No

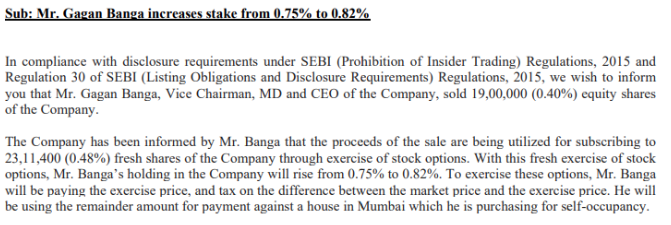

Impact on Gagan Banga stake !!

This is done to meet ESOP payments and tax outflows.

Many a times, insiders have to sell their shares in open market to pay for their ESOPs, as they do not have any other major assets.

Company has explained this in their filing here:

2 Likes

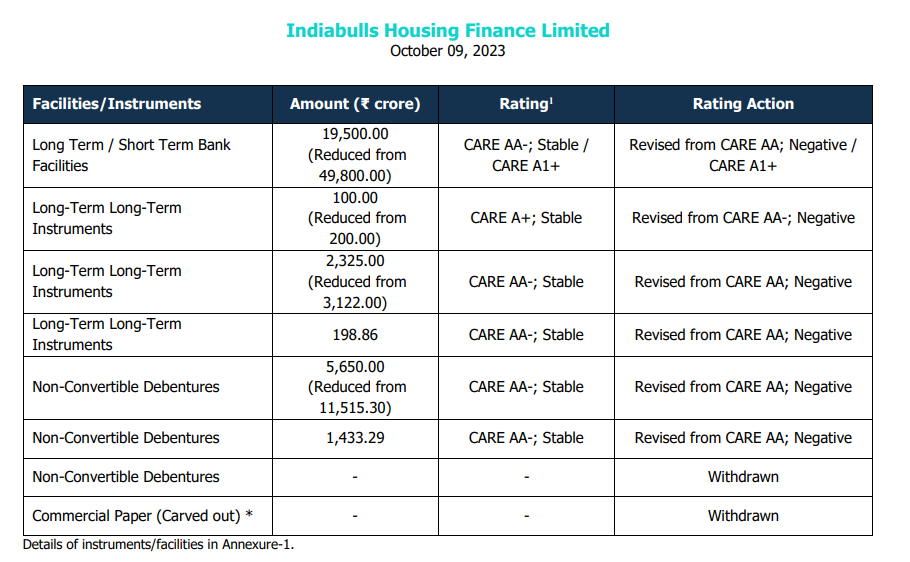

CARE downgraded IBHL from AA to AA-. CARE rightly pointed out the high cost of funding issues in the company.

1 Like

I feel the concerns raised are fair but reflect only some aspects of business. IHF management has expressed their dissent and market also seems to have digested the rating change.

IHF current management has been very conservative till date and rightly so considering the reputation of old promoters. I fail to understand the rating downgrade by CARE now and not in last 2/3 years when situation was far more worse. Seems some big players have shorted IHF and looking for opportunities to cover by influencing some News.

I will love to see them getting trapped as in that scenario movement of IHF from 175 levels to 215 level will be very fast.

I being a long term investor am always looking for any opportunity to add below 170 levels,

6 Likes

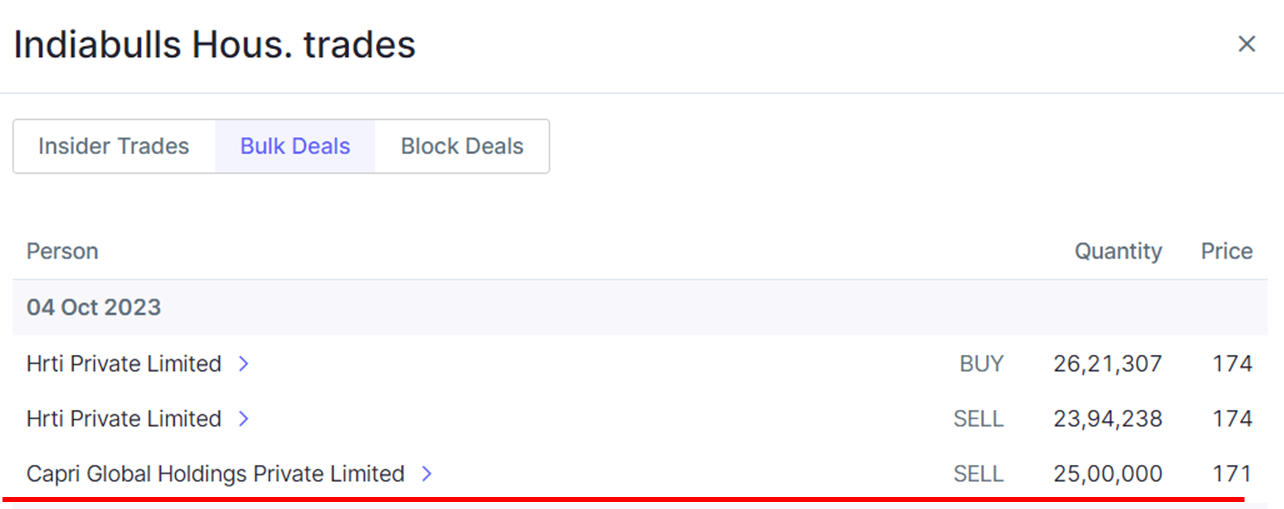

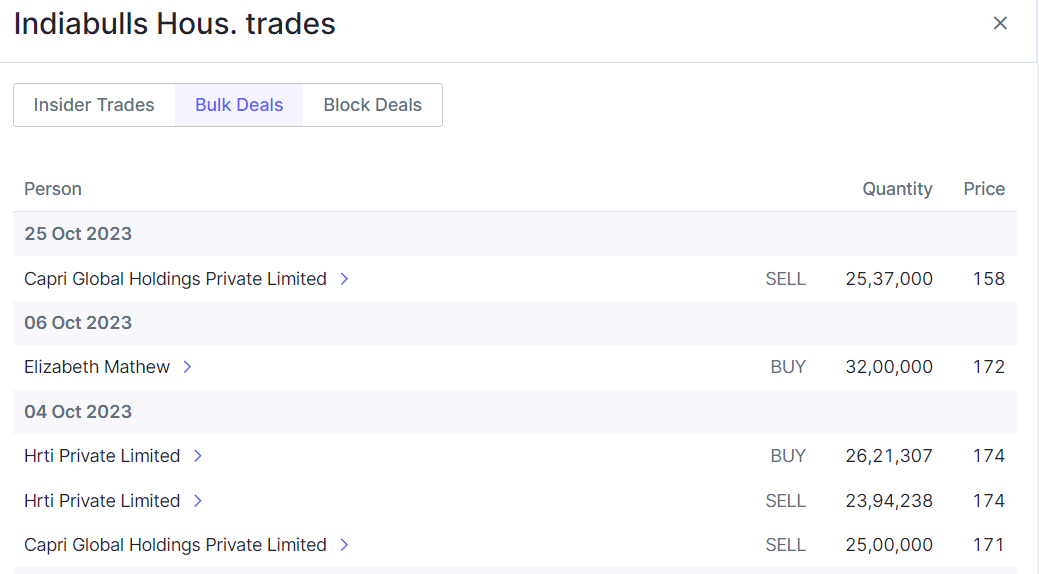

Is it possible that Capri would have shorted Indiabulls in F&O and selling in cash to create pressure?

3 Likes

For past 2-3 days, there has been continuous insider selling. Many senior management names like Ramnath Shenoy (Head Investor relation & analytics), Ashwin Mallick (Head Treasury) & Naveen Uppal (Chief risk officer) have sold their shares in the range of 50k-1 lac shares at 185-190/- price range ?

what can be the reason , is it bull trap ?

Why ESOP is being valued below book value ?

Is their possibility that new investor will liquidate existing share holders while acquiring ?

Please let me know your thoughts !

2 Likes

My view is that the personnel are liquidating the shares for creating cash which they can further use for subscribing to ESOP at more attractive prices. Same thing which happened with Gagan selling few weeks back.

I remain optimistic on the long term story and gap between BV and MP has to close if all other things remain same on macro level and if AUM start growing as per Gagan’s projections in concalls.

Views are biased as I am invested for long term story.

4 Likes

Let me try to answer your questions:

-

On ESOP exercise price: If you read enough about company - you will get idea that management tries its best to smooth out earning/quarter like taking provision/playing catch up when had unusal earning and taking profit from reserve if there is shortfall. To avoid any cost to PnL - company issued ESOP at market price so it will not have any impact on PnL as exercise price = market price. it also help to show less employee cost. Hope it gives you gist of the matter.

-

As employee eagerly waiting to encash their quasi salary so you can see seeing them selling share as soon as they get vested. I do not think except Gagan any employee selling their share to buy more ESOP (you can verify downloading report from BSE side (bulk deal for last 3 months - put filter on employee name so you can see what he acquired as part of ESOP and what he has sold). I have done this exercise last months come and it is visible that employees are selling as long as Gagan name does not appear in selling list, we should be okay. Thanks!

Disl. Holding it. May be biased.

2 Likes

Seems like RBI/AIF tightening has hit Indiabulls Housing also. My understanding of the industry dynamics is that builder financing transactions constitute a major portion of the evergreening trend. I could not find any AIF data in annual reports or investor presentations. Anyone has any thoughts if this AIF impact is overstated for Indiabulls? Where can we find AIF exposure data?

1 Like

The Recent Ratings Update clarifies the AIF exposure:

Further, investment by REs in the subordinated units of any AIF scheme with a ‘priority distribution model’ shall be subject to full deduction from the RE’s capital funds.

In this regard, ICRA notes that currently, Indiabulls Housing Finance Limited (IBHFL) has investments in such subordinated units of AIF, at a consolidated level, aggregating to about Rs. 1,000 crore. Accordingly, the company’s tier-1 capital is expected to contract by this amount.

The report is actually a good read for anyone looking to invest in the Company. The past problems and the current headwinds in Implementing the Co-lending model are also explained.

3 Likes

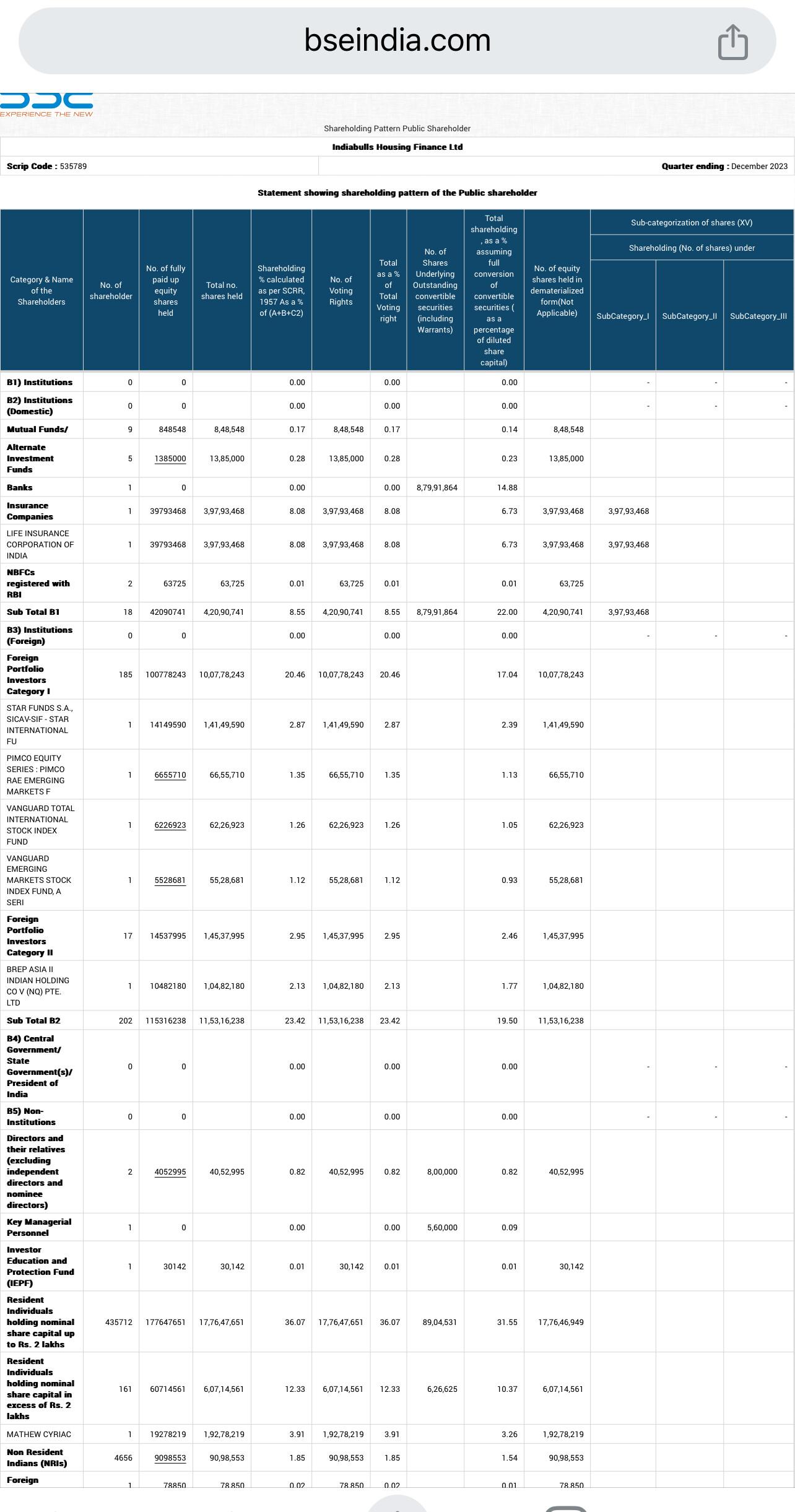

Mathew Cyriac raised his stake from 1% to 3.91% in this stock as per December Shareholding pattern update.

6 Likes

cf50ae2d-126c-493b-af6c-0225a36c11a7.pdf (331.6 KB)

Rights issue announced @150.

1 share for every 2 share held. Issue open dated 7/2/24 to 13/2/2024

Comments invited on below queries:

- My understanding 50 rupee with Rights application and 100 can be paid on demand in one year time. How will this impact the original share trading ?

- Will market adjust price post record date of 1st February considering 100 percent people subscribe?

- Any other points which we need to keep under consideration as I will be subscribing first time and have holdings with 3 brokers-Zerodha, HDFC and IIFL

Thanks

4 Likes

I’m baffled by this move! What’s the need for rights issue when they are already claiming to have excess liquidity on the balance sheet. Simultaneously, in 2023 AR they reported to raise 23k cr through NCDs and plan to raise remaining amount out of sanctioned 50k.

On the other hand, due to this move the book value per share will reduce from current 384 to 269. At the market price of 200 with additional 24.62 Cr shares the adjusted price should come to around 140, resulting in a P/B of 0.52

3 Likes

My best guess is that they need to provided for 1000 crs (from CARE rating report) for AIF as per RBI notification and if you consider 50 INR payment on application it comes around 1200 crs. Thanks!

May be you are right. But, this is a massive dilution of equity and does not conform with their statements in the q2 investor ppt where around slide 6 or 7 they are projecting that every quarter they have 1200 cr to 1800 cr excess cash. Alternatively, they could have met this requirement easily through bank loans.

I feel management has decided to reward old shareholders especially LIC and other FII which invested at 260 before.

Growth story in coming years is a given and equity addition supports company to leverage accordingly in coming years.

Also, i am not sure of this move for FCCB holders which have option of equity conversion in this year at 230. Anyone with more insights can advise.

1 Like

Will their stake not be diluted? Can you please explain how they are being rewarded?

In my opinion, At this stage growth capital is required in the company and exisiting investors are best aware .

Pardon me if my understanding is incorrect, but why come out with a rights issue at a price below book value per share? Doesn’t that destroy value for existing shareholders and reduce the book value per share?

1 Like