Q1FY21 CCT Notes

Regulations

Changes in interstate transmission charges, losses and REC floor and forbearance prices. Will benefit the exchange market trading. Will put exchange transactions at par with the interstate. Will incentivize the DISCOMs to optimize power purchase through exchanges.

Shakti Coal scheme will allow generators to participate in coal linkage auction even if they sell power in DAM or DEEP. Will boost sell-side on exchange. They will have market prices in both coal procurement and selling power.

SEBI and CERC have resolved their conflict of jurisdiction of new power products F&O. This will provide longer hedges to clients. Delivery based contracts on power exchange will be under CERC and derivatives under SEBI. We have already designed the contracts, will move to approval from CERC. Hope to launch in Q3.

PMR (Power Market Regulation) has just come out, we will be responding to it shortly. We believe CERC with MOP is working to create a very robust and transparent power market. All the discussions on the regulations front we believe is being done with the view to streamline operations for an exponential markets growth. If we were to have such growth today, the market could have challenges because certain operational structures need to be put in place. The draft also allows for the introduction of new product enhancements without approvals. As for market coupling, there is a vision involved, discussion with all parties, and the decision will be made for what is right for the country, the most effective design, the best process. As growth happens, they need to give it some streamlining.

Fee - In OCT-18 we got approval from CERC for our fee, any changes need to be approved by CERC. So there is no change in how we were functioning already. It has just been formalized.

The markets will have many new products like long-duration contracts, cross-border, green TAM & DAM. The operational requirement from technology, people is different for different products.

MBED - Directionally MBED and Market Coupling could be our route. Volumes on the exchange could be skyrocketing. Direction would be that all volumes get to the exchange to ensure efficient price discovery. The regulator is looking at what others have done, what is best for the country, and we are also helping in that. Coupling for just 4% of the volumes has little relevance because they are already coupled. This is not the reason for coupling, you would see then the whole operations, we would launch new products, we would make the whole system far more robust and then on top of that, we will get to a volume, which is unprecedented so I think that would be the way in which the Ministry would want to go for a plan.

Financials

PAT growth would have been 18% if not for one-offs like 5 cr to PM CARES and 2.6 cr to last year’s tax liability. Volume traded saw 14.5% growth yoy.

Invested 15 cr in technology.

RTM

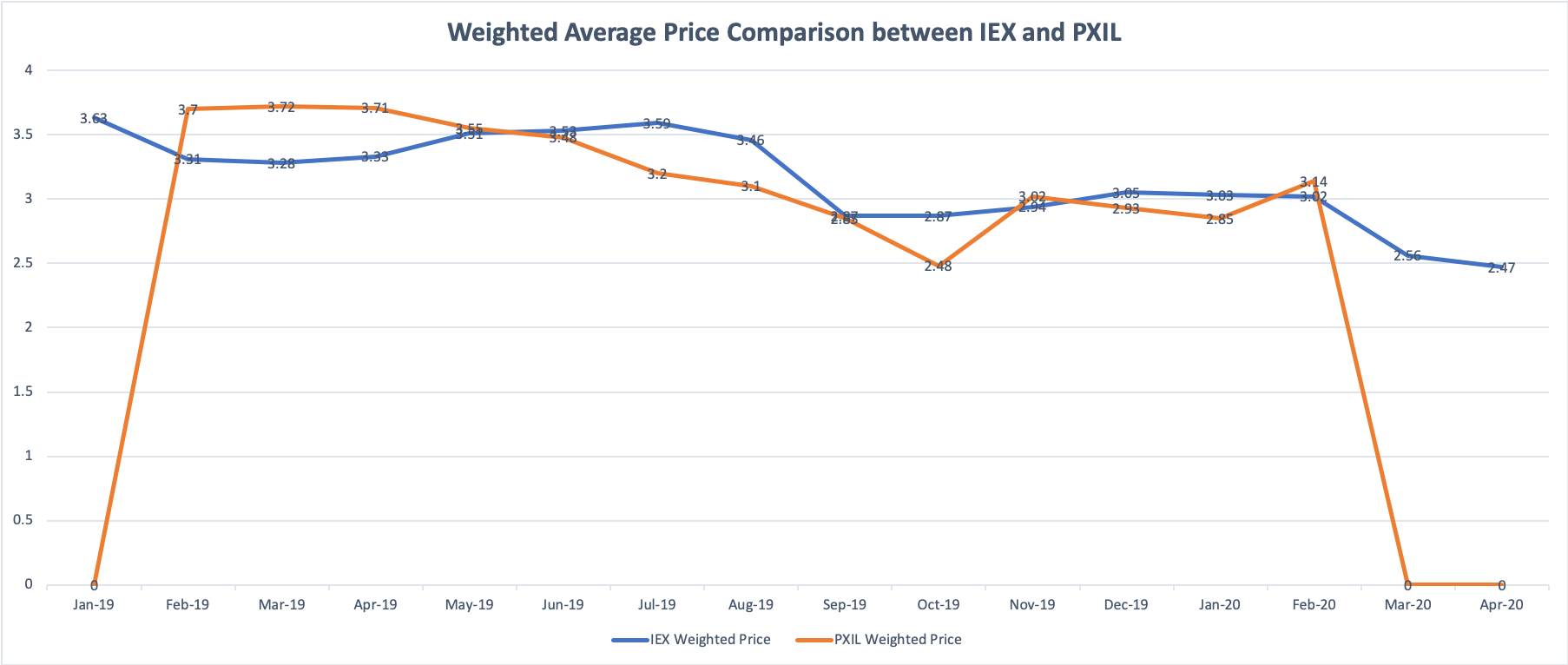

Makes up 10% of total volumes of IEX in 1st month. RTM has affected 80-90% of the intraday market which was 2.5 hrs in advanced and now is 1 hour in advance. Have not seen any cannibalization in DAM yet but not ruling it out.

Derivatives Products

Seeing the need for such products as DISCOMs dependence on such market is increasing and they want to hedge. Delivery based contracts will be launched in IEX as there are no regulatory hurdles. For the pure financial products, we will need to form a new company, details of which are yet to be finalized. We will take a few weeks to decide on whether to partner with some other exchanges, we are not constrained from a holding co. perspective. There are different routes to go to market for the derivatives, and then whenever these are to be delivered the delivery happens on IEX. We will maximize delivery, derivatives and future. There are limitations to holdings of pure financial exchanges. Different players are doing well in their segments so there could be some partnerships in the future.

In mature markets derivatives play a signalling role. The dependence on the spot has increased and one needs some financial product to support. You are transacting more and more in spot and you cannot keep all your positions open. In global markets derivative’s volume is 10x of spot delivery.

Forward markets currently on different platforms is at 20 BU. There are some interstate transactions which are forward in nature, they are not included in this 20 BU. This volume is in bilateral. Trading licensees are participating on behalf of DISCOMS and IPPs and represent both buy/sell on most occasions. In future, it would be done on our longer duration contract platform, which is an extension of TAM, from present weekly to monthly, quarterly and annual. It will not be closed double-sided, exploring reverse auctions.

Double-sided auctions are good for liquid markets, here in forwards we may see a few sellers and fewer buyers, price discovery may not be optimized. In an open auction, you can revise your bids seeing other party’s bids.

We will play a big role in derivatives because for delivery they will come to us. We are exploring the index product and its sub-segments. It is still too early to comment. They will be cash-settled but those that go for delivery will come to IEX.

IGX

We want strategic partners in the exchange. Have sent our proposal to GAIL’s EOI. We have other proposals from other gas players as well which we are evaluating. Will share more in the next quarter. We would like to keep 51% holding as IEX is a neutral player, and IGX should be seen as a neutral entity. We are in talks with the regulator who may not allow such high holding, fair market regulations allow 26% for a player in the market and 5% if you are a member.

PNGRB has proposed a cap on holding to 15%, not 26%. Exchanges should be allowed more than 26% as they are neutral entities. We are in discussions. A final decision has not been taken by PNGRB, one is to let exchanges hold more than 26% the second discussion is to allow time to reduce below 26%.

Coal

Cannot answer on other energy baskets right now.

Future Growth

There is a huge range of products which are coming in. Now to take the part as a reference for the future growth of these markets as a starting point, it does not give you enough analytics because over time every buyer would want to play in the whole basket to figure out what is the most optimum and most optimized procurement program for themselves, so each one of them will do that so that would be the way in which the whole buying partners will evolve across the market because right now we are also seeing the same thing happening in the movement of TAM where the RTM has been launched. You are seeing people making trade-offs between DAM, TAM and RTM which is what is happening and so they will come to an optimized procurement model and the same thing will happen in many, many, more ways and think of it there is a three, four more products getting launched, people will start to figure out what is the most optimized procurement.

Products Strategy

All these products are required, to balance the surplus and shortage from other products. LDC (longer duration contracts) will be for adjusting seasonal impacts. Within the ST market exchanges have grown the fastest. The ST bilateral and DSM has shrunk.

Selective Q&A

Dwelling on your previous comments on this price coupling thing, which is already existing in the market how do you protect your turf now given that some of the feedback that we received, they did mention that price discovery has been tough given the liquidity is entire with IEX especially in the DAM and RTM market so can the other players now enter if the uniform pricing mechanism comes in going forward, so that is question number one and secondly on the transaction margins again the draft regulation speak about separating the three functions which are price coupling operator, the exchanges and then clearing and settlement mechanism, so these three functions are being separated out, so can we still continue to defend a 2 paisa margin and the other functions will get hived off like the European exchanges have, just wanted to check your thoughts on the same?

On the separation of the clearing settlement functions from the exchange, look first of all it is done that way across many exchanges in India as well as globally and the unbundling will be linked to facilitating this sort of growth and from an IEX perspective we clearly see this as a very strong great business opportunity, we run a perfect clearing and settlement process right now, it is flawless, if we were to settle it down as a 100% own subsidiary of IEX we will do that, it is just the functional separation and then what it does Abhishek is and that is a great point. What it does is it allows you to do many other things with the clearing and settlement function including the OTC provider there is a provision which is coming in the PMR it allows me to explore pretty much other potential business opportunities to set up a clearing and settlement function for anybody else who is setting up an exchange and there would be many such opportunities possible because the commodity trade business in India is at an early nascent stage and it is only going to grow. I think we see that as a tremendous opportunity for IEX to step up and capitalize on such a brilliant provision that the regulator is trying to think of and create so we see that as like it is absolute progress.

On the market coupling front now the reason I said that it is a coupled market right now because the electricity market is currently 4%, we are pretty much all of it give and take a percentage point here and there, so your objectives of coupling in terms of getting an accommodative price that will make sense because you cannot make more than that or your element of getting any more social maximization done again it is all of us so you are getting a complete social welfare maximization that we can get in this. Going forward if the design and the way we are trying to work on the design, it is a design that allows a huge amount of volume to be flushed through the exchanges, which is what the overall design of that I think it will reach the underlying current business in the PMRs and the fact that overtime there would be a talk in the business, if you get all that risk then there is bound to be a tremendous escalation in the volume that have to flow through this mechanism of business model and in that sense there will be more exchanges, there should be more exchanges, there should be more places because you are wanting more efficiency to come into the whole segment, then you are wanting people to go down and do much more work at a business development level, sell more different kinds of products even though innovation might be comprised, but we sell more different kinds of products, you go and sell on the fundamental element of your user experiences all as well so there is a tonne of innovation, which is possible in this whole thing and there will be a huge amount of growth like I said, which is being envisaged and in which case it is a tremendous benefit for everyone all across in the new model, which is going to come in, but like I said I think there is a huge amount of work to be done to get the capacities and come up with a most right sort of a business model a framework which will really deliver for a country like India. There are no models across the world right now where price coupling has been done and volume coupling that I can get. Price coupling is a completely different thing, so we have to make sure that we arrived at the best exchange model.

Source: https://www.dropbox.com/s/l0xj1dbrltud6rc/Q1FY21.pdf?dl=0

PS:

MCX Comment on Electricity Futures in Q1FY21: As to colors to electricity features contract that is the power ministry has come out with a circular or note or whatever it is you call it saying that these are the activities that CERC is responsible for these all the contracts where SEBI is responsible in the case of electricity products and both of them will work together to put the framework in place. Once the framework is in place then they can start doing that by that time and it is all said that it is subject to the approval of the Supreme Court where the judgment is pending and once that is done probably we are good to go and on our part we are in advanced stage of discussions with IEX for using their prices and for designing our products.