IEX shares rise up to 13% on likely APTEL relief on CERC market coupling norms

As per my views stated earlier …let’s hope wrongs are righted now

IEX shares rise up to 13% on likely APTEL relief on CERC market coupling norms

As per my views stated earlier …let’s hope wrongs are righted now

As per efficient market hypothesis, if market coupling is removed, and everything else remains the same, price should immediately increase to pre-coupling price (before 23 july).

As per behavioural finance, recovery may take time due to increased perception of regulatory risk, investor memory bias, and other behvioral biases at play.

Between coupling announcement and now there have been following changes -

Pre-coupling price also included overhang of a potential coupling order. In case the coupling order is withdrawn the overhang is also removed, which implies price should immediately increase to levels above 23july levels on 9th Jan.

Happy to learn if i am thinking correctly.

imo TTM EPS (INR 5/share) * median PE (40) should be the fair valuation anchor. not sure when it will be reached.

wrt transaction fee reduction. HPX, PXIL have represented that they dont have much room for fee reduction [143.pdf] in last petition order (https://www.cercind.gov.in/2022/ROP/143.pdf), doesnt seem like this would have changed much since 2022. Any meaningful reduction in transaction fees would directly impair the commercial viability of both exchanges.

Quoting from the petition, IEX platform saved INR 32000 crore for buyer, ~ INR 0.74/unit against which INR 0.02/unit is charged as fee, ~3% fee does not appear excessive and is arguably well within what any DISCOM would be willing to pay.

IEX has shown, arbitrary regulations of CERC will get legally challenged and must ultimately satisfy the test of materially improving market efficiency. This places the regulator on a tightrope, ensuring fairness and competition, while avoiding outcomes that undermine the efficiency and integrity of the power market.

On the transaction fee side, the ceiling comes from power market regulations 2021 and the above petition has been decided based on that, for which the final order came in April 2023 allowing them to charge upto 2p per unit (20 Rs per lot of 1MWh).

Unless there is separate new regulations by CERC, which would be a pubic consultative process for few months whenever the need be, any change in transaction fee ceiling is highly unlikely.

Disc: Have positions and biased

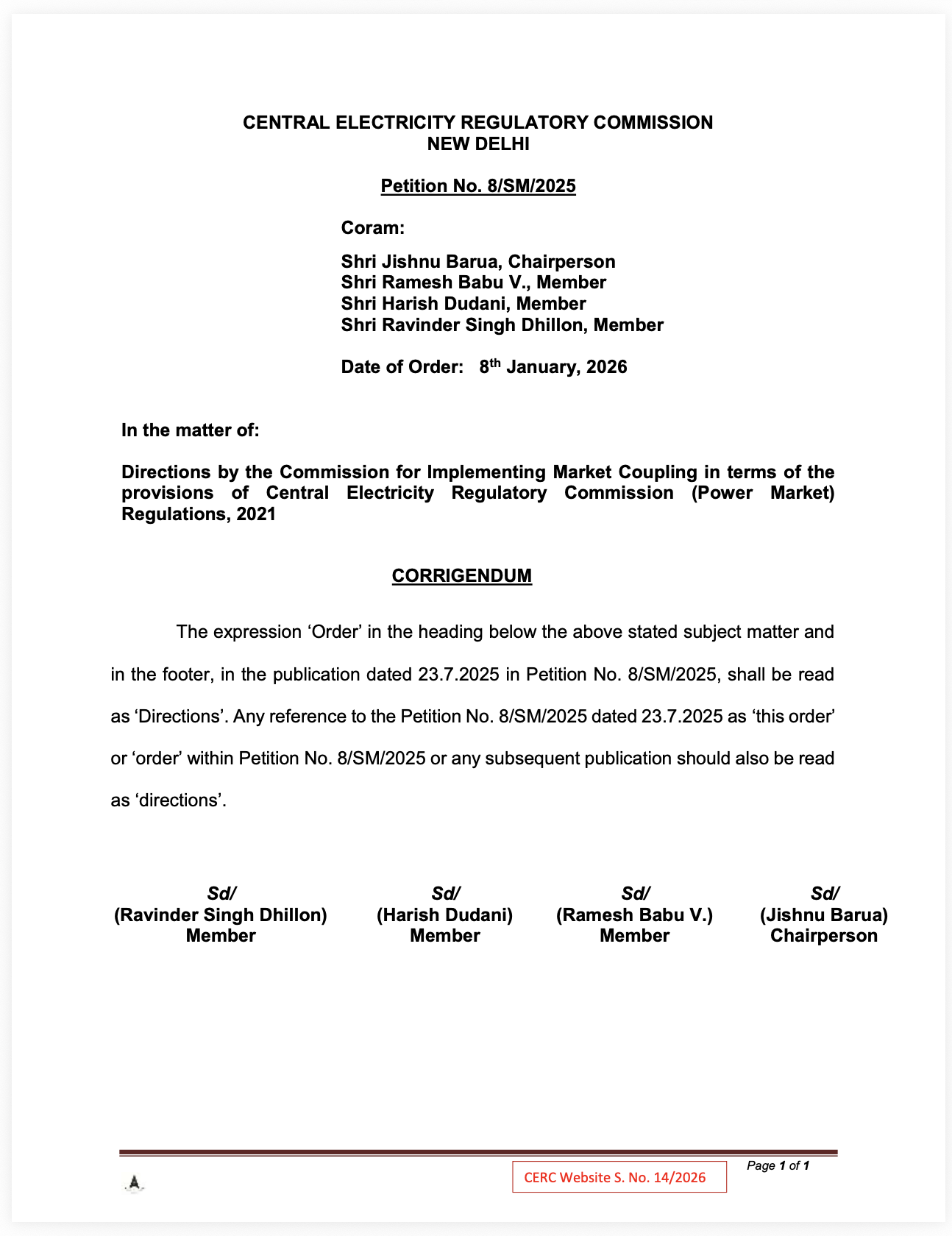

Corrigendum-8-SM-2025.pdf (87.2 KB)

2026.01.09_06_48_09am.pdf (117.3 KB)

(Link for Video Conferencing for Hybrid Hearing through Cisco Webexis)

( https://bit.ly/Court-1)

The recent fall in IEX looks driven more by short term news flow and operator led volatility than by any real deterioration in the business. The market coupling narrative and hearing related updates over the last few days have amplified sentiment swings, but the core franchise remains intact. This kind of event driven pressure is exactly when high quality platform businesses often become attractive for long term entry, because price temporarily disconnects from business strength.

Fundamentals in the latest quarter continue to be solid. In Q2 FY26, electricity volumes were 35.2 BUs, up 16.1 percent year on year, despite largely flat all India demand in H1. Revenue grew 9.2 percent to ₹183.3 crore, with the gap versus volume growth mainly because certificate revenue fell sharply due to lower REC volumes and the transaction fee cut, while electricity revenue itself was up about 16 percent. PAT was ₹123.4 crore, up 13.9 percent, which again shows the operating leverage and resilience of the model even when a non core revenue line is weak.

The most important structural positive is the mix shift. RTM has now become the largest segment for the first time, with about 15 BUs volumes and about 39 percent year on year growth, and roughly 36 percent share. This is not a one quarter story. It is a structural outcome of rising renewables, higher forecast error, and the growing need for tighter balancing. As renewables keep rising, the system will require more short term procurement and intra day correction, which naturally expands DAM and RTM versus the long term PPA heavy world. In simple terms, the short term power market will grow much faster than the long term contracted market, and the exchange volumes can become multiples of today over the coming years.

Even if we assume a tough regulatory outcome and market coupling happens, the dominance of IEX is unlikely to vanish. Market share could reduce from the mid 80s to maybe 60 to 70 in a worst case, but liquidity driven businesses do not lose relevance easily. Trading tends to concentrate where liquidity is deepest, because liquidity attracts liquidity, and that is IEX’s biggest moat built over many years. The same logic is why simply giving licenses to large players does not automatically shift volumes. We have seen in commodities that even big brands can struggle to build meaningful liquidity if the market already has an established venue.

One more long runway opportunity is IGX. It is growing steadily from a low base, and as India’s gas ecosystem expands, city gas, industrial switching, LNG based balancing, and eventually more flexible generation, a gas exchange can become increasingly relevant. If IGX continues to scale and liquidity deepens, it can evolve into another strong platform business under the IEX umbrella, adding a second growth engine and meaningful optionality over time. Net net, this correction is giving a chance to enter a high quality, asset light, network effect business at a far more reasonable price than the euphoric periods, with long term volumes and new products still pointing upward.

Invested and Biased.

With the increasing penetration of renewable energy—which has a relatively unstable power supply over the 24-hour cycle—coal and hydro plants are required to frequently adjust their output. As a result, power trading, especially in the Real-Time Market (RTM), is expected to increase.

Overall, power trading is a regulated market with a limited number of participants—primarily generators and DISCOMs—numbering at most a few hundred. The market for Renewable Energy Certificates has a larger, but still limited, set of traders. Given the small size of the market, this raises the question of whether there is any real need for multiple power exchanges, as opposed to ensuring that a single exchange is well regulated and operates smoothly. The rationale behind CERC’s insistence on multiple exchanges is something only they can explain.

CERC affidavit changes the June 2025 “Order” to “Direction” which makes it non-binding. Effectively market coupling order will not apply in near future. That should be positive for stock why it’s no positive reaction to this. What am I missing here?

Disc: Invested in IEX

My interpretation is the following (although trying to guess price movements is likely injurious to my health)

a. Correction of order to direction does not confirm that there will be no market coupling. APTEL clarified that for CERC to implement they will need to establish a proper regulatory framework and therefore as a worst case scenario, market coupling will still be implemented but is delayed from the original timeline (see CNBC TV18 link posted above by @jainpatti ). Of course CERC could change their mind and on Jan 19 when the next hearing is they could decide there is no need for further regulation (which is what IEX is arguing for) - they could also say they want to review more or even that they will now go into a consultative process to implement the direction to a regulatory order.

b. Press reports (currently not validated by IEX or CERC) on potential price cap reduction from Rs 2.00 to between 1.25 / 1.5 had soured sentiments at the end of 2025 (Lower, fixed transaction fee for power exchanges in the works - The Economic Times).

If I combine a small loss in market share with a decline in price caps, then even a reasonable transition to more traded power translates into a revenue growth of less than 10% for the next 3-4 years - which would affect valuation and price. Of course there is a more bullish case where neither of these happen (no market coupling and no price cap change). There is also a more bearish case where other products get added into market coupling over time although most arguments seem to imply this is low probability (I have not particular insight into the likelihood of this)

So in effect, the price seems to be affected by the overall poor sentiment coming from regulatory uncertainty. The next hearing on Jan 19 may bring more clarity - or may not. I have been building a position in IEX but am unable to gain the conviction to make this a full position as I am looking to protect downside at this point. The price cap regulation is a a tricky one as it has a big impact on revenues of all players (and smaller will suffer more). No market coupling and price regulation will be a really problem for PXIL and HPX so likely they will argue against further price cap regulation - if that is not a rumour and an actual event.

Happy to hear other views on this

Disc. Invested but looking to add (based on regulatory clarity) so likely to be biased. Not SEBI registered and this is not financial advice - just my approach

until APTEL gives a formal order nothing has changed fundamentally. Media is creating narrative basis ongoing arguments of IEX & CERC counsel which is used by operators to create volatility.

I wrote down my thoughts on how competition could evolve in a post-coupling world. it may be a bit verbose. Apologies for that.

Let us assume that market coupling is implemented across segments such as DAM and RTM. In such a scenario, the liquidity and network-effect moat of IEX largely disappears. The central question then becomes how competition reacts once this structural advantage is neutralized.

I have attempted to think through this using basic game-theoretic reasoning, though my understanding may be imperfect.

The power exchange industry has a few defining characteristics:

At the industry level

At the customer level

Once market coupling is in place, exchanges lose the advantage of liquidity concentration. The remaining competitive levers are therefore limited to:

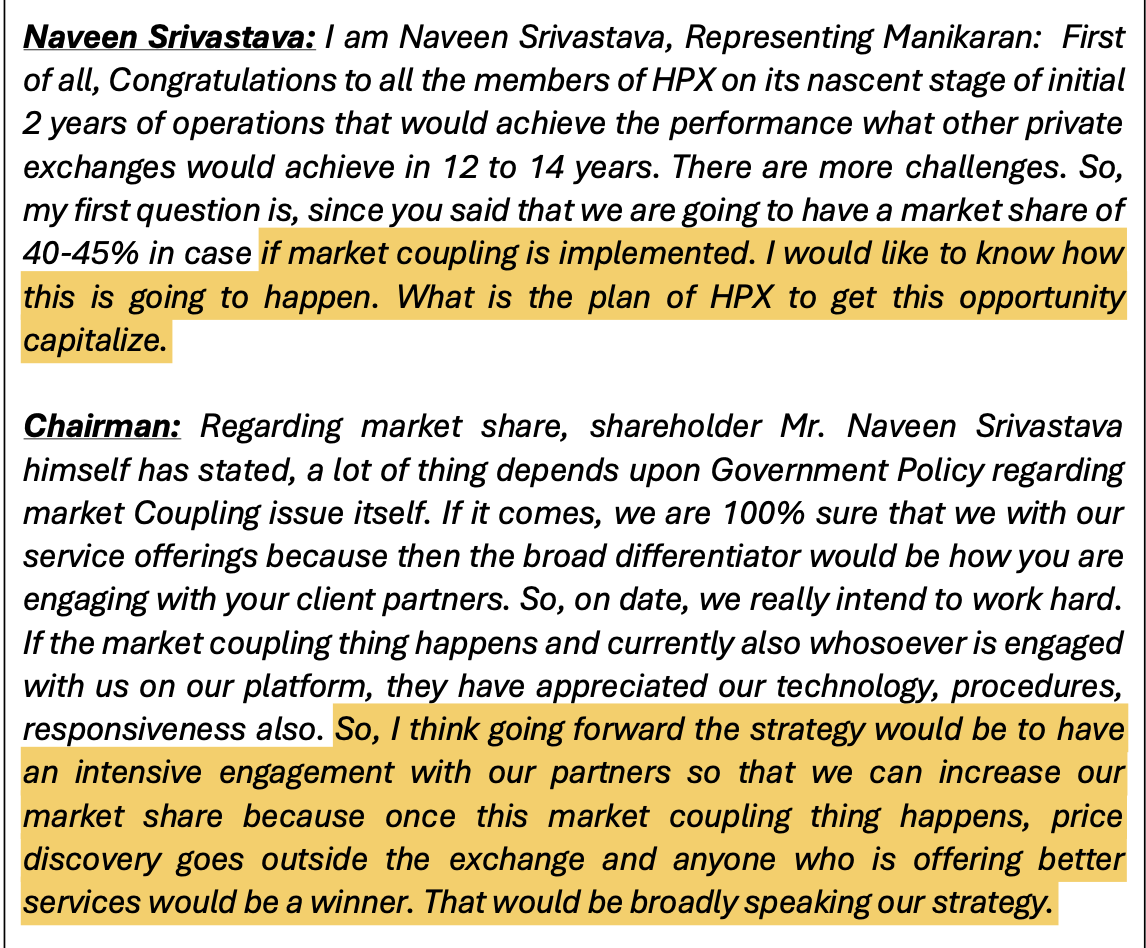

Rather than speculating in the abstract, it is useful to look at stated strategies. The chairman of HPXIL, in the AGM transcript, explicitly mentioned that their post-coupling strategy will focus on product, technology, and service quality.

Source: https://www.hpxindia.com/downloads/Sixth_AGM_Tanscript_23_24.pdf

This naturally raises two questions:

This is where balance sheet strength becomes relevant.

| Company | Cash Balance / Investments | Comments |

|---|---|---|

| IEX | ~₹1,700 Cr | As of Sept 2025 |

| PXIL | ~₹200 Cr | FY24 revenue ₹63 Cr, PAT ₹22 Cr |

| HPXIL | ~₹215 Cr | FY25 revenue ₹40 Cr, PAT ₹10 Cr |

If competition is centered on technology and service quality, IEX clearly has the financial capacity to close any reasonable gap. A strong balance sheet also serves as a deterrent against aggressive pricing wars.

Based on this, one could reasonably conclude that customer churn driven purely by product, technology, or service quality differences is likely to be limited.

Given that the industry has only three players, with one being clearly dominant, the market could evolve into a form of cooperative competition. A useful analogy is telecom, where consolidation eventually led to a small number of stable players (after the brutal pricing war). Another is cement companies in certain micro-markets.

However, there may be a fifth lever available to competitors that is not available to IEX: shareholding structure.

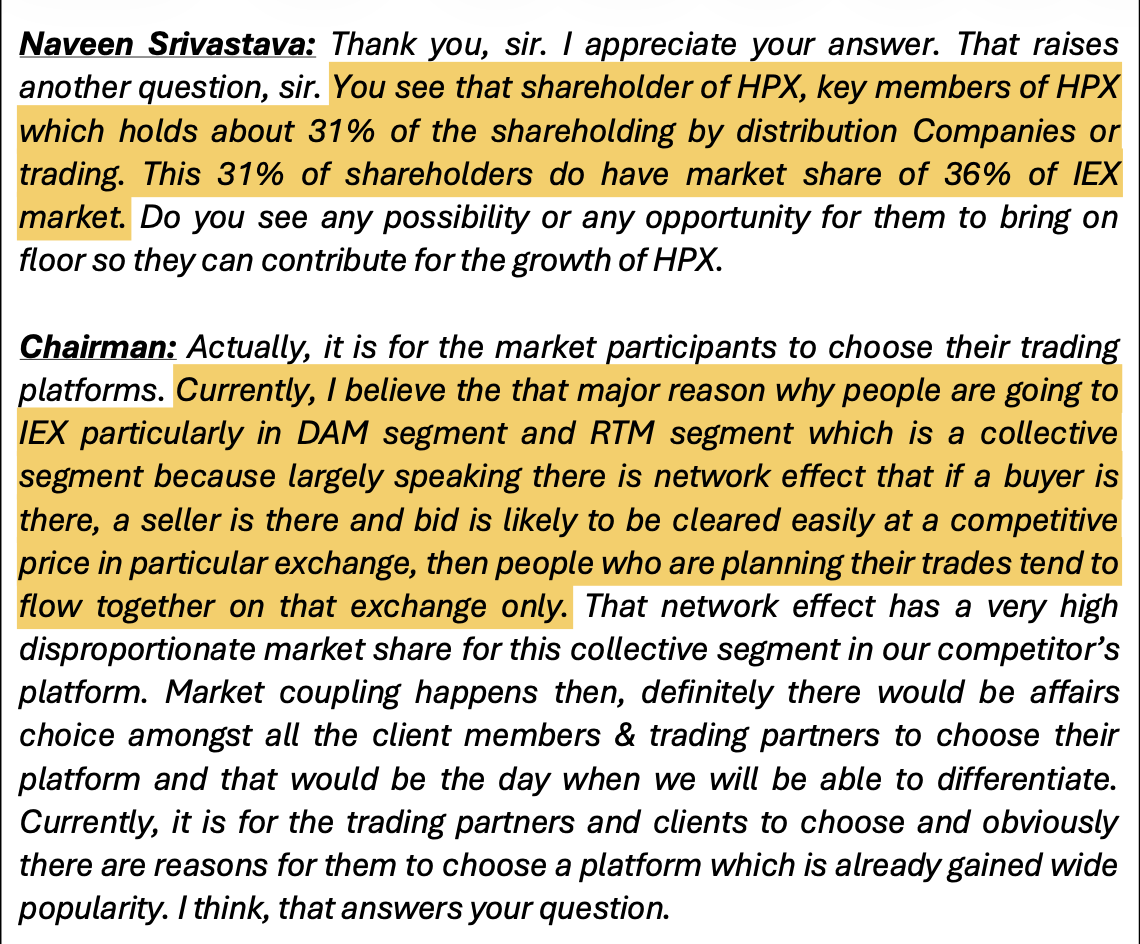

HPXIL is promoted by entities such as PTC, BSE, ICICI, and several power producers and buyers including Greenko Energies, Jindal Power, Manikaran Power, SJVN, REC Limited, and certain state DISCOMs.

Source: https://www.hpxindia.com/downloads/Sixth_AGM_Tanscript_23_24.pdf

Notably:

At present, the primary reason these participants do not migrate volumes is inferior price discovery on non-IEX exchanges. This is especially visible in DAM and RTM, where price discovery is concentrated on IEX.

PXIL’s shareholders include entities such as Power Finance Corporation, NTPC Vidyut Vyapar Nigam, Gujarat Urja Vikas Nigam, MP Power Management Company, West Bengal DISCOM, Tata Power Trading, GMR Energy, and JSW Energy.

While public data on the share of IEX volumes attributable to PXIL shareholders is unavailable, it is unlikely to be insignificant.

Both HPXIL and PXIL also have plans for future IPOs. This creates an incentive for their shareholders to strengthen the exchanges’ trading volumes ahead of listing.

Today, volume migration is constrained because price discovery is weak outside IEX. Market coupling directly addresses this constraint.

Once price discovery becomes exchange-agnostic, the easiest and fastest way for competing exchanges to gain volume may be to encourage their shareholders, particularly those below the 5 percent regulatory threshold, to route trades through their own platforms.

This dynamic is largely independent of pricing, product quality, service levels, or balance sheet strength.

Assuming DAM and RTM contribute roughly equally to total volumes, the following scenarios appear plausible:

| Scenario | Expected Volume Migration |

|---|---|

| S1: No coupling | Nil |

| S2: Coupling in DAM only | 15 to 25 percent |

| S3: Coupling in DAM and RTM | 30 to 50 percent |

The critical question is which of these scenarios the market is currently pricing in. Unfortunately, there is no clear way to know with confidence.

All of the above reasoning could be flawed. The future is inherently difficult to predict, especially in a regulated market undergoing structural change. However, the shareholding-driven volume migration channel appears to be a material risk that is not fully captured when analysis focuses only on pricing, technology, service quality, or financial strength.

I am not able to figure out how IEX management will be able to mitigate this. Open to hear the views of fellow members.

Disclosure: Invested. Although my brain is telling me the negatives, my gut is telling me to go ahead. This is going to be a good learning experience for me. Hopefully not a costly one.

Disclaimer: Not a SEBI advisor.

Great points. Any thoughts about the shadow pilot?

At this point, there do not appear to be any publicly available interviews or discussions featuring power buyers or sellers (DISCOMs, generators, large industrial buyers) who have actively traded on all three Indian power exchanges (IEX, PXIL, HPX) or only one of the mentioned that would have given some idea on which direction the air will flow. Existing material online is generally limited to platform explainers or regulatory analyses rather than first-hand trader perspectives.

Given this, the only reliable way to gauge exchange preference remains market behaviour, and the data consistently shows that IEX has been the dominant venue for short-term power trading due to its deep network effects and efficient technology.

Even in the context of market coupling, where price discovery could shift to a central algorithm, the expectation is not necessarily that IEX will lose relevance overnight. Its long operating history, user familiarity, and higher transaction confidence continue to give it an edge.

PXIL and HPX may publicly project confidence about offering better services or competing effectively, but practically, it is difficult for any newer exchange to match IEX’s operational experience and established user base . No company will publicly state that it is less competitive, but real-world adoption is alws difficult.

Regarding recent price movements in IEX stock, the fluctuations appear to be driven more by uncertainty around the final regulatory stance on market coupling, rather than the CERC directive itself. Commentary from January 2026 hearings indicates that even the tribunal has raised questions on the rationale of the proposed coupling framework, signalling that clarity is still far off.

Given this uncertainty, it is unlikely that full-scale implementation of market coupling will occur in the next 1–2 years. During this period, IEX should continue to maintain meaningful absolute volumes, enabling sufficient cash flow to fund growth even if its long‑term market share eventually tapers by 20-25%. Meanwhile, IEX has historically introduced new market products and is likely to continue doing so to strengthen participation.

Disclosure: Invested; may be biased