IOCL Bought 4.93% of IGX as per todays news. Adani Total Gas,Torrent Gas,NSE and now IOC have bought into the company. Interesting developments.

7 Likes

Is there any chance higher competition will reduce Margins? Any news regarding new platform created by BSE charge less tariff per KWh? Currently IEX charging 40 rs per kwh

This is bad , ideally u would want to own 100% of it to reap in maximum benefit as a shareholder and may be divest in future when its a mature company to extract maximum value out of it.

They are bound by the regulations of the governing body to offload a significant stake in IGX. That was always going to happen. IEX’s stake in IGX shall be further reduced to around only 25 Percent in the long term.

“The gas exchange regulation also requires that we bring down the Indian Energy Exchange (IEX) equity to 25 percent within five years. That is what we will do in five years’ time. All equity partners, who are from the gas sector, can only hold 5 percent in the exchange. If there is someone who is not trading on the exchange, he is allowed to hold more than that.” - MD,IGX

2 Likes

Govt eyes 25% power purchase in spot market. Probably good 1.5 years away.

6 Likes

Correct , thats why its not something to cheer about , IEX will be a minority holder in IGX long term growth story ( value it by keeping holding discount on minority stake in that)

In an interview to CNBC on 24/12/21, they said their target is to achieve 100 bn units mark in 2021-22, if IEX charges 2 paise each from buyer and seller, means revenue could be around 400 cr for the entire year, which is ok considering first half they have already done 200 cr, however, what was the number of units transacted in fy2021…? anyone please

2 Likes

IEX_Results.pdf (1.7 MB)

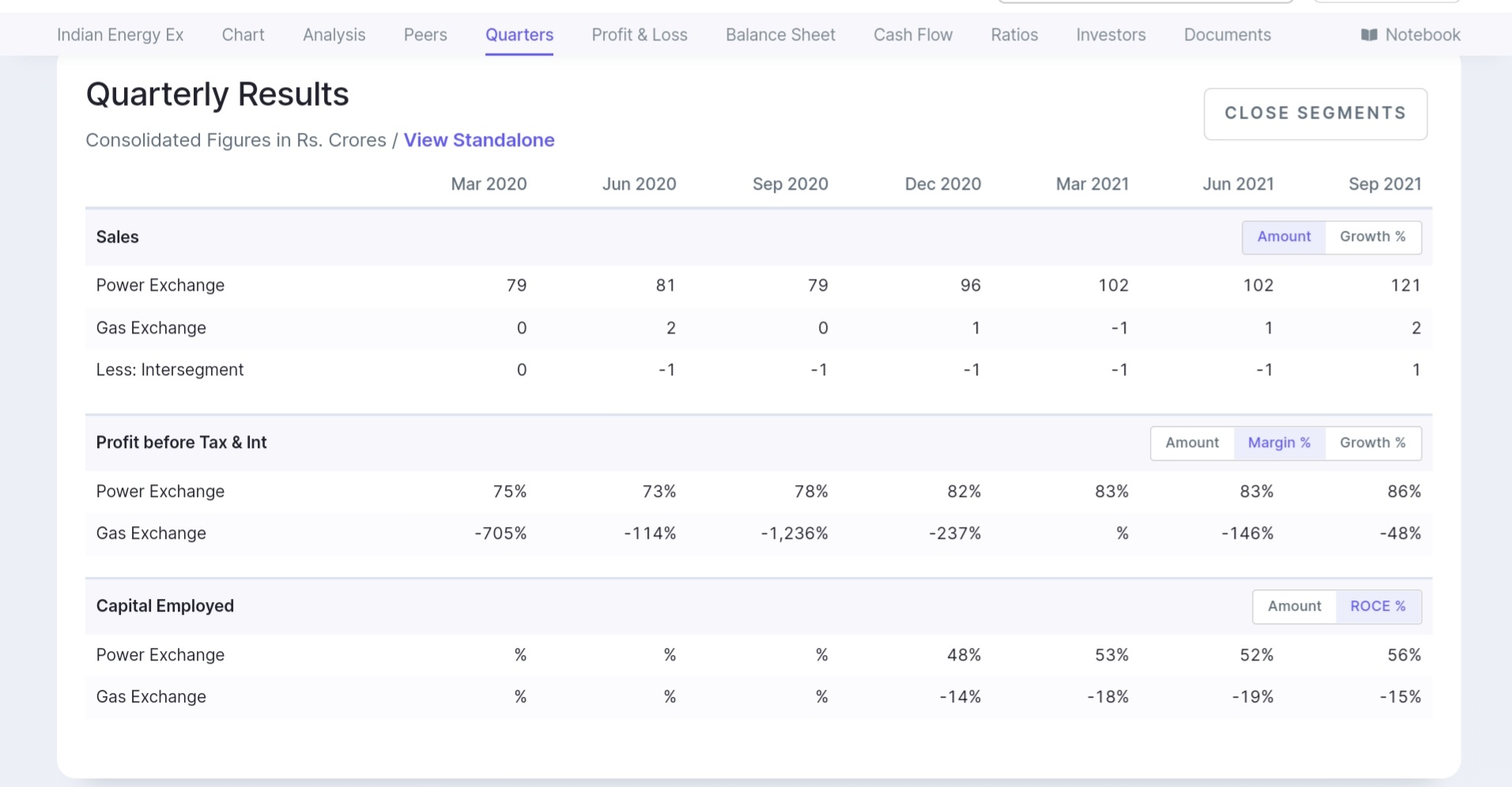

Page 40 of their investor presentation says they did roughly 74 billion units cleared in FY21 so a growth of 35% for the year.

4 Likes

- Opportunity size 4X by 2025. ( exchange share of this year is at 6.5% and planned to go to 25%)

- IEX is 90%%+ share on exchange driven volumes, and debate is on weather they will lose mkt share - IMO the future is hockey stick growth for exchanges, should be the case for IEX as well

- Renewable is focus - multiple green products launched and more in pipeline including med term ( up to 11 months which was not the case till now)

- RE surplus states and large players are supplier on their platform, given good traction for them due to better realization of excess capacities - one can think of humongous RE capacities being built and Policy push to build it - this vertical is likely to see exponential growth

Valuations

- They have done 226 cr topline( H1 21 at 161 cr) and PBIT of 189 cr ( 116 cr in H1 21)at consol in H1 22, I.e. 40% top line and approx 70% bottomline - operating leverage will keep kicking in as revenue grows

- H2 on similar lines can deliver approx 250 cr+ top line( 177 cr) and PBIT of 230 cr( 136 cr H1 21)

- FY22 at 475 cr+ revenue and 420 cr PBIT, at 24% tax we have a PAT of 400 cr approx - current mkt cap is 22K cr

- FY 23 this core biz will continue at healthy pace( may moderate over FY21 to FY 22 pace but still be healthy)supported by increasing volume on exchanges( 50%+ CAGR if exchange share has to go from 6.5% to 25% in 4-5 years), renewables will add upside, IGX losses will come to profits - can simulate for mkt share losses if any but doubt it in near future.

IEX represents non linear growth opportunities with optionality - which are getting favorable policy and Market dynamics support - near Monopoly atleast for near future ( mkt share losses will be visible if at all that happens to some extent). We are lucky to have access to play such story in listed markets at reasonable valuations wrt to opportunity size - unlike most of quality IPOs which are quoting at 20X -30Xsales+ for similar growth at cost of far fetched profits , leaving no margin of safety and rerating for retail folks.

Risks of regulatory aspects are there but power policy ambitions need IEX to do what it is good at doing now hence IMO no meddling in near term. Could be wrong but IRCTC meddling and immediate rollback tells something.

Invested from lower levels

16 Likes

For some references related to energy policy and increasing % of short term contracts.

Discl - tracking

I have one question.

one of competitor for IEX in electricity space is PTC india. They are coming with their own exchange which will be launched in Jan time frame. Don’t you think, IEX fundamentals has to catchup with IEX stock price.

IRCTC is exception… But govt is not promoting monopolies , so there can be some hurdles for IEX . These are some of anti-thesis I had … So, please share your views.

No position. Currently evaluating bet IEX and PTC.

There is plethora of information in thread on why should IEX continue to do well in spite of new /existing competition. One should build own views though

Would be better to think in terms of

-

Can marketsize for power exchanges grow exponentially as proposed in policy push to get spot markets to become 25% in next few years from currently 6.5%.

-

Can IEX continue to hold efficient price discovery advantage( thus higher market share)with larger number of ecosystem particpants getting higher value

Valuation are very subjective, IMO its quite long term opportunity

5 Likes

6 Likes

6 Likes

#IEX interesting SHP… Dec2021

FIIs 37.74 → 31.01 ( - 6.73 %)

DIIs 23.13 → 17.66 ( - 5.47 %)

Public 38.81 → 51.02 ( + 12.21 )

5 Likes

Usually when Fii and Dii participation decreases and retail participation increases, it is followed by a fall - is that what you are implying?

I am not implying anything my friend. I am just sharing this information as it seems intresting.

4 Likes

yes. if FII and DII is not increasing interest in the business with current valuation then we retail investors must double check the thesis. Am I missing something. please help

1 Like

One can assume this contributing to float increase, as FII and DII’s concentration is getting lower, which will eventually add to volatility to both sides.

3 Likes