No impact. Prudent exercise by management to create confidence in Foreign investors on repayment assurance.

1 Like

I agree with this analysis, I am getting veey similar figures. I assumed a networth of 25k but it all depends on dividend payout. Anyways, PAT is expected to be min 4000cr.

Given all this, I am very surprised at why DIIs are not showing interest. What is the anti thesis here?

I do not see any capital risk, maybe lower ROA but with Aset light model, ROE is more apt. Eitherway, I do not understand the downside risk that market seems to be assigning here.

2 Likes

The company has Rs 37,380 Cr of legacy loans (housing + developer finance) on their balance sheet as of June 2024 as per their Q1 earnings update. The market seems to be saying that all of this book will likely go bad (maybe that’s why they haven’t been able to unload it yet in the first place) and given their track record of 70% recovery from bad loans, the hit will be to the tune of Rs 11,000 Cr. Hence, discounting the same from their current net worth of Rs 20,000 Cr gives you Rs 9000 odd Cr of market cap.

However,

a) the company already has imputed provisions of Rs 6000 odd Cr from the written off pool which the market is not accounting for, and

b) not all or even a majority of the legacy book is likely to go bad (my opinion)

Nevertheless,

The management seems to be indicating that a substantial portion of the legacy book is likely to be unwound after requiring some provisioning and that’s why there is no talk of write-back of provisions from the expected recoveries (and all the jargon around “tactical” actions to reduce the legacy book which is nothing but another way of saying that we will require to provide for some part of the outstanding legacy loan book before either offloading it or running it down over the normal course of loan repayment)

Lastly,

All of this ultra cautious approach could also be a ploy by the management to keep the share price depressed till 30-Sep-2024 when the optional put option will be exercised by the FCCB holders. If the share price were to rise before that, the FCCB holders could simply exercise the conversion option and add 5 Cr shares to the already large number of diluted shares after the Rights Issue. The FCCB conversion price is somewhere in the handle of 200 Rs per share but am not sure.

The management is also working on another ESOP plan which was approved by the board in Feb 2024 but implementation was deferred till after all the name change and KRAs for performance evaluation (the eight metrics they started reporting on since Q1)

were implemented. Lower the stock price, lower the strike price for their ESOPs since ESOPs are awarded at the market price of the day to avoid P&L hit.

My take on business performance going forward -

The increase in profitability will be gradual but steady over the course of next 8 quarters. The management will ensure that there are no surprises on the positive or negative side going forward. Not sure about the figure of 4000 Cr p.a. as I still don’t understand how the ROE of 18% will be achieved without substantial leverage. If the 18% ROE is after accounting for provision write-back sometime after 2027, then it is not sustainable.

At some point well within the next two years, the market will get enthused by the steadily rising asset light AUM and earnings as well as reducing legacy book and assign a higher book multiple to the share.

Disc: Invested with a large holding

9 Likes

Thanks for the detailed response. IMHO as well, legacy book issue must have been known by now for most part of it. There is no incentive for management to hide a big negative surprise until later.

As for FCCB, I think it was like 240rs. In one of previous con calls, MD mentioned that he is confident about foreign lenders converting them to equities. He put it as positive and they are confident in the business, etc etc. It was when the share was above 200rs. Lets see what happens. We will know soon.

I have not thought about leverage due to asset-light model. Don’t really know how much % percent co. will keep in its balance sheet for each of partner banks. But 1 lakh crore is indeed a decent growth number with 18% ROE.

Management ESOPs is a great motivator for sure. For all these troubles, none of senior management left the company. There must be some good incentives in play.

p.s: Invested.

3 Likes

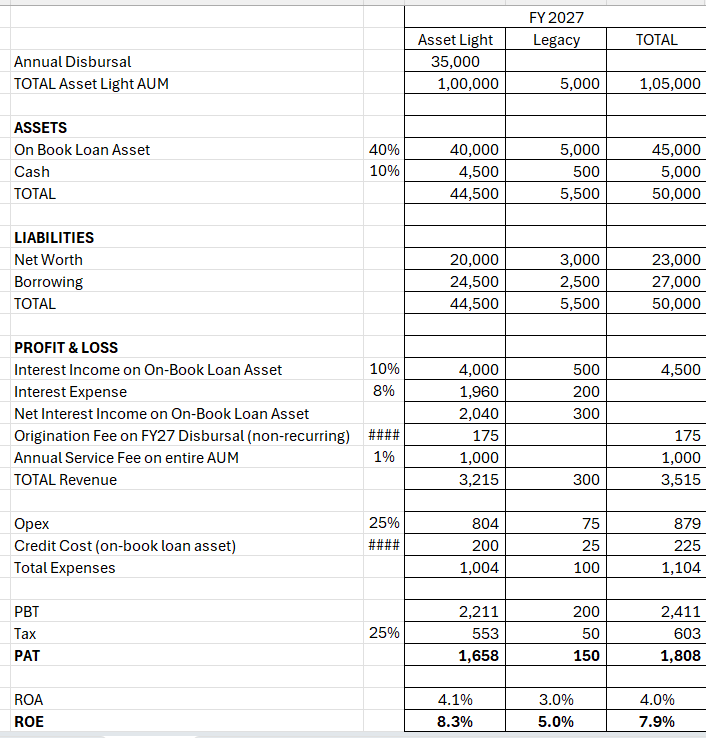

Hi,

Here is a rough calculation of how the FY2027 numbers will look like taking management’s word. In my view, without accounting for write-back of provisions, the company can’t have anywhere close to Rs 4000 Cr PAT. Further, without considering substantial leverage (much higher than the 2x gearing the company is guiding for), 18% ROE from ongoing business cannot be generated.

Comments and critique invited

Excel Attached

Sammaan FY2027.xlsx (12.2 KB)

1 Like

Thanks for insight by learned contributors.

Can someone also project Book Value for FY26 or 27 with all foreseen Equity Dilution ?

1 Like