Any thoughts on the NFO of Motilal Oswal Nifty India Defence Index Fund? considering the strong and optimistic growth story of the Indian Defence sector.

1 Like

They are releasing this fund, because this is the flavour in the market. every fund house has 100s of funds, that does not mean, they have done their research on this. if every AMC has their XYZ fund, then no one can be left out, they have to compete and bring the same XYZ fund.

2 Likes

Customs duty exemption on import of defence parts extended for another 5 years

The move will enhance output of defence equipment/ machinery. The beneficiaries will be all defence equipment manufacturing companies

India can not become atma nirbhar bharat overnight it is a gradual process. Till that time we continue to.import parts to increase our output and export value added products or fully assembled products.

For example , Prachand helicopter engine by HAL has currently 45% indigenous content and aiming to increase to 60%

1 Like

What can be proxy benefactors of the move by the government? Can anyone throw any light on it?

1 Like

The beneficiaries are clearly the companies those who are importing some components/parts that goes in to manufacturing defence equipments/ assemblies / sub-assemblies / finished product.

Which means not only the front line defence companies like HAL, BEL, BEML, Bharat dynamics , All 3 defence shipping companies, Midhani , Bharat forge, etc ,

But also the ancillaries to these front line companies could also be the beneficiaries if they are importing some components to make their products they supply to the front line companies as above.

1 Like

Hi, can you share list of front line, defense shipping, ancillaries companies? as you have highlighted in your comment.

Thank you very much.

2 Likes

already HDFC defence fund is active in the space, and entry of more players gives validation to the sector and leads to brighter prospects

1 Like

The listed front line Defence shipping companies are Cochin shipyards, Mazgaon Dock, Garden reach ship builders.

The other front line defence companies are BEL, HAL, BEML, Midhani , Bharat dynamics , Bharat Forge, Solar industries, L& , Paras defence , Idea forge.

Ancillaries are those who are engaged in supplying parts , components , assemblies, sub- assemblies , Software , hardware , telecommunication system, EMS to the front line companies.

Some of them that comes to mind are Astra microwave, data patterns ,Cyient DLM, Kaynes, DCX systems, Avantel,. Mtar, Apollo micro systems , Taneja aero space , Sika interplant, Zen Technology

The above list may not be comprehensive.

If someone can add to the list please if you find it is left out

5 Likes

https://www.screener.in/company/compare/00000085/

Hope that this helps.

1 Like

It is not only a “Self reliant / Atma Nirbhar Bharat Play”, But , the Govt has set an export target of 50,000 crore for exporting to its friendly countries.

These companies are unique and near monopoly. Defence of our nation is top most priority of the current govt and budget for defence spends can not be neglected.

They have exempted customers duty for import of some critical components for defence equipments , which India is currently not able to produce.

in order to increase liquidity in the market, the Govt/ promoter of front line PSU is gradually coming out with OFS for Defence PSU front line stocks “where the Govt stake is very high”

So considering the future prospects, more AMC’/ MF 's are likely to add defence stocks to their portfolios

3 Likes

2 Likes

Hello, everyone in this thread seems to be bullish for this cycle of defense sector rally and as we have seen in past overly bullish approach in any sector leads to disasters.

I will try to present my thesis as to why I think the valuations at the moment are stretched and very little to no valuation comfort lies which is contributing to a dangerous euphoria.

Defense Sector Red Flags:

- Indian defense sector is in itself at a nascent stage.

- We come no where close to the defense RnD spend done by countries like US, Russia and China.

- Defense sector in India is highly concentrated and dependent on govt. funding no private players exist which can give competition to big names such as HAL, Mazgaon Doc.

- Sector requires high capex before any additional set of revenue can be turned into profits.

- Intensive RnD lead sector.

- Since dependence on govt spending is key sector demands high growth in GDP to defense expenditure YoY.

- Govt policies have a strong say in spending and procurement of defense equipments, a coalition govt in centre may not be able to continue with the old growth plans although in the current scenario this is unlikely. A strong opposition also might scrutinise the defense deals leading to delays.

We will be looking at listed companies which are directly involved in making of arms, ammunitions, armoured vehicles, aircrafts, ships, frigates, UAVs, night vision devices, missiles, launchers and avionics.

The prominent listed companies along with their p/e and p/bv are: (P): PSU;

- HAL (P) - 46 ; 12xBV

- Mazgaon Dock (P) - 44 ; 14xBV

- Cochin Shipyard (P) - 42 ; 12xBV

- Bharat Electronics (P) - 56 ; 14xBV

- Data Pattern - 93 ; 13xBV

- Paras Defence - 182 ; 13xBV

- Taneja Aerospace - 141 ; 13xBV

- Bharat Dynamics (P) - 96 ; 16xBV

- Krishna Defense - 153 ; 14xBV

- Zen Technologies - 26 ; 5xBV

- DCX Systems - 60 ; 4xBV

- Bharat Forge - 85 ; 11xBV

- Garden Reach Ship Builders - 73 ; 15xBV

On current valuations the

- Avg pe: 84 vs historic avg pe: 32.3

- Avg p/bv - 12xBV vs historic avg p/bv: 4.5xBV

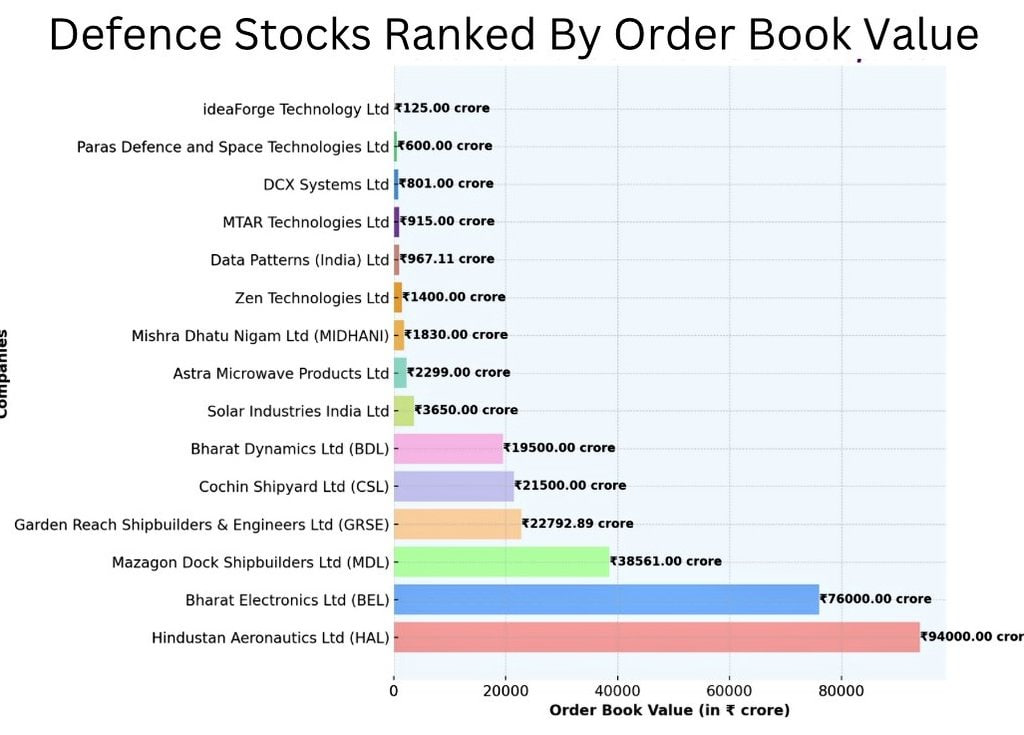

Apart from these very basic valuation metrics the order book scenario of major defense companies are below, these numbers are usually thrown around on the internet to show potential upside in top and bottom line, while this might be true in a bull run investors are often

A lot of these companies especially companies working solely in defence manufacturing are dependent on each other for components and survive through orders given to them by a bigger vendor. This poses a serious problem because if a bigger vendor is late on its payment it will have a tinkering down effect on the smaller players. Mutual fund houses also have recently launched their defense funds which is signalling exuberance in the sector.

The problem with order book led stock rerating is that while a 94,000 cr order book look monstrous from a bird eye view it might not be as attractive when the execution is done over a period of 2-3 years. Order book concentration is also something to be cautious about since a few orders in the pipeline may boasts the majority of the revenue posing a longevity threat.

What is important here is to look if the companies are going to substantially increase their revenue YoY while maintaining their margins, equally important is their profitability. Since the street tends to pay for the actual EPS growth when the froth settles down it would be dangerous to bet on stocks which tend to over estimate their growth in the next 3-5 years time frame.

Assuming all of the order book is executed on time without any operational delay and assuming the payment from govt comes on time and more new orders are procured we seem to be over paying for a lot of what these stocks are worth for.

For eg: Paras defence order book is 600cr at a market cap of 5561cr the mcap/orderbook comes close to 9.

15 Likes

It is always good to have contrarian views.

Views on valuation of stocks differ from individual to individual. In my view Nobody is right or wrong in stock picking. That is why for every seller, there is a buyer at any price and vice versa.

The Market which is a collection of intellectuals who finally decides the price of a stock depending upon company’s fundamentals, financial performance, earning visibility in terms of order book.

Mr Market is always right, though at times it may behave irrationally. But then it corrects in due course. I have been watching , whenever the market corrects, defence stocks remain resilient and whenever these defence stocks correct, it is bought in to by investors.

Further, we cannot compare historical P/E with current P/E of PSU’s. History remains as history. I have been closely watching PSU stocks performance for the last 3-4 years.

PSU’s never had the kind of order book currently they have which only increases day by day which ensures that there is an earning visibility for the next 5-6 years or even more.

Execution wise , PSU’s have shown remarkable improvement as reflected in recent financial performance.

So, clearly During the Modi regime , there is a structural shift in PSU functioning.The PSU’s remain in focus of the Govt. There is a heavy Capex happening and the clear beneficiaries are the PSU pack and many Pvt corporates are also getting the benefit of the heavy Capex allocation to defence , railway , infra and most PSU defence companies are unique business with a strong moat at least in Indian context.

I agree that India’s defence sector is at its nascent stage as in the past it never got a chance to grow. Now that it has started getting the attention , this can grow faster provided the Govt walks the talk - not only Atma nirbhar Bharat but as an export hub too where India has just got 1% market share in Global market.

If I look at the entire stock universe, no stocks are currently trading at a cheaper valuation than PSU stocks if we compare recent Quarterly performance and earning visibility due to order book for next 5-6 years. And apart from that these companies are debt free, minimal corporate governance issues, no Tax raids , no balance sheet manipulation issues. Regular and decent dividends from psu stocks is only an icing in cake.

My take is that as long as there is a govt policy continuance, order inflow remains strong, execution quality remains good , and it is reflected in financial performance , the defence PSU stocks may continue to remain in demand and may remain in the limelight…

I agree that some defence stocks especially in.pvt sectors have moved up very fast beyond fundamentals. And I am sure market may correct in those cases whether it is PSU or Pvt.

10 Likes

1 Like

Excellent analysis and providing a healthy debate opportunity to all of us, otherwise mostly reading positive about defense sector everyday Vaibhav bhai.

I think all your points are valid. But PSU are performing really well, they have good order value for sure. And a bit cheaper than private companies.

And yes, few companies are not in healthy situation. Over valued.

My personal opinion. HAL is a solid company, quite old, very good experience in this space. And have good PE (lowest among others). One can target this company. I am sitting on a good profit, will add more on every correction.

BEL BEML - highly volatile companies, lots of ups and down. I have purchased this stocks a while back, so on a healthy profit, but will not add more.

Mazagon - good attractive PE - will add more. Also government will issue OFS, so we may see correction, but it will bounce back.

Cochin, Garden - news specific movement.

I have minor holding in Zentech, netweb, kaynes, nibe. Will keep them for few years.

I think from a long term perspective, this will be a good bet. Government will not be able to afford any kind of mismanagement or blunders in this space. But if current government goes - sell everything!

(I am invested)

4 Likes

Thanks to Mr Basu Mallick who initiated this thread in May 2022. After going through his first introductory post which was an inspiration for me to start my investment journey in Defence stocks.

Those starting points of Basu mallick in his first post in 2022 are stilll valid today and if we see the financial performance of defence companies, the Govt seems to have walked the talk -the FDI automatic route, defence acquisition council, Atma nirbhar Bharat, Exports potential to name a few- all are playing out very well…And it is not only the PSU defence companies - even the Pvt corporates both Large and MSME’s engaged in defence sector are doing well.

The recent announcement of extending custom duty extension for 5 years for import of parts / components for defence equipment manufacturing for next 5 years is another incentive for increasing output of defence equipments.

And recently the govt giving a export target of 50k for defence sector (the defence PSU’s are now seen to be on their toes) where we have just 1% market share in international defence market which is currently dominated by developed countries.

Apart from exports contribution from HAL & BEL, Bharat dynamics , now all 3 defence shipping companies apart from their obligations for meeting India’s defence needs , are now targetting building of commercial ships for exports which has huge potential as western countries are looking for replacing their ailing fleet with new generation ships to run on cleaner fuel like green hydrogen, Ammonia, methanol etc.

Here is a you tube presentation from equity masters on shipping stocks.Tanushree of equity masters gives a warning on Pvt shipping stocks.

Discl: Invested from lower level for long term Hence may be biased. not a buy sell recommendation. please do your own assessment before buy sell.

Defence PSU carry risk of policy uncertainty. If govt cuts defence budget , stocks may decline or crash. so it requires a lot of caution before investment at current level

1 Like

Current defense sector mania is very similar to infra mania in 2000’s, basically same wine in a different bottle. Low free float in PSU defense stocks is a cherry on top and adding further fuel to the rally. Marketcap/sales ratio of PSU shipbuilding stocks is obnoxious, even higher than high ROE, sustainable growth sectors like IT, FMCG.

Management of Mazagoan, GRSE have mentioned in concalls that they are likely to see peak revenues in FY25 or FY26 and they see 20-25%CAGR revenue from FY24-FY26. This shows that current order book size while large, the execution will happen over a period of years and peak growth is more than factored in current valuations.

Like infra, defense is also cyclical. Apart from may be HAL, Midhani, BEL, its important to note that R&D spend, IP of Indian defense stocks is nothing to boast about. In case of most companies, most of the technology is insourced from Indian entitities like DRDO, or some foreign entity.

7 Likes

It is good to have a healthy debate and contrarian views especially when we put our own money in stock market with an aim to get some return and healthy debate may help us to correct our thought process.

In my view and what I have seen in my investing career, Every sector is cyclical in nature in stock market. There may be very few specific stocks without being sector specific which may have given consistent returns in every cycle.

Once , FMCG was thought to be non- cyclical. now it is found it is not.

IT is no longer non- cyclical. It is cyclical now as being seen last few years

Pharma once thought to be non- cyclical, it is not so. it has its own cycles

Steel , cement and all commodity all are cyclical.

Energy power is cyclical as it depends upon overall industrial activity and overall economy.

so, basically all business are cyclical as it depends upon capex & consumption , demand and supply which many time we try to balance.

Now coming to 2000 infra boom , what was the capex?? It was 0.5 % of GDP and that also was not actually spent due to lack of drive and initiative at that time . it was just not sufficient to drive the infra sector. So infra companies did not perform well and so also the infra stocks.

During 2023-24, what was the capex as % GDP? And what was the capex in interim budget of 2024-25 as declared on Feb 2, 2024.?? you will get the answer from the following links at the end of this post !

Not only the capex was fully utilised last year fy 2023-24 , it is reflected in order book position and financial performance of infra companies.

And still manufacturing has to take up and has a long way to go, given the capex push during Modi 3- a lot of PLI schemes , renewables , Atma nirbhar Bharat , Railway capex mega plan , enhanced defence budget allocation and export of defence products to international market are under implementation.

And yet fiscal deficit was still maintained at 2000 level and still the govt trying to reduce.

The Govt walks the talk.

So , my take is that as long as the Govt initiatives continue with mega capex push , there is no reason why the infra, defence would not do well.

So for infra , capital goods , defence , railway , it seems to me has a long run-way for growth.

Valuation of stocks is something , I am not an expert. But what I have seen whenever there is a froth in the market, the market tries to correct downwards And if the market finds under-valuation in stocks , it corrects upwards. It is natural. And if there is some black swan event , then everything falls.

I always tend to believe what the realities are and the way market move is the collective decision of an universe of intellectuals.

Edit 4 July 4.45 PM

Interim budget 2024-25: Capex raised to 3.4% of GDP despite fiscal consolidation

5 Likes