HDFC Securities has published a report on Microfinance Industry where they have initiated coverage on Bandhan Bank, Ujjivan Financial Services & Small Finance Bank and CreditAccess Grameen.

1 Like

PFA

3 Likes

good data points -nice analysis

Is it possible for you to add pre provisioning profit growth % for last 5/3 /1 year and analyse -this gives you an indication of the sustainable profitability over longer period and then see credit cost /GNPA (underwriting skills )along with the matrix i asked for (along with these we need to see ROE and ROA which you have done) ,thanks

Hi Debashish,

I do not track growth metrics for financials and thus don’t have the data. I prefer to focus more on asset quality rather than growth.

2 Likes

This is an long pending action in bringing banks and SFBs portfolio under similar framework of MFIs, but pricing cap cannot be put on banks and SFBs, since this will do more harm to MFIs rather than banks

Yeah, and many of the SFBs (top 3) at least will be moving to universal bank license in the next 3 years.

I have seen arman finance as 15cr company share price was 17 . Now it becomes 1000cr company almost.

I can see similar story happening with QGO FINANCE but this time story was some what different.

But i was prettymuch optimistic about rachna singis vision and his ability to execute.

I request members to have look and input to the relevant thread.

Thanks

Disc. Invested.

1 Like

Why NBFC’s which do Mircrofinance are specifically categorised as NBFC-MFI. We do not see much another classifications in other areas like vehicle finance, personal loans. One other case is Housing finance, where if you got classified as NBFC-HFC. In this case, they can access funding from NHB which is a low-cost funding. Once the size of NBFC reaches certain size, seems this low cost funding also stops. Recently IndiaBulls Housing mentioned that they are asking RBI to classify themselves as NBFC instead of NBFC-HFC, since there is no advantage is getting classified as NBFC-HFC.

On similar lines, what is the benefit companies are getting if they are getting classified as NBFC-MFI?

Havent gone into the details, but NBFC-MFI “MAY” have benefits of,

- being classified under PSL, enabling them to sell the loans to banks to fulfill their PSL requirements. Though not sure if one require to be NBFC-MFI to sell PSL certificates related to MF.

- SRO participation, standardized regulatory window, protection from local politics. (NBFCs must have this as well for the last one).

- Pricing of loans, collections teams as per regulations (before the current deregulation of loan pricing)

- RBI regulations may say that anyone having MF portfolio of more than 500 cr needs to be classified as such.

- Raising funds from impact investors, NABARD and other MF targeting schemes. This can help reduce funding costs.

2 Likes

Could someone please update on the present crisis in the microfinance industry with focus on the Fusion Finance.

If you notice, for last few year there is a huge increase in microfinance portfolio of all the companies. Microfinance has this peculiar thing that in good time, asset quality of these companies will be quite low, but when thing go bad, they happen in very short span of time. For achieving the growth, these companies tend to give loan to some customers who already have got some loan with other companies. Even though each company is is giving something like 50000 only to the customer, when many companies lend to same customer, suddenly customer is over levered. Below pic sums up what happening

In the pool of fusion customers, by the end of FY23, customers having loans from more than 4 lenders is 6%, but by end of FY24, customers having loans more than 4 lenders is 24%. Now Fusion and Spandana showed higher detoriation, but the general trend is NPA is increasing in all lenders. If you read Equitas concall, the openly stated that microfinance lenders are following bad practices(please read equitas Q1FY25 concall, you will get more clarity)

5 Likes

Banks/ NBFCs also do micro finance lending and the vice versa Microfinance institutions also do MSME and other loans. In my view the classification of the lending business should be secured vs a vs unsecured lending. The present problem is shown as the problem segregated to the MFIs only and the other lending businesses are fine. Is it that the problem will not percolate to the other lending businesses and the MFIs will only face the headwinds resulting to the value compression from its peaks of P/BV multiple of 3 to 0.2 ( in an extreme passimism) or MFIs are just ahead of the downward curve in the whole financial sector? As the rate cuts are just round the corner this situation would have been avoidable. Fusion Finance had a picture perfect situation up to FY 24 with ROE of 20%, ROA of 5% along with doubling AUM every alternative years and everything got melted in 4-5 months that too when the rate cut cycle is about to start! Please help me as I am unable to connect the dots. I had a perception that MFIs would do well in the rate cut cycles that doesn’t seem so far.

2 Likes

This issue is purely because of over leverage on the customer front and currently this is in microfinance business only. MFIs lacked discipline, went on crazy to lend. They created this mess themselves.

Rate cut or raise will have small impact in margin here and there, this will not have relation to asset quality. My personal view, Interest rate cut doesn’t mean these companies will do well

4 Likes

Respectfully, if one is unable to study the entire sector over a cycle and not separate the good management against bad ones, they should just avoid the sector.

There have been so many opportunities (2010 AP crisis, DEMON, COVID and now 2024 elections) that can help identify who is lending responsibly, who is diversified in products and geography etc.

Dont just chase the managements which are guiding for 2x the industry growth when the peers are turning cautious.

5 Likes

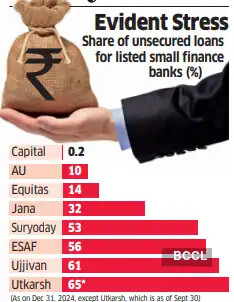

Small finance banks face concentration risks in two ways. First, many have high exposure to the microfinance sector, which has been reeling under stress. Second, a few such banks have large exposure to the geographic pockets of higher stress.

So on one side, there’s the mandate of financial inclusion, priority sector lending, presence in the form of unbanked rural centres, high capital requirements, on the other side there’s pressure from RBI on margins because MFI lending is considered a concern as opposed to making a statement to the state governments to stop making political interventions in MFI lending and instead working directly with MFI bodies (Sa-Dhan, MFIN, AKMI) to ensure compliance to RBI norms on lending prudence and recovery practices.

What’s even more surprising is - An Ujjivan - with an unsecured portfolio of over 60% and a Jana with an unsecured portfolio of around 30% or Equitas with an unsecured portfolio of mid teens (around 15%) are all trading a similar valuations - around 1.15-1.2x recent book value.

This is because all unsecured lending isn’t necessarily risky - it depends on the borrower profile, loan duration, loan purpose (income generation or other). There are MFI companies which have 90%+ unsecured lending (e.g. CreditAccess Grameen) who have been able to successfully navigate many cycles with a healthy loan book / balance sheet

1 Like