Estimated revenue from transactions is up 84.6% for the FY till April end as compared to the same period last FY. Revenue has been supported by DAM, RTM and G-TAM volumes.

DAM - On a cumulative basis, FY22 volume and estimated revenue till April end are 54.4% greater than revenue in FY21 for the same period.

TAM – On a cumulative basis, FY22 volume and estimated revenue till April end are down 17.7% compared to revenue and volume in FY21 for the same period.

There have been no REC transactions since June 2020.

RTM – RTM continues to be a strong revenue generator. RTM volumes grew by 4.2% MoM after having grown 26.4% MoM in last month’s update.

G-TAM – GTAM grew 262% after having dropped 43% MoM, in last month’s update.

FY21 estimated revenue contribution break up:

DAM – 74.2% (-)

TAM – 4.2% (-)

REC – 0.0% (-)

RTM – 19.2% (+)

GTAM-2.4% (+)

CERC Short term market update (January 2021 report):

The short-term market witnessed a 35.4% rise in January compared to the same period last year while the long-term market witnessed a marginal uptick in volumes of 1.9% in the period. The overall market growth rate was 5.4%.

IEX’s DAM market share has continued to stay above 99.8% in January.

While IEX’s TAM market share has been under pressure from 90% in March 2020 to less than 20% in September 2020, the steady recovery since then has continued and reached above 45% in January.

No REC transactions have taken place.

IEX has a 100% market share in RTM for the sixth consecutive month.

Any idea why the difference exists? The other numbers are an exact match. Something to do with contract tenure based calculation? (guessing it’s a calculation issue, because I assume both the numbers aren’t incorrect).

@ankush12495 - For starters, pretty insightful article! Good stuff in there!

Just had some questions, hoping you could answer them:

Banking Transaction - Not sure what Goel meant by this offering. Can you help understand this financing instrument better, may be with an example?

You mention that “government is also looking to move a proposal wherein everyone would have an option to choose their power supplier” - This means that new private players could come up who would want to source electricity efficiently for distribution and for that, they would go to exchanges, correct?

Can you help understand, how hedging using derivatives will help increase short term volumes? Wouldn’t hedging be generally for a long period of time to cover for the possible variables / volatility?

On MBED, the value proposition to Discom is that they can reduce the variable cost component of power by procuring from exchanges. Even if they continue to incur the fixed charge, overall they save right? However, then how will generators recover their capital cost? Unless the fixed is aimed at just that. Also, one thing that always puzzles me how will investment flow in this sector if there is no commitment and if everything is short-term? May be what Goel said is that base load requirement will be under PPA and the rest will be on ST market?

On PTC risk - The risk is that PTC can move all or part of its volume from IEX to PXIL or the third exchange coming up right? Don’t think this could instantly happen and even if it did, it would phase out over a period of time I think. Also, I think Pre MBED the risk is quite high, but post MBED, once there is uniform price discovery across exchanges, then IEX could still retain some piece of it based on either the buy side or the sell side by collecting 2 paise per unit?

Let me try to answer your second question. In the western world a customer is free to choose their supplier. You go and find the cheapest deal on any aggregator sites and take a lock-in contract. That is about customer side. From the supplier side , it is easy for anyone to go and set-up their retail power trading business ( I can see loads of suppliers , 99% of these are neither into energy production , transmission or distribution , only major players like British Gas, Eon Energy, nPower etc… , rest all are retailers, they buy the energy on the trading platform and then sell to retailers (this is my layman understanding )

Example : Bulb energy was setup by an expat Indian in UK

Are we going into that direction? I think yes, but is it really going to happen soon ? I doubt, in India it is one of the commonly used goodie to win votes. Power supply and pricing is states matter, until governments give up this I don’t think something will really change so soon.

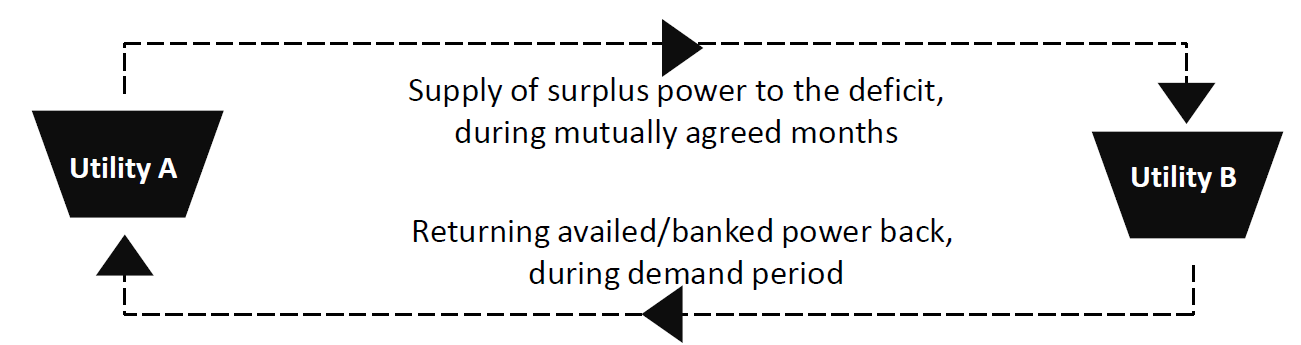

Banking Transactions-

Currently the way banking contracts between discoms works is that if a Discom A has surplus capacity for few months of any year and deficit for some other months and then you have Discom B who is into a similar position but in reverse, then they enter into an understanding that they will swap power during mutually agreed months. So it is basically barter of some sort without involving cash payments.

What IEX is trying to do is, they will provide discom an option to hold their sale proceeds for them during the month of surplus, which a discom can then use to buy power during the deficit months.

Yes, entire power distribution space will basically open up for competition using the infrastructure of existing discoms. Like how in CGD, post exclusivity new players will be allowed for atleast 20% of the transmission pipelines.

Currently, participants on the exchange are hesitant to keep a large part of their requirement open to be met through exchange because they are not sure what would be the price of the exchange, 1 week or 1 month from now. Exchange is based on market dynamics and prices vary every day. But once everyone gets an option to hedge this price risk through derivatives, they will be open to keep a larger share of their requirement open for being met through exchange.

I think this plus, ability of exchange to offer long duration contracts of upto 1-year would be a key pivot in increasing the share of short term market from current 10-11%.

India currently has >370 GW of power generation capacity with annual generation of ~160 GW, so we have a lot of excess capacity currently. But we still do have investments flowing into generating assets because in a competitive market, there will always be more efficient players looking to offer their offerings. I had mentioned in the blog that share of STM depends on the kind of power market structure that India takes up. Under MBED, exchange will facilitate 100% of trade, but market will still be split between Long term PPAs and pure STM market.

Will strongly recommend you to read the MBED draft to get more clarity on role of PPA in such model.

See it all depends on what incentive PTC has going to other exchange. Will 5% stake in the new exchange be enough for it to do that? I am not sure, will have to see. It will take another 1-2 years for new exchange to be operational and that is a good enough time to explore this risk, which is what I am currently focused on in case of IEX.

You are right that having states involvement makes it difficult to implement changes.

But I think that things are different in case of power because, no state makes any money of power distribution. They all rely on center to make it work. Plus, Electricity is a part of concurrent list, so center has the first say in it.

Recently you would have seen the case of online MSP transfer for wheat wherein Punjab was not ready to implement the same. Center has supposedly said to Punjab state that if they don’t implement the same, they will stop procuring wheat from Punjab. So crux is that if states rely on center for something, they have to accept their policies.

In case of Alcohol and Fuel, I will agree it will be extremely difficult to get states to agree onto something because, both these areas are big revenue generators for state.

I basically think that IEX will be like say CRISIL in rating business. It will be market leader with good margins. So maybe the early entry in stock will help in long-term capital appreciation.

Also I think this will be a GREAT dividend story in coming years as not much capital required for technology upgrade ( compared to other capital intensive businesses like coal, oil, renewable energy, gas, metals etc)

Its perfect INDIA Growth story.

Of course, my views maybe biased at I was lucky( thanks to Mohnish Pabrai) to enter this stock around 120 ( & now aveg buying price is 200)

So my plans are to hold this one for my retirement which is around 20 years away.

My personal Opinion.

Regards,

Vikas

That’s the risk. Govt is also apprehensive of a monopoly in this segment. So future developments can have an effect on IEX.

However, IEX’s technology is much superior than other exchanges. IEX’s management is also smart, they are engaging with other quasi government entities for IGX and building relationships with them and allowing them to invest. As an investor (even through quasi govt entities) the govt gets a vested interest to build and evolve the platform.

Share of trading volumes from PTC should go down in future from the current 50% as IEX enhances long term contract trading and more discoms start participating.

I view PTC risk for IEX on the same lines of a manufacturing company having 50% of its sales to a single customer. With time IEX is gaining more customers and this % of sales to single customer should reduce.

Its already a great dividend story, you seem to have entered around the same time as I did. My avg. buy price is somewhere around 160 though. Quarterly dividend yield for me is around ~1.5% (~6% yearly) on this investment and the dividend is just going to keep growing from here on now.

PS: Such a dividend yield is not possible at current price.