Good analysis @rupeshtatiya. It is worth noting that Indian Bank is the only PSU bank that will not get govt bailout bonds (recap bonds) because as per government it is not on the verge of collapse. But that’s not to say that is in good financial shape. NPAs are very high and for for market to re-rate this stock, NPAs will have to go down a lot before market will assign a higher P/B ratio.

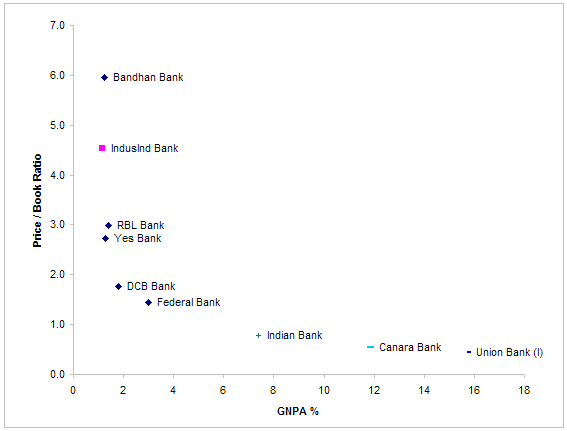

P/B ratio is highly correlated with GNPA ratio.

Source: Capitaline

Indian Bank has to get its GNPA ratio down to 2% before market will value it at 1.5 times book. Last time its GNPA ratio was below 2% was 2011 and it been going steadily up since then. I don’t see the NPA situation improving anytime soon. Bank will need a new credit culture to make a meaningful and sustainable improvement in asset quality which I don’t think will happen in a PSU bank.

As you rightly said, this is an attractive security and not an attractive business. Perhaps, we can go down the P/B scale to find even more attractive securities.