Why India cements? India Cements is the largest cement manufacturer in South India and is available at a market cap of 3500 crores Recently Ultratech cement bought over jaiprakash associates cement plan with a capacity of 22 mtpa for 16000 crores. India cements has a capacity of 15 mtpa , so the comparative valuation would be 10000 crores. Now if we remove the debt of India cements from this, the valuation would be 7000 crores which is a 100 % from here.This valuation is based on Private Market Value.

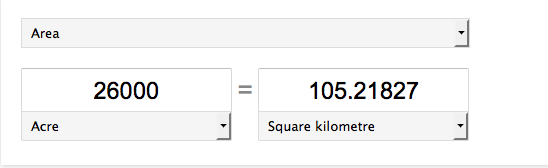

There are other assets that india cements which is not factored into this calculation like captive power plants, ships and 26000 acres of land.etc

However there are negatives associated with this stock that as below.

Increased competition in the cement sector

Credibility and integrity of the top management – IPL Scams and other political interest of the promoter

Highly dependent on the development of states like Andhra – if you see in 2009 as development stalled in Andhra due to political uncertainty it had significant India cements financials

Consolidation of companies in cement sector can increase competition

Profit margin is highly dependent on any other cyclical industry and freight charges has significant impact on pricing

Though this is not a stock that you would hold for long period of times due to its negative factors like cyclical stock, question over credibility of the management. However it seems to be available at a significant discount based on private market value and could be a value buy at current level.

Disc: Invested.

I believe Trinetra cement is also owned by this management. It is available at more attractive price and considerably cheaper. The company is improving it’s performance every quarter.

After Demonetisation and cyclone in Ap how do you people see to this stock, this is available at very cheaper as compared to other stocks in this sector.

Can any one share the valuation thesis of india cements.

They are reducing the debt and results are also good.

Going ahead how are we seeing this scrip.

Just had a glance - One very important factor is whether the company has created wealth for its shareholders in the past 10 years - Unfortunately thats negative . The total Retained earnings in the past 10 years is 2032 crores , however the increase in the market cap is negative . But this is one Factor , need to go through in detail .

My view is that India cements is a cyclical stock and looking at whether it created wealth over long term would not be appropriate. I invested when it was around Rs 70-80 range based on 2 reasons. I looked at the cement company acquisition that was happening and based on capacity my valuation for India cements was in the range of 6000- 8000 Crores roughly around 180 Rs per share. So there was enough margin of safety . The other reason i felt was the cement cycle was ending it down cycle.

It is always good to keep eye on great / well known investors to know where they are putting their hard earn money!!. However, blindly following them could end-up painful situation for retail investors!

Unless we know - (1) fundamental of the company (2) What prices they purchased (2) what is % of their wealth invested? (3) Are they part of promoter / friend or relatives ? (4) what is your risk taking capability (5) How long you are going to hold it ? and many more questions to answer before following /copying great investors !

There are many examples —one example many already burn their fingers in Rain Industries by following Monish Pabrai and many more names are there.

Which I am not able to guess as all the fundamentals are against India Cements. However, now the Damani is holding 2nd highest stock after the promoter i.e 20%.

Damani is a investors , trader and an entrepreneur as we all know.

Generally hni investors don’t come to far taking huge stake for a short term or trading.

Hence this is definitely for a long term or may be identified as take over opportunity.

As sebi ban promoters from trading for 6 months due to covid situation. So promoter of India cement also declared one public holding co. 5.85% as promoter co and raised holding up to 35% which will reflect in next quarter.

India cement has good presence in South , but now they have built one plant in North at the cost of 1400 crores.

Though, what’s your source of information as I am not able to find that Promoter has raised their stake . It would be quite a big positive for the stock.