Hi,

There is no announcement regarding this by IEX to the stock exchange most probably because this decision taken/to be taken by the Government will affect the power sector in general & not specific for IEX.

3 Likes

Substantial opportunity

Buy back of Shares update as on 20 Feb, 2023

As per the information filed at stock exchanges by IEX, they have bought back 38,97,159 shares from the market.

MCOs essentially pool all their trades under their umbrella and execute them. In Scandanavia , there is a rotating system of having each power exchange perform this role so there is equitable sharing of revenue among them. Now, in India, that has not been proposed and I believe CERC has advocated for a new entity to be MCO. Hence, it is a existential threat to exchanges who will barely have any business if that happens.

2 Likes

A detailed article on the carbon market and its current developments in Southeast Asia.

1 Like

Found this on stock edge social.

ICRA’s outlook on thermal power segment

With govt policy of har ghar bijli the power sector is on improvement. Let’s know the details:

ICRA’s outlook for the thermal power segment has been revised to Stable from Negative, supported by the healthy improvement in the thermal Plant load factor(PLF) level in FY2023, which is likely to sustain in FY2024 and the reduction in dues from state distribution utilities (discoms).

The PLF improvement is driven by the strong recovery in electricity demand growth in the country. The all-India thermal PLF level is expected to improve from 58.9% in FY2022 to 64.0% in FY2023 and further to 65.5% in FY2024, led by healthy demand growth and limited thermal capacity addition.

The full-year demand growth for FY2023 is estimated at 9.5-10%, which is likely to moderate in FY2024, though remaining healthy at 5.5-6.0%. India still meets 65% of its power requirement with thermal.

India’s dependence on thermal power is expected to reduce to 50 percent by 2021-22 and 43 percent by 2026-27 on the back of renewable energy (RE) capacity additions. India has the 5th highest installed thermal power capacity Globally.

The Indian power sector is forecasted to attract investments worth $128.24-135.37 Bn between FY19-23. The future of the sector looks bright since by 2026-27 the country’s power generation installed capacity will close to 620 GW, of which 38% will be from coal and 44% from renewable energy sources.

As of May 2022, India has a total Thermal installed capacity of 236.1 GW of which 58.6% of the thermal power is obtained from coal and the rest from Lignite, Diesel, and Gas. Share of non-fossil fuel-based generation capacity in the total installed capacity of the Country is likely to increase from 42% as of October 2022 to more than 64% by 2029-30. The private sector in the power industry in India generates 49.4% of the country’s thermal power, whereas States and the Centre generate 24.6% and 26.0%, respectively.

Advantages:

Discoms in several states is clearing the outstanding dues to the power generating companies through installments of 12-48 months with funding support from the PFC and the REC, following the notification of the Electricity (Late Payment Surcharge and Related Matters) Rules, 2022 (LPS) by the Ministry of Power. This will improve their financial profile.

Healthy growth in electricity demand (10.7% YTD) leads to higher demand for thermal power. Peak demand reached an all-time high of 216 GW in April 2022 against 203 GW in FY2022 & 190 GW in FY2021.

The peak demand is expected to increase to 225-230 GW in FY2024, with expectations of a sharp rise in demand during the summer season. Thermal generation reported a 9.4% growth in 10M FY2023 to meet the growing demand. Improved visibility on new PPAs; 4.5 GW medium-term PPA tender notified by PFC based on requisition from discoms.

The bidding parameter under this tender would be the tariff quoted, comprising fixed and variable charges. The variable charge component would include the cost of fuel and transportation. The fixed charges shall be revised annually to reflect 20% of the variation in WPI. The variable charges will be linked to the coal price notified by CIL/SCCL and the transportation charges notified by Indian Railways.

Higher prices in the short-term market; average tariff of Rs. 5.9 per unit in 10M FY23 vs 4.4 in FY22 & LT avg of 3.5/unit Realisation of overdues from the discoms under the LPS scheme .

Disadvantages:

Elevated international coal prices; negative for imported coal-based units without fuel cost pass-through Supply side constraints in meeting domestic coal demand which is why much of coal is imported.

The coal stock level at power plants is witnessing a gradual improvement, though remaining below the normative stock level of ~24 days. Stocking up coal before the onset of summer demand remains important to avoid any loss of availability or higher dependence on imported coal which is costly.

International coal prices have stayed elevated since the Russia-Ukraine conflict in February 2022 and the uncertainty in coal prices is likely to persist till geopolitical tensions ease. Spot power tariffs show a sharp increase in FY2023 over historical trends. 10M FY2023 price is at Rs. 5.9 per unit against the long-term historical average of Rs. 3.0 - 3.5 per unit and Rs. 4.4 seen in FY2022, owing to the sharp revival in electricity demand along with the supply-side constraints arising from the high international coal prices impacting utilization of imported coal-based units and the subdued domestic coal stock level.

3 Likes

Does this mean that, Demand for coal in India may remain elevated in FY23 and FY24 both?

e-Auction prices of coal have increased sharply during FY23, Is there a possibility that, those may not revert to Mean prices soon?

It looks like that Revenues of Coal India may remain slightly better than Pre-2022 levels during FY23 and partially in FY24 as well.

I am looking at it from both angles since invested in IEX and Coal India both at the moment.

Higher electricity prices is Negative for IEX volumes but might be slightly positive for Coal India.

I am new to both these stocks and may be wrong in my analysis.

1 Like

Thanks for sharing ICRA outlook. if Plant Load Factor (PLF) is expected to improve further, I think NTPC might be worth looking at this stage as operating leverage can kick in beyond a certain threshold value of PLF.

2 Likes

6 Likes

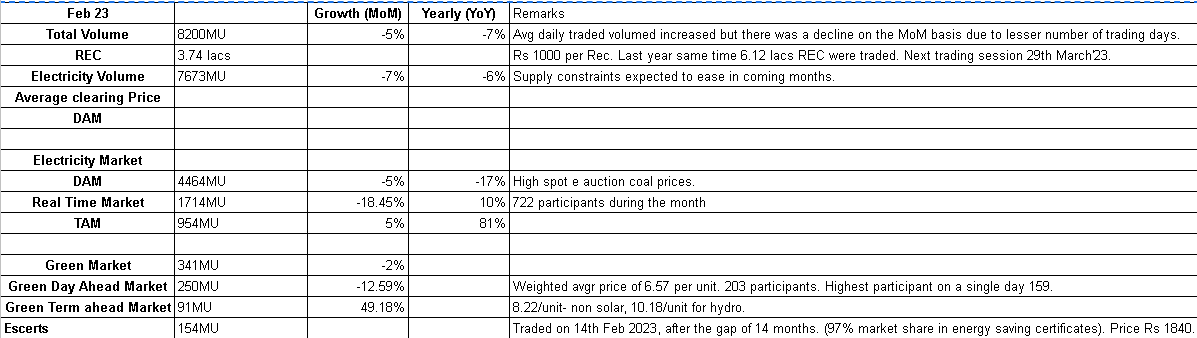

IEX Power Market Update- FEB 23

-

Shinning star this month is the term ahead market(intra-day, daily weekly, contract up to 3 months) in the electricity and green market. It has shown impressive growth.

-

Major decline in the overall volume due to a lesser number of trading days and high spot e-auction prices.

-

Positive point: Energy saving certificates have again started trading after a gap of 14 months. Renewable energy certificates trade only once a month while energy-saving certificates trade every Tuesday between 1:00 PM to 3:00 PM.

11 Likes

Sorry. If the question is not so relevant to the Thread here.

A recent approach I have taken is to buy a stock even if it has expensive valuation but is a damn good business. I start making SIPs into the stock even it goes down. When the stock reaches to my initial buying price, I sell the shares that I have bought initially at higher valuation. I then deploy that same amount into a different stock with same strategy. This way, my average buying price is less and I don’t miss out the chance of investing in a company which I genuinely like but was optically expensive in the first place. Is this approach good or is there any fundamental flaw to the approach?

The reason I am posting this question in this thread is that, Indian Energy Exchange is a damn good business with around 80% Operating Profit Margin. There are very few businesses in the world which are able to do that. However, with Yearly Sales of Rs.400 Crores and Market Cap of 13,000 Crores, the Price to Sales multiple is at 32 times which is quite expensive. So I am really contemplating to follow the above mentioned approach for IEX.

P.S: I know that the stock I have invested may take some time to reach my initial buying price after a heavy fall but I am ready to bear that opportunity cost. Investing for long term.

4 Likes

Some of the investors slowly increase the exposure to stock from initial 25% to 100%, as the stock becomes undervalued and become more attractive. This staggered buying approach ensures that, you get an opportunity to reduce your average purchase price as the risk reduces at lower prices, assuming that fundamentals are intact.

After this you should hold for longer duration so that when it gets overvalued, you can sell or you can sell in staggered manner as well.

Personally I have used the strategy of staggered buying to increase the buy position from 25% to 50% or some times 100%, but the time it takes to give meaningful returns is much higher than buying full 75% to 100% at low valuations.

If you are willing to hold the stock through the down cycle and also ready to hold for longer time, it can generate reasonable returns.

But if are ready to wait for lower valuations and then buy full 100%, and if you are lucky, and market turns around then you can get very good returns in 1-2 years as well.

Each strategy has its own pros and cons.

For fundamentally strong business, staggered buying or SIP might be good but not for all the businesses.

6 Likes

My Investment Hypothesis for the company

A Natural Monopoly and pioneer in the field: Around 95 percent of all the trades carried out in the country are carried out on IEX platforms, making them a natural monopoly in the field. They are the pioneers in establishing the electricity exchange in the country which provides them a great advantage over other exchanges. As the first mover in the field, they have the “Facebook advantage” basically the most number of buyers and sellers are on the platform, which provides the company a long-term moat that cannot be replaced easily. Not only energy exchange they just pioneered a gas exchange(IGX) which has over 95 percent trades of gas on exchange in just a year since inception, in the long term company will keep owning a 25 percent stake in this exchange which will be a cash cow for the company. In the past 2 quarter investors’ presentation company have communicated about the plans to establish a coal exchange as well.

India’s Per Capita Electricity is projected to rise 3x: India has the lowest per capita consumption of electricity in the developed and developing nations, which is bound to rise, some estimates put it to 3x by the year 2050, combine that with the government push to trade most of the electricity over exchanges, is going to be a great growth driver for the company. The amount of electricity traded in comparison to the European exchanges is very low(80 percent vs 8 percent), and this is bound to increase. 3x per capita production increase of electricity and 10x trading volume increase. The current trade volume is bound to increase in the next 5–10 years, and IEX will the leader even if the natural monopoly is somehow taken away but there is a high percentage chance that IEX will continue to be the leader, according to numbers provided in the very best case the current volume will 30x and I would say there is the good percentage chance of it being 15x which is still a huge number. Another way to put the total current market size of trades is around 400 cr, 30x of which is 12000cr, in the best case, IEX will earn 10000cr of these trades and in the worst case, they will make 5000cr per year, for years to come, it is astonishing to me how much money the company will make.

4 Likes

Great Thesis points.

But can you also elaborate on the Anti-Thesis points?

Also hope you have gone through this thread in details

Regards,

dr.vikas

2 Likes

“I never allow myself to hold an opinion on anything that I don’t know the other side’s argument better than they do” - Charlie Munger

Anti-Investment Hypothesis

- New Exchanges are coming up: There are two exchanges currently established and the 3rd one has just been given approval by the regulator to operate, of course, it will take away some part of the pie from IEX, so now we have three horse race, and much more exchange can come, as the opportunity is so big. This will have an impact on IEX business in the long run, the scale of impact isn’t clear though.

- CERC push to take away the monopoly: Of course, the monopoly nature of business is not good for any type of market and consumers as well. CERC floated papers regarding MCO last to last year which introduced will have an impact on the business, and we are also not certain what steps can be taken by the government or regulators and there are uncertainties around it as well. These regulatory changes will be huge for the market and until they are not implemented we cannot be sure what kind of impact will they have, we can be certain that if implemented there will be an impact.

PS: Of course, I have thought about all these aspects and there are a lot of details in the thread regarding all these things, I thought about it a lot before investing, but other than these two points all the discussion(I haven’t read all of it, but whatever I have read) is around short-term macroeconomics points or some short term news, I am not bothered about any short term news, macros or any other short view, the points in favor are much better then points in against. But yes, I would keep an eye out for the two points mentioned above and any new changes that I don’t see right now.

PPS: Follow Whatever Guy Spier has said about the company.

5 Likes

The key issue is that IEX is a commodity player. If Power prices are low, then offtakers use the exchange else they rely on PPA. Price of power is linked to price / availability of coal. Coal prices are dependent on domestic production/ international prices.

A couple of years back if someone had suggested that IEX is a commodity player, I would have shrugged it off. No longer.

Disc : Invested

8 Likes