DIsclosure : Recently bought this stock between 80 and 82 and it stands as ~10% of my equity portfolio.

This is a 50 year old company, which has transformed itself from manufacturing industrial meters to one of the top 5 transformer manufacturers in its class of products. Government to push for 24x7 power and upgradation of T&D network will boost demand for transformers.

Below is article from a blog :

IMP Powers Ltd (BSE 517571 / NSE INDLMETER) FV Rs 10 – CMP 84.00

IMP Powers Ltd (IMPPL) was incorporated in 1961, Growing from manufacturing Indistrial Meters, to India’s leading manufacturers of various types of Transformers, ranging from 1 MVA to 315 MVA, upto 400 kv Class with target of taking this production capacity upto 500 MVA., Today the company is amongst the Top 5 power transformer companies in India, in the 132 – 220 kv class.

IMPPL has well equipped Manufacturing Unit at Silvassa spread across 4 Acres, factory floor area for 1 Lakh Sq Ft Built up (Thus enjoying location advantage of close to National Highway and 3 Ports), for manufacturing the entire range of Transformers with an installed capacity of 12,000 MVA per annum, which is backed by in-house Design Center, R&D and own Impulse Testing facility upto 400 kva, which is accredited by NABL, (Department of Science & Technology, Government of India.)

The company is an approved Class ‘A’ supplier to all SEBs and other Government Agencies such as PGCIL, NTPC, NHPC & DVC. Non SEB customers include EPC companies, leading Consultants and other industrial players with whom IMPPL enjoys Preferred Vendors status.

IMPPL with a 5 decades of experience, has about 30,000 installations / Customer base which is spread across India and in about 26 countries across the world, catering the requirements of Utilities, SEB, PSUs and Private Industries. Some of the Clients are listed as below :

India : All SEBs (State Electrical Boards), State owned Transmission Companies, SAIL, PGCIL, ZESCO, Nepal Electricity Authority.

International : UK, African Continent, Asia and to the farthest corners and difficult terrains of Austrailia and New Zealand

EPCs : Godrej & Boyce Ltd, Jyoti Structures, KEC International, Larsen & Toubro, Kalpataru Power, UB Engg, IVRCL, Shreem

Corporates : Birla, Tata, Essar, Videocon, HPL Electric, Bajaj Electricals, Alstom, Crompton Greaves, ISOLUX, INABENSA, Siemens, Aditya Birla Group, Areva, Etc

Future Growth :

In India, the demand for equipment used in power sector is multiplying at a rapid rate because of social, economic and industrial development. The new government plans to fund up to 75% of the investment required to supply electricity through separate feeders for agricultural and rural domestic consumption, which will benefit the Power Sector Companies and ultimately boost the regional demand for power transformers. The government’s commitment to provide 24x7 uninterrupted power supply to all homes and Deendayal Upadhyaya Gram Jyoti Yojana to augment power supply to rural areas, strengthen the sub-transmission and distribution systems will ultimately boost the demand for Power Transformers.

IMPPL now also focuses on growing export market sales especially in Africa, Asia & Middle East, tying up with several International EPC players, which will improve its profitability owing to higher gross margin ranging from 25% to 30%.

Order Book : as on June 2015 stands as : 291 Crores, for 4821 MVA. 44% orders are from SEBs, while 21% from EPC Contractors, 31% is Deemed Exports and 3% Exports Orders Received.

While the installed capacity increased from 7000 MVA to 12000 MVA in last 5 years, Production increased from 4000 MVA to 7883 MVA, capacity utilization increased from 25% to 40% during this period, keeping immense scope for order intake and production capacity, with no spending on Capex.

Industry Outlook :

The Transformer market revenues in India are expected to grow at the CAGR of 14 % till 2018. Under the 12th five year plan (2012-2017), the government plans to spend 200 billion on developing and strengthening power infrastructure in India. The Indian government expects to add another 85,000 MW of power capacity during the 12th Five-Year Plan (2012-2017) period. The demand for power Transformers is also expected to go up as a direct consequence. Government’s attempt of attaining 100% electrification across the country by 2017 would contribute to the demand for power transformers. With the continuous support from the government to promote the power transformer industry through investments, tax benefits, subsidies, etc. will help the industry to grow over the coming years. With the upswing demand for reliable power in the country, the transformer market is witnessing a growth trend.

Triggers :

Company has idle plot of 20,000 Sq.Ft. at Kandivali west, the value of which should be not less than 60 Crores, if sold on outright basis, if develop & sold by the company, it can fetch a sale consideration anywhere between 80 to 100 Crore, depending on the project.

IMPPL is the only transformer company in India which is entitled for Sales Tax Exemption till 2017, such benefit will provide a significant price advantage to the company.

IMP Energy Ltd (IEL), a subsidiary company of IMPPL, incorporated in the year 2012, is acting as a Project Management Consultancy (PMC) to explore emerging opportunities in mini and small hydro power projects upto 25 MW. IEL received 13 small Hydro projects orders totaling 12.7 MW & amounting to Rs 137 Cr in Leh & Kargil, the progress of which is extremely encouraging. There may be value unlocking going forward, by listing this PMC subsidiary at rich valuations.

Falling in Input Prices of raw material such as Copper, Aluminium, Steel Stampings, Crude Oil (Transformer Oil), etc, will directly add to the bottom line of the company. Fall in interest rates will reduce the interest burden of the company.

The company has done CAPEX during tough times, the benefit of which will be seen going forward.

Valuations :

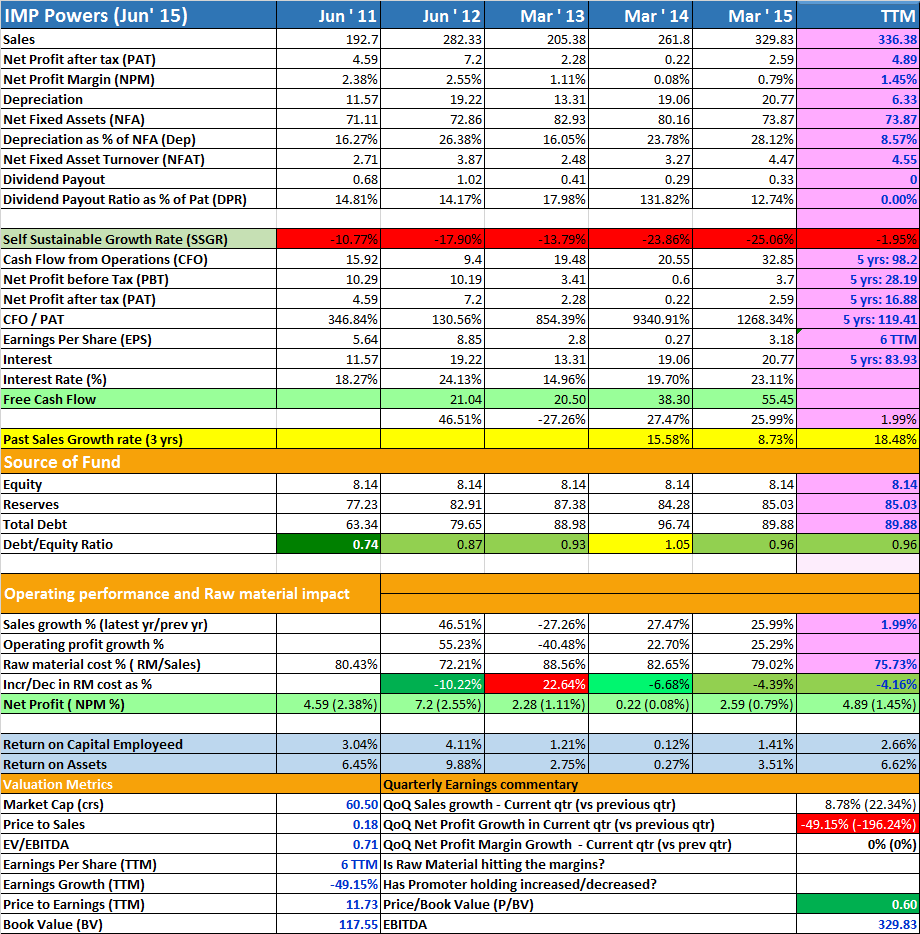

This Rs 10 paid up stock is trading at 0.8 times of book value of Rs 116.75 (Industry Price to Book Value 2.51), With FY 15 sales at 330 Cr and current Market Cap of only 70 Cr, its trading at Market Cap to Sales Ratio of ridiculously low of just 0.25 times. The company has turned around in last 3 quarters by making profit of Rs 6.43 Cr, giving EPS of Rs. 7.7 per share, making this stock so far the cheapest profit making company within the industry with a P/E of just 8.5 times (Industry PE of 68.63), if we add June 15 quarter EPS of 3, making this stock a great value pick among the high growth power sector with a modest target of 140 in the next 12 months.

Promoters recently allotted 500000 (5 Lakhs) shares to themselves at Rs 80 per share on Preferential basis, thus increase the stake in the company by a whopping 6% indirectly.

Thanks

Amit