Q3FY22 notes:

Takeaways from presentation:

-

IIFL Finance appoints former SBI Chairman Mr. Arun Kumar Purwar as Chairman

-

Added 6000 employees and opened 554 branches in 9MFY22

-

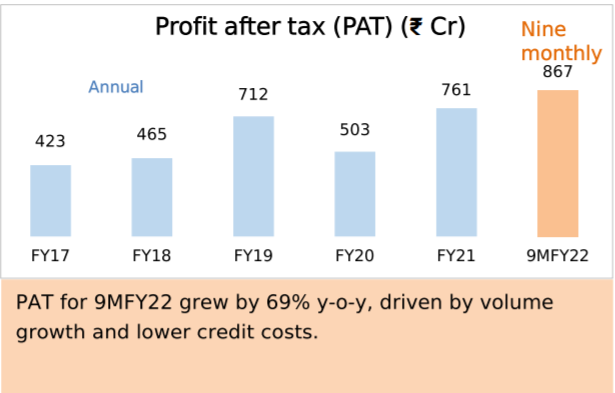

9MFY22 PAT at Rs.867cr where Annual PAT of FY21 was at Rs761

-

Provision coverage ratio at 133%.

-

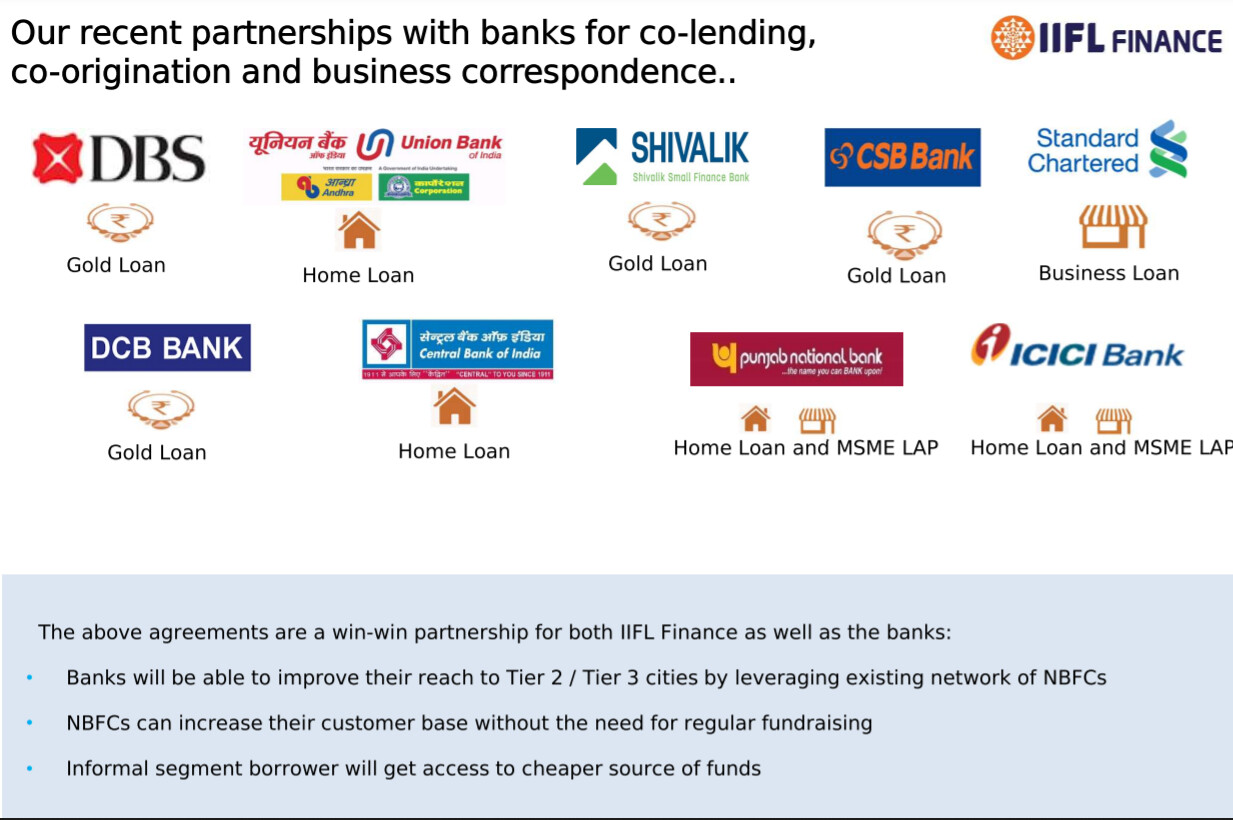

Co-lending

Concall notes:

- Bank credit growth in the economy at 9% YoY vs 5-6%

- Every quarter there is something which affects the numbers like this quarter was RBI notification.

- DIY loan: either from MyMoney app or WhatsApp.

- MSEME DIY loan grew 4 times

- 2 lakh average active users on the app for the month of December.

- 94% are retail in nature and 67% are PSL compliant. (Except gold loan) PSL complaints loan can help them sell these loan and raise long term money.

- Cost of borrowing declined by 27 basis points year on year to 8.7%

- GNPA: 2.8% NPA 1.5% (included impact of RBI notification of 12 Nov 2021)

- Impact of RBI Circular: 30 basis points.

- Disbursement in quarter is flattish because of pent up demand in Q1.

- YoY December was ATH in home loan last 1-1.5 years

- Growth guidance for next 12 months: around 25%

-

Average interest has got slight pressure: on portfolio there is 60 basis points decline.

- Incremental yield might have fallen by 1%

- Falling of yield is because of competitive pressure from banks

- But management says that this happens in this industry and they have witness this earlier.

- In gold loan you start with low interest rate and if the customer doesn’t pay on time then interest goes up over period of time.

- Some players have already withdrawn the low interest rate but the new stabilization of interest rate will be lower than previous standard.

- Home loans:

- 60-65% are salaried customers seeking home loans and first time home buyers. (Blue collared customers)

- Yields at 9-9.5%

- LTV at 75 to 78%

- Co-lending

- 850cr disbursement for co-lending with banks so far with home loans. (only 20% will be on company’s balance sheet)

- Half of the total disbursement of loan should be from co-lending model is their internal target

- Interest rate remains same in this model.

- Eg: Charging 10% interest to customer on Rs.100 that is Rs.10

- For that Rs.100 principal amount Rs.80 was provided by bank and if the deal with bank is set at 8% interest then Rs.6.4 (that is 8% of that 80% principal amount) will be paid to bank.

- Remaining Rs.1.6(that is extra 2% interest of that 80% principal amount) + Rs.2(10% of the Rs.20 principal amount which IIFL gave from its own books) will be retained by IIFL. Total Rs.3.6 earned out Rs.100 loan.

- Rs.1.6 will be shown as Assignment income and Rs.2 as interest income.

- But operating cost is on the IIFL books.

- Eg: Charging 10% interest to customer on Rs.100 that is Rs.10

- 850cr disbursement for co-lending with banks so far with home loans. (only 20% will be on company’s balance sheet)