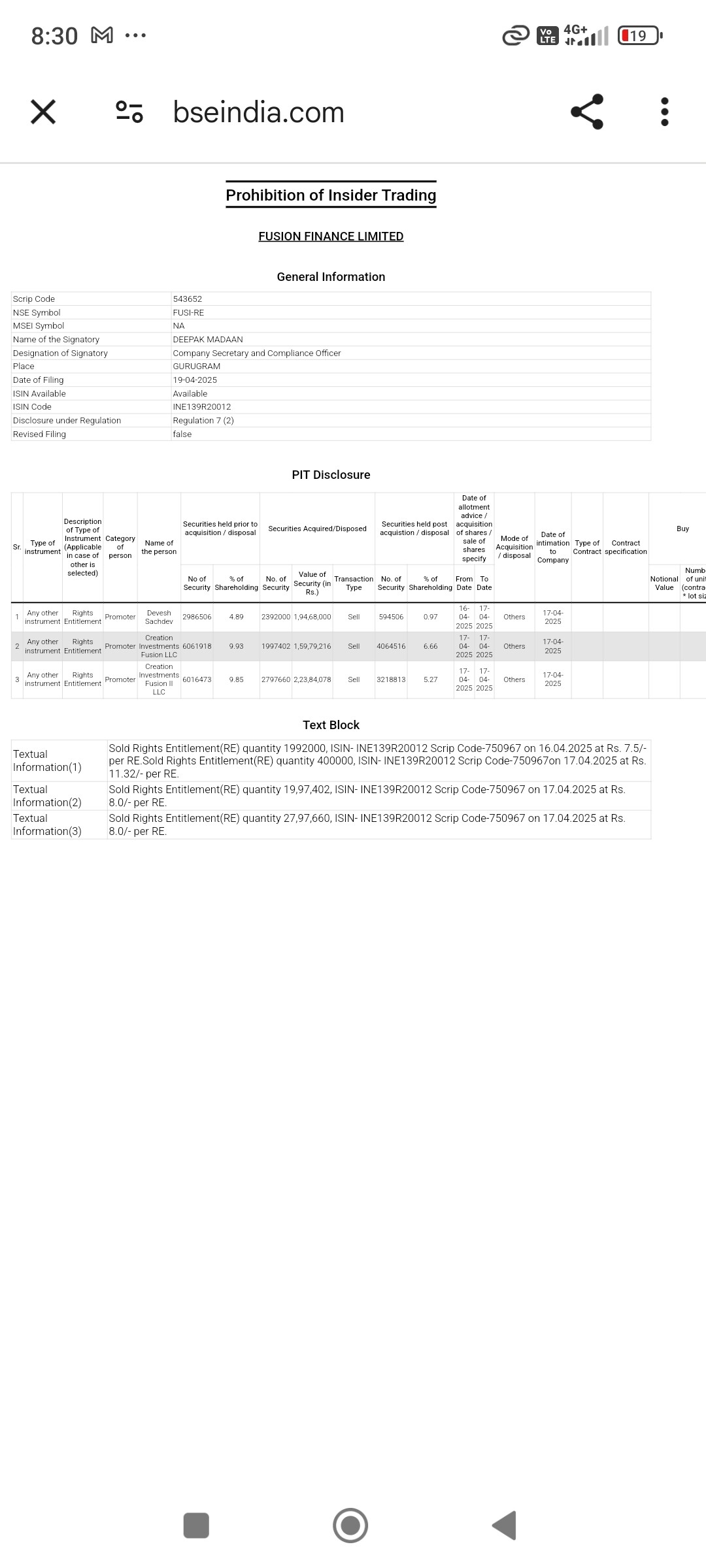

Regarding fusion:

They are raising 800 cr via rights.

But rights entitlement to a lot of extent were sold by promoter, means they are forgoing rights and not indusind money proportionate to their shareholding.

I was trying to find a buyer , if they have sold the rights to open market or via a blockdeal to an institution.

If the buyer of rights has been an institution , I’d take that as a positive development.

But no clarity yet.

some one with clarity may shed some light.

If promoter sells his rights entitlement, does it cast a doubt on the exercise of rights turning out to be successful/failure?

These two promoters had already made their intentions clear in the offer document. Two new FIIs have entered very recently. Till now the Rights subscription is 0.19 times and nearly 86% shares are held by non retailers; so the very likely is that the Rights issue would sail through.

1 Like

Are u referring to Acm global fund vcc making its position in counter in last quarter .

Still don’t have information if waburg piscus is following the rights through for the rights.

Would you have any information or source of information supporting their backing in rights subscription?

1 Like

Please refer the Offer documents of the Rights issue. The same was committed in the last concall.