Hi, Can any one help me understand, what makes Kotak bank so lucrative to command a much higher PB as compared to lets’s say even HDFC bank. I agree it is smaller than HDFC however I don’t believe it is as well managed as Hdfc.

Any specific parameter you see that makes Kotak bank to command that valuation.

Is it the ROA vs ROE ratio.

That it is less leveraged and has lesser cost of fund and higher spread. Retail business share. Steady growth, I read higher growth is not always good for banks

However does it makes it that lucrative to command that higher premium.

Just trying to lean, I am very new to investing.

Thankyou in advance.

Should corporates & new banks be teaching IndusInd on how to run the bank?

Sometime back, IndusInd Bank refused to publicly declare its total exposure to the ILFS Group. Fortunately, good sense prevailed, and it disclosed that it had a Rs 2000 cr exposure to the parent company and Rs 1004 cr exposure to the SPVs. There is merit in the argument that the SPV’s are operating companies and the haircut will be minimal, if any.

However, what doesn’t cut ice is IndusInd’s handling of its exposure to the parent company. The parent company is only a holding company with hardly any assets and a standalone debt of around Rs 16,000 cr as on March 2018. It is generally believed that recovery of exposure to the parent will be minimal, if any.

Sensible corporates like Symphony Limited and Apollo Tyres have taken a 100% write off on their exposure to the parent. Even a newbie bank like Bandhan Bank took a 100% write off on its exposure to the parent in the December 2018 quarter itself.

Surprisingly, IndusInd has decided to take only a 70% provision on its Rs 2000 cr to the parent. No prizes for guessing why. If it decided to take the additional Rs 600 cr provision, it would have reported a loss during Q4 & it would have seriously dented its profit for FY2019.

Exposure to ILFS parent (Rs crore)

Provision taken

Symphony Ltd

21.5

100%

Apollo Tyres Ltd

200

100%

Bandhan Bank Ltd

385

100%

IndusInd Bank Ltd

2000

70%

While it is the prerogative of the bank to decide on the level of provisioning, it is a sad moment for a bank celebrating 25 years of its existence for corporates & newbie banks to guide it on how to run a conservative ship.

South Indian Bank was in limelight few years back when some US based investors along with others bought significant stake in the bank.

I am suprising now at 1800cr valuations what are the factors that changed their mind set !

Does South indian Bank will come up with bright future ahead?

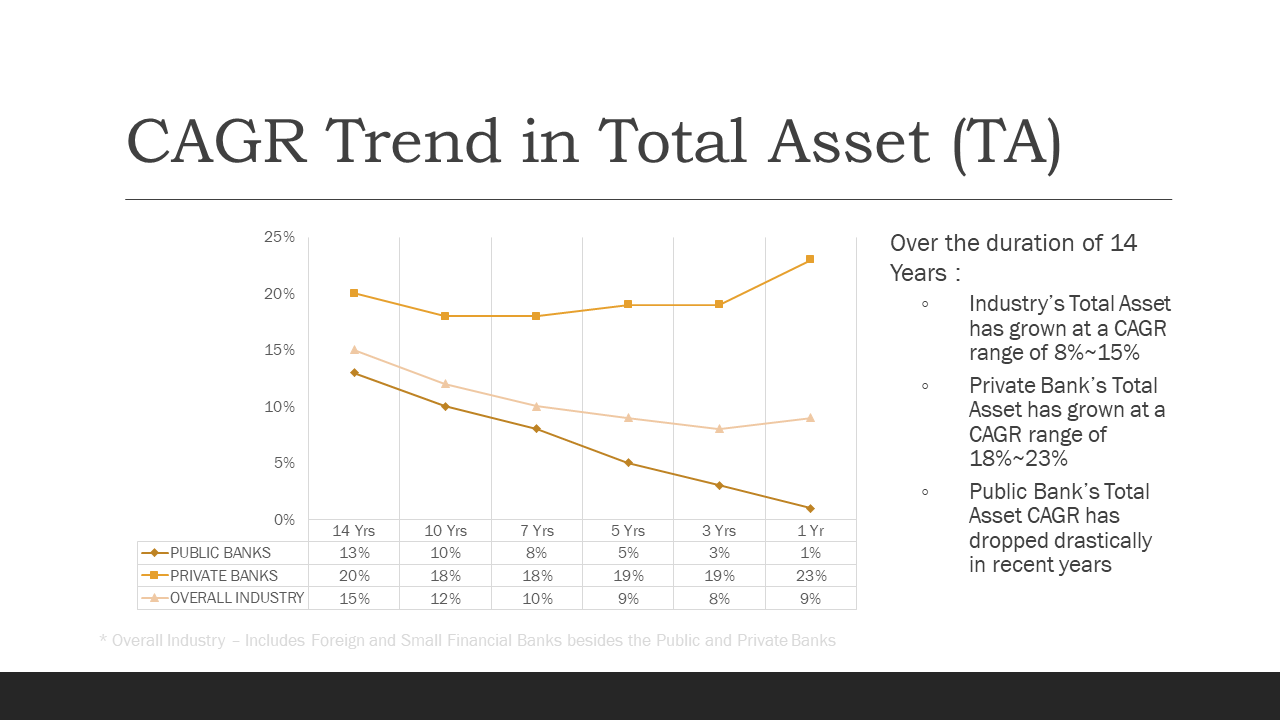

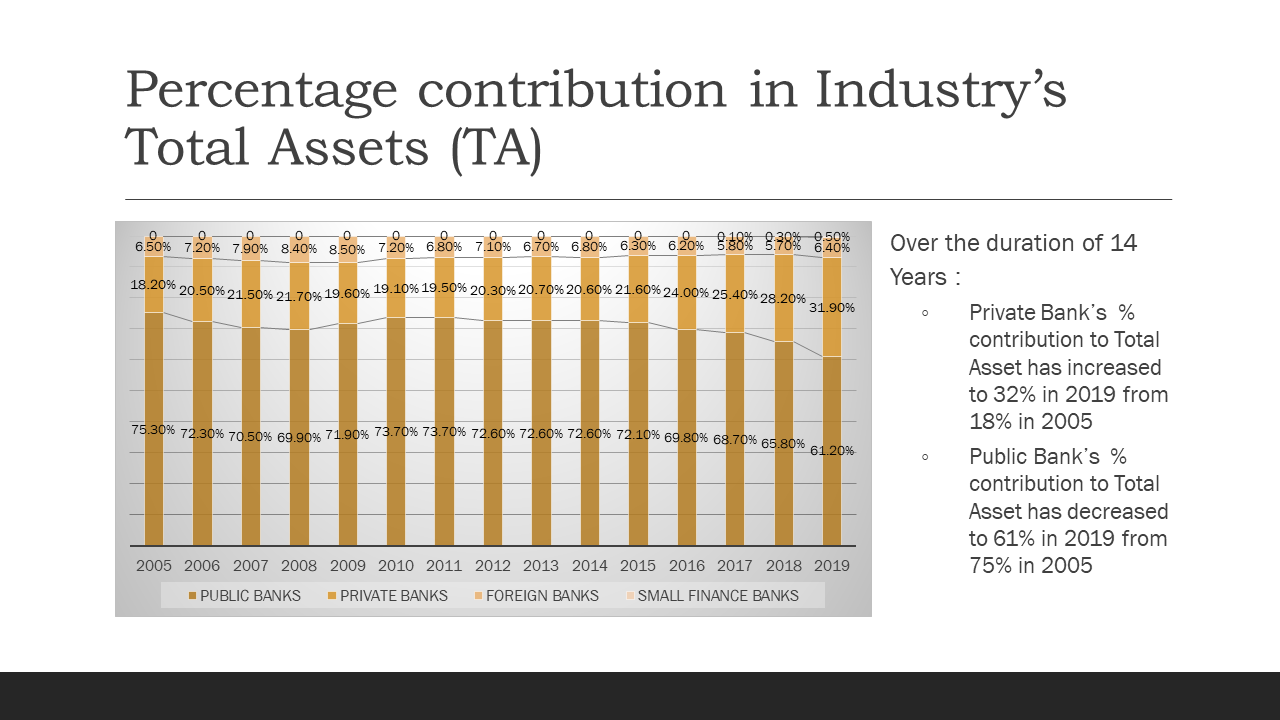

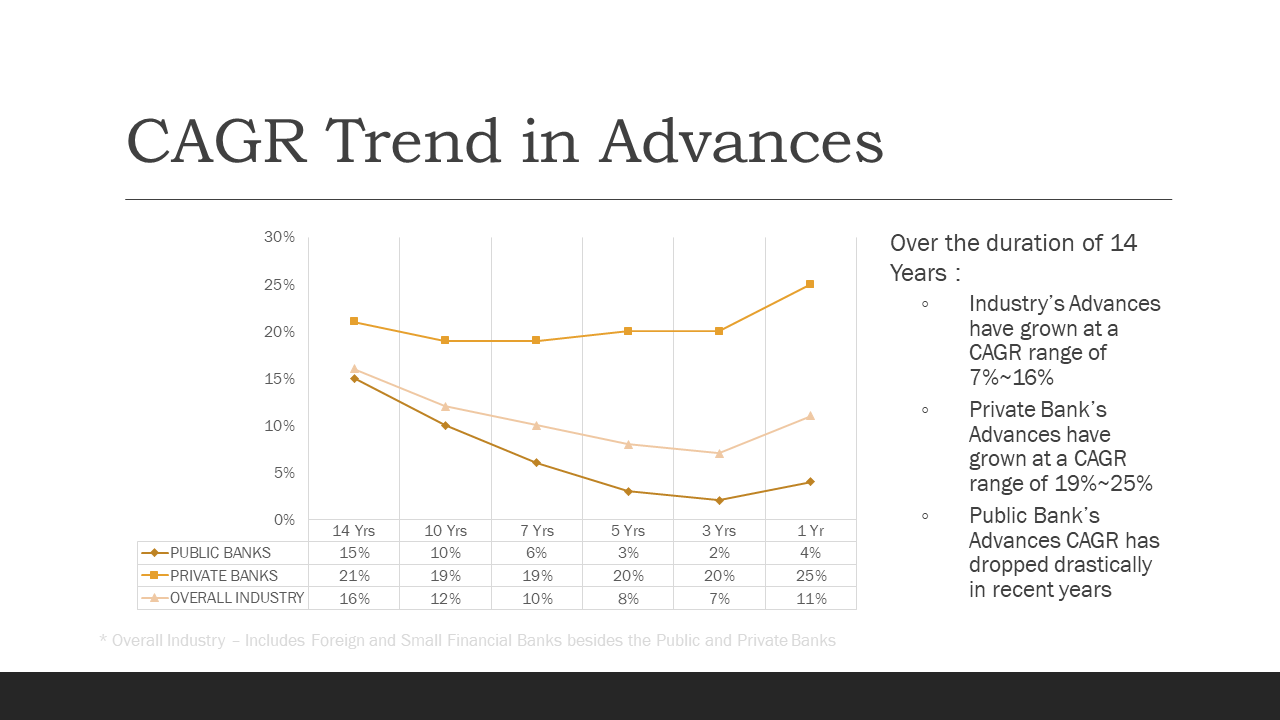

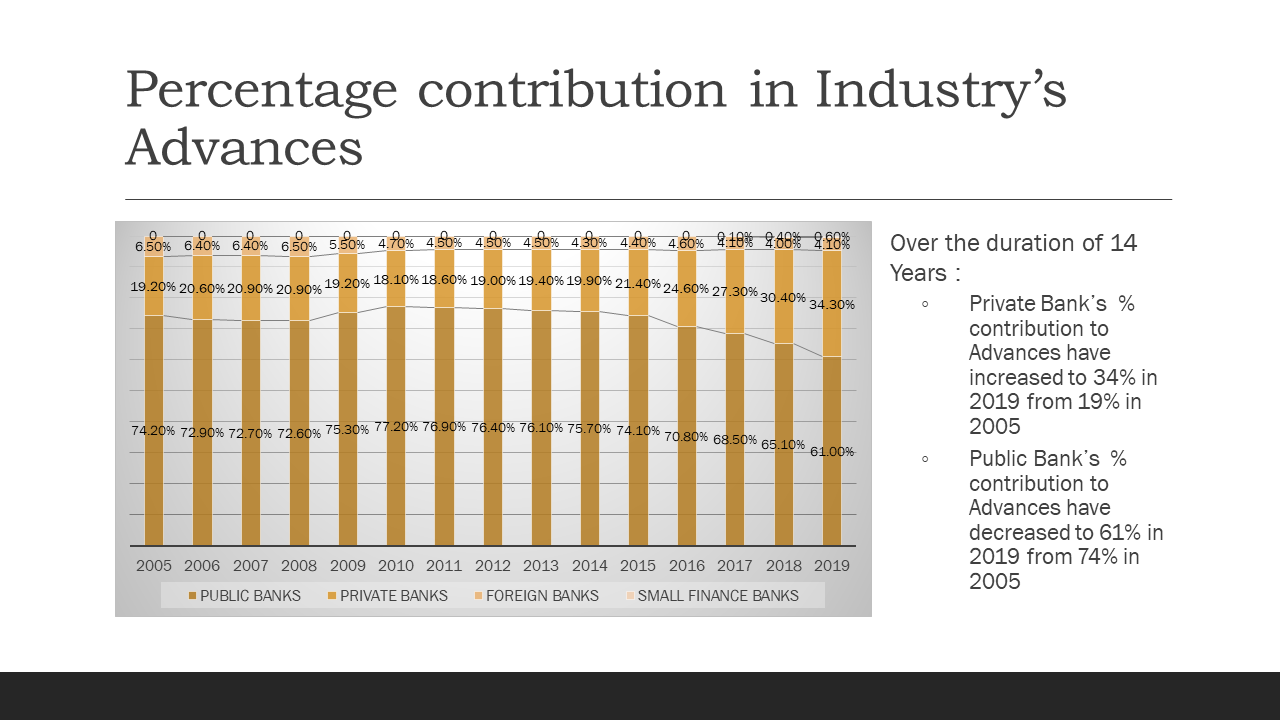

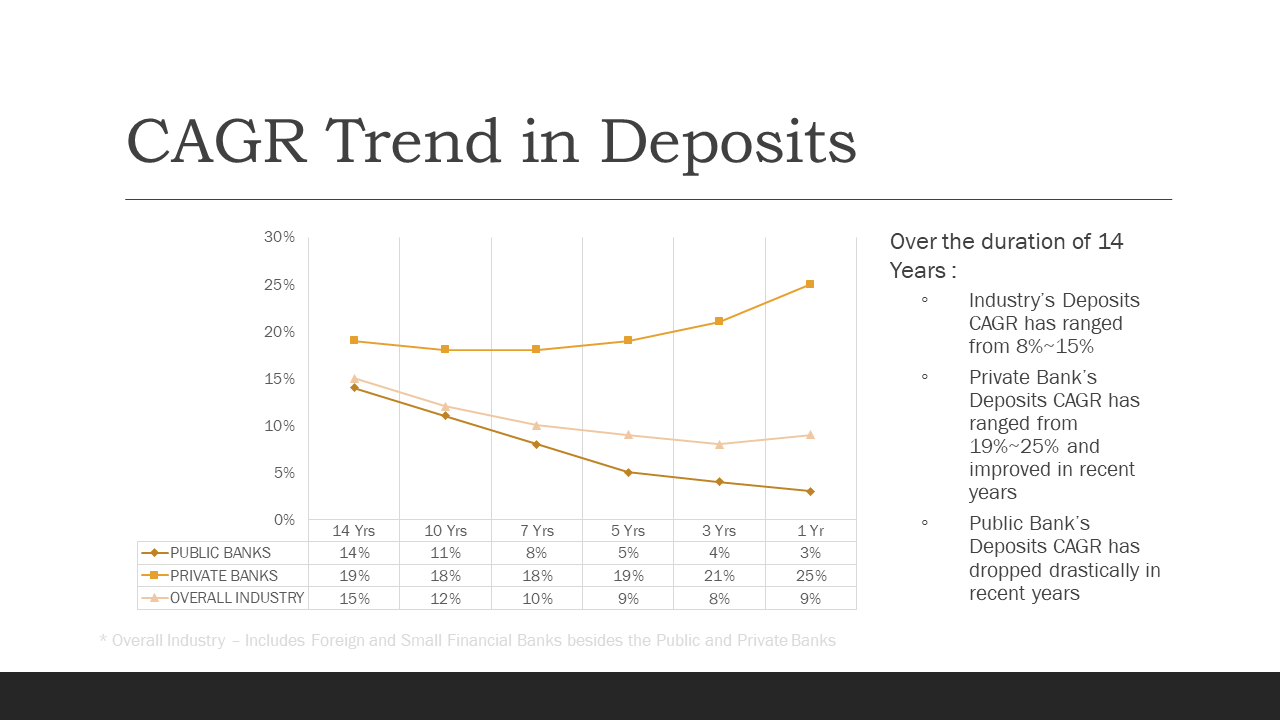

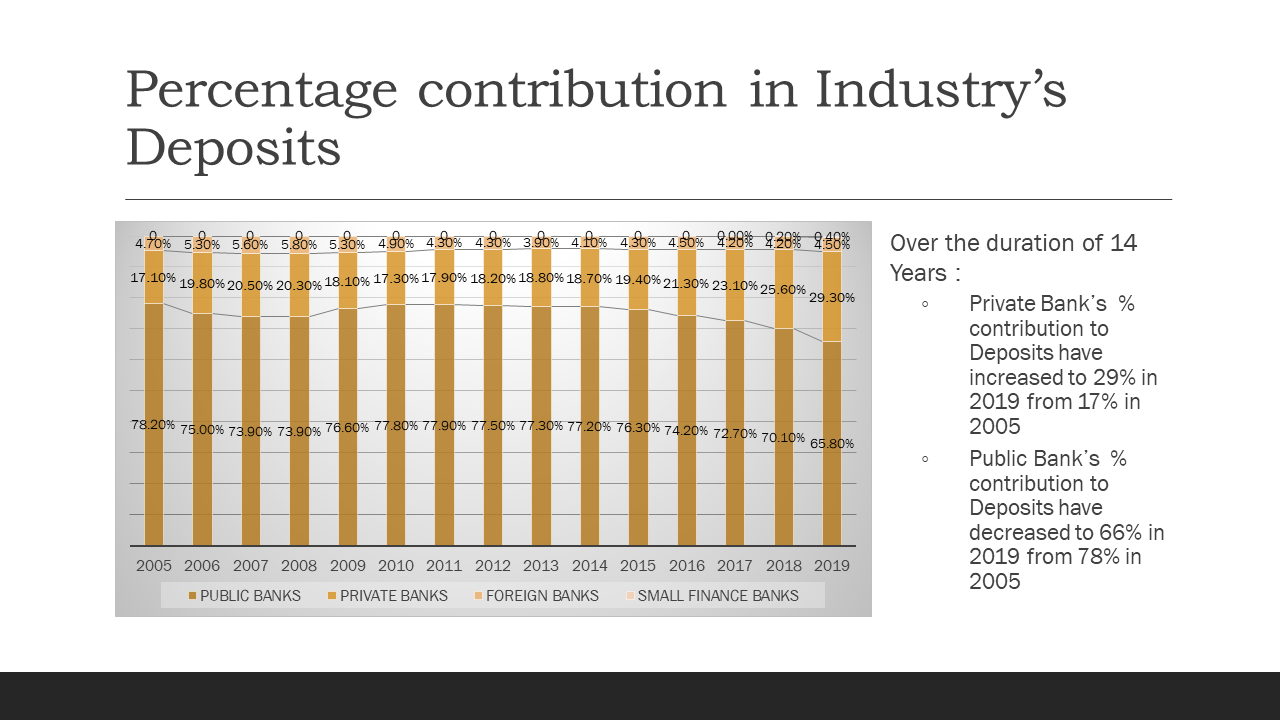

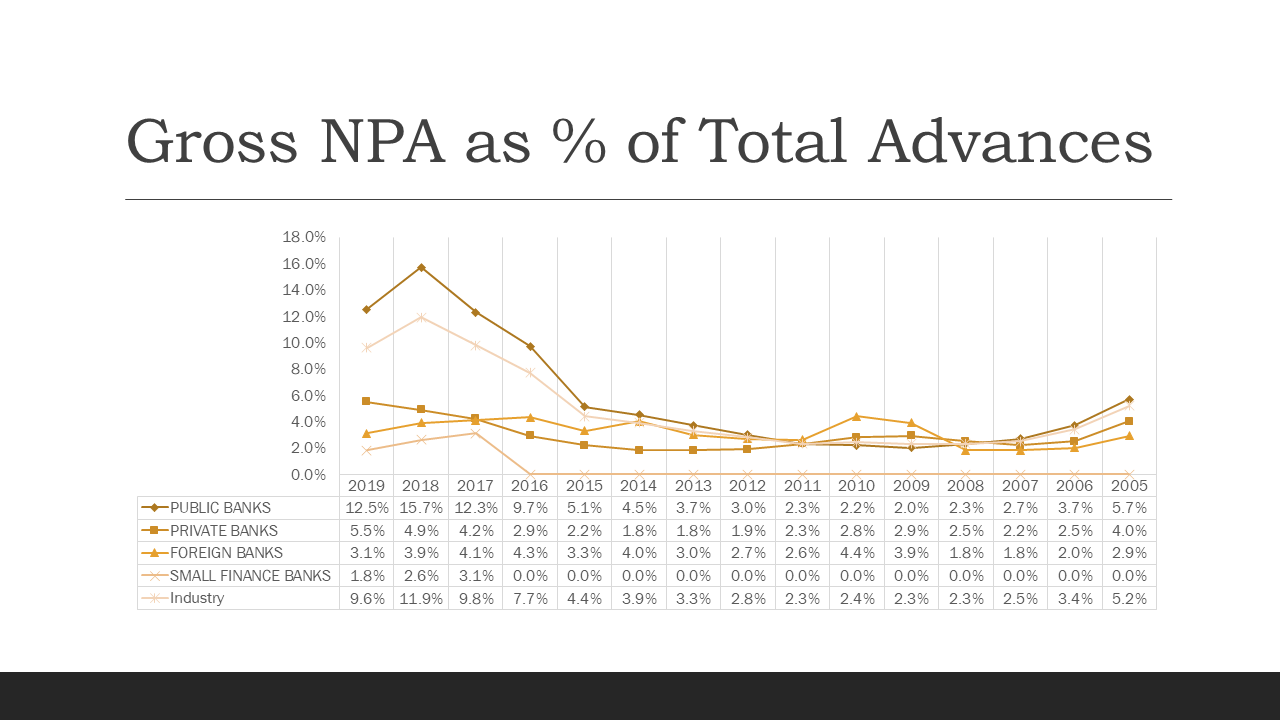

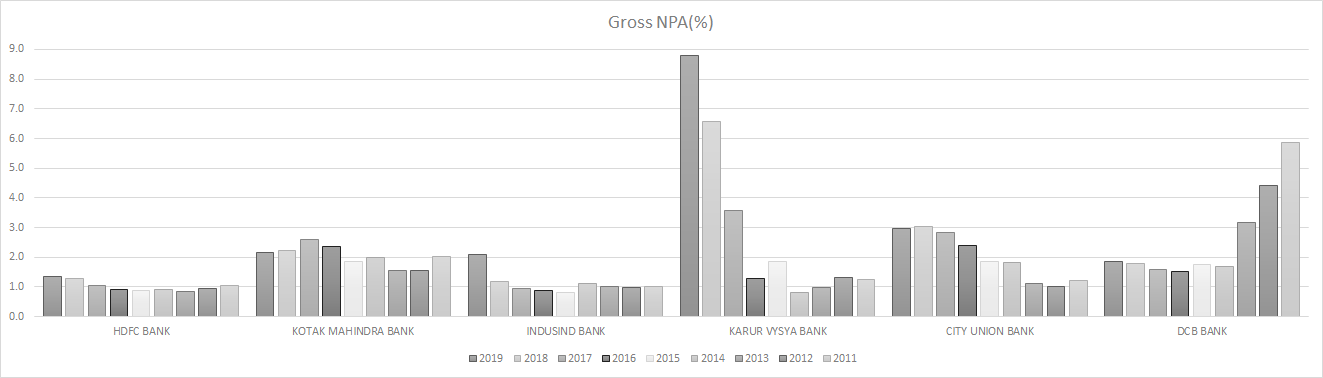

Here are the industry level notes, for Total Assets, Advances, Deposits and NPA’s, that I created while exploring banking industry. Data for graphs is taken from RBI’s website:

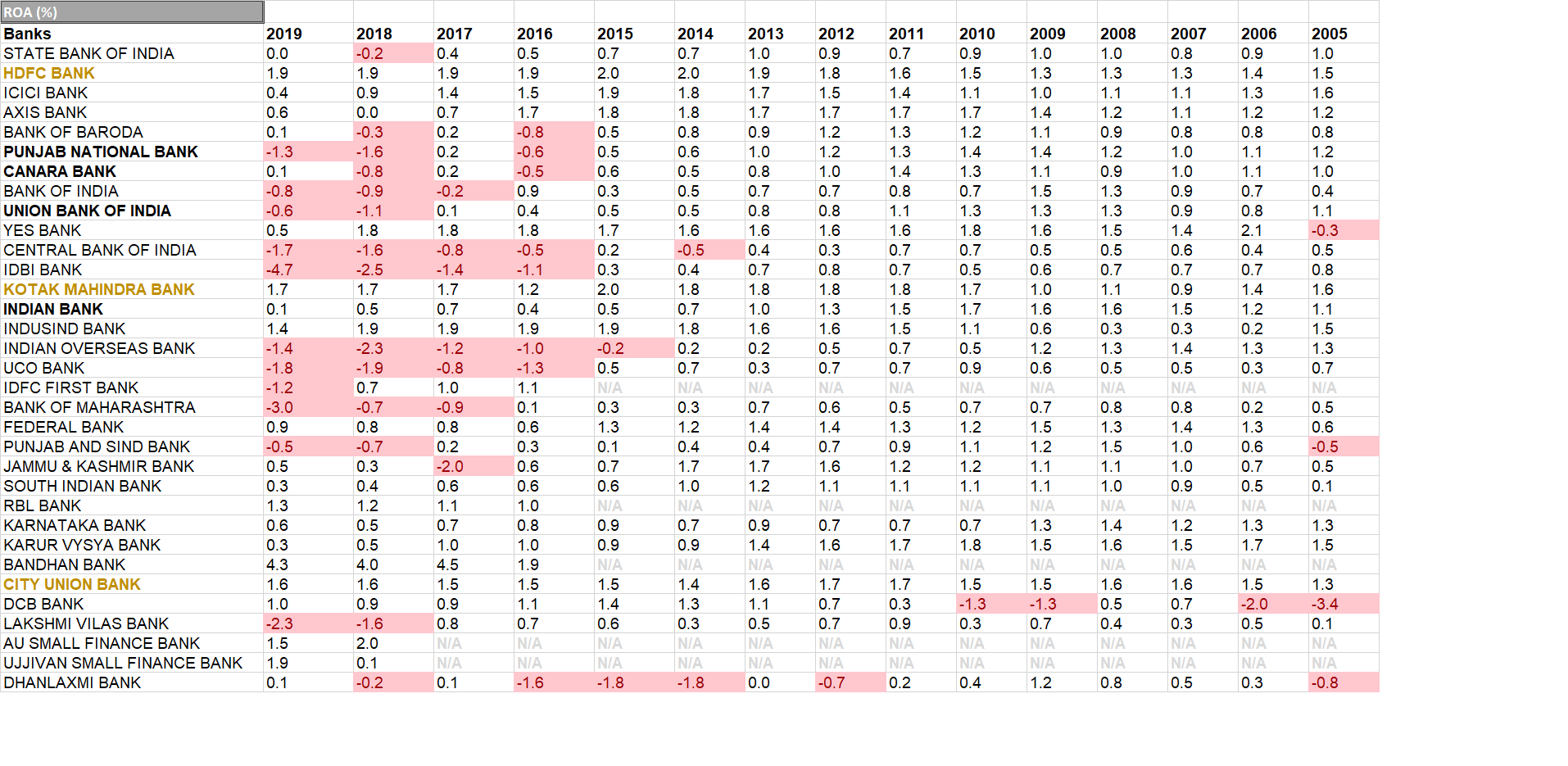

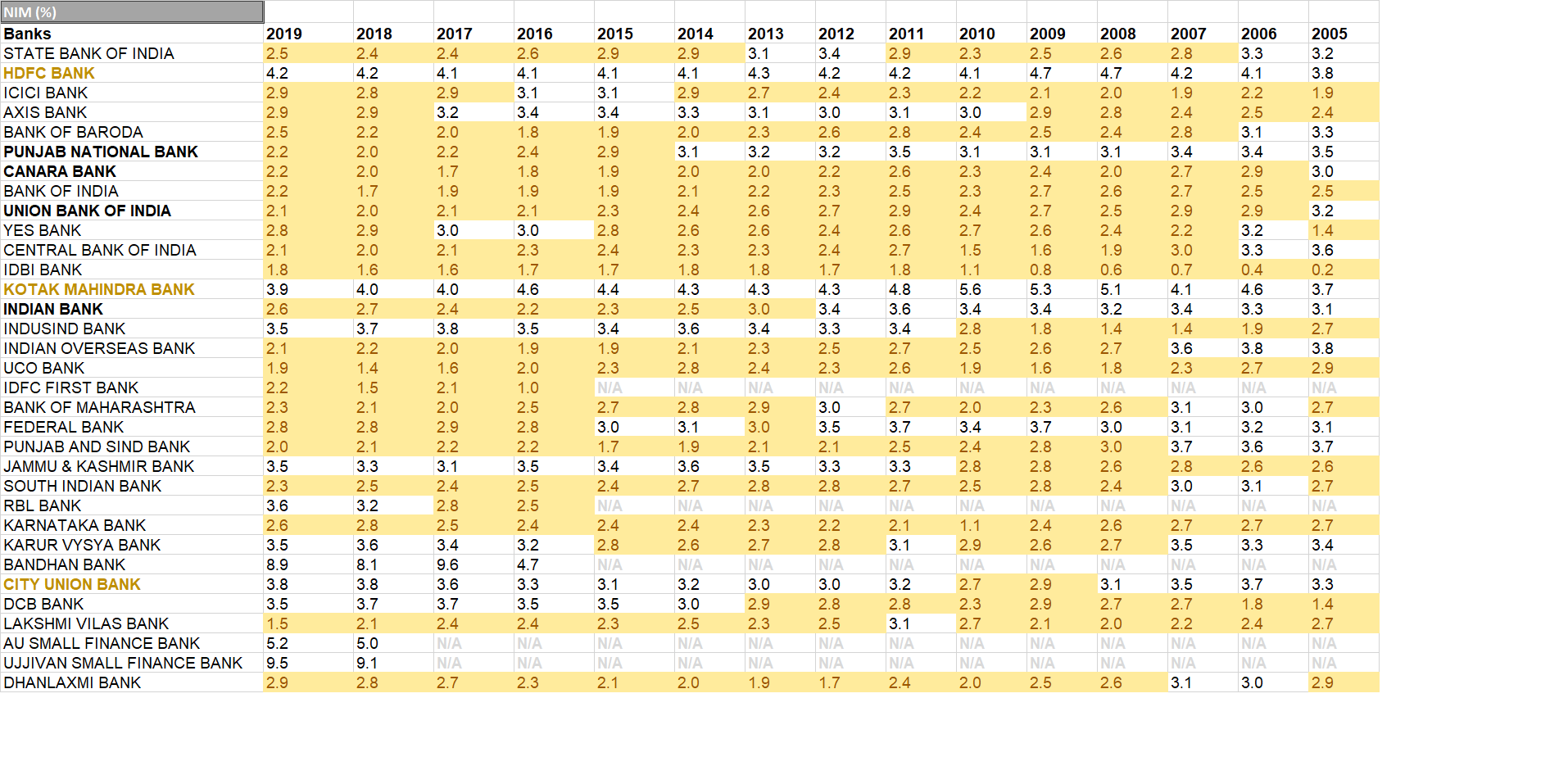

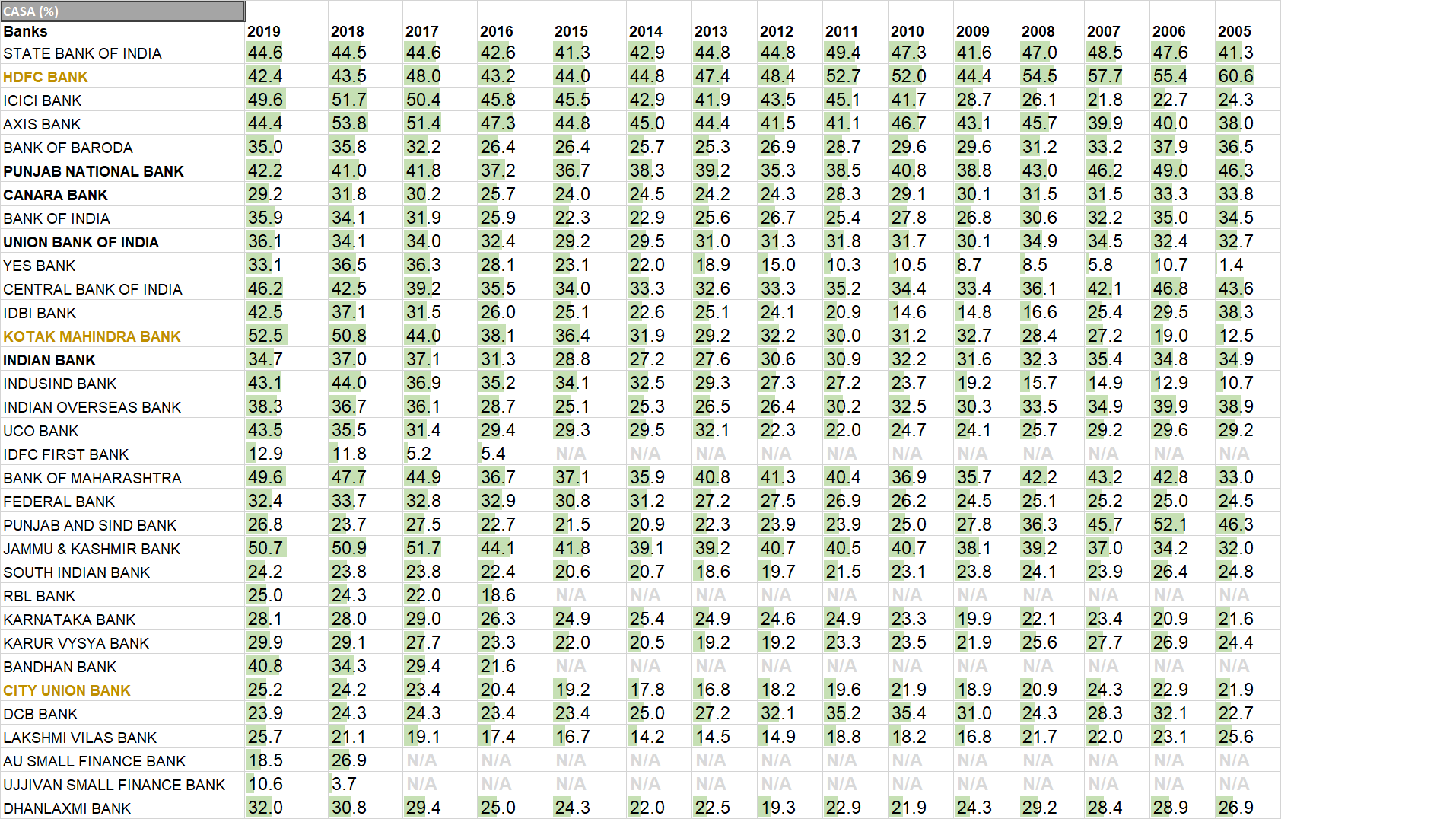

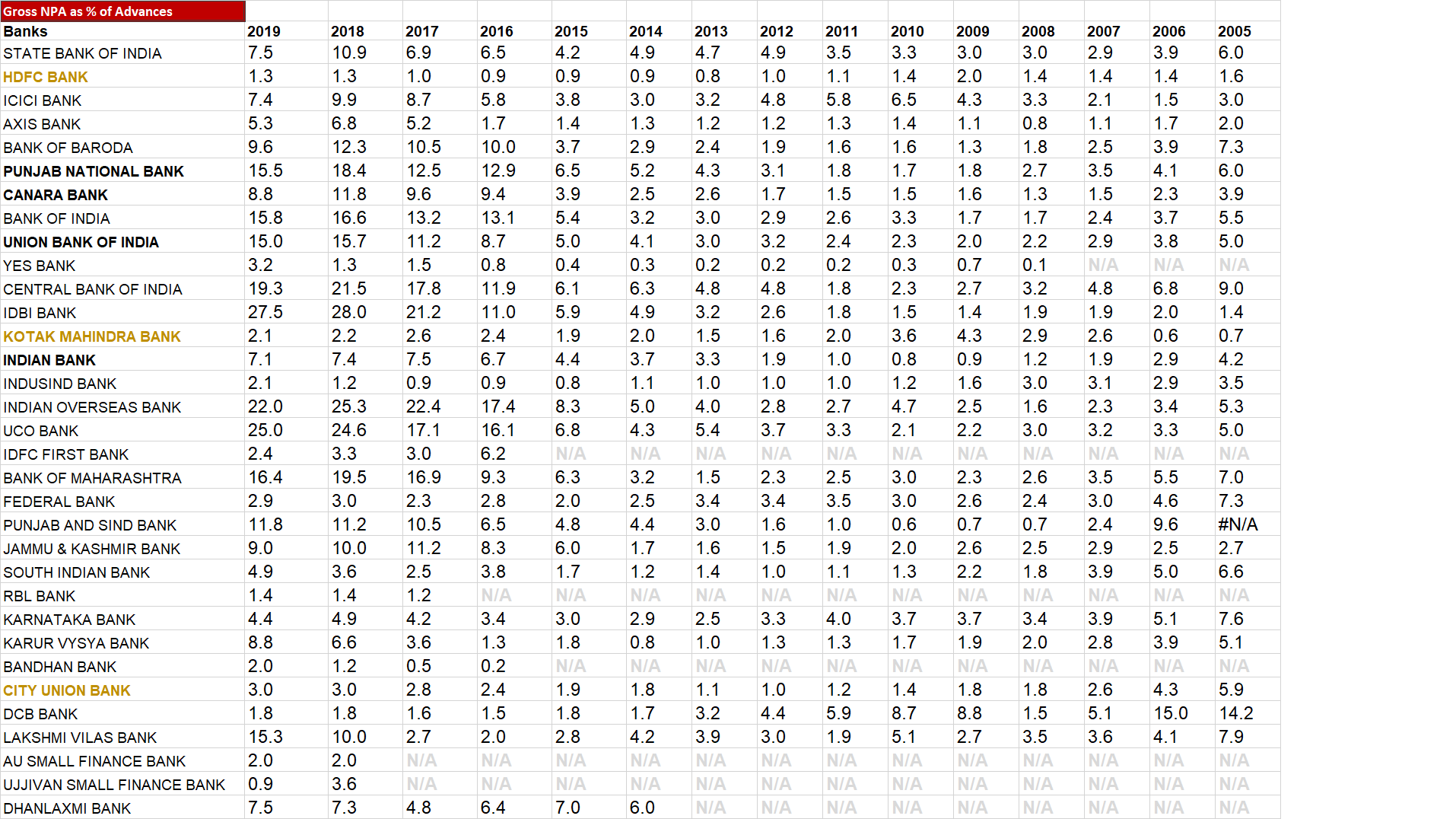

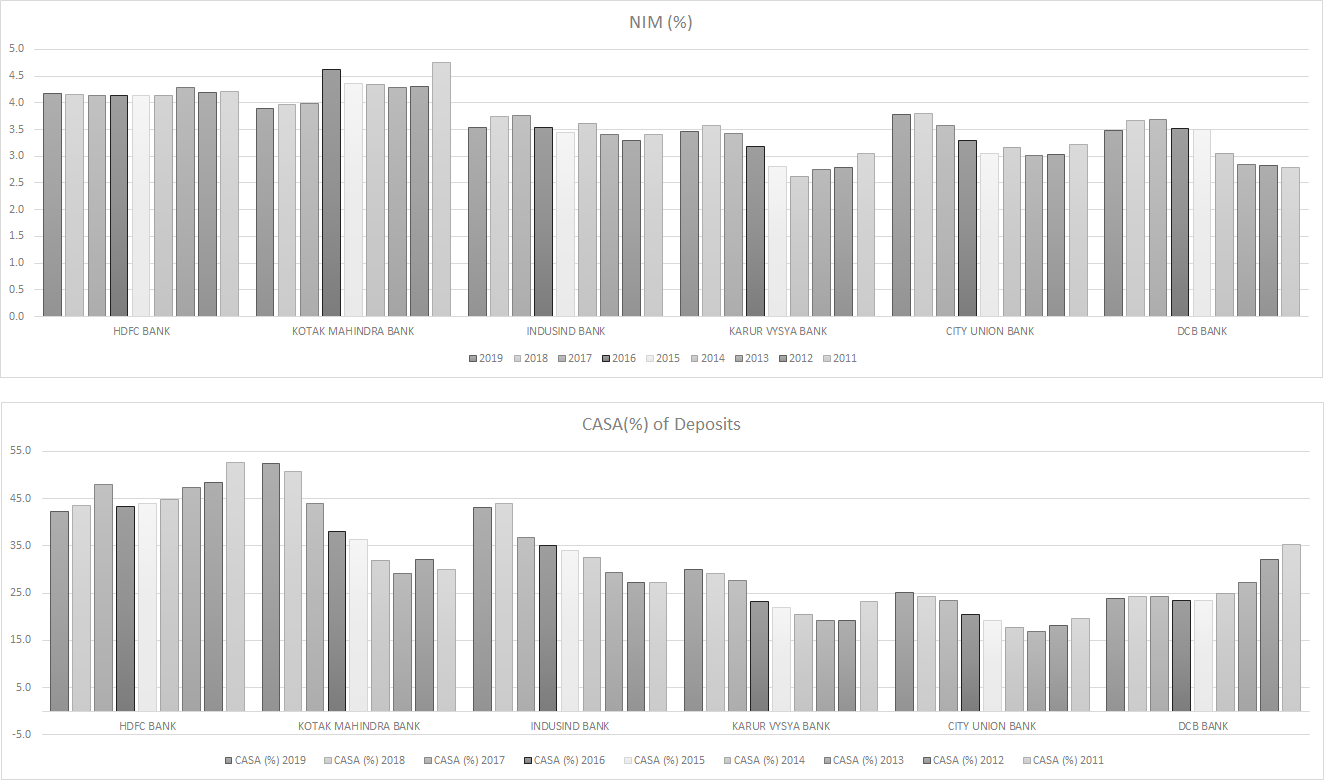

The above analysis directed me to look at the Private Sector Banks. KPI data for ROA, ROE, NIM(%), CASA(%) and Gross NPA(%) for all the banks available in India’s investment universe is as below:

Banks are highly leveraged, with an average Asset/Equity ratio of 10/1 that is Debt to Equity ratio of 9/1. A 10% loss on the assets (which are primarily Loans) will make the equity ZERO. Regulatory guidelines mandate the bank to maintain certain threshold of equity w.r.t debt to remain solvent and ready to extend new credit in the economy.

NPAs: Typically these are of two types- Gross NPAs and Net NPAs.

Gross NPAs reflect the amount of LOANS/ADVANCES on which payment is due from past 90 days. Interest income from such accounts is not accumulated in P&L after labeling them as NPAs to avoid reporting of ghost profits, which results in ballooning of equity. The principal amount blocked in such loans belongs to depositors and banks are accountable to repay the same.

Provisioning is the mechanism to back-fill the depositors money from bank’s earnings. Provision is an expense that is deducted from quarterly profits to reduce the Gross NPAs.

Net NPAs (= Gross NPAs- Provisions) is the effective principal amount blocked as NPAs and banks are hopeful to recover the same in subsequent period. If not recovered, P&L will take a charge in the form of Provisions.

Credit Cost: The EXPECTED loss, which varies as per product category, on the LOANS/ADVANCES extended by the bank. Assume a bank that loans money only for one product category- Home Finance, which has a Credit Cost of 1% as per historical norm/ industry standard. The bank has taken deposit of Rs.100 from customers/financial institutions at 5% and plans to earn 4% spread. In order to earn a spread of 4%, the loan to home buyers WILL be extended at 10%.

In nutshell, Credit costs are the losses which were EXPECTED as per managements judgement. Due to poor economy or lenient underwriting, NPAs are the losses that are REALIZED, if no recovery happens. Provisioning is the mechanism to apply realized losses to banks profit/equity in a graceful manner so that the bank’s equity does not reflect irrational exuberance.

Also, in recent years bank has started reporting its number as per IndAS (previously they were reporting as per IGAAP). If have to compare the numbers (especially provisions & NPAs) of IndAS with IGAAP, any idea how we do that?

However, there is no benchmark to say that up to X% of NPAs are OK. As the same regulatory body governs all the banks, inference of NPAs can be derived by relative comparison across banks and observing the trend for an individual bank.

Even if the conversion is possible by any yardstick, the essence of analysis will not change.

I meant, how we can compare the financials of FY2017 (IGAAP) with FY2018 (IndAS) of a same company? As there are few differences in reporting, we have to adjust number to make them comparable