[ Comment too short ]

Mcap = 6400Cr

Net Worth = 13870 Cr

CMP/Book Value = 0.46

Net NPA = 2856Cr (2.48%)

CAR (Basel 3) = 13.26%

June Quarter Results -http://www.indianbank.in/pdfs/fin/jun14/REVIEW_REPORT_300614.pdf

Shareholding pattern - Govt. holds 81.5%. Free float is just 5.9% (rest held by institutions)

And for whatever the broker recommendations are worth, Motilal Oswal has put has target of 230 on 26th July-

Comprehensive Report -

http://www.indianbank.in/pdfs/fin/jun14/Financial_results_june_2014.pdf

Tier I CAR (basel 3) = 10.74%

Tier I capital = 11300 Cr

Tier II CAR (basel 3) = 2.54%

Tier II capital = 2676 Cr

CASA Ratio = 29.2%

This stock is held by a large number of AMCs such as Birla, Kotak, Goldman, HDFC,HSBC, Sundaram, Mirae, DSB BR , Religare etc and many of them have bought from July month -

The ROE/ROA might be low for this bank but the valuation are still quite cheap for its relatively low Net NPAs.

You can buy because it is undervalued however you should also look at potential for growth while investing. You can see the returns of PSU some companies with moats. Companies with great moats always give higher returns…

Ofcourse this has been the only reason for buying as of now. Say that they can recover zero rupees from the ~2800Cr NNPA, even then the net worth is 11000Cr and the market cap was 6400Cr.

T M Bhasin, CMD,along with ED & GM add the call.Highlights by Capital Mkt:

- Bank has continued with the strategy of reducing the high cost deposits as well as low yielding advances. Bank shaded about Rs 8000 crore of high cost deposits and about 8000 crore of low yielding advances in Q2FY2015. The strategy has helped the bank to improve Net Interest Margin (NIM) by 23 bps on sequential basis in Q2FY2015 to 2.67%. Bank proposes to continue with the similar strategy for rest of the year and plans to further improves NIM by 10 bps.

- The capital adequacy position of the bank remains strong. The capital adequacy ratio of the bank stood at 13.05%, while the ratio was further high at 13.54% including the H1FY2015 PAT at end September 2014.Bank does not have any capital raising plans for FY2015.

- Fresh slippages of advances to NPA category eased to Rs 786 crore in Q2FY2015 from Rs 941 crore in Q1FY2015. Bank expects further decline in fresh slippages, going forward.Bank has been focusing strongly on recoveries of non-performing loans.Bank plans to sale about 17-18 account with the exposure of Rs 1000 crore to Asset Reconstruction Companies (ARCs).

- Outstanding securities receipt on the book of bank stands at Rs 1358 crore at end September 2014.Fresh restructuring of advances stood at Rs 594 crore in Q1FY2015. Restructured advances of the bank stood at Rs 9783 crore at end September 2014. Bank does not any significant restructuring pipeline.

- Bank has targeted business growth of 12% for FY2015 with deposits as well as advances growth planned at 12% for FY2015.Bank proposes improve the distribution network to 2500 branches and 2500 ATMs by end March 2015 from existing 2380 branches and 2189 ATMs.Bank has fully provision for AS-15 related employee provisions. Bank has been making provision of wage revision at higher rate of 15% amounting to Rs 30 crore per quarter.

- The average age of the bank staff has declined over last three years from 51 years to 48 years. Currently about 33% of the staff is below 30-years of age.Bank sees about 900 employee retiring every year for next five years. Bank is planning recruitment of 2500 fresh staff.Bank has been meeting the Priority Sector Lending Targets (PSL), so its RIDF investment stands nil.

CONFERENCE CALL - from Capital Markets

Proposes to position as retail and mid sized bank

Indian Bank conducted the concall on 12 May 2015 to discuss financial performance for the quarter ended March 2016. Mahesh Kumar Jain, MD&CEO, Indian Bank addressed the call:

Highlights:

- In the backdrop of slower economic recovery, the bank has been taking various corrective action since 2010. Bank moderated its business growth below the banking system level. The bank has been in the consolidation mode since 2010. Bank defocused from top line growth and focussed strongly on bottom line growth.

- Bank has been focusing strongly on growing retail liabilities and assets. The banks deposits grew mere 5% against system deposit growth of 11%. The bank has posted 15% growth in its CASA deposits, while exhibited about 300 bps improvement in CASA ratio in last two years.

- Retail deposits share has increased to 83% of the total deposits. On the other hand, the share of banks high cost deposits has declined from 18% at end March 2014 to 8.7% at end March 2015 and further down to 4.6% at end March 2016.

- Bank has improved the share of retail advances from 43% in March 2014 to 46% in March 2015 and further up to 49% at end March 2016. On the other hand, the share of corporate advances have declined by 600 bps over last 2 years.

- Bank has put strong focus on technology, while spending Rs 300 crore in last 3 years. The share of banks e-transactions has increased from 43% to 52% in FY2016.

- On asset quality front, the bank has reduced the exposure to top five stressed sectors from 19% to 16% in FY2016, where the banking sector exposure stands at 24%.

- The bank has continued to maintain the top capital adequacy ratio position among public banks with the CRAR ratio of 13.2% at end March 2016. Bank has not made and request for capital infusion to the Government. With regard to capital raising, bank would wait for appropriate time.

- The Net Interest Margin of the bank declined to 2.33% in FY2016 from 2.5% in FY2015. The interest income reversals stood at Rs 365 crore, mainly impacting NIMs by 30-35 bps in FY2016.

- The fresh slippages of advances increased to Rs 3400 crore in Q4FY2016. About Rs 1600 crore of fresh slippages were contributed by the weak accounts as identified by the RBI under Asset Quality Review (AQR) of the banking system.

- Bank has fully recognised and made provision against the stressed assets as part of Asset Quality Review (AQR) of the banking system conducted by the Reserve Bank of India. taken care of AQR related stressed assets. However, bank has only Rs 80 crore provisions to be made in FY2017 towards AQR accounts to be recognised in FY2017.

- The restructured advance book of the bank declined to Rs 6366 crore at end March 2016 from Rs 8900 crore at end December 2015. Bank has restructured Rs 675.48 crore advances in Q4FY2016 due to floods in Tamil Nadu.

- The asset sale to Asset Reconstruction Companies (ARCs) stood at Rs 1000 crore in Q4FY2016.

- As per the bank, its balance sheet has been fully cleaned up on asset quality front. Bank expects fresh slippages of around Rs 2000-2500 crore in FY2017, of which about Rs 500 crore are expected to be contributed by restructured advance book.

- Bank expects upgradations of about Rs 800-1000 crore in FY2017, while sees overall asset quality to improve in FY2017.

- Bank had conducted Strategic Debt Restructuring (SDR) for accounts having exposure of Rs 1000 crore, and all these accounts have been classified as NPAs. The 5/25 refinancing for the bank stood at Rs 2400 crore and about 75% of this is classified as NPAs. As per the bank, any resolution to these SDR and 5/25 refinanced accounts would provide earnings upside for the bank.

Mid-sized bank

- Bank proposes to position itself as mid-sized bank with the focus on retail and mid-corporate segment.

- Organisational reorientation, human resource reforms and business process engineering are being undertaken.

- Bank has created three verticals 1. Mortgage loans including home loans, 2. Mid-segment comprising of MSME and mid-corporate, and 3. Other retail loans.

- Urban financial inclusion is also taken up as focus area.

Outlook

- Bank is targeting overall 11-12% loan growth for FY2017.

- Loan growth for new verticals is targeted at 20-25%, while bank expects negative loan growth in the large corporate segment.

- Bank proposes to raise Rs 500-1000 crore from Tier II bonds in FY2017.

- Bank expects to improve NIMs to 2.65-2.7% in two years.

Awesome analysis, can you kindly share the updates.

Also, will be great to know your opinion on shift of CEO from here to IDBI bank.

It’s one of the undervalued stock in this raging bull market

I could find.

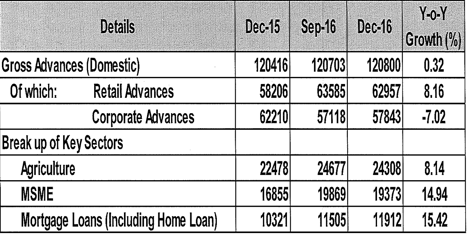

Key points from Q3 Results:

Ø

Book value grew ~10 % YoY, stock available at

0.85 P/B (Current Price)

Ø

9M FY17 profit increased by 1.73 times profit of

9M FY16

Ø

Cost to income ratio reduced from 50.93 % on

Dec-2015 to 44.69 % in Dec-16

Ø

CASA increased from 30.7 % on Dec-15 to 38.71 %

on Dec-16

Ø

Breakup of Advances show focus on Retail ,management seems to be walking the talk :

Ø

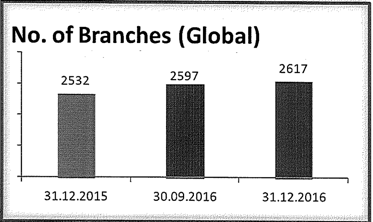

Number of branches increasing at a steady rate:

Ø

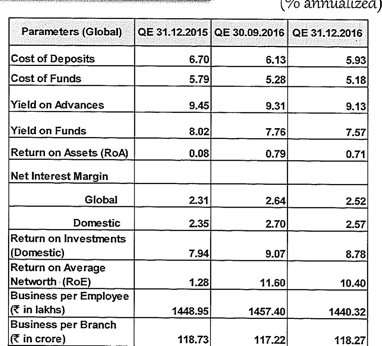

Other Key Ratios:

Concerns:

Ø

Star CEO , Mahesh Kumar, who helped turn around

the bank moved to IDBI Bank.

Ø

NPA figures still very high:

GNPA : 7.69% and Net

NPA : 4.76 %

Other Important News in recent weeks:

Last but not the least on Technical analysis front. Though I

am a novice in Tech Analysis, however looking at the trend line it appears

stock is near its support level. Results are a week away ,IMO it’s good time to accumulate:

Disclosure: Invested and planning to increase my position. Pls do your own research before making any purchase.

And here you go… excellent set of results from Indian bank. Full year ROE will be greater than 10 %. Hope to see more improvement going further.

Can someone good in banking domain please let us know what would be the affect (positive/negative ) of any Bank going for FPO to raise funds

We had some work on PSU bank numbers across several parameters. The link is enclosed below →

The idea was that - the public setup is so against the public sector banks in the light of recent events that there might me some undervalued/mispriced securities that we can find. Based on that, a few banks had come out for tracking & Indian Bank is one of them.

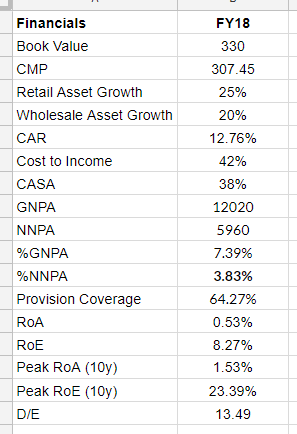

FINANCIALS

Few points which caught eye for Indian Bank are →

- The GNPA/NNPA numbers are better than most of the PSU banks & they are better than even ICICI Bank!

- When most of the the PSU banks are not growing or growing moderately, Indian Bank is growing at a decent pace.

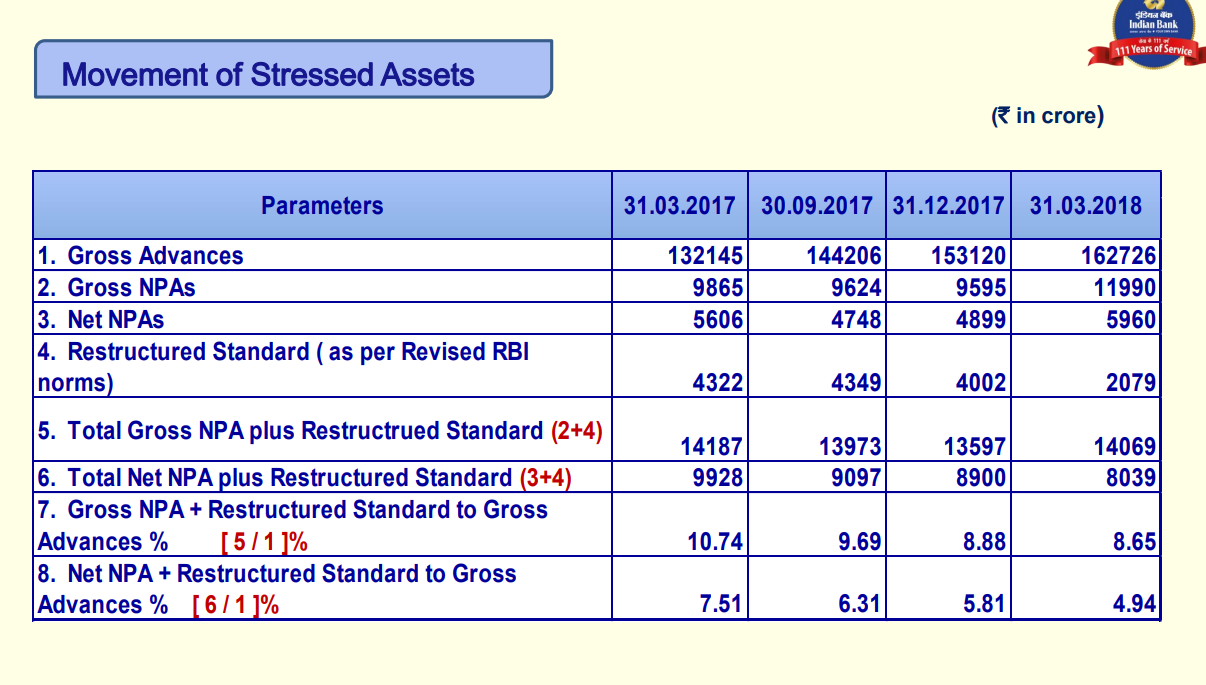

- Following slide provides asset quality picture for Indian Bank & it can be seen that it can be decently managed. More than 2.5% reduction in NNPA + Restructured Standard Assets is quite significant.

- For FY18, the RoE & RoA of banks took a lot of hit primarily due to credit costs. The bank reported loss in Q4FY19 mainly due to clean up induced by RBI Feb 12 circular on SDR, 5/25 etc.

The investment thesis depends upon -

- buying price well below book value

- bank getting to decent RoA & RoE numbers over next few quarters

- Some potential resolutions/write-backs from IBC accounts

- ability of the bank to raise capital at some premium to book value.

The thesis might not play out due to following things -

-

Value discovery in PSU banks might take a long time due to various things & it might test investor’s patience. There are also opportunity costs involved in various market scenarios. That being said downside looks limited from here based on current information.

-

GoI holds 80%+ market share in the Indian Bank & bank has been trying to bring this stake down unsuccessfully for a long time. Equity dilution at a premium to book value remains an important trigger for potential gains which bank might not be able to achieve.

Further some interesting points from last conf call →

Q4 FY18 CONF CALL

- Around 2347Cr of additional NPA was recognized due to RBI related actions. This includes 1727Cr of additional NPA due to Feb 12 circular (provision of 504Cr). Further bank had to account for 520cr of divergences (provision of 440Cr).

- The restructured standard book has come down to 2079Cr from 4322Cr. The exposure to power sector is close to 500Cr in 2 accounts.

- The are 41 cases in IBC resolution process with total exposure of 5481Cr.

- The bank has provided following guidance for FY19 - NIM (3%), GNPA (6%), NNPA (3%), Credit Cost (2000Cr provisioning for entire FY19)

FY18 Investor Presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachHis/ba9eede2-7182-4ea3-a1a5-a44480b3aa21.pdf

FY18 Results:

https://www.bseindia.com/xml-data/corpfiling/AttachHis/aa13ea72-7587-4bec-ba5b-591519fcc087.pdf

Disclosure -

I am invested in the stock, forms < 5% of portfolio, no transactions in last 60 days.

This stock falls in the category of attractive security (AS) for me where I will buy & sell at certain price points. It is not an attractive business (AB) for me which can be held for several years. This is not a buy/sell recommendation, investors are advised to do their own due diligence before investing.

3 Likes

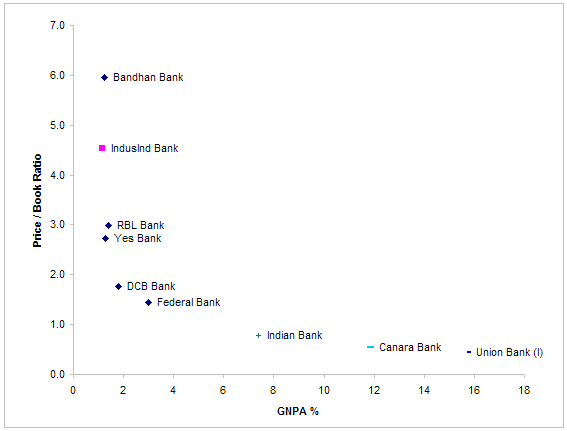

Good analysis @rupeshtatiya. It is worth noting that Indian Bank is the only PSU bank that will not get govt bailout bonds (recap bonds) because as per government it is not on the verge of collapse. But that’s not to say that is in good financial shape. NPAs are very high and for for market to re-rate this stock, NPAs will have to go down a lot before market will assign a higher P/B ratio.

P/B ratio is highly correlated with GNPA ratio.

Source: Capitaline

Indian Bank has to get its GNPA ratio down to 2% before market will value it at 1.5 times book. Last time its GNPA ratio was below 2% was 2011 and it been going steadily up since then. I don’t see the NPA situation improving anytime soon. Bank will need a new credit culture to make a meaningful and sustainable improvement in asset quality which I don’t think will happen in a PSU bank.

As you rightly said, this is an attractive security and not an attractive business. Perhaps, we can go down the P/B scale to find even more attractive securities.

6 Likes

@Yogesh_s

I agree.

There are two ways to play the PSU undervaluation story similar to cyclicals -

- Buy the bottom banks which large GNPA (15%+), NNPA (10%+) or even -ve net worth. One one is sure that these banks will survive the cycle, they will be highly rewarding when the cycle turns. This is similar to buying high debt sugar stocks at the bottom of the cycle as they might give better return than stronger players.

- The second way is to buy a little bit stronger player. In this case, returns might be lower than above case but risk will also be lower as financial performance of the bank will take care of itself.

Indian Bank fits in second category above. There are few interesting players in category 1 as well like Bank of India, Dena Bank etc. with IDBI bank as the most interesting one (Mahesh Jain of Indian Bank moved to IDBI Bank & it looks like he is hired to clean up books).

I keep tracking these banks but have not made any investments in category 1 banks yet.

Regards,

Rupesh

1 Like

PSU banks’ P/B ratio bottomed out in March 2016 at around 0.3. These banks (especially the bottom of the stack) are trading above their March 2016 lows (in terms of p/b ratio) and their financial health is worse than what it was in March 2016. In a way market is already looking at better days ahead and has already priced that. Really bad ones with GNPA of 15%+ may not survive and will be merged with others. I think the asset quality reviews by RBI is to identify candidates for shotgun marriage.

About your category 1 banks, I think the best case scenario is when their financial condition improve from horrible to very bad and IMO market has already priced that.

1 Like

Most of the PSU banks are trading at a price below or at the same level as in March 2016. P/B calculation for these are speculative as most will assign close to zero book value. After a certain point the valuation of these PSU banks are based on their branch network and customer reach. These will occasionally burst upwards and fall back to these levels till their is a concrete solution is in place.

1 Like

Hi the stock has fallen to the prices of 2013 and 2016 levels of around Rs 100. They had issued ESOP’s around few months back to staff when stock was around 280 levels and was given at 25% discount rate, most of the staff’s was forced to buy the stock at those levels. Now its trading almost 50-70% down from that level. I would like to know if there is any reason why there has been a sharp fall and are you still holding the shares?

I had small position in Indian Bank & had sold out Indian bank on some profit & it was always short term story for me.

PSU banks valuations have been attractive for a long time & hence we were trying to understand the broader landscape. In that context, Indian Bank was looking interesting with lowest NPA & no need for fund infusion by GoI. But NNPA spiked in the quarter right after I wrote that post.

Also there is no stability in top management of the bank with 2/3/4 CEO changes in last 2/3 years. There nothing differentiated in their lending model & RoA are sub-par.

Further, with GoI as major shareholder, wealth creation or PAT is not always the focus. GoI might want directed lending or might want to monetize stake or M&A as we are seeing. When biggest shareholder is not aligned with your goals, little bit tough to take long term position.

These might be some reasons along with broader sell-off bearish sentiment for the fall in share prices.

As I understood banking more, I have moved to private sector lenders who focus on underwriting, who have better margins for the risk they are taking, management stability & product innovation/category creation etc. With PSUs & NBFCs in mess, there is also some tailwind behind them.

1 Like

I’m expecting higher loan growth for all PSU banks and heavily long On Indian Bank. The only concern is Allahabad banks high NPA and toxic assets.

All PSU are expected to post fair result in this quarter. NPA slippage can be a tailwind