Established in 1996 as a subsidiary of the IIFL Group, IIFL Securities Limited is a comprehensive financial services provider, catering to both retail and institutional clients across India. The company specializes in retail and institutional equities, financial products distribution, commodity broking, currency broking, investment banking, financial planning, and wealth management services.

Key Offerings:

Retail Broking: Services include equities, commodities and currency broking, financial planning, depository participant services, distribution of mutual funds and bonds, portfolio management services (PMS), alternative investment funds (AIF), retirement planning, and estate planning.

Institutional Broking: Provides broking services, corporate access, and research support to institutional clients.

Investment Banking: Engages in activities such as Initial Public Offerings (IPOs), Qualified Institutional Placement, Rights Issues, Preferential Placement, Follow-on Public Offer, mergers and acquisitions, share buybacks, tender offers, and delisting. Additionally, the company offers advisory services.

Revenue Split (FY22):

Capital Market Activity: 81%

Insurance Broking: 4%

Facilities & Ancillary: 15%

Pan-India Presence:

IIFL Securities has a widespread presence, serving over 3.5 lakh active clients and reaching more than 2.4 million customers through a network of 2,500 points of contact across 500 cities in India.

Institutional Broking Franchise:

The company holds a prominent position in the industry with offices in Mumbai, New York, and London. It serves 770+ institutional clients, both domestic and foreign, covering a wide range of stocks, accounting for over 80% of India’s market capitalization.

Subsidiaries:

IIFL Securities Limited has five major subsidiaries, namely IIFL Facilities Services Limited, IIFL Insurance Brokers Limited, IIFL Management Services Limited, IIFL Capital Inc., and IIFL Wealth (UK) Limited.

Business Developments:

Entered the Alternative Investment Fund (AIF) business through subsidiary, launching two AIFs in listed and unlisted/startup spaces.

Achieved the top ranking in raising equity for private sector IPOs during the FY18-FY21 period.

Strategic Movements:

Sold a 5% stake in Livlong Protection and Wellness Solutions Ltd, a wholly-owned subsidiary, to Mr. Gaurav Dubey.

Acquired 1.1 million accounts of Karvy stock broking through a formal bidding process.

Established a tie-up with Karnataka Bank to introduce “KBLSmart Trade,” offering instant paperless account opening and a consolidated Demat and trading account feature.

Financial Highlights:

Conducted a buy-back of 1.7 crore equity shares on February 15, 2021, with an outlay of 105.7 Crores.

Reported investments totaling 227 crores as of March 2022, demonstrating a substantial increase from the 73 crores recorded in March 2021. These investments comprise various equity and debt instruments.

Invested in small quantity.

Need your help in analysing this stock is the good for long term hold?

The company and 5paisa (promoter group company) have a pending scheme of arrangement wherein IIFLSEC will transfer its online retail accounts to 5paisa in exchange for 1 share of 5paisa for every 50 shares held. Management has repeatedly said that they want to focus on high margin traditional brokerage business and not discount broking.

They have real estate properties which they are looking to sell. Management mentions this regularly in concalls.

My thesis is bullish on the entire brokerage industry. Rising tide (derivative volumes) will raise all boats. The sale of Sharekhan (similar in terms of market share) has given a benchmark valuation for an otherwise contracting market share business.

Cons are you don’t know what skeletons are in the closet of these legacy brokers. Recent SEBI action on IIFLSEC for activities in 2013-14 led to a sharp fall. SAT suspended the order though.

Yet another outstanding performance from IIFL Sec. It has grown in all segments: equities, MF, insurance, investment banking etc. Seems to be among the undervalued stocks stocks in the wealth management/broking sector

Anyone has any views on sustainability of these earnings?

This company has almost no products of its own- PMS, AIF, Mutual Funds, etc. Yet, it plans to transform its retail broking business into a wealth management practice by initially merely distributing 3rd party products. In fact, its retail broking business itself is flat in the face of competition from discount brokers like Upstox and Zerodha and full service brokers like Motilal Oswal, Geojit, etc.

…

How and why will a retail investor, who isn’t leaning towards IIFL Capital for basic broking services, now select IIFL Capital for its wealth management (an enhanced service)?

Why will an investor (regular as well as HNI, UHNI) select a wealth manager who is merely distributing 3rd party products instead of a wealth manager who has its own strategy, etc?

HNIs and UHNIs are a very small segment of retail category. There are more established wealth managers with their own in-house strategies, strong performance histories, etc. As for regular investors (non-HNIs), they are averse to onerous fee sharing of PMS, etc. They are more likely to burn their hands but not have a wealth manager, seek advice of their CAs, lean towards mutual funds, or probably select a well-known wealth manager if they decide to accept the high fee sharing. Even here, why would they select IIFL Capital?

Does anyone have insights on management strategies to address the above concerns?

..

I also feel that its investment banking business (IPOs, QIPs, etc) is really promising. The Company has already proven its merit in this category. Why is the management not focusing on becoming a market leader in investment banking itself? Any insights?

.. I think pivot in the right direction is crucial for its success- Option 1: Retail to wealth manager without in-house products OR Option 2: Gaining more market share in investment banking and becoming a market leader in this segment.

Within global investors, who are the target customer (E.g., salaried NRIs, businesses, etc) and key competitors? For salaried NRIs (who are migrated from middle class segment and just started getting affluent), there appears to be no major player who has captured the market. Is there a whitespace on this front? If yes, is the Company looking to attract this target? How does the Company plan to market itself and capture this space?

I think pivot in the right direction is crucial for its success- Option 1: Retail to wealth manager without in-house products OR Option 2: Retail to wealth manager with specific focus on Salaried NRIs (emerging from middle class in India and newly getting affluent abroad with little or no guidance on investing in India) OR Option 3: Gaining more market share in investment banking and becoming a market leader in this segment.

Regulatory risk. I.e: What is good for retail is not good for brokers. It is inevitable that brokers will face headwinds going forward from SEBI (which is a good thing in long term ) , Broking business can be cash cow, but might not be growth engine

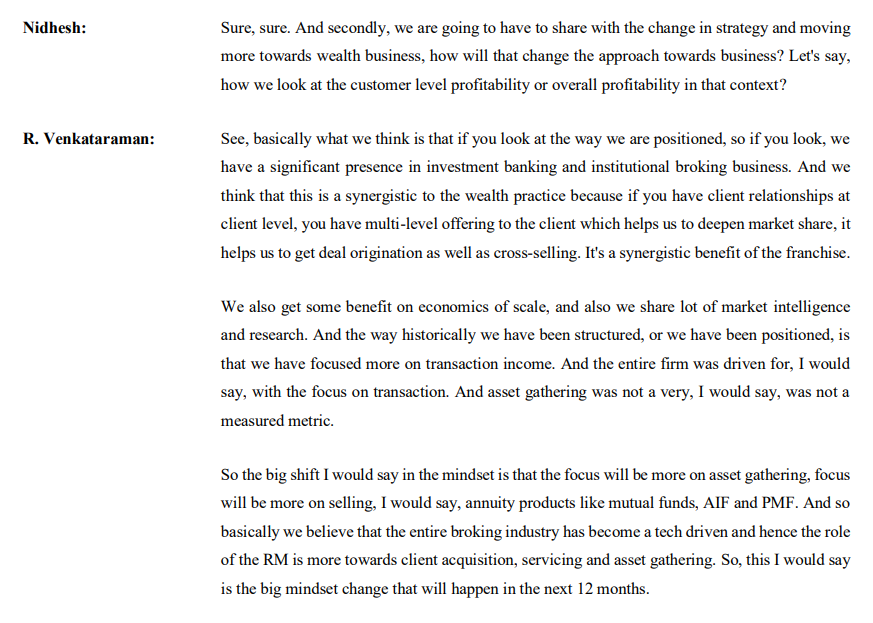

Investment thesis:

Transformation from securities business to weath management

Sections that are closely related to market cycality: i.e: Investment Banking - IPO listings , OFS

Moderately correalted with market cycles: i.e: block deals, research coverage for foreign funds, investor meetups etc.,

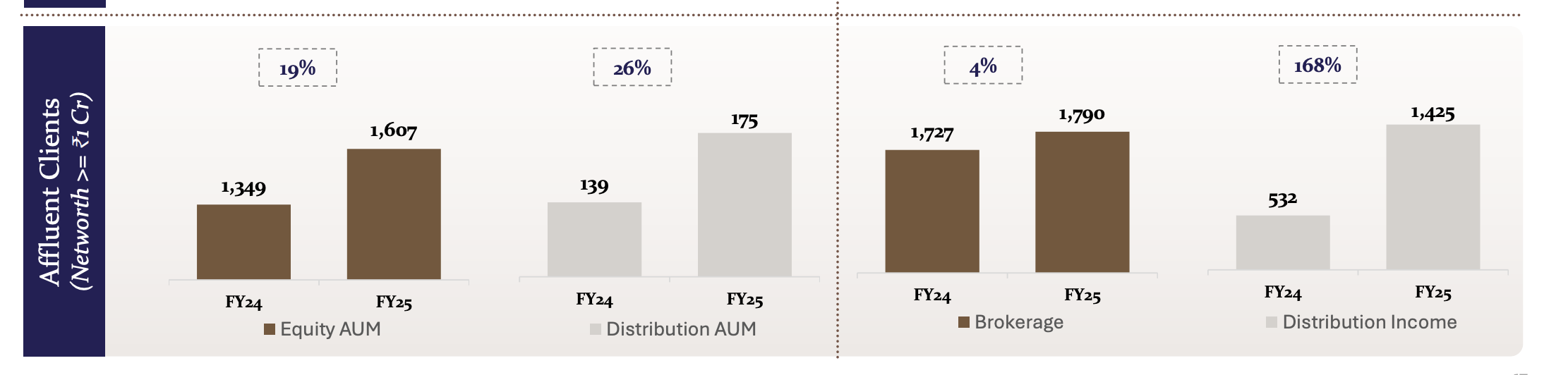

Secular play: India’s Financialisation i.e: Wealth Management for new age HNI(s) as well as old school investor(s)

For context India have roughly 80,000 HNI ($10M+) , which in itself is $800B TAM, which is expanding YOY, and the actual money is in this segment, not in the broking segment or MTF (I am treating them as optionality due to deeply cyclical nature tied to market booms)

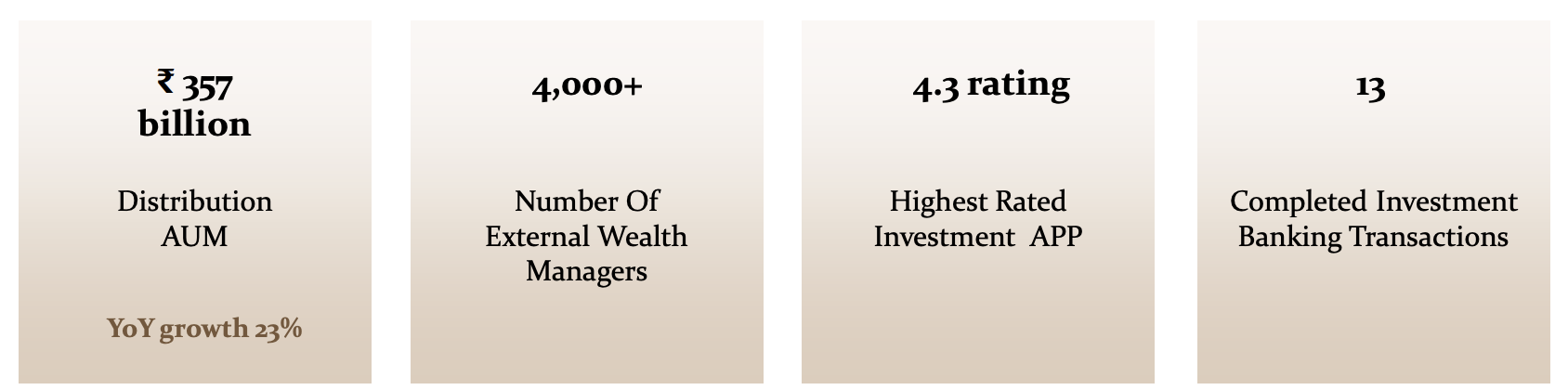

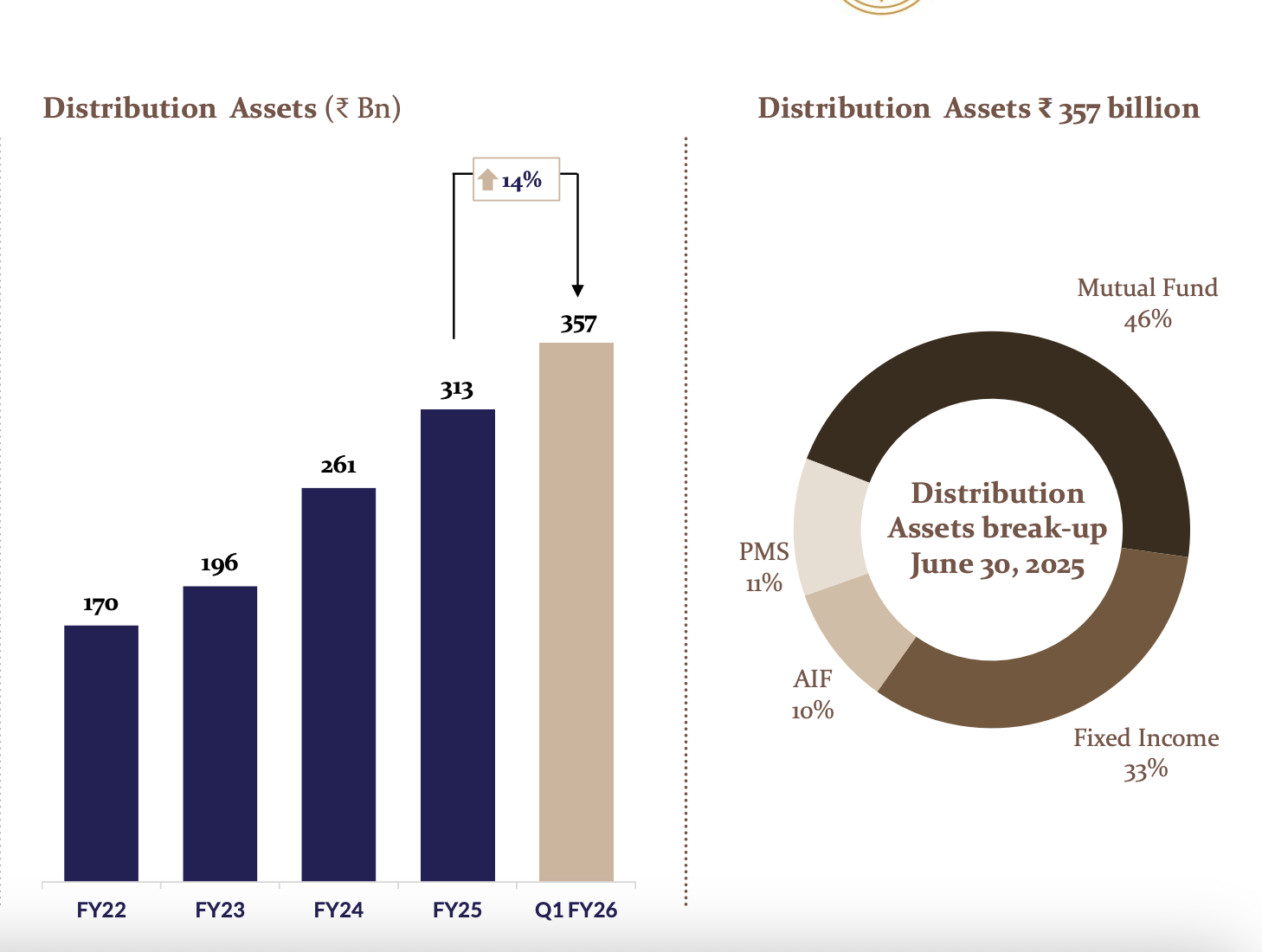

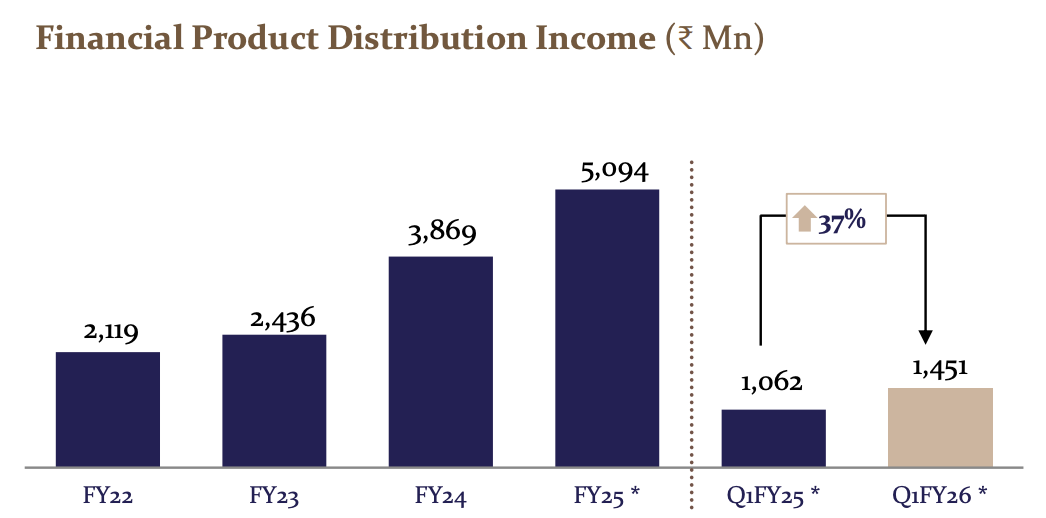

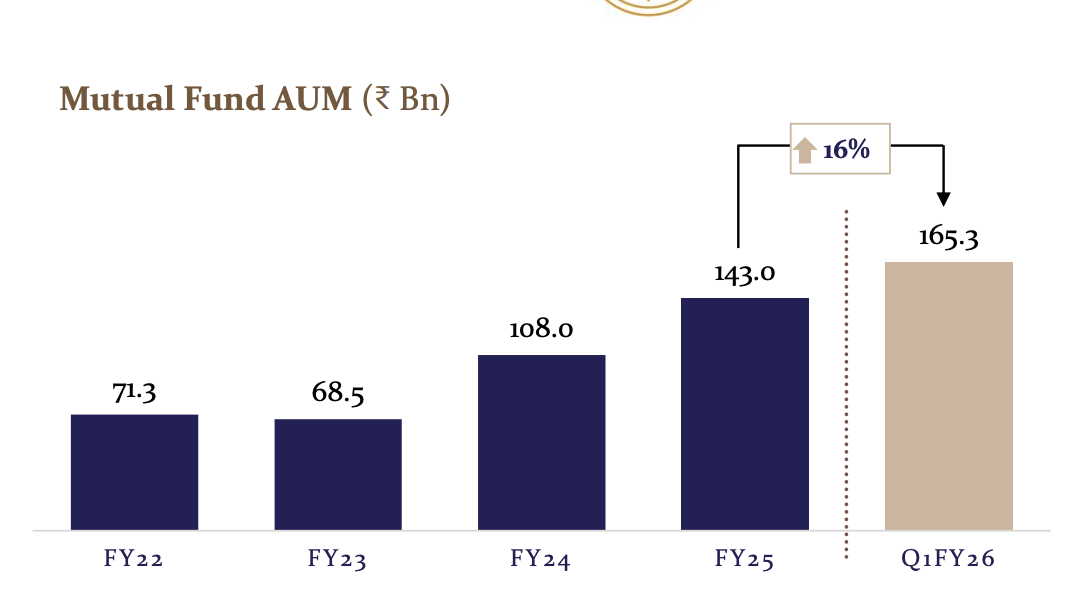

The above screenshot is where actual growth lies and the company needs to be tracked going forward

This is going to be highly competitve industry, however i believe they have right to win. Read The IIFL Capital Story (IIFLCAPS) , they have a few hidden moats in my opinion (Customer stickness, network effect, Brick n mortar offices in tier 2,3 cities, roughly 1700 touch points)