To me the rise in NPA it seems like mostly from restructured assets.

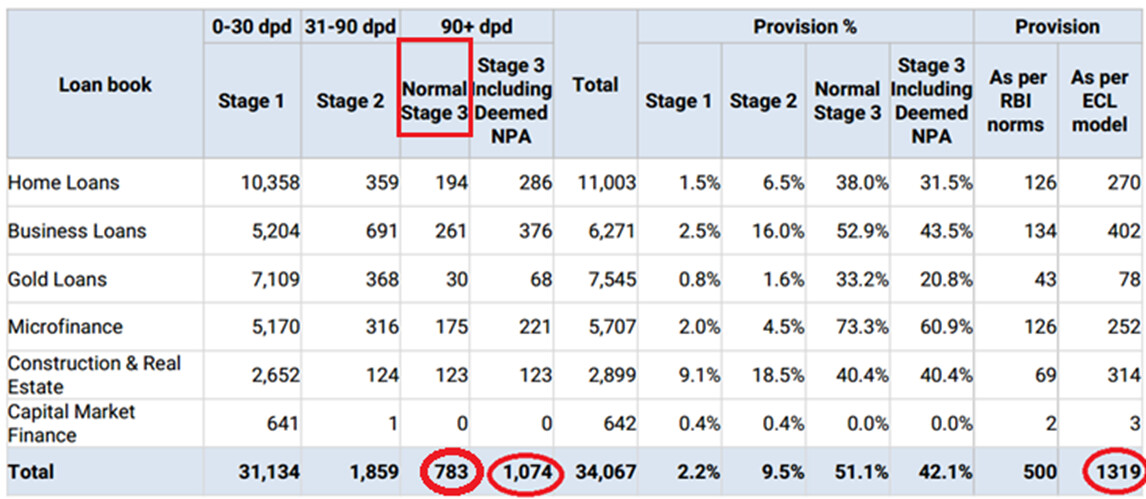

Lets take a look at the Stage 3 (90+ dpd) assets trend

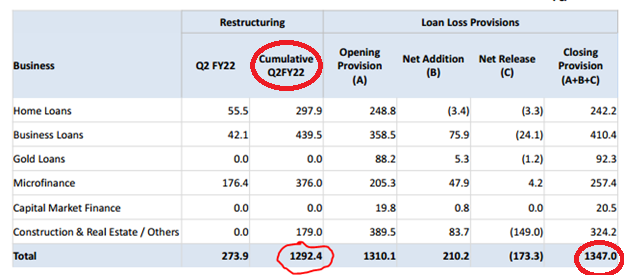

Q2FY22

Q3FY22

Q4FY22

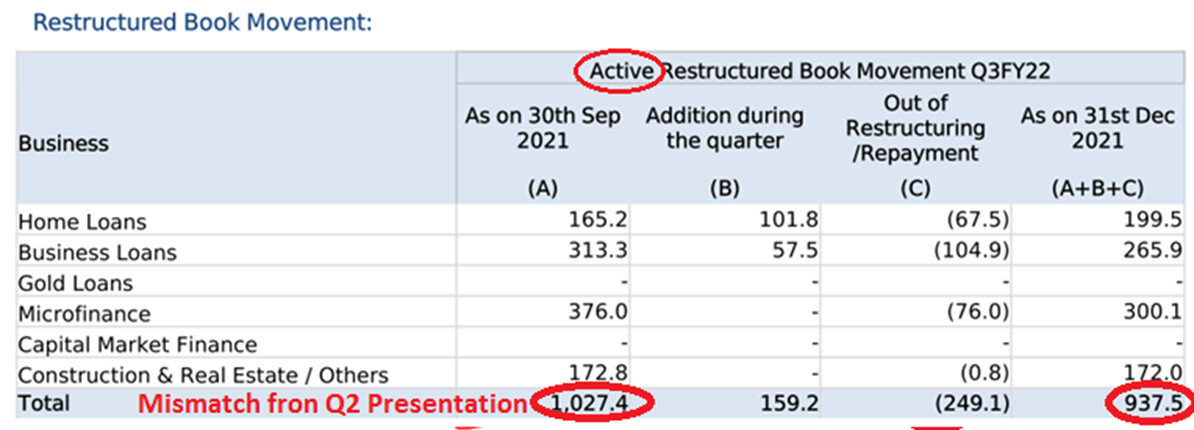

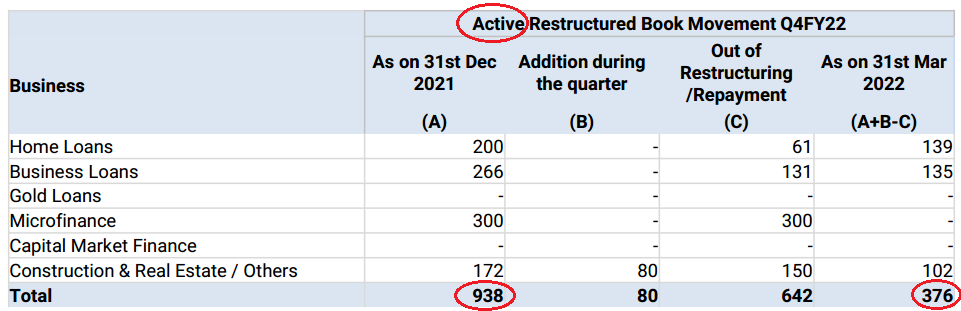

Now lets take a look at restructured loans trend.

Q2FY22

Q3FY22

Q4FY22

Please note that there is a mismatch between Q3 & Q2 restructured loan data. Maybe my understanding is wrong.

So the question is what is the source of this new Stage 3 assets or GNPAs. Whether it’s from the restructured loans or the loans disbursed after 2nd wave? If it’s from the restructured loans then it’s fine. Because as of now Restructured loan + Stage 3 = 1074 + 376 = 1500 cr and total provision is 1317 cr.

So this question needs to be asked in tomorrow’s concall.