When I look at the core product - IndiaMart website and app - it seems woefully substandard compared to good B2C apps. If IndiaMart has 100 cr to spray at minority positions in a bunch of startups, I wonder why they don’t also invest 100 cr to hire 100 quality designers/ developers for 2 years to improve the core product. Or maybe good UI/UX doesn’t matter to their customer base -– yet.

There are many things that may affect this first is what they want to target and the answer is businessmen of SME etc and that might not be any advantage of getting better UI/UX and more things to do with their algo and speed of the site.

Also to note most people will not like a more hard and fancy website or app to be there as in reality most people are not that well rounded with tech in India and may prefer a simple website than a more fancy good one.

Also, the benefit might be more shallow and unjustified in their eyes also to know their target audience is mid-age people that have their own business than young adults and teenagers.

They should work on it but even as a person who values UI still can’t justify this investment just look at Alibaba website and compare.

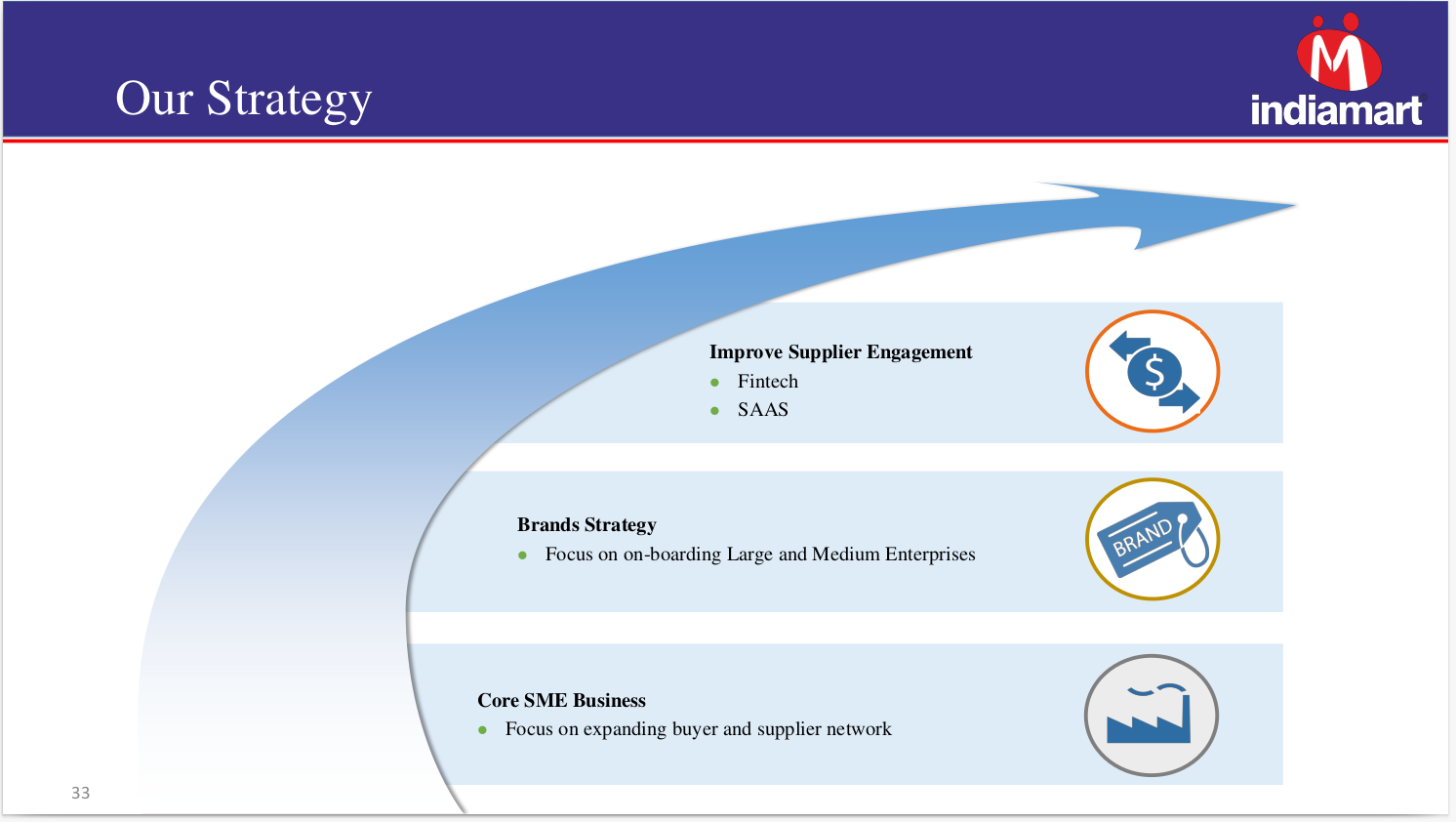

They have generally not used the term “Large Enterprises” earlier, sticking to either SME / MSMEs or the more generic “B2B”. Anything to read into this?

I did a little digging on the timeline of these Enterprise Solutions they are offering and the term Large Enterprises.

They have been using this slide (with slight design/format changes) since their first quarterly results and the investor presentation (Dated 31st July, 2019). This seems to be the first reference to the term Large Enterprises.

On the website they’ve mentioned following as part of their Enterprise Solutions:

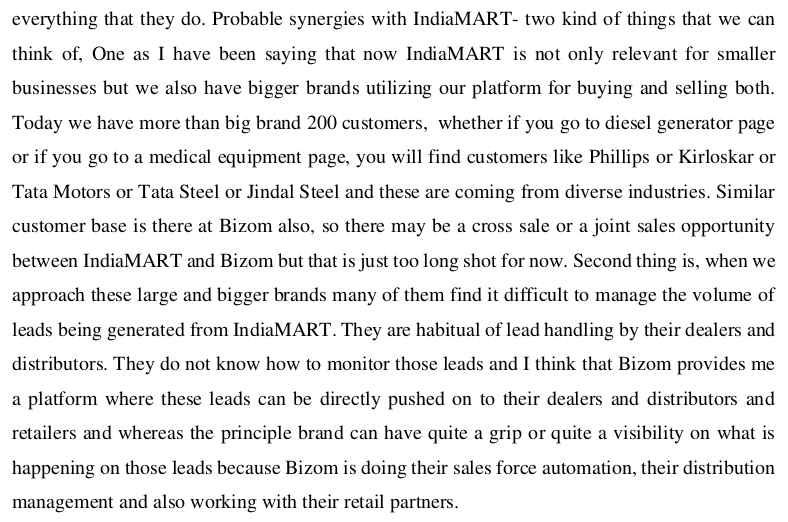

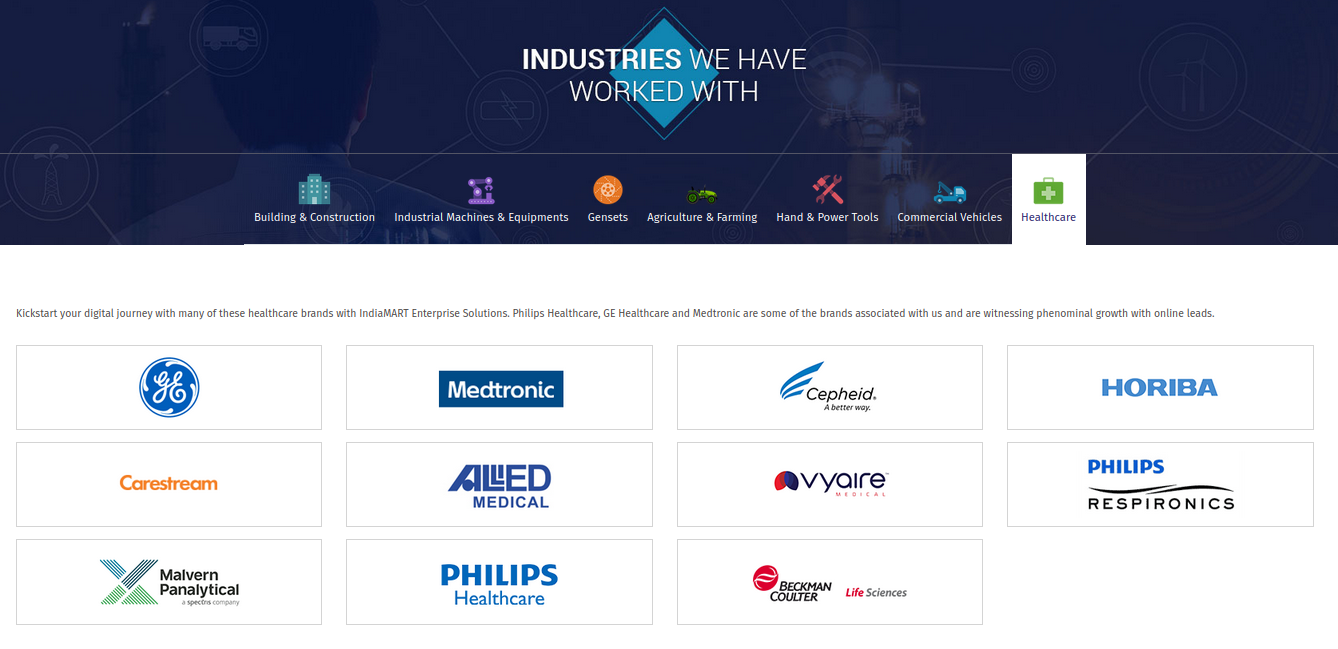

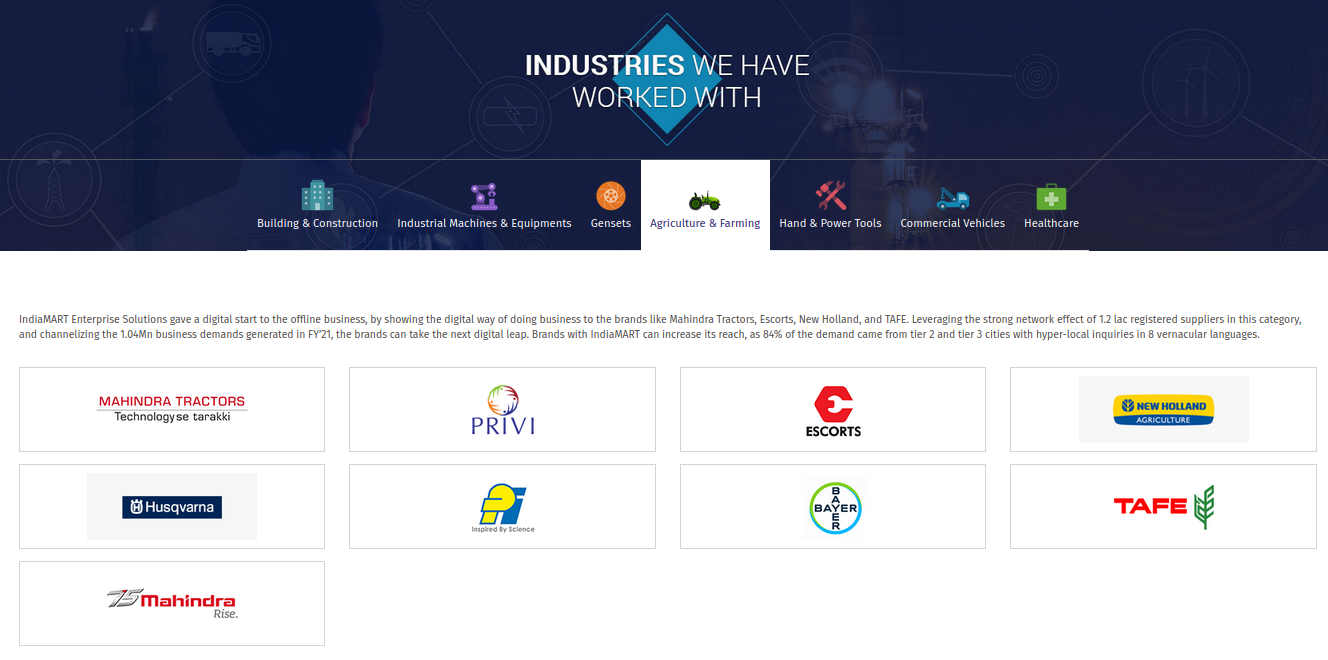

They spoke about briefly about big brands associated with them and the problems they face. Also explained how their investment in Mobisy, who developed Bizom, helps tackle some of these problems.

They seem to have been working actively towards these solutions since last 2 years it seems.

In Feb 2020, Sany, a Chinese multinational heavy equipment manufacturing company with mcap of USD 27.12 Billion opted for the Indiamart Enterprise Solutions.

They have a few numbers of posts on their Twitter as well Linkedin profile which might be a part of the “Digital Advertising” Enterprise Solution. The earliest post on their LinkedIn feed seems to be from around a year ago.

The list of big companies they work with is quite impressive:

I recently attended a webinar conducted by India Independent Insights (Nitin Mangal and Pranav Bhavsar) on Indiamart. They have done independent analysis on projected growth of Indiamart based on information available in public domain. Please note that this analysis was done only on the core business of Indiamart and does NOT factor in any recent acquisitions

Some key takeaways (based on data analysis):

Bullish growth projections may need to be tempered as their key “actual” addressable market of MSMEs is limited

ARPU absolute numbers are not reconciling with management commentary. Their analysis shows ARPU numbers to be lower for a large set of customers. The most likely explanation could be that it is offering deep discounts to new / existing customers. Nothing wrong in this, however management has not mentioned this fact in concalls

The growth projections based on number of suppliers listed on the portal or those having trusted seals will give misleading picture as many supplier entries look dodgy or outright funny (like Dabur is listed as supplier selling biscuits…there are many more such entries or large enterprises as well including bajaj finance and other well known names). Indiamart did mention in DRHP that they many times create supplier entries on their own and then approach potential customers for official conversion. However it seems many people forget this fact and take supplier numbers on face value. Hence total listed/verified/trust seal suppliers on website is not a reliable metric . This point was also raised earlier in this forum

Their were observations on deferred revenue recognition where data analytics suggest there is deviation from standard practices. No harm in this as long as management provides reasons for the same which was not observed in the current company reports.

Last 3-4 years of analytics shows employee base is growing but PF contribution going down. Also reported outsourced employee cost is much higher vs independent quotations received from similar vendors for similar work

Please note: This is not a call out that management is fraud or accounts are fishy. It is just an independent data analysis based on information available in public domain and is done from education perspective. They have not sought any clarification from management on above points as per their standard practice.

The broad conclusion of the webinar was that future growth of their core business may not be very strong and that could be one of the possible reasons management was going down the path of acquisitions

Not exactly sure about why the futures are in so much discount but one reason could be that the QIB lock-in period is expiring…

Indiamart had issued some shares exactly an year back to QIB and their lock-in is expiring… So they may have shorted in futures as they intent to exit their holdings…

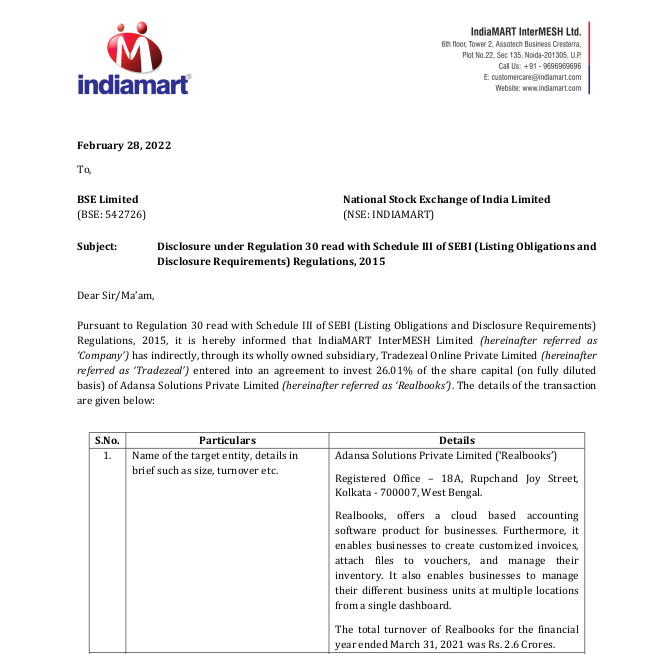

One more acquisition announced in the accounting software sector. Bought 26.01% stake in Adansa Solutions Pvt Ltd via CCPS + Equity route for Rs. 13.75 Crores. The company has developed Realbooks which is a cloud based accounting software product for businesses.

Lots of Investment happening is Startup by IndiaMart. Are they trying to take away the focus of investors from their current performance to startup investments?

I had similar thoughts. With so many acquisitions/investments, valuing the business, growth and modelling the cashflow is gonna become a challenge in near future.

If they continue with this then yes it can be a struggle to generate free cash flow but looking at recent most can easily be funded by their current cashflows+reserves as no recent debt or equity dilution is done to fund these.

Just by looking at recent acquisition and investment they at least are very related to the core business and may act as an addon even management is saying they are working on integrating at least if we see their full-on acquisition of BuildDesk but will they be able to do the same with other deals where they hold minority or majority stake.

Their valuation of some recent looks quite steep, especially the last 3 is a little bit overvalued in my personal opinion.

Does this new entry of giant like L&T will affect IndiaMART growth.

Yes L&T focus on only some segment ie infra only.

With there new initiatives L&T-SuFin.

Besides being an investor ; I am an Indiamart user for the past 7-8 years of which i am a paid subscriber for last 4-5 years and my experience as a user made me look into the company for investing. A few points which I think about the core business

Network effect - currently I draw appx 5-10 % revenue from new or repeated customers which were connected to me via IndiaMART and it’s so essential for me today that i have 2 dedicated Telecallers working only on IndiaMART leads since it’s the go to place for business leads ( much ahead of justdial, exporters india, trademart etc)

Ever evolving platform - the back end team is very dynamic since they keep on improving the interface and add relevant features regularly. This I think will keep them ahead of the Competition and 2-3 years down the line I won’t be surprised if it gets integrated into a full- featured SaaS CRM kind of platform, for which many companies like mine are paying additional subscription, it’s a good opportunity !

Acquisitions - this is the pain point, as a user I have not been able to derive any material benefit from accounting, logistics et al recent acquisitions. Nor have I ever received any calls or mails from indiamart for cross selling these products which the company claims is a huge opportunity for them. So I would be interested to see how these acquisitions pan out for IndiaMART.

Valuations - not very worried, given the interface maintains it’s lead over others, the new generation is preferring this model for generating business and I think there is a good addressable market without much competition since the network effect would take care of repeated subscription and new customer addition.

Thankyou for sharing your experience and insight…really valuable.

Great to hear some of the strengths of the company, and it is clear that they are ahead of the competition, so that is the good part.

However I am still looking for data points on core hypothesis - whether the growth will be really fast or we need to temper expectations on that front. Management itself is guiding for only 15-20% growth, hence lofty valuations do become a concern if execution does not happen.

Also, remember that businesses evolve all the time and so does competition. So we need to keep verifying hypothesis with numbers as we move forward.

Thanks again for valuable inputs. Much appreciated!

Growth - As far as growth is concerned I don’t think it’s gonna be exponential, think we need to be comfortable with 15-18% in topline but bottomline can be higher due to operating leverage in these types of businesses.

Dividend / buyback - the company is doing acquisitions right now since it has spare cash, but 2-3 years down the line if it doesn’t have any inorganic growth opportunity and the core biz would be churning out returns at a regular rate, there is a possibility of buyback or dividends.

Valuations - 12000 cr m-cap is not cheap for 150 odd cr NP, but if it is able to maintain the topline growth of doubling in five years (330 in 2017 to 660 in '21) which I think is reasonable given various acquisitions other than core biz, bottom line can triple to 500-600 cr (last year NP was 280, I am considering the year before it) - I think it’s a long term play, many ifs and buts can come in picture but the pool in terms of addressable market in India is big.

I may be having some biases since I am a user as well as an investor looking to add more on dips, so kindly infer the above in that context!