Taken From there presentation:

1)IL&FS Transportation Networks Limited (ITNL) is a leading surface

transportation infrastructure company and the largest private sector BoT road

operator (in terms of lane kilometer) in India

2)ITNL has 14,680 lane km under its road assets portfolio comprising a mix of toll

& Annuity based projects

3)Has presence in other sub sectors viz. mass rapid transport system, urban

transportation infra system, car parking and border check post systems

4)ITNL’s International operations are primarily in the road segment and spread

across Spain, Portugal, Latin America, UAE and China

5)Operational portfolio of 9,439 lane kms of highways from 20 projects

Additional Points

1)They had a right issue recently at Rs 90 and raised around 800 crores

2)Managment is telling that there current protfolio will get completed by 2017 end (excluding srinagar sonmard tunnel project

3)Jorabat Shillong,Baleshwar Kharagpur Road and Thiruvananthapuram City Roads III should be completed by this quarter

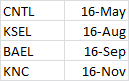

4)CNTL, Kiratpur Ner-Chowk, Barwa-Adda and Khed-Sinnar will be completed Next year

5)Managment projection is they will collect 12.75 crore daily after completion of all these project (currently they collect around 6.75 Crores daily)

6)Madhyapradesh border checkpost to be completed by Jan 2016 and Rapid Metro phase II by Dec 2016

Negatives

1)Huge debt and with every new project debt is increasing

2)Currently rapid metro phase I has a loss of around 120 Crores

3)Very Frequent Equity Dilution

4)Cost of debt is high (Averaging around 12.5%)

5)Sales Numbers are stagnant in last couple of years

Positives

1)Good Dividend yield

2)Managment guiding the profit will double after the whole current protfolio is completed by 2017

3)Good parentage (Some rumours of Piramal’s acquiring stake in parent company)

4)Sole bidder for Zojilla project for the last two times (project around 9000 Crores). They are execution two similar tunnel project currently

5)Expected to get a big project from nepal (Currently stuck in some court case)

6)Both the metro has lease of 99 years…

7)currently RBI have reduced interent by 125 basis points but banks have passed 30-40 basis points to them (interest burden is very high and can increase profitability drastically as interest rate are decreasing vice versa is a big risk to the story)

8)Managment and employees have shown confidence by increasing there stake via right issue

Disclosure : My second biggest holding in protfolio bought at a average of Rs 100

Useful Links

http://www.itnlindia.com/application/web_directory/Corporate%20Presentations/Analyst%20Presentation%20November%2006,%202015.pdf

http://www.itnlindia.com/invrelation.aspx?page_ID=21&Sec_ID=5

Added more on this news today. Companys fortunes will change. Even the disclosure on how they spent the money received from right issue is very encouraging and shows managment’s honesty a key factor to look out when investing in midcaps

Added more on this news today. Companys fortunes will change. Even the disclosure on how they spent the money received from right issue is very encouraging and shows managment’s honesty a key factor to look out when investing in midcaps