Personally this sounds more of a wishful headline to me. Volume growth also has to be looked in the context of the expensive valuation (my personal opinion) and near to medium term growth potential. Average electricity price is still high compared to the guidance given by management earlier (<=3) at which they think traded volume growth shoots up.

Disclaimer: Have minor holding and watching closely before going big

Not bad, actually. Seems the current price already discounts this and the stock may do somewhat better. IGX volumes also seem to be picking up. I haven’t gone through the results closely yet, not sure if they report revenues for IGX separately or if they only report volumes.

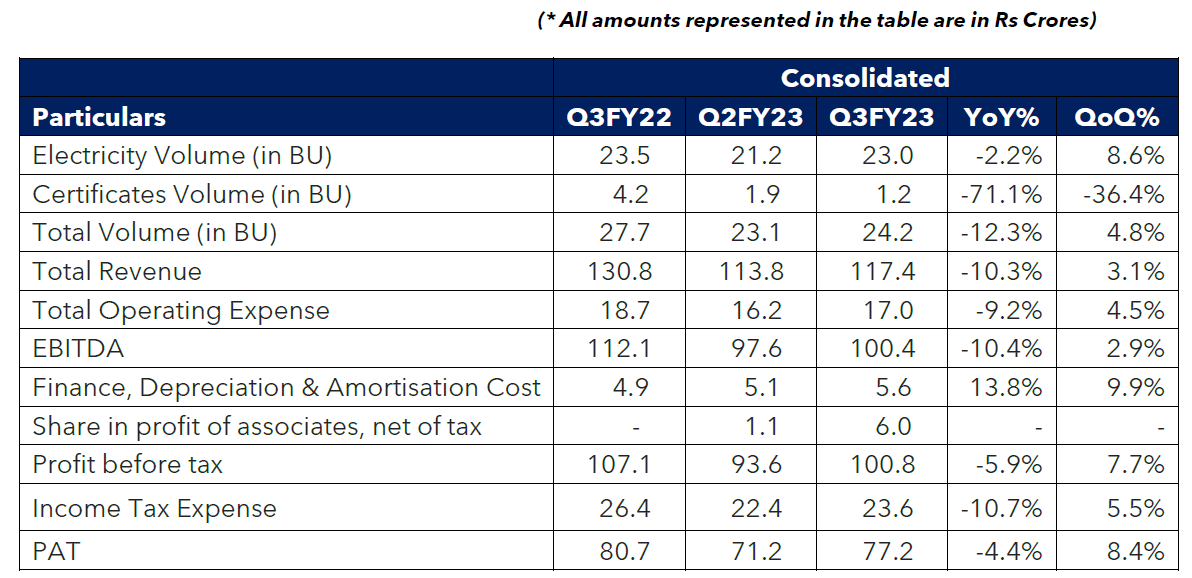

Q3FY23 result Update:

Indian energy exchange released its Q3FY23 results on January 20, 2023 sharing some of the key points from the same.

First of all a very detailed investor presentation of about 46 pages. For those who have recently started tracking IEX, recommending them to go through the same.

**The problem of high prices of e-auction of coal continued in this quarter as well. The electricity volumes witness a growth of 9% QoQ and a decline of 2% YoY.

There is a major decline in REC volumes. Last year There was a stay by the appellate tribunal for electricity for the trading of REC for the period of 16 months. Due to this reason, there was a pent-up demand in Q3FY22. Hence Q3FY22 is not a comparable base as far as REC is concerned.

As far as the Gas segment is concerned, segment revenue has not been disclosed for the past 2 Qtrs. On a volume basis, the company has disclosed in the investor presentation that it has achieved YoY growth of 568%. The current active clients are 120+, PAT is Rs 12.76 Crore which is 427% up QoQ and 1437% YoY. Also, the company launched GIXI which represents volume weighted average price for all gas traded on any day.

On a consolidated basis, revenue for the quarter increased by 3.1% QoQ, from Rs. 113.8 Cr. in Q2FY’23 to Rs. 117.4 Cr. in Q3FY’23. PAT grew by 8.4% QoQ from Rs. 71.2 Cr. to Rs. 77.2 Cr. with a margin of 66%.

This qtr company has incorporated a wholly owned subsidiary for International carbon exchange. Almost 500 million units of carbon credits are traded globally and by 2030, India will sell almost 200 million units of carbon credits with demand from corporates alone of 120-130 million.

Future opportunities/ growth triggers

Company working with the ministry of coal to set up coal exchange.

Also developing new products such as HP DAM and ancillary markets.

Coal prices expected to stabilize ( 100% FDI allowed for commercial mining, auction completed for 46 Blocks, Coal India Limited has offered 20 discontinued coal mines for reopening on a revenue sharing basis.

They guided that the company would be able to maintain their 5-year CAGR growth of ~20% in revenue, going forward if the market situations are conducive.

The management guided that the high prices of e-auction coal to come down after the month of August or September 2023, as in the summer season power demand is high.

IEX Forms Wholly Owned Subsidiary to Explore Business Opportunities in Carbon Market.

IEX is working with Ministry of Coal to explore options for setting up Coal Exchange. Coal Prices are expected to stabilize in the coming quarters.

Robust Volume Growth expected in IGX. As LNG prices moderate, volumes will increase. Launched Index GIXI for tracking of Gas Prices.

Has anyone done calculation of how much electricity we will need if 50% of passenger transportation will become electric. This can be a big tailwind for India’s power sector in coming decade and in turn for IEX.

The calculation would need total passenger Kms driven annually in India and how much power would be needed.

Well, this would be additional capacity and that you’d need to have higher transformers and substations. Imagine 10 cars in a high income flat complex in 1 tower trying to charge their cars overnight. that’s 80x10= 800Kwh; there’s no way any electric infrastructure is in place or planned for a city grid wide loading of this sort.

That is not to say that it is not possible, just that we are some way off in building such infrastructure.

Model Inputs:

1/ Vehicles that can be easily electrified - 2w, 3w, 4w (PV + CV short haul cargo).

2/ Conservatively let us assume 50% of all the vehicles above will be EV by 2030.

3/ Current vehicle fleet in operation, and growth rates.

4/ Current average annual KMs driven by each vehicle category above and growth rates.

5/ Average battery size, charging efficiency, and mileage for each vehicle category.

6/ Charging pattern for each category, commercial owners might charge twice a day while private owners may need to charge once a week.

If anyone can help with sourcing these inputs, we can work on this together as a community.

This is interesting discussion and good to see some projections.

Considering that, electricity demand will rise, how is industry planning to meet this increased demand? If the cost of electricity starts moving up rapidly due to shortage, it might adversely impact IEX volumes as we have seen this year.

If the increased electricity demand can be fulfilled easily then the charges per unit may not shoot up and it might help IEX volumes.

There are some news in Mumbai that, all companies are already planning for substantial rise in charges per unit. So keeping electricity charges at moderate levels seems to be a challenge at least as of today.

India’s coal minister said at the end of 2022 that the country has no intention of ditching coal from its energy mix any time soon. Addressing a parliamentary committee, Coal Minister Pralhad Joshi said that coal would continue to play an important role in India [until at least 2040]

referring to fuel as an affordable source of energy for which demand has yet to peak in India.

Anybody can explain what is happening with MBED and MCO from CERC, as per management discussion during the meeting with the UBS analyst, they said and I quote paraphrasing “We are not hearing anything about MBED framework, it is a long-term and hard to implement change, State government are against it, GOI can’t ignore State government on this matter as they are ones who will need to implement it, they heard something back in April 2022, nothing after that, even if they start today it will take 2 years at least to implement”. Someone with any insights around the topic can help?

MBED means Market Based Economic Dispatch. This is basically a proposal to have a centralised clearing house that will sort all the sources of power and dispatch the lowest cost ones, thereby lowering cost of average power nationally. But this would theoretically impinge on the Electricity Act and independence of discoms which are state owned. Hence the view by IEX that it is hard to implement and get the states onboard.

Thanks, @Intrepid_Captain, Got it why state governments are against it, can you please help me understand why MCO is necessary for implementing MBED, What is my understanding of it is the settlement of trade will be removed from the exchange and a centralized organization will be formed for price discovery and settlement, Can you please comment on MCO and its effects on exchanges.

Two interesting developments and potentially some good news for IEX -

Govt allowing the expensive power to be sold via exchanges using a separate product for the power produced via imported coal and how a regulation to mandate that such plants generating electricity from the expensive coal to run at a full capacity and sell on exchanges.