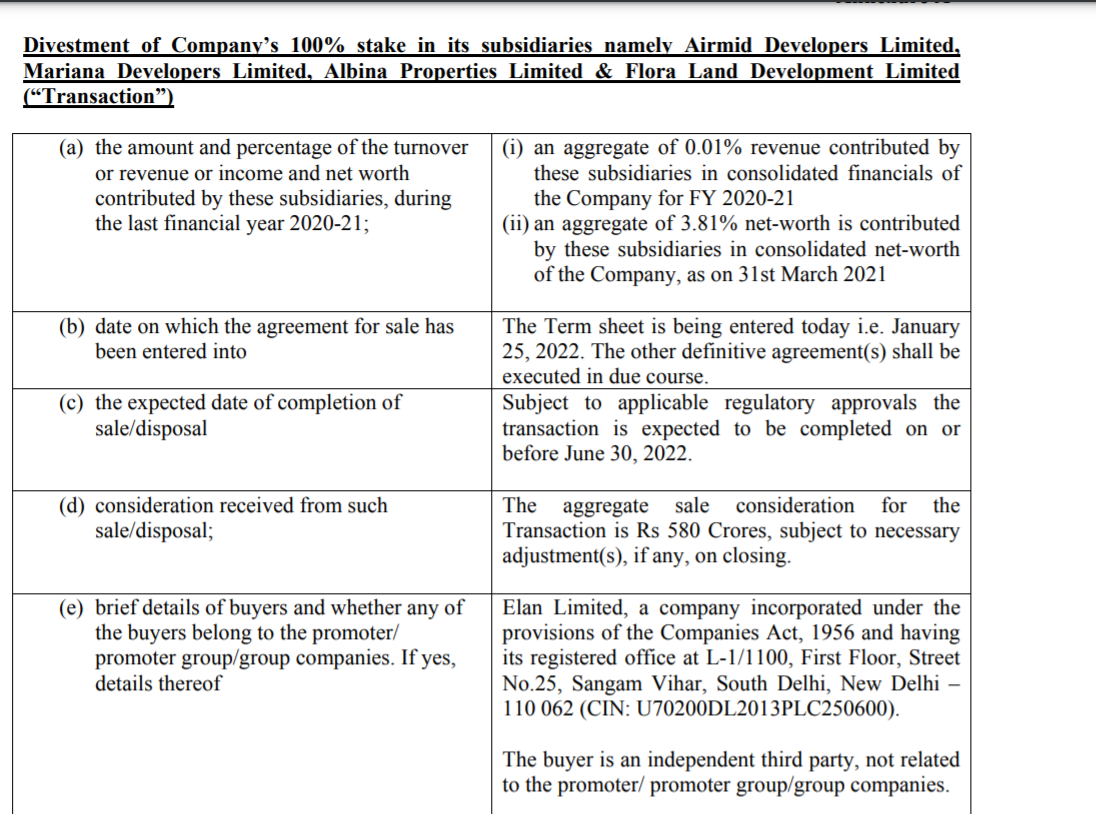

The Company is going to Divest 100% stake in its subsidiaries Airmid Developers Limited, Mariana Developers Limited, Albina Properties Limited & Flora Land Development Limited.

Going to receive 580 Crores for the sale.

The Company is going to Divest 100% stake in its subsidiaries Airmid Developers Limited, Mariana Developers Limited, Albina Properties Limited & Flora Land Development Limited.

Hi ,

On the latest results , was wondering why the co. has been making losses and sales going down in a real estate upcycle. I understand the co. is looked at more as Embassy now than IBREL and so not much emphasis on the results. But stll is there any specific reason why IBREL can’t focus on growing sales and profitability. Would be great if the learned members can shed some light on the same.

Disc: Invested

Real estate companies cannot be evaluated on the basis of P&L because they follow project completion method or POCM to recognize revenue. It simply means whatever sales they achieve gets recognized in their books 2-3 years later depending upon the construction progress.

Some key variables to track is booking value, booking volume, debt, collections, deal pipeline, launch pipeline, leasing income etc.

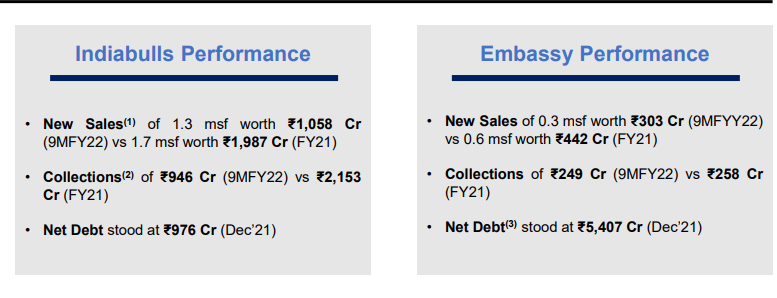

New sales in IB is poor for this quarter especially when most RE companies are reporting bumper sales volume. It may be useful to dig deeper on the reasons for their low sales this quarter.

Hope this helps.

How much dilution for minority shareholders, any one have those calculations?

Form current 62% of public holding you go down to ~26% in the merged entity.

Thanks. Would it affect our buying price? For example, if I buy at 125 today — would it mean that post merger, price would go down to 50 (around 60% decline?). Or, this is already priced in?

Price wouldn’t decline, your ownership in the standalone pre merger company will dilute post merger. For example, if you own 1% of IBREAL today, post merger, you would own 0.5% of the merged company.

Above are just made up numbers to help explain, actual dilution ratio will differ.

From 45.6cr, the new merged company will have 100.8cr shares.

Yes, no of shares go up. But, the market cap won’t change, right?

So, per share value should go down. Sorry if it is a very basic question.

Number of shares will go up and in proportion the market cap of the company will also go up. Price of share will remain same.

Is this the housing finance entity or the real estate entity? Seems about an old case

Seeing IT raids is definitely a red flag.

However just a thought that if money siphoned from the company is brought to books, is it not good for the shareholders?

A company run by dishonest promoters will see severe derating that’s for sure.

Disc:

1% pf invested

If I am not wrong, Mr. Sameer Gahlaut is not the promoter of Indiabulls real estate any more. They have already converted themselves into Public shareholders.

If you are bored of conspiracy theories, ED raids & social media bashing, do analysis on IBRE recent price action post approvals.

Hint : Search 5407 cr on 12 Feb presentation uploaded on exchanges and see the impact. It’s the first time this number has been disclosed

THis is tweet of Mr Amit Kumar Gupta, a special situation specialist. Can seniors throw more light

5407 crores is the debt of embassy .

Net debt of Embassy Group was disclosed earlier at 4300 odd crores. Now, that has gone upto 5400 crores it seems.

Also, the company has committed to reduce the debt of the merged entity to about 3700 crores, during merger.

So, the fall must not exactly be related to this in my opinion.

Disc- Invested

I was again through this numbers which got me puzzled why their sales got reduced even for embassy it is flattish when other players are increasing . Going by this number their Q4 will also get impacted

Their planned inventory provide good scope for rerating

one project i personally track which is near to my home is embassy taurus project

QIP was announced during Feb 7 where market price was 144 and now down by 30% . How they will set the QIP price will be an interesting thing to watch

Qip issue price 106.38

a0c6c648-8999-455b-9216-61d1ea60aca0.pdf (361.6 KB)

Some interesting snippets from the QIP document. https://www.indiabullsrealestate.com/qip/

No access to capital for tier-2 unbranded developers

Since 2012, non-banking financing companies (“NBFCs”) have been the largest lenders for the real estate projects. Indiscriminate lending by NBFCs to tier-2 unbranded developers led to a significant increase in the supply of under-construction projects. Due to lack of experience in executing and completing the projects, tier-2 unbranded developers delayed their projects significantly, which resulted in loss of customer confidence. Further, in order to compete with tier-1 branded developers, tier-2 unbranded developers often resorted to price-cuts, which further eroded their profitability. However, they were able to continue with this business model due to ample liquidity present in the system prior to 2018. While project delays jeopardised cash flows for these projects, NBFCs continued to refinance and provide incremental capital for project completions. In September 2018, the Infrastructure Leasing and Financial Services (“IL&FS”) crisis caused a severe liquidity crunch. Thereafter, NBFCs significantly reduced real estate funding during the under-construction phase, which led to low sales and poor cash flow management for the developers, especially smaller developers with limited access to bank loans. Since tier-1 branded developers were able to sell substantially at the time of launch and throughout the under-construction phase, limited financing was required for the completion of under-construction projects. Most of the tier-1 branded developers also had access to bank loans, and were able to complete under-construction projects on time. The dramatic fall in incremental credit from banks and NBFCs to developers resulted in most of the tier-2 unbranded developers being unable to continue existing projects as well as launch new projects. Such tier-2 unbranded developers along with the financial institutions who supported them are now looking at tier-1 branded developers to rescue those projects by taking over existing projects or establishing tie-ups for their new land parcels.

JDA (Joint Development Arrangement) model once again picking up

Post IL&FS crisis and COVID-19 led lockdowns, several of the landowners and unorganized developers have come under stress. Lenders associated with these entities along with the landowners are often approaching the tier-1 branded players to tie-up JDA deals. Given the state of the industry, deals which are now being signed are win-win for both the parties. Typical JDAs which are being signed up have the following characteristics from the lens of tier-1 branded players:

(i) Upfront investment: Typical JDAs require the tier-1 branded developers to deploy capital equivalent to 5%-6% of the GDV (Gross Development Value) in markets like MMR & Pune. This is often in the form of refundable deposits.

(ii) Profit margin: A branded player with a good execution track record can generally achieve 18-20% PBT margin on such projects. Typically, if the sales planning is good and execution is as per the plan then there is a potential to generate upwards of 50% ROEs from such projects as the upfront investment requirement is low.

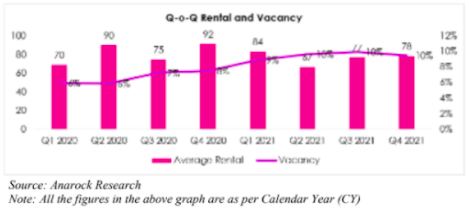

Quarterly Office Rentals and Vacancy Trends For The Last 2 Years

There have been fluctuations in office rentals in Bengaluru especially from 3rd quarter 2020. Rental dropped from INR 90 per sq.ft. per month to INR 75 per sq. ft. per month from Q2 2020 to Q3 2020. However, it increased to INR 92 per sq. ft. per month in the subsequent quarter. Bengaluru office rentals have shown bounce back after each drop in rental. The vacancy has been increasing especially since Q3 2020. Q4 2021 has shown signs of recovery in vacancy with a marginal reduction.

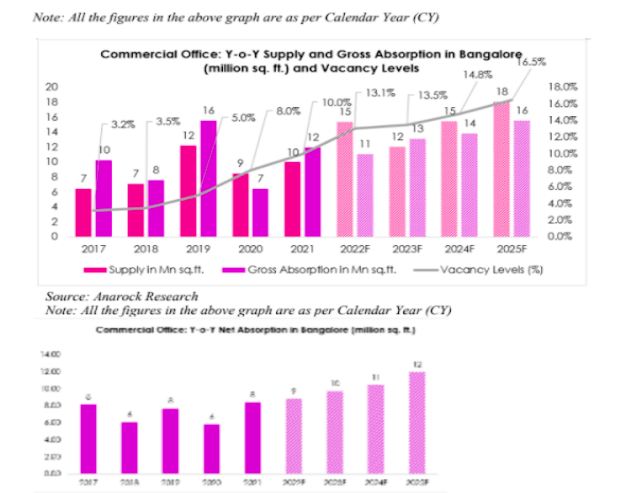

Annual Office Absorption, Supply and Vacancy Trends For Last 5 Years & Future Outlook Till 2025

Supply and Absorption witnessed a decrease in 2020 due to the COVID-19 pandemic outbreak. Year 2021 witnessed recovery in supply and new absorption. Supply is expected to witness a peak in the year 2022 with the completion of office buildings especially in North and East markets of Bengaluru. Absorption is expected to come back to the pre-pandemic levels by the year 2025.

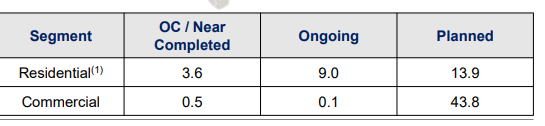

Land Bank, Residential Stock and Commercial stock vis a vis competition

Disc: Tracking

Value distructive allotment

fbd10ed0-4283-42ab-aedb-18f8e4918494.pdf (443.7 KB)

Dis one of the largest bet

Do explain as to why you think it is value destructive.