IndiaMart buyback is good news, though specific details are not yet known. It has been pretty clear they are unable to find any meaningful acquisitions, so better return the cash to investors than fritter it away. I would have been happier if they had done this much earlier, especially without spending those Rs.500 crore on Busy, but anyway, better late than never.

The QIP was opportunistic (did not need the funds) to take advantage of the expensive share price. Likewise, the buyback is to capitalise on the 50% fall from peak. They did make some small acquisitions but are sitting with Rs2500cr of cash on books. This may perk up the stock. I think the promoters are smart and know when to issue and when to buyback basis the stock price but some may also complain that they are too stock price focused. Especially when the business is such that they really do not need to access capital markets on an ongoing basis.

This show a special sign to me for the management is that they are very opportunistic that they took advantage of good share price and now taking advantage of lower share price this show they are actually creating a value from the cash and there own stock.

Have seen this very less with many indian management but have seen with some very good us management like amazon is one such that do this quite nicely.

Just want to see this should be a no tender issue as if that is the case then it would show they value price and return on cash more then just making investors happy.

Let’s see what the overall size of buyback is.

Hope it is significant and return good and if it is a tender issue then I will participate to downsize my position.

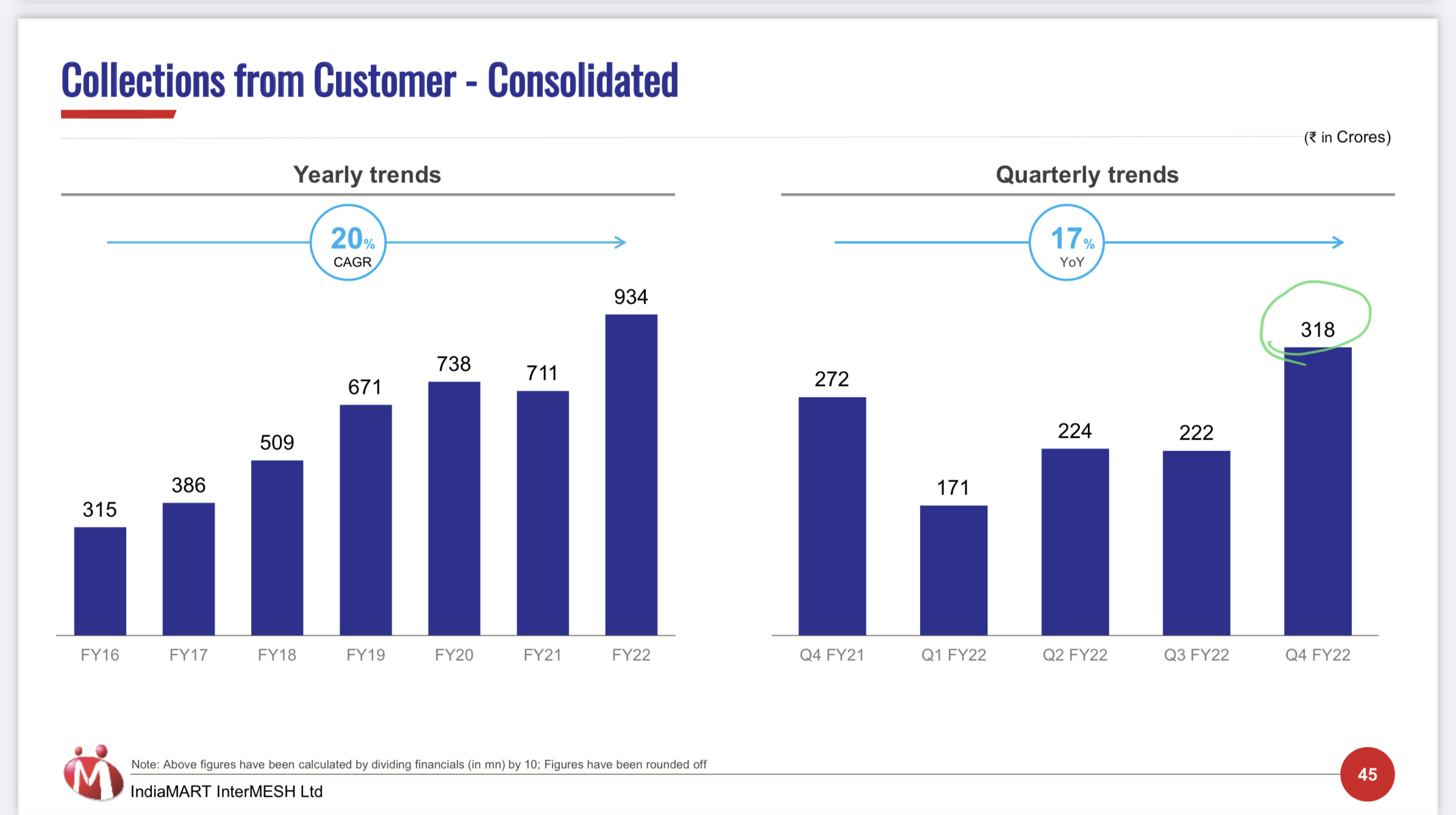

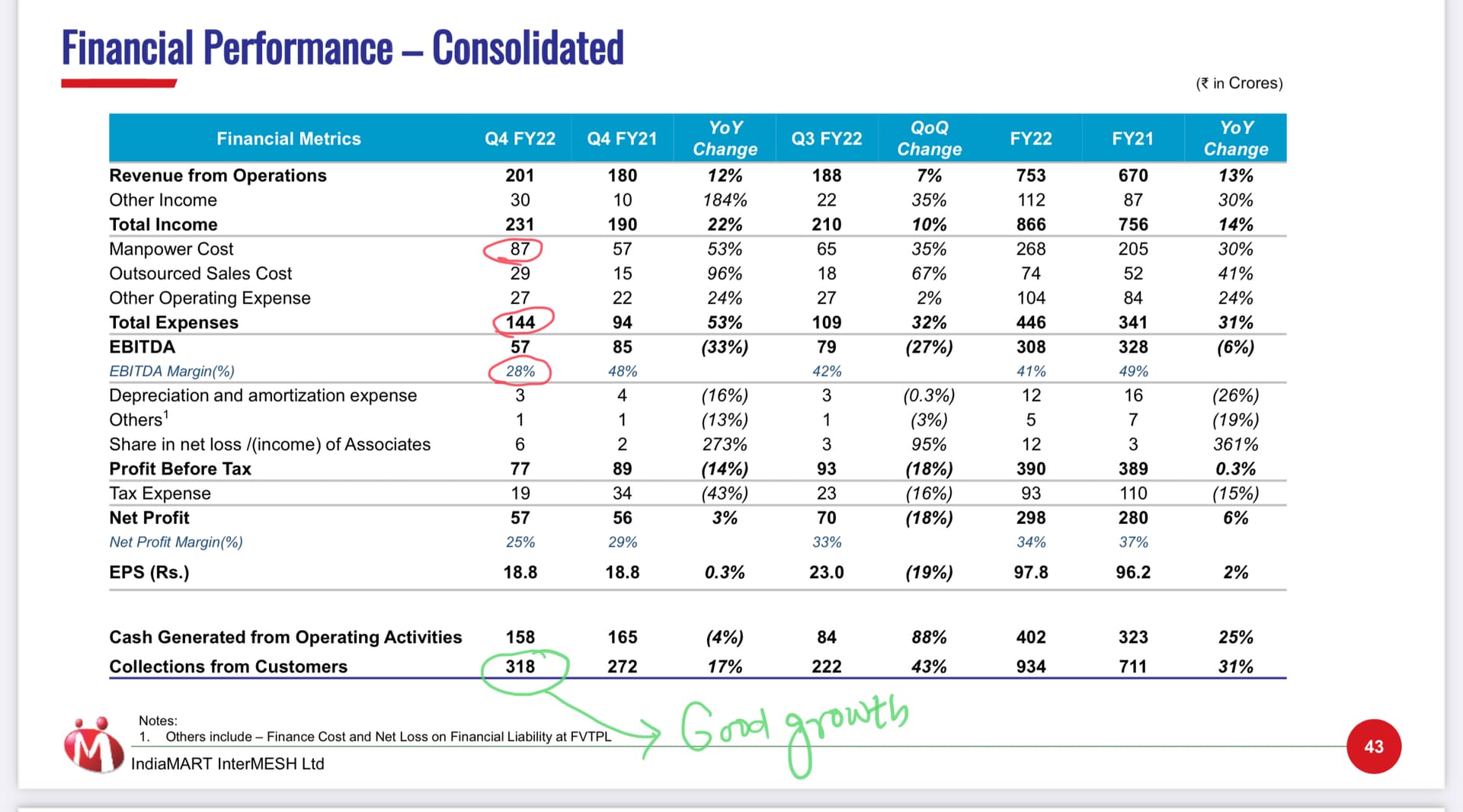

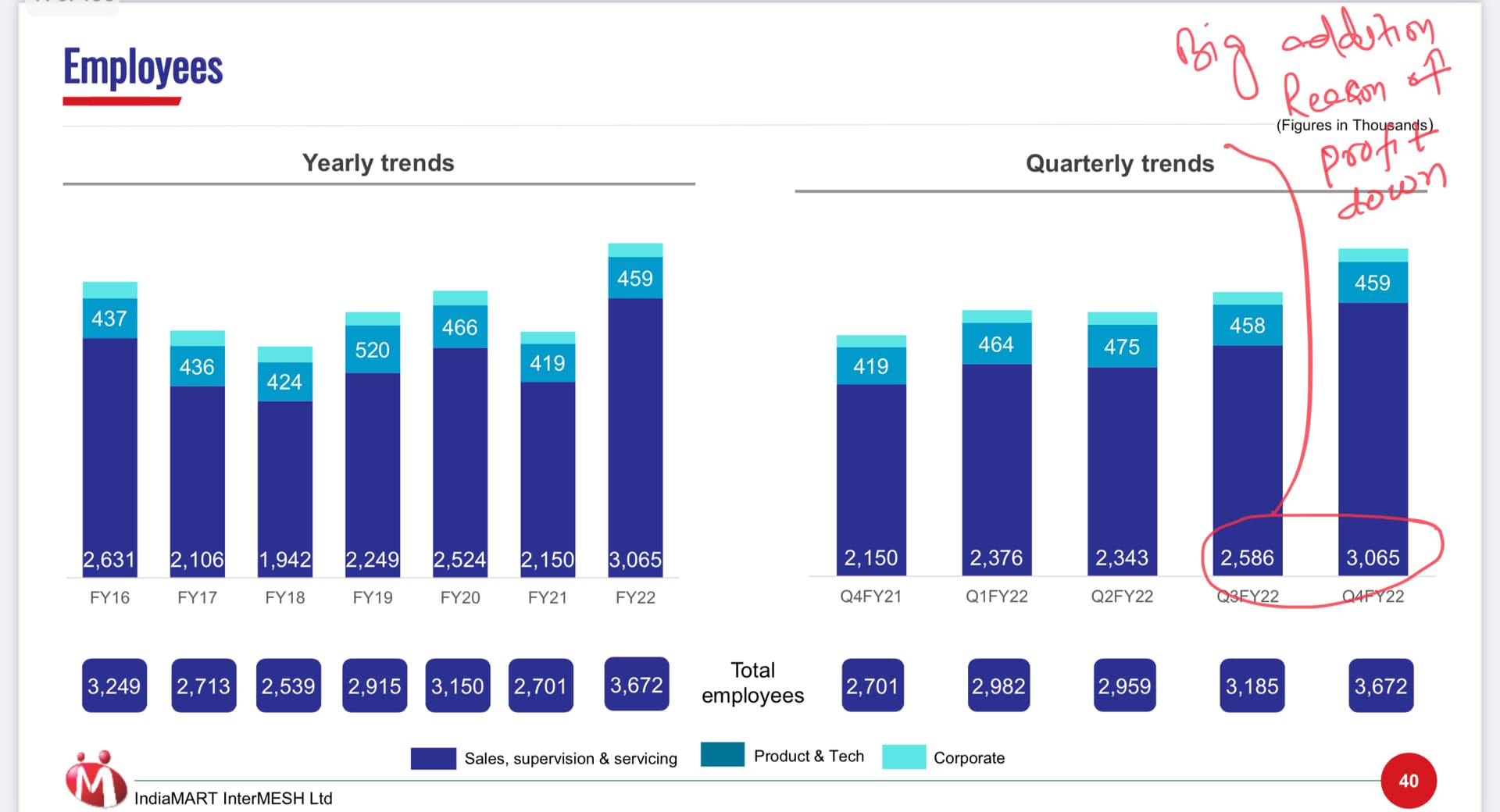

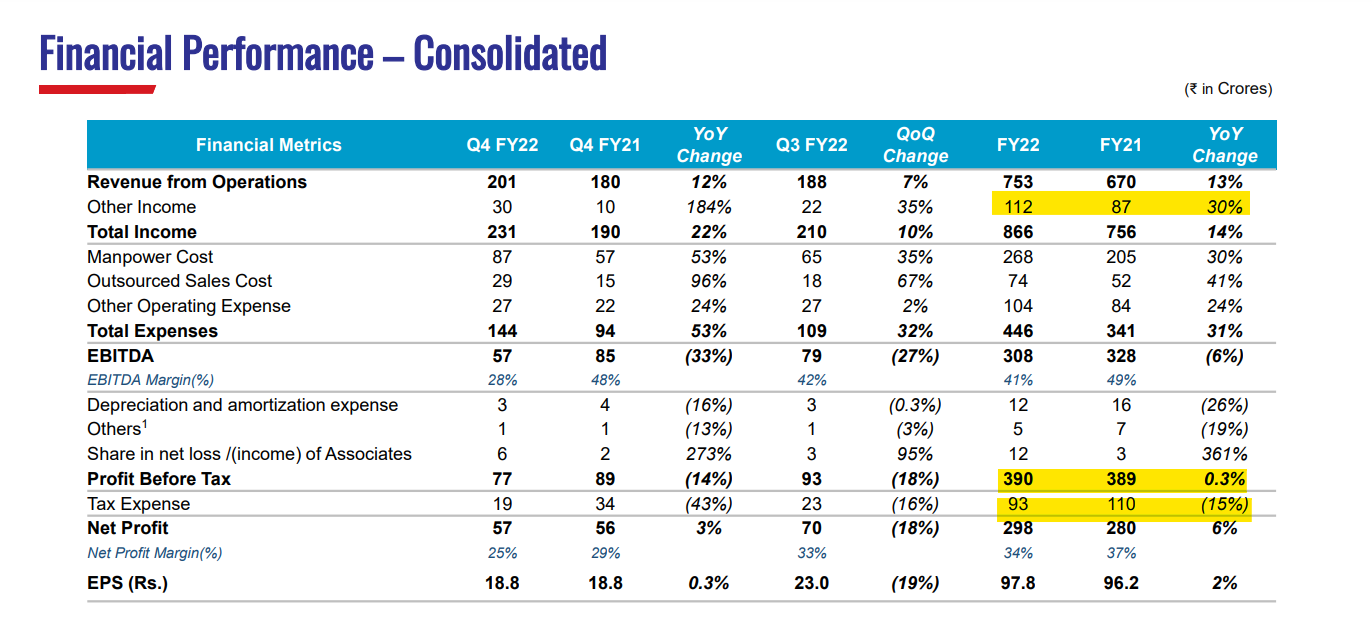

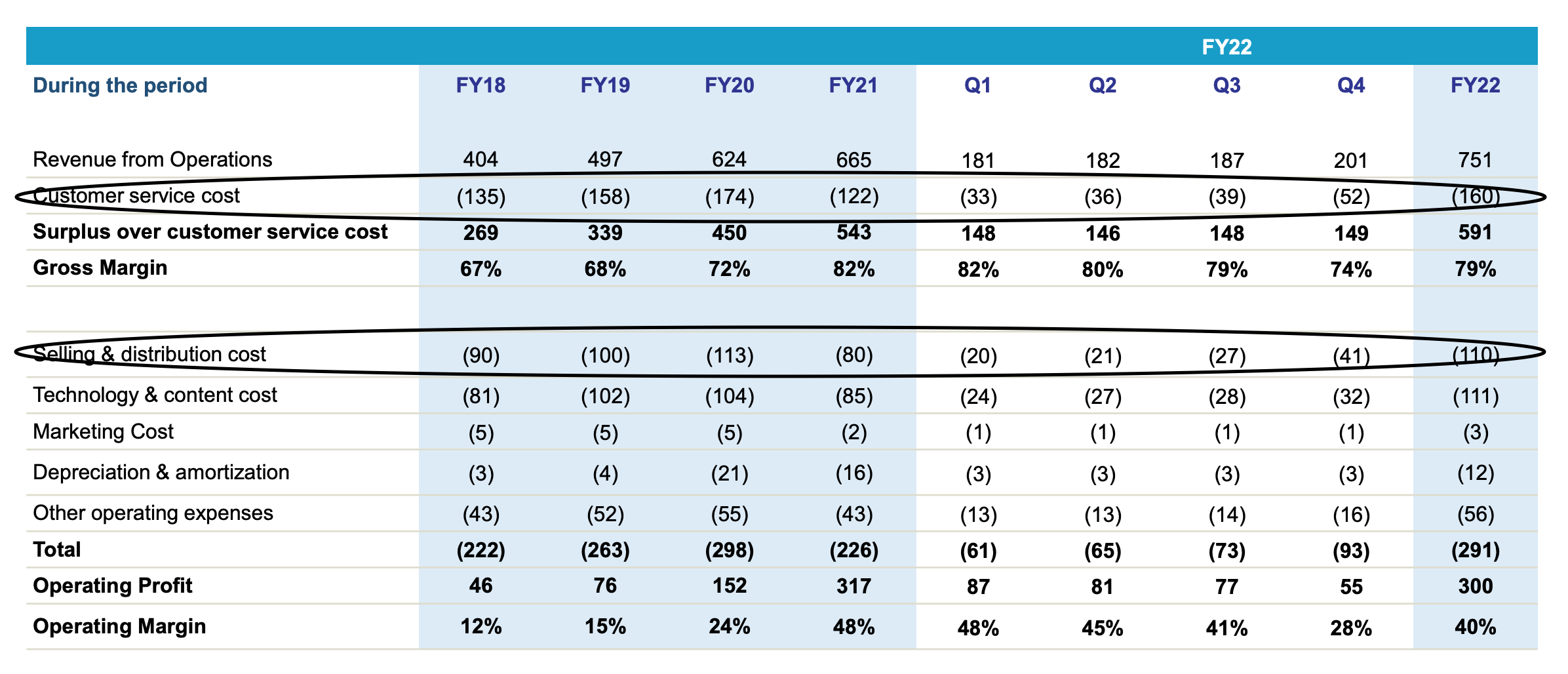

Results are not at all bad. Paying suppliers increased to 169,000 from 156,000 – an increase of 13,000 for the quarter which is among the highest we have seen. Customer collections are also at all time high of Rs.318 crores, a big 44% jump over previous quarters. The management now says they are planning to invest in growth, and are hiring aggressively, with most of this hiring happening on the sales and servicing side. A statistic of requiring 1 new employee per 75 new customers was mentioned in the concall. Since this hiring has happened mostly towards the end of the year, the current sales growth is mostly organic i.e. simply on account of improved macro-economic conditions and the network effects of the business model. Going ahead, faster growth can be expected, assuming no new macro shocks. Of course, this will lead to increased costs and margin compression, as per the management. But clearly, growth is what market is looking for first.

Almost the entire cash generated during the year (~Rs.400 crore) has been invested in subsidiaries. What this will achieve requires a separate investigation, but so far none of the investments (even those more than 5 year old) seem to have given any tangible benefits.

Cash in hand is close to Rs.2,000 crore (excluding Rs.500 crore earmarked for Busy acquisition). In this context, the Rs.100-crore buyback is quite an embarrassment. Better would have been not to announce a buyback at all. When I first looked at the Rs.100-crore amount on the stock exchange intimation, I almost fell out of my chair laughing – at my own stupidity of expecting at least a Rs.1000-crore buyback, thinking the management will admit they are unable to find meaningful acquisitions and so returning the money back to shareholders (see previous post two days back). In the concall, the management made a vain attempt to explain the Rs.100 crore lollipop, but let us leave it at that. I have seen many promoters sit endlessly on their cash (Bajaj Auto, AIA Engineering, HMVL etc. from my own ex-holdings) and Indiamart also now joins the list.

For me, Indiamart now falls in the ‘most difficult to decide’ bucket – good business with a bad management. Always a dilemma what to do with such stocks in your portfolio.

Over last 2 years, Indiamart has clearly underperformed in line with their target segment MSME. Q4 call finally showed some potential of turnaround.

Good parts

Revenue is a lag indicator and moving average of past few quarters Deferred revenue ( which in turn is function of Collections), both lead indicators are strong

Past 2 years mgmt has been shy of committing beyond 5-6k paying subscribers, guidance is now 8-9k per qtr,

Current qtr strong paying subscribers of over 13K subscribers includes reactivation of some of lost customers, major sales team hiring happened in Feb & Mar, good to see focus and aggression on growth and GTM

Paying subscribers mix - top 10% contribution is 25%+ in revenue ( platinum band), I.e. 1.8 Lac per paying subscribers, this band gives them comfort on YoY 5% subscription upside over med term( key characteristics of SaaS model Op lvg - key monitorable)

Mild diluttion in ARPU in near term given major new customers join at lower band/silver, but sustainable range and 5% YOY growth guidance over med term

Change in mgmt perspective on customer base - no more SMB only, equal focus visible on enterprise segment( platinum membership key monitorable) - better equipped now with broader offerings to engage this segment beyond core offerings

Lowest cost per lead per mgmt in digital universe, large organic traffic and registered users present good opportunity ( was always there but couldn’t monetize in last 2 years per mgmt own admissions)

Unlock phase activates lot of industry which were not doing well for them - Schools, travel, hotel etc

Acquisition universe to stay current base, focus on integration and booster investment per merit - no indication of mad run.

Net net optmist scenario of 25%+ growth in topline in core biz , margins to be around 30%, after 2000 cr cash Market cap is 13K cr for FY 23 at 11-1200 cr revenue and 350 cr-400 cr+ EBDITA - not cheap but not expensive either as long as growth is sustainable and near Monopoly. We are yet to factor acquisition of 1000 cr done in this year. Once market gets delivery confidence, such businesses start to get valuations on few year forward basis( froth did happen here too before sustainable delivery)

Not so clear parts

QIP at 8500+ for 2000 cr, buy back at 6200+ for 100 cr in small time frame - can’t make out the character- smart or opportunistic - given transparency of mgmt, inclined to trust intent and focus on biz delivery for now

Digesting bouquet of Acquisitions and deliver returns on 1000 cr invested, appears overwhelming for both bandwidth and skill set of current team - not even talking insane valuations, would like to see a concrete and measurable plan around integration & delivery , unless idea was to try many and get lucky in some. Time will tell, will be assuring to see some professional help coming in organization.

IMO when IndiaMART’s valuations was very high they tactically did the QIP. Now when start up market is in cash crunch, they have the liquidity and now they are focusing on growth. But didn’t understand the buyback.

Platform businesses are prone to hit by disruption. For such businesses, stability of earning or return on investment has high risk. (not the category of buy…hold and forget !!)

Success of ONDC could hit many platform businesses In such category of businesses… leaders take all and others get crushed under it! (Considering success of UPI, Aadhar done by Nandan Nilekani, there is more probability that ONDC could hit hard to other platform business)

One of the most exciting revelations from the concall was how they have started integrating their older investments into the business. Mgmt mentioned that they have started bundling Vyapar as a free trial for new premium paying customers. So far, about 20% of new customers are availing the free trial. We can assume some of the newer investments also over time will be bundled/cross sold this way. If executed well, this becomes a really really interesting opportunity to monetize the attention that they already have of the SMEs on the platform. If cross selling is effective we start to have really strong value creation opportunities coming into play: 1) Lower churn as the platform is delivering more value , 2) Some sort of commission income from the cross sold products & 3) Since the company is taking minority stakes in these companies, potential for appreciation in value there. This almost seems to be a free option as of today as most market participants are highly skeptical of most of the recent investments done by the company.

Any idea what would be the acceptance ratio at the buyback and it is even justified to just buy some position only for the buyback.

Do note I am ready to add and average down and not currently to size the position

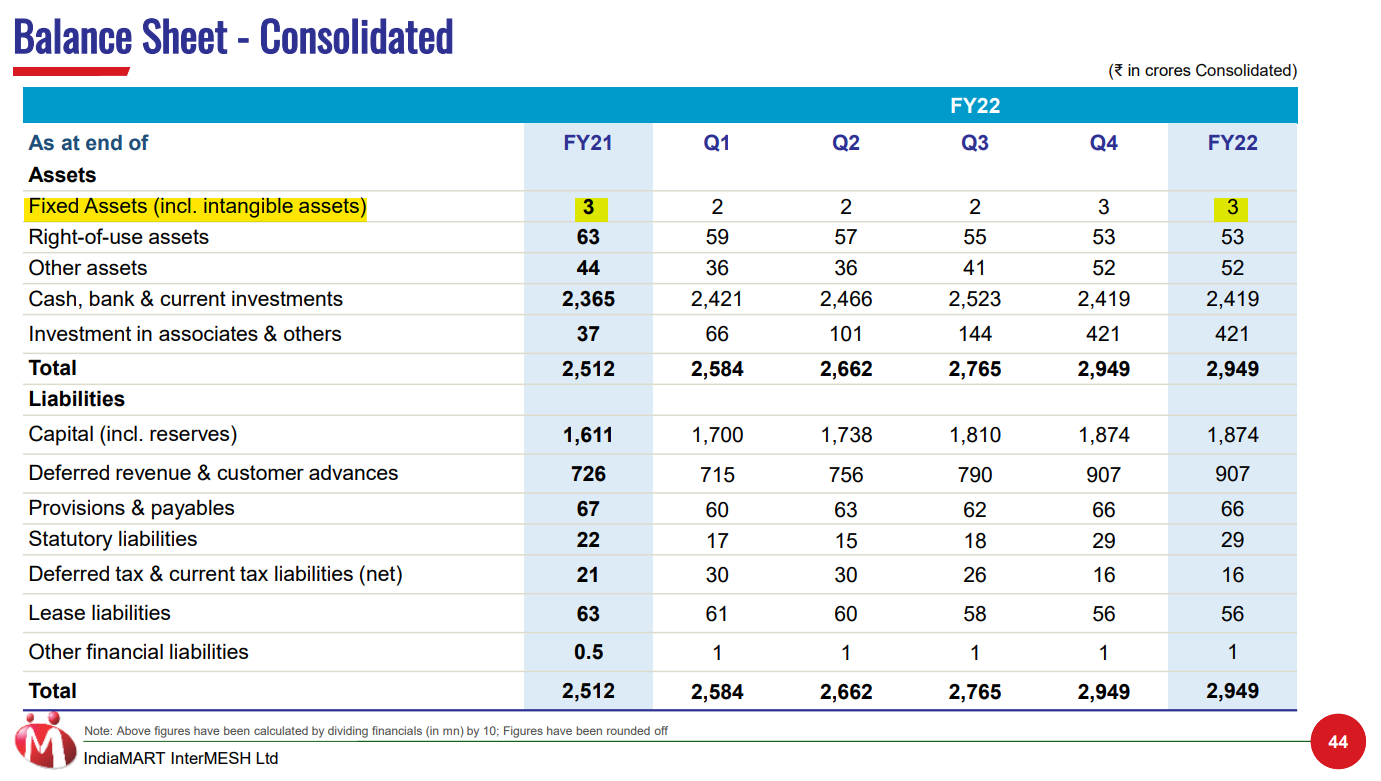

The platform businesses I have seen have a lot of capitalised intangible assets / goodwill due to continuous software development directly or capabilities via acquisitions. Out here intangible assets are flat and no goodwill item seen from the illegible FS. Maybe it’s hidden in ‘Investment in Associates’ since they may be unconsolidated

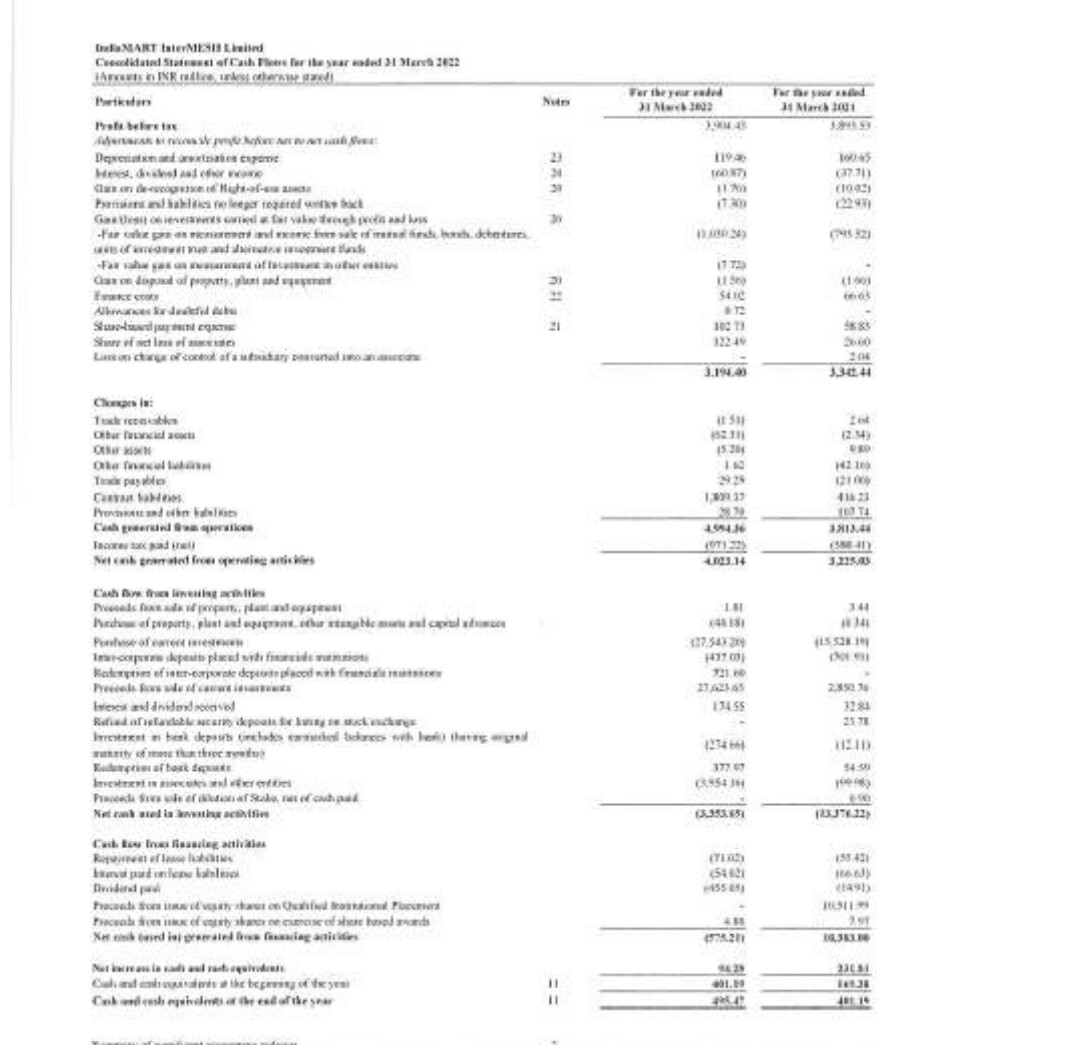

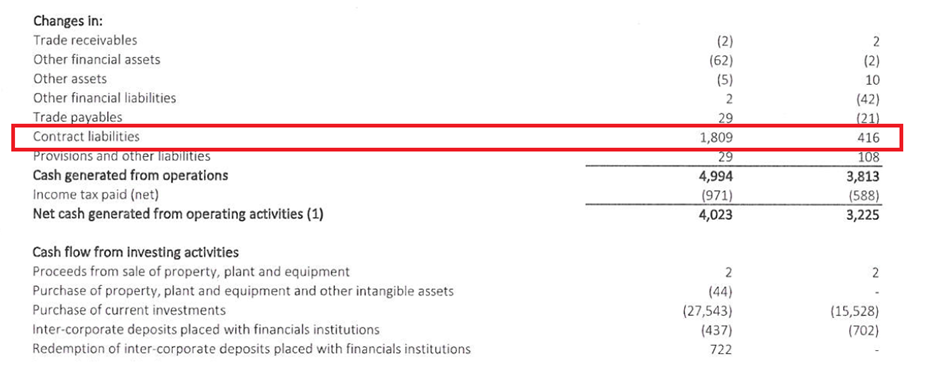

IndiaMart showcases “Deferred Revenue”, i.e payment received in advance for services yet to be provided, to give a leading indicator of its future prospects. This inflates its ‘Cash Flow from Operations’ to the extent that the cash expenses to serve this revenue does not yet appear. We need to thus temper the number (in case you happen to do that rare act these days of finding out free cash )

To find cash generated by the business conducted in FY 22 we need to remove cash contributed by increase in Deferred Revenue. This assumes all the increase in Deferred Revenue flows in cash (there maybe rare accounting loopholes or revenue booked other than cash - unlikely). So ‘CFO earned from revenue served for FY 22’ should atmost be a number arrived at roughly by deducting the increase in Deferred Revenue.

If you look at the slide picked from the presentation here’s what we see

Increase in Deferred Revenue is Rs 181 cr, and CFO is Rs 402 crores. Minus Deferred Revenue cash contribution of Rs 181 cr., CFO is Rs 221 crores. This against PAT of Rs 298 crores. Revenue for FY 22 was Rs 753 crores.

Comparing with last year; increase of Deferred Revenue was Rs 41 crores and CFO was Rs 323 crores. So adjusted for that ‘CFO earned from revenue served for FY 21’ was Rs 282 crores. This against PAT of Rs 280 crores and Revenue of Rs 670 crores.

CFO adjusted for Deferred Revenue has thus deteriorated substantially from Rs 282 crores serving Rs 670 cr of business FY 21 to Rs 221 crores (-22%), now serving Rs 753 crores (+ 12%) in FY 22. This is more bad news as a lot of future revenue is booked and will need to be served more expensively!

Absolutely. The fax has not gone through properly, and the management should have ensured to fax it again a second time. But here is a hint: take the results from the company website, this problem is not present there.

Valid point, thanks for bringing this to attention. This needs to be looked into more closely. I think now with the Rs.500 crore Busy Infotech 100% stake acquisition, going ahead the excess of cash consideration over Book Value should begin to appear as Goodwill.

On the whole point about Deferred Revenue, I have a different view. Your argument is correct from an accounting perspective. However, the very business model is like this and therefore there is no need to exclude this amount from CFO. With the ‘going concern’ assumption, this will recur every year and is certainly a result of the normal business operation. For the current year, since collections spiked towards the end of the year (Q3 & more in Q4), the jump in Deferred Revenue seems high vis-a-vis ‘Revenue served for FY21’. I don’t see this as a negative.

By the way ICYMI, this amount is directly available in Cash Flow Statement and need not be derived from the difference in Deferred Revenue.

I have the same view as @Chandragupta, this logically should be part of CFO. Effectively this is a deeply net negative working capital business where as revenues grow, cash flows will grow faster (just like for eg a strong FMCG business). The ability to collect cash before rendering the services is a sign of the platform power of the business. For arguments sake, if we even were to remove the increase in deferred revenue from the CFO, we would also have to then remove the corresponding costs that went in getting that additional deferred revenue (the customer acquisition cost effectively) which are being expensed in the P&L.

If we take a step back and look at the core platform business, what strikes out at me is that it is effectively an infinite ROE business. The equity in the business is about 1870 cr as of Mar’22 and the cash balance is 2700 cr with 0 debt. Effective capital employed in the core business is about -900 cr which is your deferred revenue. The platform is completely funded with suppliers money. Its basically a cash flow stream growing at 25% that requires no capital investment!

The question is what we do with all the cash that the platform throws out. If the company is able to deepen the moats via these minority investments and create a decent ROI while doing so, that becomes a really powerful proposition.

Just surprising that the entire audit report except FS has gone through properly. Even in the FS the digital signature of the auditor is clear.

I think I am going to struggle re-making my point on my post on Deferred Revenue.

Deferred Revenue is not revenue but expected revenue over many years, paid in advance.

That revenue is yet to be earned.

To earn that revenue, expenses are yet to be borne.

If expenses to be borne to earn that revenue is higher than in the past, the economic performance will be weaker, and if vice-versa, stronger. Hypothetically if the expenses borne are higher than revenue then you could end up in a loss…unlikely to be the case here, but just making the point better.

So it’s important to know whether such Deferred Revenue earned in the past and booked this year is generating better cash.

One way to do that is to remove increase in cash provided by deferred revenue and see how much cash you have generated. This cash will be on account of earning revenue this year - which comes from Deferred Revenue in previous years and Revenue earned this year.

You are correct to indicate that we need to remove expenses accrued this year to earn Deferred Revenue, and also add expenses of the previous years for this year’s Deferred Revenue earned. You can do that exercise and you will find conclusions don’t change.

It’s deceptive to think that cash from a lot of Deferred Revenue makes it a negative working capital business. In a well run FMCG business, cash from earning revenue comes before paying cash to suppliers/other expenses against that revenue - there is nothing more to be done, thus it is called as negative working capital. In this business cash is taken but spends are yet to be made to earn that cash. This cash is cash that is owed to the customer till you earn it, it’s just customer’s cash sitting in your bank account and that cash is against a ‘liability’ because you have to fulfil your contract (vs say ‘inventory’ in an FMCG).

The cost of fulfilling that contract may exceed the cash taken (imagine if certain performance guarantees are provided that makes it costlier to achieve). Or, as is often seen to happen in a fixed cost business - to be clear, IndiaMart is not, excessive focus on Deferred Revenue will incentivise making future promises, and that may be difficult to achieve, especially in an inflationary environment.

(one indicator is to check how much of the Deferred Revenue they said they will earn in year 1 was earned - the AR provides that)

I really have no intelligent thoughts on whether IndiaMart’s valuation is good or bad, but just this specific point that if a business has Deferred Revenue, then we may have to look at cash generated a little differently.

Fantastic Post, thanks for articulating your views, it really made me think. I have to say, I am starting to come around to your view!

You are absolutely right, thanks for the explanation. It is a very important distinction. I guess a better example would be more a real estate company that collects some of the cash upfront but still has to incur the actual cost of constructing the building. If the construction costs go up meaningfully in the meantime, then the contracts we hold are far less profitable.

Agreed. Just to take this example to an extreme. If we assume the cost of fulfilling the contract is more than the cash collected (unprofitable business); that is basically what a ponzi scheme would look like. Obviously Indiamart still makes money and is a highly profitable business and is in no way a ponzi scheme.

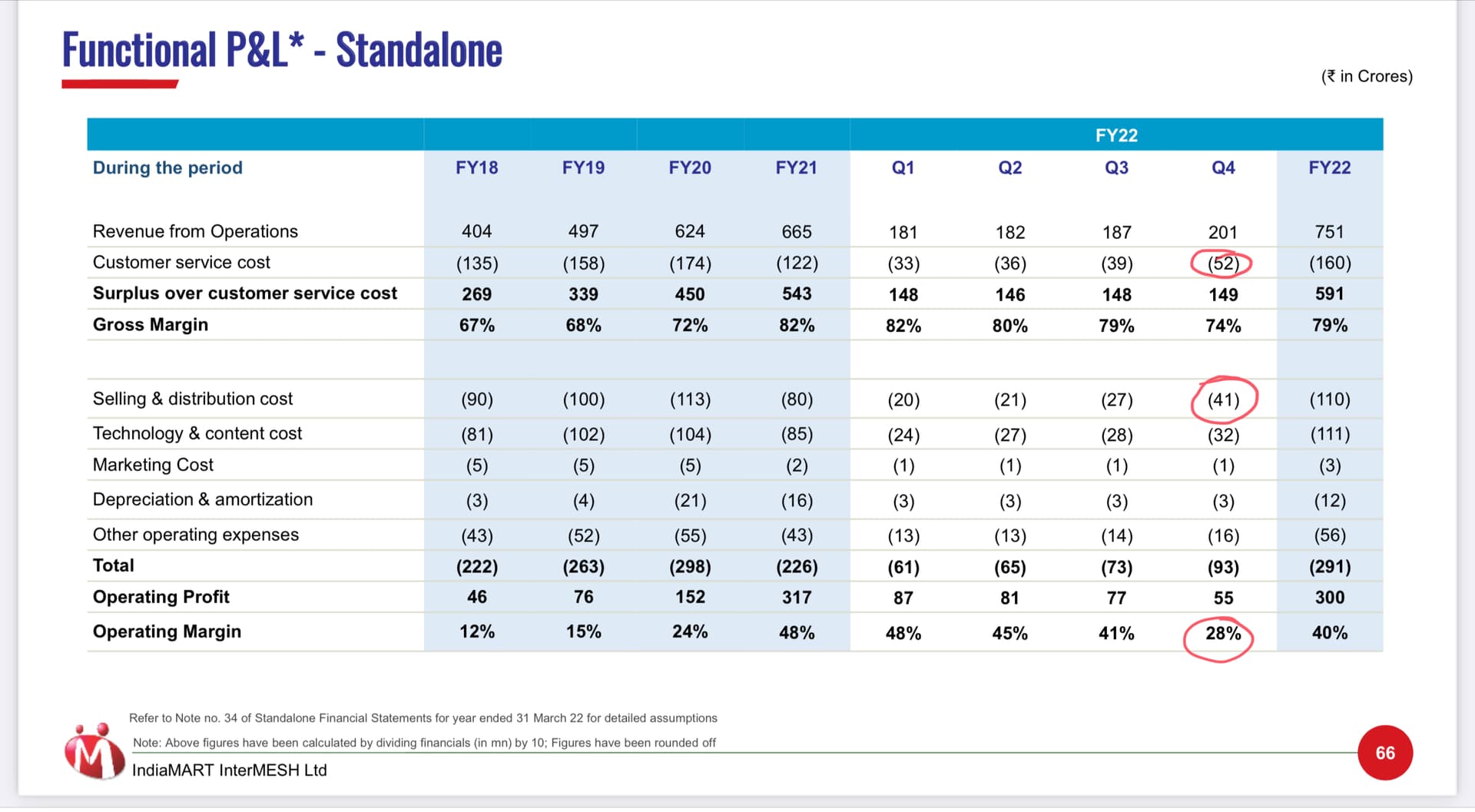

I guess what we need to do is differentiate the cost of acquisition from the cost of servicing. Luckily the company breaks those up (if we chose to believe those numbers). They do point to some of what you were saying. The direct cost of servicing has gone up from 18% in FY21 to 26% in Q4FY22. An equally large impact on the margins is on the increase in sales staff cost. This has gone up from 27 cr in Q3FY22 to 41 cr in Q4FY22. However, the company also acquired 2x the number of paid subscribers in Q4 as compared to Q3; so there seems to be no increase in the absolute cost of acquisition per customer and we would expect the other expenses (technology, content and marketing) to be somewhat fixed and come down with scale.

I really don’t understand this strategy of so many small minority investments. It is like not having enough conviction in any investment.

Out of 100cr buyback, 50% will go back to promoters and only 160000 are being bought back our of 3cr shares which means only 0.005% or if you surrender 200 share 1 will get accepted. Looks like designed to benefit promoters.

Yeah - of the Rs 100 crores of buyback, ~ 49.19 crores will go to the promoters in return for a 0.52% or more reduction in their holding.

More importantly, they pay zero tax as the buyback tax is paid by the company. The company bears the 20%++ cost of this payout, i.e. ~ Rs 23 crores. (this is very very very rough, exact computation is quite unclear)

Promoters and others who tender thus cash out at 41% higher than CMP as of last closing; tax free. The remaining shareholders (including Promoters) will have to bear this non-tax deductible cost that amounts to ~ 8% of FY 22 PAT. If it becomes an annual feature (like TCS) then this will impact the intrinsic value.

To be sure this has got nothing to do with Indiamart Promoters but the lopsided tax rules here that ostensibly began with plugging tax loopholes, but ended up creating new ones with perverse incentives.

Taxes on dividends were increased over time from zero to maximum marginal tax rate, leading shareholders to increasingly prefer buybacks to minimise frictional costs by way of taxes, to distribute earnings. The frictional cost via Buybacks was zero to less than 10%.

To plug this loophole Buyback tax was introduced, taxing ~ 20%++ on the difference between share price paid and bought pack (on a FIFO basis but not very clear in case of complications).

This tax is to be paid by the company and not by the tendering shareholders! Amount received by the tendering shareholder is free of tax in his hands.

Thus, it is the remaining shareholders who did not tender their shares who pay the tax for the shareholders’ shares bought out! Whoa

This buyback tax remains lower than the only other way of distributing earnings of a company, i.e. dividends.

Dividends, which were initially tax free, are now taxed at maximum marginal tax rate that is higher than 20%++ buyback tax

This created a new loop-hole. Take money out of the company tax free by giving your shares in return; while creating tax liability on the company

Now if the object is to take money out of the company with no tax implications on the tenderer, then it incentivizes to price the buyback as high as possible, especially for the Promoter who typically decides the price.

Why is that?

(a) Buyback is generally thought of as a ‘fair-value’ transaction; i.e. for the tenderer I give up one share (or all future earnings of the company) and get company decided present value i.e. buyback price.; and for the Company (i.e. remaining shareholders); I will now get share of rights to the earnings of the tenderer as well since for the same earnings so I will get more for my share as there are fewer shares around. Not with the Buyback tax

(b) Buyback now incentivizes a lopsided transaction; i.e. to now think of Buyback as selling your shares at a highest price without paying tax; and at a price that you (the Promoter) are free to fix! So you better fix the price much higher than what you think to be its fair value, and be sure to tender as much shares as you can (which is why buyback where Promoters don’t tender is nearly gone). It’s like selling a certain number of your shares at a price you want, without paying taxes on it!

(c) The Buyback price also sends wrong signals about what the company thinks to be its intrinsic value, because while in theory a Buyback is to be conceived by the Company to get more than it gives (i.e. share for cash); but in practice enables the fixer of the buyback price (who also runs the Company) to sell his shares at the best price. Which is why generally you will find buyback prices in the last few years have been much higher than market prices.

(d) Buyback disincentivizes dividends in some cases and not in some other (where Promoter would like to receive dividends and is taxed less - typically MNC ones). This has problems for those who prefer receiving steady dividends and do not want to engage in such transactions as above to distribute earnings.

(e) The gullible ones (every market has some) thinking Buyback is at a fair value might not tender, or may buy more thinking he is getting a good discount to fair value (Buyback price) in the open market. The tenderers profit at their cost.

There is fundamental flaw in your analysis. Buyback give benefit to other shareholders by increasing EPS. IMO, buyback is win-win for every stakeholders.

I will always choose companies doing buyback over those who are giving dividends.